Best PPO Health Insurance Plans for Individuals & Families

The best PPO health insurance plan is rarely the same for two households — it is the one whose network covers your doctors and the places you travel, with out-of-network terms and a premium that fit how often you actually use care. PPOs cost the most of the main plan types because they pay a share of out-of-network care, so “best” means getting that flexibility from a carrier with a broad, reliable network at a price that makes sense. This guide compares the best PPO health insurance plans for 2026: the top national carriers, what the best PPO insurance costs, the best PPO plans by buyer need, and exactly how to compare and choose. Because more than eight in ten marketplace plans are now HMOs or EPOs, the strongest PPO options often sit off the exchange — so comparing both channels matters.

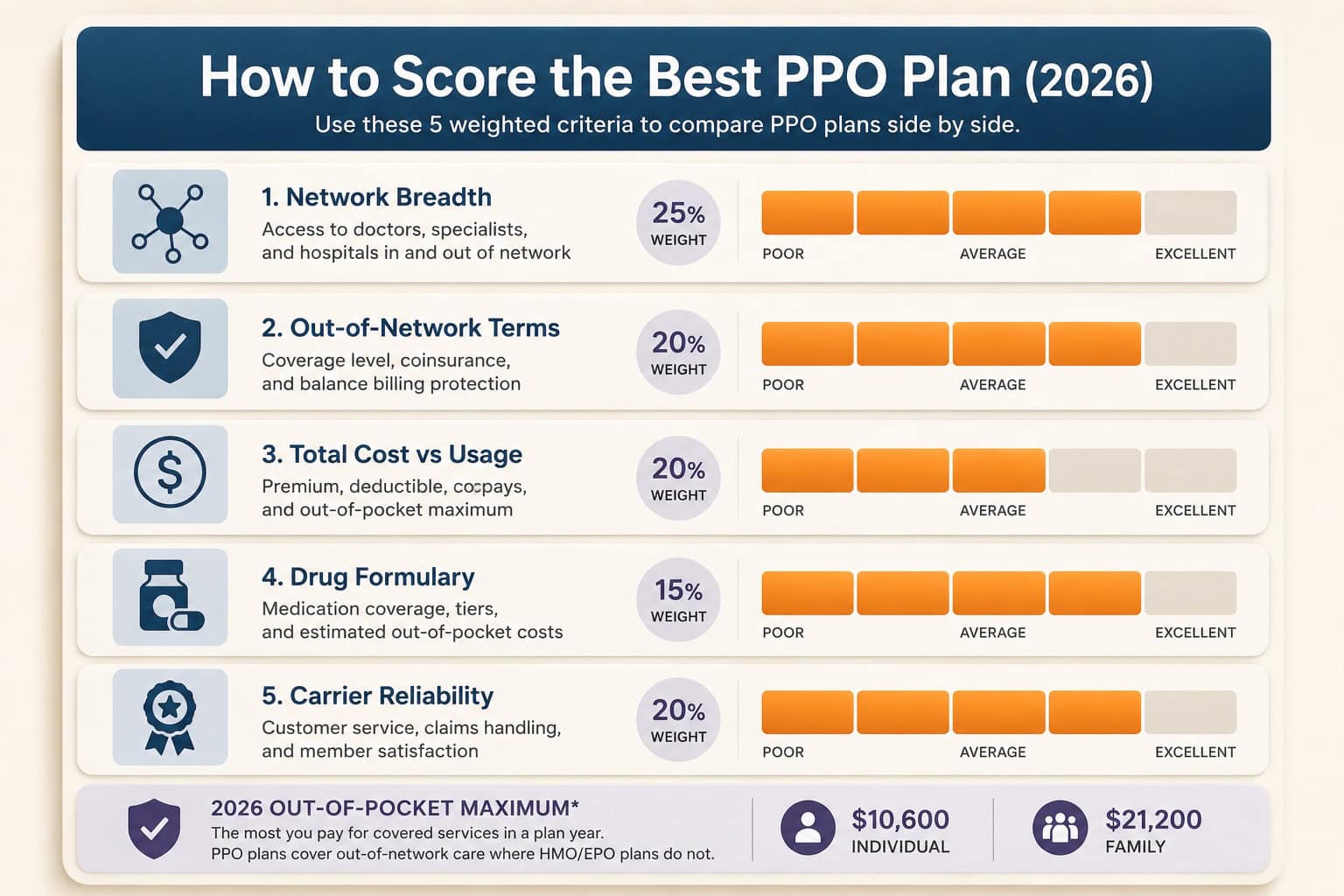

What Makes a PPO Health Insurance Plan the Best

The best PPO health insurance plan scores well on the factors that match how a household uses care: network breadth and whether your doctors are in network, out-of-network coinsurance, the in- and out-of-network deductibles, the out-of-pocket maximum ($10,600 for an individual in 2026), the drug formulary, and the carrier’s financial strength. The lowest premium is not automatically best — a higher premium can win if its network keeps more care in network.

- Network breadth. The single biggest factor — confirm your doctors, hospitals, and pharmacies are in network.

- Out-of-network terms. A true PPO pays a share out of network; check the coinsurance percentage and balance-billing exposure.

- Total cost, not just premium. Weigh premium against deductible, copays, and out-of-pocket maximum for your expected usage.

- Carrier reliability. Financial strength ratings and complaint records separate comparable-looking plans.

For a full overview of how PPO coverage works before comparing plans, see the PPO health insurance guide.

Best PPO Health Insurance Carriers in 2026

A handful of national carriers account for most of the best individual PPO options, each with a large multi-state network. PPOs remain the most common employer plan — 46 percent of covered workers were in a PPO in 2025 — so these carriers maintain deep PPO networks that individual buyers can reach off the exchange. Availability and plan design vary by state and ZIP code, so the best carrier in one market may not offer individual PPOs in another.

Blue Cross Blue Shield

Best for PortabilityThe BlueCard program links independent Blue plans into near-nationwide in-network access — the strongest option for multi-state households and frequent travelers. Individual PPO availability differs by state Blue plan, and some markets have shifted to HMO-only individual lineups.

UnitedHealthcare

Best for Network SizeOne of the largest national networks, with strong digital tools and pharmacy benefits — well suited to households that want the widest provider access and travel domestically. Individual PPO and PPO-style availability varies by market.

Cigna

Best for True PPO DesignOne of the carriers more likely to offer traditional PPO and POS designs to individual buyers. Premiums tend to run higher, but the out-of-network flexibility is real for households that need it.

Aetna

Select MarketsBroad provider participation and CVS-integrated pharmacy benefits where available. Aetna exited several individual marketplaces at the end of 2025 and is group-focused in some states, so individual PPO availability is limited and should be confirmed by ZIP code.

Every plan compared through ForHealthInsurance.com meets ACA compliance standards and includes the ten essential health benefits required under federal law. ForHealthInsurance.com is an independent brokerage, A+ rated by the Better Business Bureau, and quotes these carriers without upselling or pressure.

How Much the Best PPO Health Insurance Plans Cost in 2026

The best PPO plans carry the highest premiums of the main plan types because they cover out-of-network care. A 2026 Silver marketplace PPO averages about $789 per month for a 31-to-45-year-old, versus roughly $676 for an EPO — about $113 more for the added flexibility. The 2026 out-of-pocket maximum is $10,600 for an individual and $21,200 for a family, and the average in-network deductible sits just under $3,000.

| 2026 PPO Cost Benchmark | Figure | Source |

|---|---|---|

| Silver PPO average premium (age 31–45) | ~$789/month | CMS plan-data analysis |

| Silver EPO average premium (same age) | ~$676/month | CMS plan-data analysis |

| PPO premium over comparable EPO | ~$113/month | Derived |

| 2026 out-of-pocket maximum | $10,600 individual / $21,200 family | HealthCare.gov |

| Average in-network deductible | just under $3,000 | KFF |

| PPO share of employer plans | 46% of covered workers (2025) | KFF |

The figure that decides value is total annual cost, not the monthly premium alone. The 2026 out-of-pocket maximum is set by HealthCare.gov, and average deductibles and premium trends are tracked by KFF. A best-value PPO weighs the premium against the deductible, out-of-network coinsurance, specialist copays, and prescription tiers for the household’s expected usage.

Best PPO Plans by Need

Because the best PPO depends on the household, it helps to match plan traits to the situation. Travelers and multi-state workers prioritize network reach; the self-employed prioritize year-round enrollment and deductibility; families weigh deductible and pediatric access; and those managing chronic conditions value referral-free specialist and out-of-network access. The table maps common situations to the PPO traits that matter most.

| Situation | Prioritize | Best-Fit PPO Trait |

|---|---|---|

| Travel / multi-state | Nationwide network | BlueCard or national-carrier PPO |

| Self-employed / 1099 | Year-round enrollment, deductibility | Off-exchange PPO |

| Families / frequent care | Low deductible, pediatric access | Gold-tier PPO, broad network |

| Chronic condition / specialists | No referrals, out-of-network coverage | PPO with strong specialist network |

Compare the Best PPO Plans in Your ZIP Code

Enter a ZIP code and date of birth to see the best PPO health insurance options on and off the exchange in about 60 seconds. Licensed agents can compare networks and out-of-pocket costs at no extra charge.

Get a Quote Call 888-215-4045How to Compare and Choose the Best PPO Plan

Choosing the best PPO plan takes four steps, and comparing both on-exchange and off-exchange options is what surfaces the widest selection. Since more than eight in ten marketplace plans are HMOs or EPOs, a buyer who checks only the exchange may miss a national PPO that covers their ZIP code and providers. The process below starts in about 60 seconds and ends with licensed-agent help at no extra cost.

- Enter ZIP code and date of birth to pull available PPO plans on and off the exchange.

- Check your providers against each plan’s network — the deciding factor for “best.”

- Compare total cost — premium, deductible, out-of-network terms, and out-of-pocket maximum.

- Apply with licensed-agent support — no referral is required to enroll in a PPO.

What to Watch For in “Best PPO” Lists

Generic “best PPO” rankings can mislead because the best plan is local: a carrier rated highest nationally may not sell individual PPOs in a given ZIP code, or its network may exclude a key local hospital. Treat any ranking as a starting point, then verify against the household’s own providers and budget. Three traps account for most mismatches between a “top” plan and the right plan.

- National ranking, local gap. A top-rated carrier may not offer individual PPOs in every market — confirm availability by ZIP code.

- Premium-only comparisons. The cheapest “best” PPO can cost more overall once deductible and out-of-network coinsurance are counted.

- Network omissions. Verify specific doctors and hospitals are in network before trusting any best-of list.

Related Guides

Compare nationwide networks, self-employed coverage, plan-type differences, and a state-level PPO breakdown.

Multi-state national networks for travelers and remote workers.

Self-Employed Health InsuranceIndividual coverage for 1099 income and work across state lines, PPO included.

PPO vs HMO vs EPO vs POSA full side-by-side of the four managed-care plan types.

Texas PPO PlansA state-level example of PPO carriers and networks.

Frequently Asked Questions About the Best PPO Plans

What is the best PPO health insurance plan?

There is no single best PPO plan for everyone — the best PPO health insurance plan is the one whose network includes your doctors, covers the states you travel to, and balances premium against out-of-network terms for how often you use care. The strongest individual PPOs generally come from large national carriers with broad networks, and many are sold off the exchange where PPO selection is widest.

Which carriers offer the best PPO health insurance plans?

Blue Cross Blue Shield (through its near-nationwide BlueCard network), UnitedHealthcare, and Cigna offer some of the strongest individual PPO options, with Aetna available in select markets. Availability and plan design vary by state and ZIP code, so the best carrier for one household is not always the best for another.

How much do the best PPO health insurance plans cost in 2026?

A 2026 Silver-tier PPO on the marketplace averages roughly $789 per month for a 31-to-45-year-old based on CMS plan-data analysis, about $113 more than a comparable EPO. PPOs carry the highest premiums of the main plan types because they cover out-of-network care. Final cost depends on age, ZIP code, plan tier, tobacco use, and any premium tax credit eligibility.

Are the best PPO plans sold on or off the exchange?

Both. On-exchange PPOs qualify for premium tax credits but are limited in many counties, since more than eight in ten marketplace plans are HMOs or EPOs. Many of the broadest individual PPO networks are sold off the exchange by national carriers, which is why comparing both channels surfaces the best PPO option for a given ZIP code.

Is a PPO plan better than an HMO?

A PPO is more flexible — no referrals and partial out-of-network coverage — but costs more than an HMO. Whether it is better depends on need: households that travel, see multiple specialists, or want to keep specific out-of-network doctors usually get more value from a PPO, while those with all-local, in-network care often pay less under an HMO for the same care.

What should I look for in the best PPO plan?

Check network breadth and whether your providers are in network, the out-of-network coinsurance and whether balance billing applies, the in-network and out-of-network deductibles, the out-of-pocket maximum, the prescription drug formulary, and the carrier’s financial strength and complaint record. The best PPO plan scores well on the factors that match how the household actually uses care.

Find the Best PPO Plan for Your Needs

Compare the best PPO health insurance plans for individuals and families on and off the exchange. ForHealthInsurance.com runs the comparison, checks networks and out-of-pocket costs, and completes enrollment at no extra cost.

Get a Quote Call 888-215-4045Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving individuals and families nationwide. ForHealthInsurance.com is not affiliated with HealthCare.gov, the Centers for Medicare & Medicaid Services, or any insurance carrier. The agency helps you compare PPO plans and enroll in coverage that meets your needs at no extra cost to you.