Texas PPO Plans 2026: BCBSTX, Cigna & Aetna Compared

Texas PPO plans for 2026 are available off-exchange only — HealthCare.gov offers HMO and EPO plans for Texas residents but no individual PPO products. The five primary Texas PPO carriers are Blue Cross Blue Shield of Texas (BCBSTX), Cigna, Aetna, UnitedHealthcare, and Humana, with networks anchored at Memorial Hermann, Houston Methodist, Baylor Scott & White, Texas Health Resources, and HCA Healthcare facilities. Premiums for a 40-year-old run $510–$1,240 monthly depending on plan tier and rating area, with no referrals required for specialist care and out-of-network reimbursement included.

What brings you here today?

Why PPO Plans Are Different in Texas

Texas operates 26 geographic rating areas under HealthCare.gov — more than any other state — and the federal marketplace certifies only HMO and EPO plans for individual coverage in 2026. Residents who want a PPO from BCBSTX, Cigna, Aetna, UnitedHealthcare, or Humana must enroll off-exchange, forfeiting APTC eligibility but gaining broader networks and out-of-network coverage.

The off-exchange-only nature of Texas PPO plans is the single most important structural fact for any Texan shopping for one. Most residents in Harris County, Bexar County, and Dallas County assume HealthCare.gov is the default starting point for individual coverage — and for HMO and EPO plans from Ambetter and Molina, it is. But the federal exchange in Texas does not certify individual PPO plans from BCBSTX, Cigna, or UnitedHealthcare. This is partly a market choice by carriers, who price PPO premiums well above marketplace subsidy ceilings, and partly a consequence of how Texas operates under the federal exchange model rather than building its own state-based exchange like California or New York. The result is a clean bifurcation: HMO and EPO on HealthCare.gov, PPO off-exchange only.

Texas is also the largest state by uninsured population in the United States — roughly 5 million uninsured residents according to U.S. Census American Community Survey estimates, the highest uninsured rate of any state. PPO plans serve a specific slice of this market: residents who can afford premiums above the typical marketplace ceiling, value specialist access without referrals, travel frequently, or have providers at multiple Texas health systems. The Texas Department of Insurance (TDI) regulates PPO rate filings, network adequacy, and consumer complaints, with PPO-specific oversight requirements distinct from HMO regulation. Texas also has no state-level individual mandate penalty, unlike California, Massachusetts, New Jersey, Rhode Island, or Washington DC — meaning Texans who choose to go uninsured face only the federal $0 penalty, not a state surcharge on top.

The off-exchange PPO trade-off

Off-exchange Texas PPO plans cannot use Advanced Premium Tax Credits (APTC) or Cost-Sharing Reductions (CSR). A Texan earning $30,000 who would qualify for a $400/month APTC on a HealthCare.gov Silver HMO loses that subsidy if they buy an off-exchange PPO. For most subsidy-eligible Texans, the marketplace HMO or EPO is the financially better choice. PPO becomes the better option above ACA subsidy income ceilings (above 400% of federal poverty level) or when specific provider access or out-of-network coverage justifies the higher unsubsidized premium.

Texas PPO Health Insurance Carriers for 2026

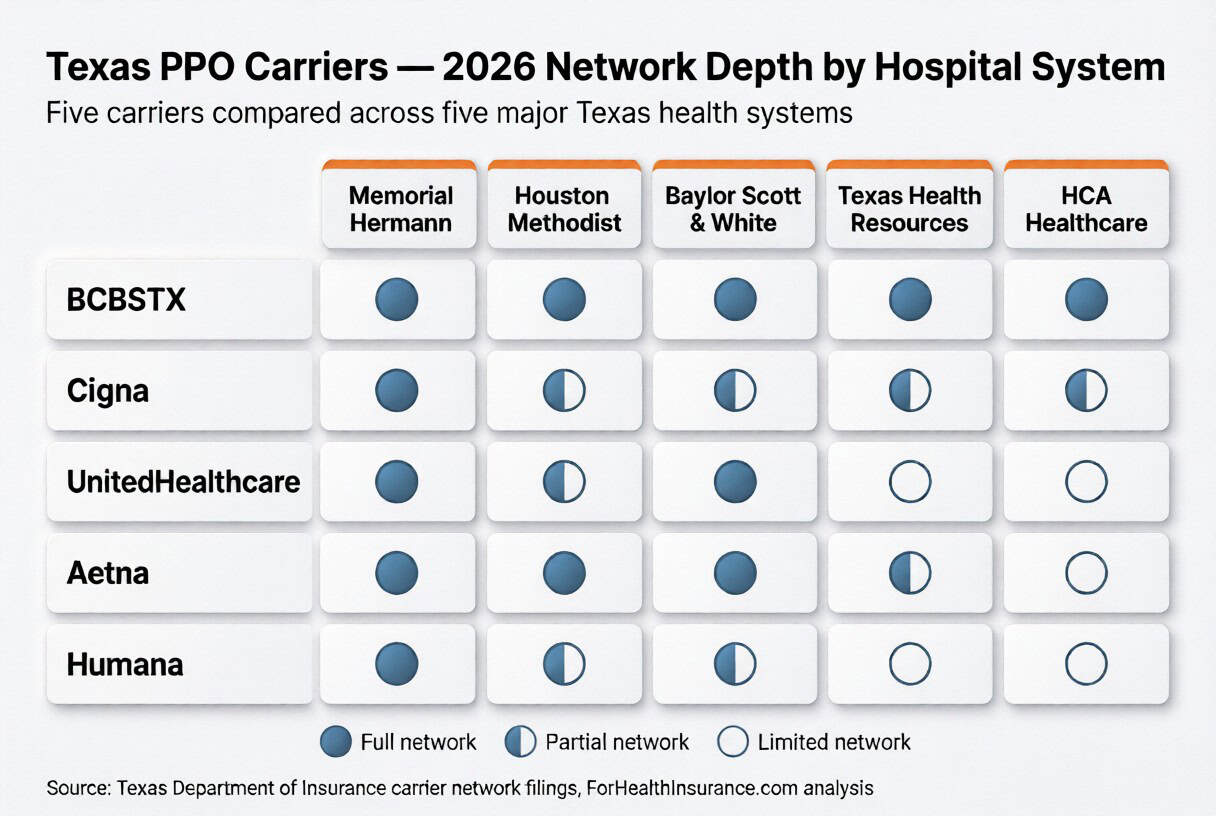

Four carriers offer individual Texas PPO plans in 2026: BCBSTX, Cigna, UnitedHealthcare of Texas, and Humana. Aetna exited the individual market at the end of 2025 and is now group-only. BCBSTX dominates through its parent HCSC with the broadest contracting across Memorial Hermann, Houston Methodist, Baylor Scott & White, Texas Health Resources, and HCA Healthcare. Cigna and UnitedHealthcare compete on national reciprocity.

Blue Cross Blue Shield of Texas (BCBSTX)

Statewide / DominantHCSC subsidiary and the largest Texas health insurer by enrollment. BCBSTX maintains deep PPO network contracting with virtually every major Texas health system — Memorial Hermann (Houston), Houston Methodist, Baylor Scott & White (Dallas/Austin), Texas Health Resources, HCA Healthcare Gulf Coast, and CHRISTUS Health. BCBSTX’s BlueCard reciprocity provides in-network access in all 50 states for Texans who travel. Strongest option for residents who want maximum statewide provider choice and national portability.

- HCSC parent (multi-state Blues)

- Largest statewide PPO network

- BlueCard national reciprocity

- Anchor at Memorial Hermann, Houston Methodist, Baylor Scott & White

Cigna

National / Metro TexasCigna’s Open Access Plus PPO is widely available across Houston, Dallas-Fort Worth, Austin, and San Antonio metros. Cigna contracts with most major Texas hospital systems but its network depth varies by metro — strongest in Houston and Dallas, thinner in West Texas and the Panhandle. Cigna’s strength is its national network and corporate small-group employer book, making it the carrier of choice for many Texas employers and self-employed professionals with multi-state operations.

- Open Access Plus PPO product

- Metro-anchored (HOU/DFW/AUS/SAT)

- Strong national reciprocity

- Small-group employer focus

UnitedHealthcare of Texas

National / Travel-friendlyUnitedHealthcare’s Choice Plus PPO offers strong national reciprocity and broad Texas metro coverage. UHC contracts with Memorial Hermann, Houston Methodist, Texas Health Resources, and HCA Gulf Coast facilities. UHC’s strength is national network depth — Texans who travel for work or split time between states (Texas-California, Texas-Colorado, Texas-Florida snowbirds) typically prefer UHC for the predictable in-network coverage outside Texas.

- Choice Plus PPO product

- Broad national network

- Strong travel/snowbird coverage

- Texas metro network at major systems

Aetna

Group Only — Exited Individual 2026Aetna exited the individual health insurance market in Texas entirely at the end of 2025. For 2026, Aetna PPO is available only through small-group and large-group employer channels — not for individual off-exchange enrollment. Aetna contracts with major Texas systems including Memorial Hermann and Houston Methodist, and offers competitive employer-sponsored PPO products especially in Houston and Dallas-Fort Worth. CVS Health’s acquisition of Aetna has integrated MinuteClinic access into network use for many Aetna PPO members.

- Employer-channel focus

- HOU and DFW network depth

- CVS/MinuteClinic integration

- Competitive group PPO pricing

Humana

Senior / Group hybridHumana’s Texas PPO footprint blends individual, small-group, and Medicare Advantage PPO products. For under-65 Texans, Humana’s individual PPO availability is narrower than BCBSTX or Cigna and concentrated in specific Texas metros. Humana’s stronger product line in Texas is Medicare Advantage PPO for residents aged 65+, with broad statewide network access and integrated wellness programs.

- Mixed individual/group/MA PPO

- Strongest in MA-PPO for 65+

- Narrower under-65 individual reach

- Texas metro concentration

CHRISTUS Health Plan & Scott & White Health Plan

Regional / SpecialtyTwo Texas-headquartered regional carriers with smaller PPO footprints. CHRISTUS Health Plan serves East and South Texas with PPO products anchored at CHRISTUS hospital facilities. Scott & White Health Plan (now part of Baylor Scott & White) offers PPO products in Central Texas around Temple, Killeen, and the Austin corridor. Both serve regional employers and self-employed professionals tied to specific Texas hospital systems.

- Texas-headquartered regional carriers

- Hospital-system-anchored networks

- Regional employer focus

- Narrower statewide reach

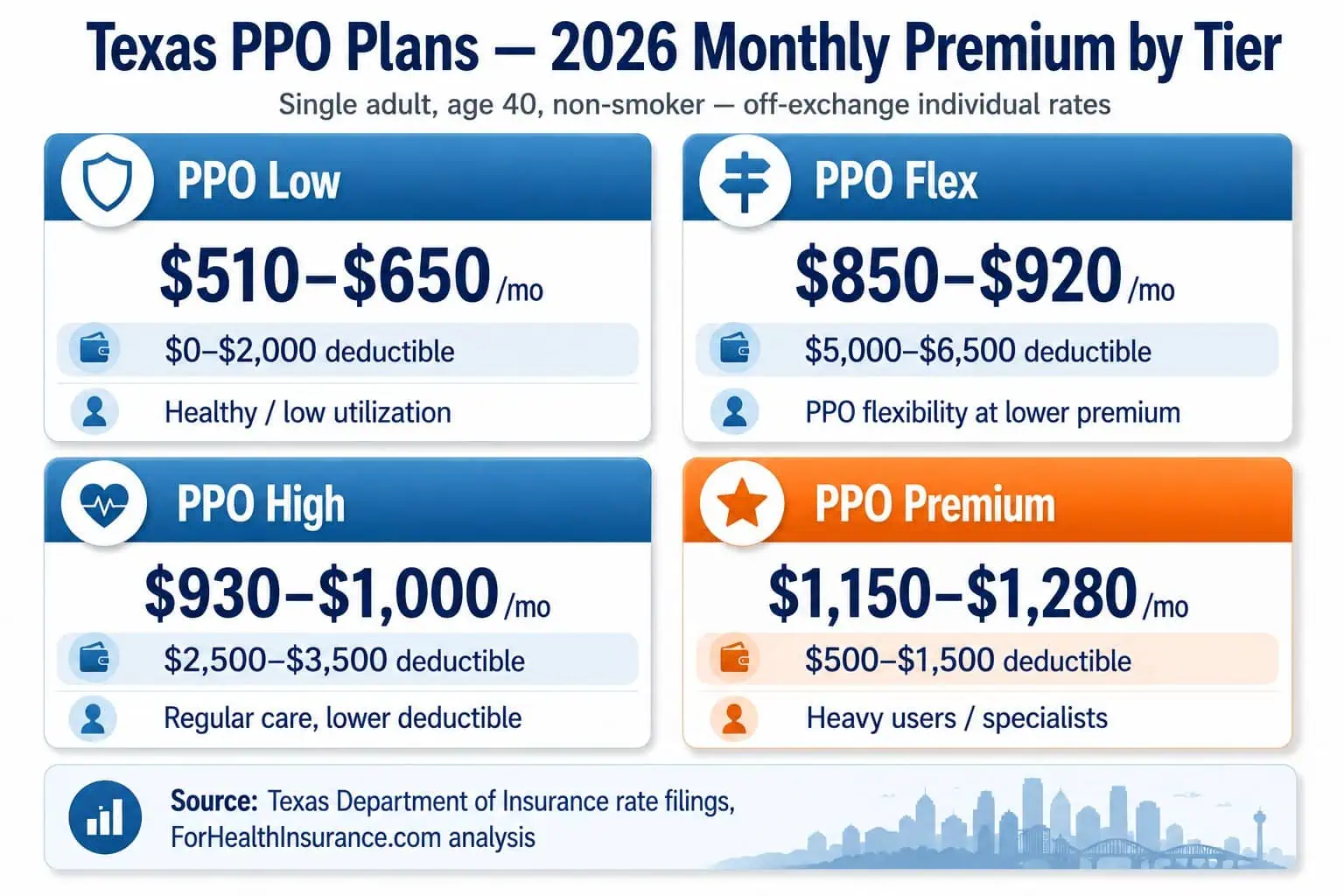

What a Texas PPO Costs in 2026

Texas PPO premiums for 2026 vary widely by rating area, plan tier, and carrier — Texas operates 26 separate geographic rating areas, more than most states. A 40-year-old non-smoker can expect monthly PPO premiums in the $510–$1,240 range, with mid-tier Flex and High PPO plans typically running $850–$960 per month. Houston, Dallas-Fort Worth, and Austin metro areas generally see lower PPO rates than rural West Texas or the Rio Grande Valley.

Texas’s 26 rating areas are unusually fragmented compared to states like Rhode Island (one rating area statewide) or California (19 rating areas across a much larger population). The Texas Department of Insurance organizes rating areas by groups of counties — The TDI organizes rating areas by county groups — Houston-area Harris and surrounding counties, the Dallas-Fort Worth metro, Austin-Travis County, and San Antonio-Bexar County each form separate rating area groups. Rural counties in West Texas, the Panhandle, and the Rio Grande Valley typically have higher PPO premiums due to thinner provider networks and higher claims experience. A 40-year-old buying a BCBSTX Blue Advantage PPO Silver plan in Houston might pay $580/month, while the same plan in Lubbock or Brownsville could run $720/month or more.

| Texas PPO Plan Tier | Typical Monthly Premium (single, age 40) | Deductible Range | Best Fit For |

|---|---|---|---|

| PPO Low / Basic | $510–$650 | $0–$2,000 | Healthy adults with low expected utilization |

| PPO Flex / Standard | $850–$920 | $5,000–$6,500 | Mid-utilization, want PPO flexibility at lower premium |

| PPO High / Enhanced | $930–$1,000 | $2,500–$3,500 | Regular care needs, prefer lower deductible |

| PPO Premium / Platinum | $1,150–$1,280 | $500–$1,500 | Heavy users, chronic conditions, specialist-intensive |

| Texas Small-Group PPO (per employee) | $480–$780 | $1,500–$5,000 | 2–50 employee Texas businesses |

The premium ranges above reflect off-exchange individual Texas PPO plans pricing — these are not subsidized rates. Texas residents who qualify for HealthCare.gov subsidies on Silver HMO or EPO plans almost always find those cheaper than equivalent off-exchange PPO coverage. For Texans above ACA subsidy ceilings (typically above $60,240 for a single adult or $124,800 for a family of four at 400% of federal poverty level in 2026), off-exchange Texas PPO plans become a serious comparison against subsidized marketplace alternatives. For broader nationwide PPO context across all 50 states, see the comprehensive PPO Health Insurance Plans hub for guidance that applies regardless of state.

Example: Fort Worth Software Consultant, Age 42

A 42-year-old self-employed software consultant in Tarrant County (Fort Worth metro) earning $95,000/year is above 400% FPL and receives no APTC subsidy on HealthCare.gov. A Silver EPO plan on the marketplace costs approximately $680/month at full price — no subsidy applies. A BCBSTX Blue Advantage PPO High plan in Tarrant County runs approximately $940/month, a $260/month gap. For that difference, she gains no-referral specialist access at Baylor Scott & White Medical Center in Fort Worth, out-of-network reimbursement at 70% of allowed charges when traveling to client sites in other states, and BlueCard reciprocity for nationwide in-network coverage. At $3,120/year in additional premium, the PPO break-even point is roughly one avoided out-of-network specialist bill — a calculation many above-subsidy Texans find worth it.

Get a Texas PPO Quote

A licensed Texas broker compares off-exchange PPO plans from BCBSTX, Cigna, Aetna, UnitedHealthcare, and Humana — with rating area pricing, hospital system verification, and provider-by-provider in-network confirmation. Free, no obligation.

PPO vs HMO vs EPO in Texas

Texas residents face a clear trade-off: HealthCare.gov offers Ambetter and Molina HMO plans with APTC subsidies — as low as $90/month for a 40-year-old earning $35,000 in Harris County — while off-exchange BCBSTX and Cigna PPO plans run $510–$1,280/month with no subsidy. The right choice depends on subsidy eligibility, whether specialist access at MD Anderson or Baylor Scott & White without referrals matters, and how often the household travels outside Texas.

| Feature | Texas PPO (off-exchange) | Texas HMO (on HealthCare.gov) | Texas EPO (on HealthCare.gov) |

|---|---|---|---|

| HealthCare.gov availability | No (off-exchange only) | Yes (with subsidies) | Yes (with subsidies) |

| Specialist referrals | Not required | Required from PCP | Not required |

| Out-of-network coverage | Yes (60–70% allowed) | No (emergency only) | No (emergency only) |

| National reciprocity | Strong (BCBSTX BlueCard, UHC, Cigna) | Texas-only network | Texas-only network |

| Typical monthly premium (age 40) | $510–$1,280 | $390–$680 (pre-subsidy) | $420–$720 (pre-subsidy) |

| APTC subsidy eligibility | No | Yes (138%–400% FPL) | Yes (138%–400% FPL) |

| Best fit for | Above-subsidy income, travelers, specialist users | Subsidy-eligible, single provider, low cost focus | Subsidy-eligible, want no-referral access |

The PPO premium gap above HMO and EPO products in Texas is partly structural and partly subsidy-driven. PPO carriers pay Texas hospital systems closer to billed rates than HMO and EPO networks, which negotiate aggressive volume discounts in exchange for narrow-network channeling. The out-of-network coverage component also adds claims risk that is priced into the PPO premium. The bigger factor for most Texas households, though, is the subsidy gap: a Texan earning $35,000 might pay $90/month for a subsidized HealthCare.gov Silver HMO and $880/month for an off-exchange Cigna PPO — a 10x cost difference driven almost entirely by APTC eligibility rather than the underlying actuarial value of the plans.

Who Should Choose a Texas PPO Plan

Texas PPO plans from BCBSTX, Cigna, and UnitedHealthcare suit four buyer profiles: Texans earning above $60,240 (single) or $124,800 (family of four) with no APTC subsidy; frequent travelers using BCBSTX BlueCard or UHC Choice Plus for nationwide coverage; residents managing specialist care at MD Anderson, Memorial Hermann, or Baylor Scott & White without referrals; and multi-state employees without employer group PPO. Most subsidy-eligible Texans will find HealthCare.gov HMO or EPO plans the better economic choice.

Above-subsidy income households

Texans earning above 400% of federal poverty level (roughly $60,240 single or $124,800 family of four in 2026) receive no APTC subsidy on HealthCare.gov plans — eliminating the cost gap that usually favors marketplace HMO and EPO. At full price, the $200–$400/month gap between marketplace and off-exchange narrows considerably, making PPO flexibility worth the premium difference for many higher-income households.

Frequent travelers and snowbirds

Texans who split time between Texas and another state, travel for work, or have providers across state lines benefit most from PPO national reciprocity. BCBSTX BlueCard, UnitedHealthcare Choice Plus, and Cigna Open Access Plus provide in-network access in all 50 states — meaning a Houston resident who winters in Florida or works remotely from Colorado doesn’t pay out-of-network rates at out-of-state providers.

Specialist-intensive care needs

Texans managing chronic conditions, ongoing specialist relationships, or complex care plans across multiple Texas hospital systems benefit from PPO no-referral specialist access. A patient at MD Anderson in Houston who also sees a rheumatologist at Baylor Scott & White in Dallas and an orthopedist at Memorial Hermann doesn’t need PCP referrals between visits, and can use out-of-network specialists at reduced reimbursement if needed.

Self-employed and 1099 contractors

Self-employed Texans, freelancers, and 1099 contractors often choose PPO for the flexibility — particularly those with W-2 spouses whose employer plans use PPO, allowing both household members to use the same provider networks. Self-employed Texans in higher-income brackets also lose ACA subsidy eligibility and pay full-price marketplace rates, which narrows the PPO premium gap considerably.

How to Buy a Texas PPO Plan (Off-Exchange Only)

Enrolling in a Texas PPO requires off-exchange application directly through BCBSTX, Cigna, Aetna, UnitedHealthcare, or Humana — HealthCare.gov does not certify individual PPO plans in Texas. The process verifies eligibility, rating area assignment across Texas’s 26 pricing regions, and provider network depth at target hospital systems. Off-exchange enrollment is available year-round with no open enrollment window.

Off-exchange Texas PPO enrollment runs on a calendar that’s more flexible than HealthCare.gov’s. Submit a completed application to BCBSTX, Cigna, or UnitedHealthcare by the 15th of any month and most carriers issue an effective date of the 1st of the following month — meaning a Tarrant County resident can switch from a marketplace HMO to a BCBSTX PPO mid-year without waiting for open enrollment, as long as the carrier accepts the application and there’s no qualifying coverage gap. Year-round availability is one of the structural advantages of off-exchange PPO over HealthCare.gov plans, which restrict mid-year enrollment to qualifying life events (marriage, divorce, birth, job loss, move).

The Texas Department of Insurance (TDI) regulates carrier rate filings, network adequacy, and consumer complaints — Texans can verify BCBSTX, Cigna, Aetna, and UnitedHealthcare financial ratings, complaint indices, and active license status through the TDI consumer portal. TDI publishes quarterly carrier complaint indices, a useful third-party benchmark when comparing BCBSTX’s statewide network footprint against Cigna’s metro-concentrated coverage. For households comparing on-exchange marketplace options, the federal HealthCare.gov portal is the official enrollment channel for HMO and EPO subsidized coverage, while PPO buyers go off-exchange through a broker.

Verify your providers before enrolling

The single most common Texas PPO enrollment mistake is assuming a specific doctor is in-network without verifying with the carrier directly. A doctor’s office may say they “accept BCBSTX” but only contract with certain BCBSTX network products — and not the specific PPO product you’re considering. Always confirm in-network status with the carrier’s provider directory and a phone call to the carrier (not just the doctor’s office) before enrolling. A 10-minute verification call prevents a $400+ out-of-network charge on the first office visit.

Frequently Asked Questions

Common questions about Texas PPO plans cover the HealthCare.gov availability question (no PPO on the federal exchange in Texas), which Texas carriers offer PPO products, 2026 premium ranges across Texas’s 26 rating areas, referral and out-of-network coverage rules, and why PPO premiums run 15–35% higher than equivalent HMO plans in the same metro.

Can I buy a Texas PPO plan on HealthCare.gov?

No. Texas does not operate a state-based exchange and uses the federal HealthCare.gov platform, but HealthCare.gov in Texas offers only HMO and EPO plans for individual coverage in 2026 — not PPO. Texas residents who want a true PPO plan must enroll off-exchange, either directly through a carrier or through a licensed Texas broker. The trade-off: off-exchange enrollment forfeits eligibility for Advanced Premium Tax Credit (APTC) subsidies, which are only available for marketplace plans. Small-group employer PPO plans are still widely available off-exchange through BCBSTX, Cigna, Aetna, UnitedHealthcare, and Humana.

Which carriers offer PPO health insurance in Texas?

The primary carriers offering individual PPO plans in Texas for 2026 are Blue Cross Blue Shield of Texas (BCBSTX, a subsidiary of HCSC), Cigna, UnitedHealthcare of Texas, and Humana. Aetna exited the individual market entirely at the end of 2025 — they remain available for employer group PPO but not for individual off-exchange enrollment. BCBSTX maintains the largest statewide PPO network with deep contracting at Memorial Hermann, Houston Methodist, Baylor Scott & White, Texas Health Resources, and HCA Healthcare facilities. Cigna’s Open Access Plus PPO is widely available in the Houston, Dallas-Fort Worth, Austin, and San Antonio metros. UnitedHealthcare Choice Plus PPO carries strong national reciprocity for Texans who travel. Aetna and Humana also offer PPO products primarily through small-group employer channels.

How much does a Texas PPO plan cost in 2026?

Texas PPO premiums for 2026 vary significantly by rating area — Texas has 26 separate rating areas, one of the most fragmented systems in the country. A 40-year-old non-smoker can expect monthly PPO premiums in the $510–$1,240 range depending on plan tier, with mid-tier Flex/High PPO plans typically falling between $850 and $960 per month for a single adult. Family premiums range from $1,380 to $2,940 monthly. Houston, Dallas-Fort Worth, and Austin metro areas generally see lower PPO rates than rural West Texas or the Rio Grande Valley. Deductibles on Texas PPO plans range from $0 on premium tiers up to $6,000 on flex tiers.

Do I need a referral with a Texas PPO plan?

No. The defining feature of any PPO plan, including Texas PPO plans, is direct specialist access without a primary care physician referral. You can schedule with a cardiologist at Baylor Scott & White, an orthopedist at Memorial Hermann, or an oncologist at MD Anderson without going through a gatekeeper first. PPO plans also cover out-of-network providers at a reduced reimbursement rate — typically 60–70% of allowed charges versus 80–90% for in-network — meaning Texas PPO members can see any provider in the U.S., though in-network use minimizes cost. This contrasts with HMO and EPO plans sold on HealthCare.gov, which restrict coverage to network-only providers.

Why are Texas PPO plans more expensive than HMO plans?

Texas PPO plans cost 15–35% more than comparable HMO plans because PPO networks reimburse providers at higher rates and cover out-of-network care. PPO carriers negotiate looser contracts with Texas hospital systems — Memorial Hermann, Houston Methodist, Baylor Scott & White, Texas Health Resources — and pay those facilities closer to billed rates than HMO contracts do. The out-of-network coverage component adds risk to the carrier’s claims pool, which is priced into the premium. Texas residents who use a narrow set of in-network providers and don’t travel often may find an HMO or EPO plan adequate; those who value specialist access without referrals, frequent travel, or out-of-network flexibility typically choose PPO.

Compare 2026 Texas PPO Plans

A licensed Texas broker compares off-exchange PPO plans from BCBSTX, Cigna, Aetna, UnitedHealthcare, and Humana — with rating-area pricing for Houston, Dallas-Fort Worth, Austin, and San Antonio, plus provider verification at Memorial Hermann, Houston Methodist, Baylor Scott & White, and Texas Health Resources. Free, no obligation.

Free Texas PPO comparison — all five carriers in one call.

Explore Texas Coverage In Depth

Statewide overview of Texas health insurance — marketplace, Medicaid, and off-exchange options compared.

Texas Marketplace EnrollmentHealthCare.gov enrollment guide — APTC subsidies, open enrollment dates, and SEPs.

Individual Texas Health InsuranceIndividual plan options — marketplace, off-exchange PPO, and direct carrier enrollment.

Self-Employed Texas Health Insurance1099 contractors, freelancers, and sole proprietors — Texas-specific coverage paths.

Cheap Texas Health InsuranceLowest-cost Texas plans — subsidized Bronze and Silver, CHIP, and affordability by income tier.

Catastrophic Texas Health InsuranceLower-premium high-deductible coverage for Texans under 30 or with hardship exemptions.

Short-Term Texas Health InsuranceBridge coverage between employer plans, post-COBRA, and other transitional needs.

Private Texas Health InsuranceOff-exchange private coverage options for Texans above ACA subsidy thresholds.

Family Texas Health InsuranceFamily coverage strategies across PPO, HMO, and CHIP for Texas households.

Texas Retiree Health InsurancePre-Medicare bridge ages 55–64 — TRS-Care, ERS, APTC subsidies, COBRA vs marketplace.

Texas Small Business Health InsuranceGroup plans for 1–50 employees — PPO, HMO, SHOP, and ICHRA options compared.

National PPO Health Insurance PlansNationwide PPO guidance applying across all 50 states — carriers, networks, and rate structures.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Texas residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.