Nationwide PPO Plans for Multi-State Coverage

Nationwide PPO plans give in-network access to doctors and hospitals across state lines, plus partial coverage for out-of-network care — coverage that travels with you instead of stopping at a state border. That makes them the natural fit for travelers, remote workers, snowbirds, and the self-employed, but the label “nationwide” hides an important catch: national availability is not the same as a national network. This guide explains how nationwide PPO plans work in 2026, the availability-versus-network distinction that decides whether coverage really follows you, who benefits most, the carriers that offer true national networks, and what nationwide health insurance plans cost. Because more than eight in ten marketplace plans are HMOs or EPOs, the broadest national PPO networks often sit off the exchange.

What Nationwide PPO Plans Cover

A nationwide PPO plan covers in-network care across state lines and pays a share of out-of-network care, with no referral to see a specialist. The reach usually comes from a national network such as Blue Cross Blue Shield’s BlueCard, which links independent Blue plans into near-nationwide in-network access. PPOs carry the highest premiums — a 2026 Silver PPO averages about $789 a month for a 31-to-45-year-old — because that multi-state flexibility and out-of-network coverage cost more.

- Multi-state in-network access. Routine and specialist care process as in-network in other states, not just emergencies.

- Out-of-network coverage. Care outside the network is still partially covered, at a higher cost share.

- No referrals. See specialists directly, in or out of network, in any state.

- Continuity when you move. A national network avoids switching plans when relocating or traveling for months.

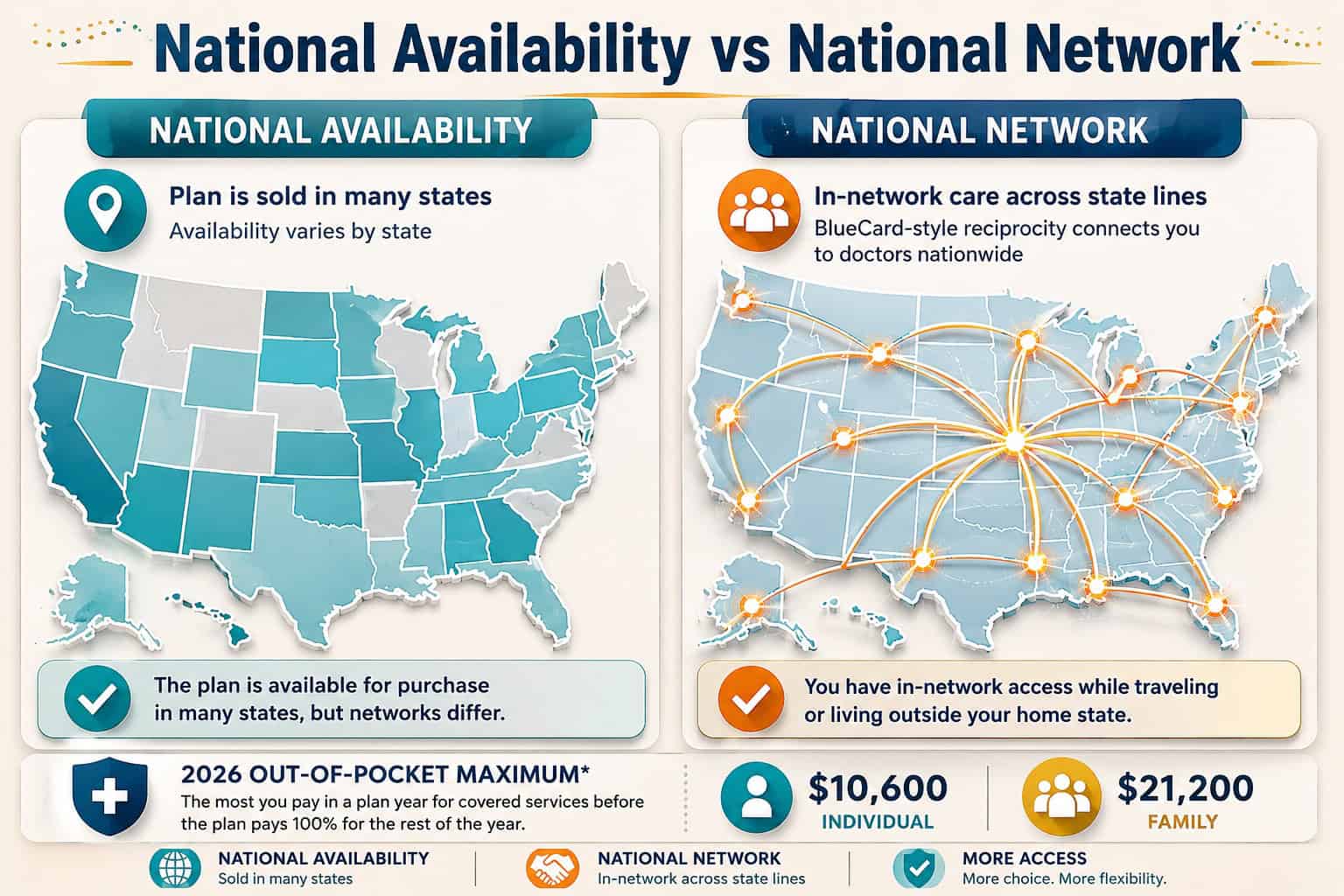

National Availability vs National Network

The most common nationwide PPO mistake is confusing national availability with a national network. National availability means a plan is sold in many states; a national network means you can use in-network providers across state lines. They are not the same — a plan can be widely sold yet still pay in-network benefits only in its home state. For coverage that follows you, the plan must use a national network such as BlueCard, not just a carrier that operates nationally.

This distinction is why some shoppers buy a “national” plan and still get billed out-of-network on a trip. A true nationwide PPO — typically a BlueCard-backed Blue plan or a large national carrier’s PPO — treats out-of-state in-network providers as in-network, which is the entire point of paying the PPO premium.

Who Needs a Nationwide PPO Plan

Nationwide PPO plans earn their higher premium for households whose care crosses state lines. The value is proportional to how much care happens away from home: someone who never leaves their metro rarely needs one, while a multi-state worker or snowbird may find it the difference between coverage that works and coverage that pauses for months. Four profiles capture most nationwide PPO buyers.

Top Carriers for Nationwide PPO Coverage

A few national carriers account for most true nationwide PPO coverage, and one program — BlueCard — defines the category. PPOs remain the most common employer plan, with 46 percent of covered workers enrolled in one in 2025, so these carriers maintain deep multi-state networks that individual buyers can reach, often off the exchange. Availability and plan design vary by state and ZIP code.

Blue Cross Blue Shield

BlueCard NationwideThe benchmark for nationwide PPO coverage. The BlueCard program links independent Blue plans into near-nationwide in-network reciprocity, so a Blue PPO bought in one state pays in-network benefits at participating Blue providers across the country — the strongest true national network for individuals.

UnitedHealthcare

Choice PlusOne of the largest national networks through its Choice Plus PPO design, with strong digital tools and nationwide pharmacy access. A practical option for domestic travelers and multi-state households; individual availability varies by market.

Cigna

National PPO / POSOffers traditional PPO and POS designs with multi-state networks and real out-of-network coverage. Premiums tend to run higher, but the national reach suits households that need care in more than one region.

Aetna

Select MarketsBroad national provider participation and CVS-integrated pharmacy where available. Aetna exited several individual marketplaces at the end of 2025 and is group-focused in some states, so individual nationwide PPO availability is limited and should be confirmed by ZIP code.

Every plan compared through ForHealthInsurance.com meets ACA compliance standards and includes the ten essential health benefits required under federal law. ForHealthInsurance.com is an independent brokerage, A+ rated by the Better Business Bureau, and verifies multi-state network reach without upselling or pressure.

Compare Nationwide PPO Plans in Your ZIP Code

Enter a ZIP code and date of birth to see nationwide PPO health insurance options on and off the exchange in about 60 seconds. Licensed agents can verify multi-state network reach at no extra charge.

Get a Quote Call 888-215-4045How Much Nationwide PPO Plans Cost in 2026

Nationwide PPO plans carry the highest premiums because they cover out-of-network care and broad multi-state networks. A 2026 Silver PPO averages about $789 per month for a 31-to-45-year-old, versus roughly $676 for an EPO, and PPO premiums typically run 15 to 30 percent above an HMO at the same metal tier. The 2026 out-of-pocket maximum is $10,600 for an individual and $21,200 for a family.

| 2026 Cost Benchmark | Figure | Source |

|---|---|---|

| Silver PPO average premium (age 31–45) | ~$789/month | CMS plan-data analysis |

| Silver EPO average premium (same age) | ~$676/month | CMS plan-data analysis |

| PPO premium over comparable HMO | ~15–30% higher | Carrier rate filings |

| 2026 out-of-pocket maximum | $10,600 individual / $21,200 family | HealthCare.gov |

| PPO share of employer plans | 46% of covered workers (2025) | KFF |

The 2026 out-of-pocket maximum is set by HealthCare.gov, and PPO enrollment share is tracked by KFF. For a nationwide PPO, weigh the higher premium against how often care happens out of state — the break-even is often a single avoided out-of-network bill on a trip.

How to Find a True Nationwide PPO Plan

Finding nationwide health insurance plans that genuinely travel takes four steps, and comparing both on-exchange and off-exchange options is what surfaces the widest national networks. Since more than eight in ten marketplace plans are HMOs or EPOs, a buyer who checks only the exchange may miss a national-network PPO. The process below starts in about 60 seconds and ends with licensed-agent verification at no extra cost.

- Enter ZIP code and date of birth to pull PPO plans on and off the exchange.

- Confirm a national network — look for BlueCard or an equivalent multi-state network, not just national availability.

- Verify providers in the states you use — check the directory for home, travel, and second-residence locations.

- Compare total cost — premium, deductible, out-of-network terms, and out-of-pocket maximum.

Related Guides

Compare the top-rated plans, self-employed coverage, plan-type differences, and a state-level PPO example.

The complete guide to PPO health insurance: how it works, costs, and coverage.

Best PPO PlansTop-rated individual PPO options and how to compare them for 2026.

Self-Employed Health InsuranceIndividual coverage for 1099 income and work across state lines, PPO included.

PPO vs HMO vs EPO vs POSA full side-by-side of the four managed-care plan types.

Frequently Asked Questions About Nationwide PPO Plans

What is a nationwide PPO plan?

A nationwide PPO plan is a Preferred Provider Organization plan whose network gives in-network access to doctors and hospitals across all or most states, plus partial coverage for out-of-network care. The defining feature is multi-state in-network reach — most often delivered through Blue Cross Blue Shield’s BlueCard program, which links independent Blue plans into near-nationwide reciprocity, so routine and specialist care process as in-network in another state.

What is the difference between national availability and a national network?

National availability means a plan is sold in many states; a national network means you can use in-network providers across state lines. They are not the same. A plan can be widely sold yet still pay in-network benefits only in its home state. For true nationwide PPO coverage, confirm the plan uses a national network such as BlueCard, not just that the carrier operates nationally.

Who needs a nationwide PPO plan?

Nationwide PPO plans fit people whose care crosses state lines: frequent travelers and remote workers, snowbirds who spend months in another state, families with college students out of state, the self-employed who work across markets, and anyone keeping an out-of-state specialist. For these households, a national network covers routine and specialist care that an HMO would treat as emergency-only outside the home state.

How much do nationwide PPO plans cost in 2026?

Nationwide PPO plans carry the highest premiums of the main plan types because they cover out-of-network care and broad multi-state networks. A 2026 Silver PPO averages roughly $789 per month for a 31-to-45-year-old, and PPO premiums typically run 15 to 30 percent above an HMO at the same metal tier. Final cost depends on age, ZIP code, tier, and whether the plan is bought on or off the exchange.

Are nationwide PPO plans available on the ACA marketplace?

Sometimes, but selection is limited — more than eight in ten marketplace plans are HMOs or EPOs. Many of the broadest nationwide PPO networks are sold off the exchange by national carriers, where availability does not depend on a single state’s marketplace. Comparing both channels surfaces the widest true nationwide PPO options for a given ZIP code.

Are nationwide PPO plans worth the higher premium?

For households whose care crosses state lines, often yes — the premium buys in-network coverage wherever they are, rather than emergency-only protection outside the home state. For someone whose care is entirely local and in-network, a lower-premium HMO or EPO usually delivers the same care for less. The value of a nationwide PPO is proportional to how much care happens away from home.

Find a Nationwide PPO Plan That Travels With You

Compare nationwide PPO health insurance plans on and off the exchange. ForHealthInsurance.com verifies multi-state network reach, checks your providers, and completes enrollment at no extra cost.

Get a Quote Call 888-215-4045Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving individuals and families nationwide. ForHealthInsurance.com is not affiliated with HealthCare.gov, the Centers for Medicare & Medicaid Services, or any insurance carrier. The agency helps you compare PPO plans and enroll in coverage that meets your needs at no extra cost to you.