Illinois PPO Health Insurance 2026: BCBSIL & Statewide Plans

Illinois PPO health insurance options narrowed significantly for 2026. Only one on-exchange carrier — Blue Cross Blue Shield of Illinois — offers PPO plans through Get Covered Illinois, and BCBSIL is the only Illinois marketplace insurer offering all three plan types (HMO, POS, and PPO) under one roof. For Illinois residents who want network flexibility, no referral requirements, and partial out-of-network coverage, the choice is clearer than ever: BCBSIL PPO on-exchange, or off-exchange PPO from a national carrier without subsidy eligibility. This guide breaks down both paths.

What brings you here today?

I want to understand the BCBSIL network

All 102 counties — hospitals and specialists

See the network ↓What a PPO Plan Means in Illinois

A PPO — Preferred Provider Organization — is the most flexible network type sold on the Illinois marketplace. PPO plans let members see any in-network provider without a primary care referral, cover a percentage of out-of-network care, and apply nationwide network rules that make them well-suited to households who travel or who want to keep specific specialists. For Illinois shoppers comparing network types in 2026, understanding the practical differences between PPO, HMO, and POS is the first step.

| Feature | PPO | HMO | POS |

|---|---|---|---|

| Primary care referral required | No | Yes | Yes for out-of-network |

| Out-of-network coverage | Partial (separate deductible) | Emergency only | Partial with referral |

| Network breadth | Broadest | Narrowest | Moderate |

| Typical premium tier | Highest | Lowest | Middle |

| Best for | Travelers, specialist preference | Cost-conscious, local care | Middle ground |

The freedom-to-choose flexibility is what most PPO members value. A patient with a long-term cardiologist, oncologist, or orthopedist outside the typical HMO network can keep that specialist in-network or covered partially out-of-network with a PPO. Households that split time between Illinois and another state — common for retirees, business travelers, and families with college students — benefit from PPO’s nationwide network rules where HMOs would treat out-of-state care as emergency-only.

Illinois PPO Plan Availability for 2026

The Illinois PPO market is more concentrated in 2026 than in any year since the ACA marketplace launched. Blue Cross Blue Shield of Illinois, operated by Health Care Service Corporation, is the only on-exchange carrier offering PPO plans through Get Covered Illinois for 2026. The other six on-exchange carriers — Cigna, Ambetter, Molina, Oscar, UnitedHealthcare, and MercyCare — offer HMOs only, with limited POS variants from some.

This concentration reflects two market forces. First, the 2025 carrier exodus removed four insurers from the Illinois market entirely (Aetna CVS, Aetna Life, Health Alliance, and Quartz), and none of the exited carriers had been major on-exchange PPO providers. Second, HCSC’s network depth across Illinois — all 102 counties — makes BCBSIL the only insurer with the provider relationships needed to sustain a broad-network PPO product profitably. The Illinois Department of Insurance 2026 plan analysis confirms BCBSIL as the sole on-exchange PPO carrier this year.

Looking for a national PPO option?

For broader background on PPO plan structures, network features, and how PPO compares across states, see the national PPO health insurance hub. Illinois residents who want PPO coverage and do not qualify for premium tax credits can also shop off-exchange products from national carriers.

Off-exchange PPO options remain available from select national carriers for residents who do not qualify for premium tax credits and prefer broader provider networks. Off-exchange plans forfeit APTC eligibility entirely — making them appropriate only for households above 400 percent of FPL where subsidy access is limited or absent. For most Illinois residents, the on-exchange BCBSIL PPO with subsidies is the better economic choice even when an off-exchange alternative offers marginally broader networks.

BCBSIL PPO Network in Illinois

The BCBSIL PPO network reaches all 102 Illinois counties and includes most major hospital systems statewide. For Chicago-area residents, that means Northwestern Memorial, Rush University Medical Center, UChicago Medicine, and the Advocate Health Care system — including Lurie Children’s for pediatric care. Downstate, BCBSIL PPO includes OSF HealthCare, Memorial Health (Springfield), Carle Health (Champaign-Urbana), and most Mercyhealth System hospitals in northern Illinois.

Chicago Metro

Strongest NetworkNorthwestern Medicine, Rush, UChicago Medicine, Advocate Health Care, Lurie Children’s, NorthShore. PPO members in Cook, DuPage, Lake, Kane, and Will counties have in-network access to virtually every major Chicago-area hospital system and the affiliated specialist networks.

Central Illinois

OSF + MemorialOSF HealthCare network covers Peoria, Bloomington-Normal, and the Quad Cities region. Memorial Health is the dominant Springfield-area system. BCBSIL PPO includes both in-network for residents in Peoria, McLean, Sangamon, and surrounding counties.

Champaign-Urbana

Carle HealthCarle Health is the primary system in east-central Illinois — Champaign, Urbana, and Danville. BCBSIL PPO members have in-network access to Carle Foundation Hospital, Carle Hoopeston Regional Health Center, and the broader Carle Physician Group network for specialist care.

Northern Illinois

Mercyhealth + BeloitRockford, Belvidere, and surrounding northern Illinois counties have in-network BCBSIL PPO access to Mercyhealth System hospitals and clinics. The network bridges across the Wisconsin border to Beloit-area facilities for residents living in Illinois but using providers in the broader Stateline region.

Plan-level network participation can vary within the BCBSIL portfolio. Some BCBSIL PPO products use the broader Blue Choice PPO network; others use a narrower Blue Cross PPO variant. Members should verify their specific 2026 plan name and network designation at the BCBSIL provider directory or by calling the doctor’s office directly. Directories occasionally lag actual contract changes by weeks, so calling the office is the most reliable check before locking in a plan choice.

PPO vs HMO Cost Tradeoff in Illinois

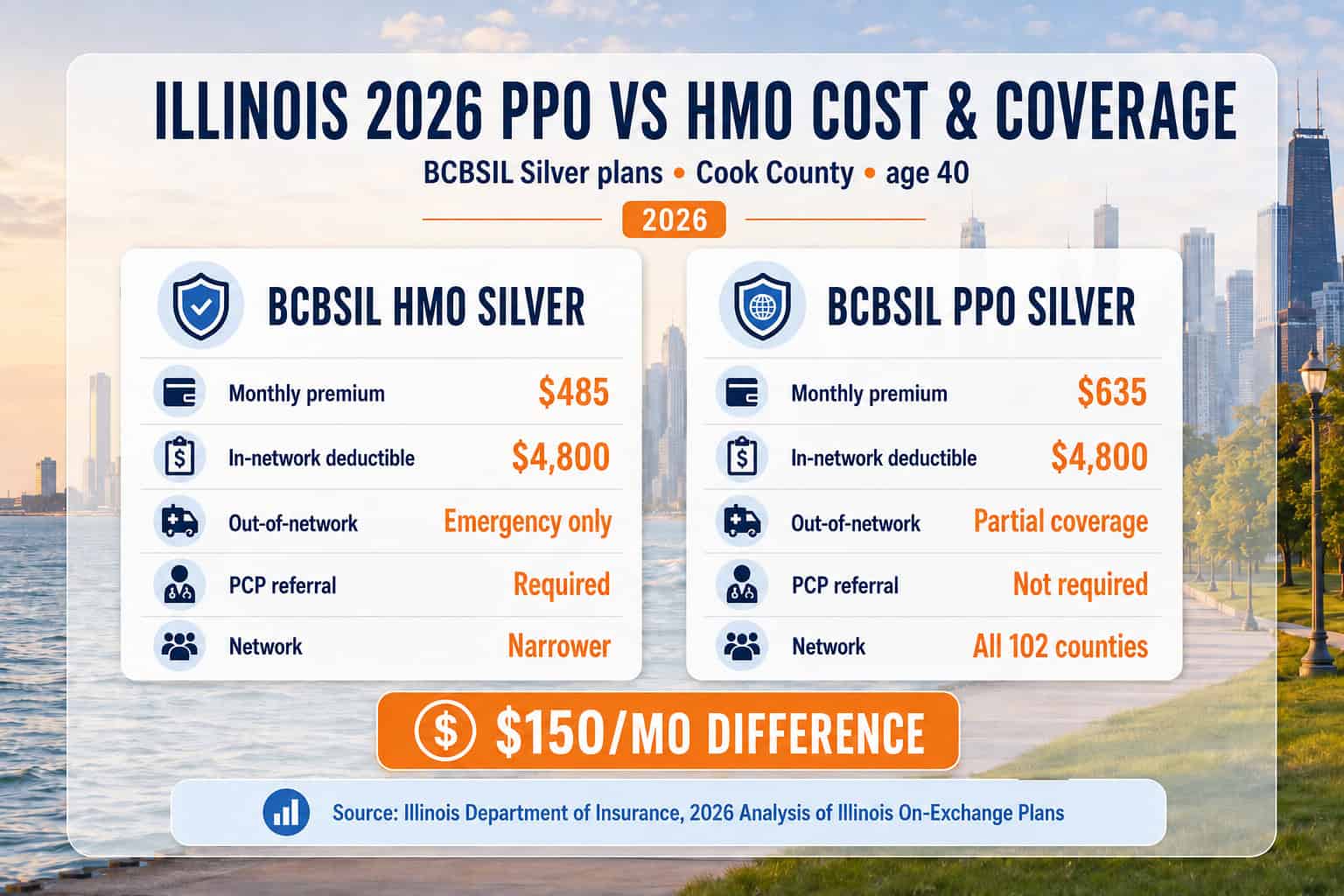

The premium difference between BCBSIL PPO and BCBSIL HMO plans at the same metal tier typically runs $80 to $200 per month in Illinois. A 40-year-old single resident in Cook County looking at BCBSIL Silver plans for 2026 might see a PPO premium around $635 and an HMO premium around $485 — a $150 monthly delta, or $1,800 per year before subsidies. The difference reflects the broader provider network and out-of-network coverage that PPO includes.

For subsidy-eligible households, the after-credit difference is much smaller. Premium tax credits cap the household contribution to the benchmark Silver plan as a percentage of income, regardless of which plan is actually chosen. A household choosing PPO Silver over HMO Silver still pays the dollar premium difference between the plans, but the subsidy applies the same way to both. Households well above subsidy thresholds — over 400 percent FPL with no 8.5 percent cap relief — pay the full premium difference and need to weigh PPO flexibility against the unsubsidized monthly cost.

| Plan Type | Typical Premium (Silver) | In-Network Deductible | Out-of-Network Coverage |

|---|---|---|---|

| BCBSIL HMO Silver | $420–$520/mo | $4,500–$5,500 | Emergency only |

| BCBSIL POS Silver | $520–$580/mo | $4,500–$5,500 | With PCP referral |

| BCBSIL PPO Silver | $585–$685/mo | $4,800–$5,800 | Partial (separate deductible) |

Premium ranges above reflect typical 2026 BCBSIL filings for a 40-year-old single resident across Illinois rating areas. Actual premiums vary by ZIP code, age, tobacco use, and specific plan within each network type. The deductible difference between HMO and PPO is usually modest at the same metal tier — most of the cost gap shows up in monthly premium, not in deductible structure.

Compare BCBSIL PPO Plans in Illinois

BCBSIL PPO is the only on-exchange PPO option in Illinois for 2026, but plan-level network and deductible variation matters. A licensed Illinois broker runs side-by-side comparisons across BCBSIL PPO Silver, Gold, and Bronze and verifies preferred providers are in-network.

Best Illinois PPO Plans by Coverage Need

The right PPO plan depends on how the household uses healthcare. Three profiles consistently get the most value out of BCBSIL PPO coverage: families with established specialists, frequent travelers and split-residence households, and adults managing chronic conditions who want maximum provider continuity. Each profile maps to a different metal tier and plan-within-portfolio choice.

Families with established specialists: Silver or Gold BCBSIL PPO. Families who have built relationships with specific pediatricians, allergists, or pediatric specialists across the Chicago metro or downstate systems benefit from PPO’s no-referral access and broader network. Gold is the right tier above 250 percent FPL when expected medical use is moderate to heavy; Silver with CSR wins below 250 percent FPL.

Frequent travelers and split-residence households: Gold BCBSIL PPO. Illinois residents who travel out of state for work, who own a second home in another state, or who have college-age children studying out of state benefit substantially from PPO’s nationwide network rules. Out-of-state care that an HMO would treat as emergency-only gets partial in-network treatment under PPO reciprocity arrangements through the BlueCard program.

Adults managing chronic conditions: Gold BCBSIL PPO. Adults with diabetes, autoimmune conditions, cardiac history, or other chronic illnesses typically have a network of specialists across multiple hospital systems. Gold’s lower deductible compensates for the higher PPO premium when expected medical use is high, and the broader network means specialist continuity even if the primary system changes affiliations.

Adults nearing Medicare eligibility: Gold BCBSIL PPO. Adults aged 60–64 typically have the highest unsubsidized premiums on the marketplace and the most predictable medical use. PPO continuity transfers naturally to BCBSIL Medicare Advantage products from the same carrier family at age 65, smoothing the Medicare transition more cleanly than switching from an HMO at the same time.

Out-of-Network Coverage in Illinois PPOs

Partial out-of-network coverage is the defining feature of a PPO plan. BCBSIL PPO products pay a percentage of the allowed amount for out-of-network providers, apply a separate out-of-network deductible, and maintain a separate out-of-network out-of-pocket maximum. The out-of-network coverage is meaningful — but it costs significantly more than in-network care, and the math depends on three factors most members underestimate.

| Cost Structure | In-Network | Out-of-Network |

|---|---|---|

| Deductible | $4,800–$5,800 | $9,000–$12,000 (separate) |

| Coinsurance after deductible | 20–30% | 40–50% |

| Out-of-pocket maximum | $9,200 individual | $18,000+ (separate) |

| Balance billing | Not allowed | Allowed for amount above reference rate |

The balance-billing exposure is what catches most PPO members off guard. When an out-of-network provider charges more than the plan’s reference rate (the maximum the plan considers reasonable for that procedure or service), the provider can bill the member directly for the difference. BCBSIL pays its percentage of the reference rate; everything above that becomes the member’s responsibility outside the deductible and out-of-pocket maximum structure. For non-emergency planned care, getting a written cost estimate from any out-of-network provider before scheduling is the only way to avoid surprise balance bills.

When an Illinois PPO Is Worth the Premium

A PPO is worth the higher premium for some households and a waste of money for others. The decision usually comes down to four practical questions about how the household actually uses healthcare. Answering each one honestly, before pricing plans, produces a clearer recommendation than abstract HMO-vs-PPO comparisons.

Do household members travel out of Illinois at least quarterly?

If yes, PPO’s nationwide network rules and out-of-network coverage justify the premium. If no, HMO usually wins on annual math — out-of-state travel is the clearest use case for PPO flexibility.

Are there specific specialists currently in use whose network status is unclear?

Verify whether the specialists participate in BCBSIL HMO before paying for PPO flexibility. Often the specialists are in both networks. PPO is only necessary if the key specialist is HMO-excluded.

Does the household dislike primary care referrals?

PPO removes the referral requirement entirely. If the friction of getting a referral before every specialist visit is a deal-breaker, PPO is worth it. If referrals are routine and the household has a long-term primary care relationship, the friction is small and HMO wins.

Is anyone managing a chronic condition requiring frequent specialist visits?

Gold PPO often beats Silver HMO on total annual cost despite the higher premium, because the lower deductible compensates for heavier expected use. Run the full-year out-of-pocket projection before choosing tier.

Common PPO Selection Mistakes in Illinois

Four mistakes consistently push PPO members into worse outcomes than they expected. Each one reflects a misunderstanding of what PPO coverage actually does — and each one is correctable before enrollment if the household compares plans carefully.

Assuming all BCBSIL PPOs use the same network

BCBSIL offers multiple PPO products with different network designations — Blue Choice PPO is broader than Blue Cross PPO, for example. Verify the specific 2026 plan network at the BCBSIL directory before enrolling.

Ignoring the separate out-of-network deductible

Out-of-network coverage feels like a safety net until the bill arrives showing a $9,000+ separate deductible that has to be met before the plan pays anything. Plan around in-network providers; treat out-of-network as exceptional.

Paying for PPO flexibility that never gets used

Members who pay $1,800 more per year for PPO and then only see in-network providers and accept primary care referrals out of habit are paying for a benefit they never use. HMO would have been the same coverage at lower cost.

Forgetting balance-billing exposure on out-of-network care

The plan’s percentage applies to the plan’s reference rate, not the provider’s billed charge. The difference can exceed the deductible and the out-of-pocket maximum for major out-of-network procedures. Get a written estimate before scheduling any planned out-of-network care.

Frequently Asked Questions About Illinois PPO Plans

The most common questions Illinois residents ask about PPO availability, BCBSIL network coverage, referral requirements, out-of-network costs, and when a PPO is worth the higher premium for 2026.

Which carriers offer PPO plans in Illinois for 2026?

Blue Cross Blue Shield of Illinois, operated by Health Care Service Corporation, is the only on-exchange carrier offering PPO plans in Illinois for 2026 through Get Covered Illinois. BCBSIL is also the only Illinois insurer offering HMO, POS, and PPO plan types on the exchange. Off-exchange PPO plans are available from select national carriers for residents who do not qualify for premium tax credits and want broader provider flexibility.

How much more does an Illinois PPO cost than an HMO?

PPO premiums typically run $80 to $200 per month higher than HMO equivalents at the same metal tier. The exact difference varies by county, age, and plan. BCBSIL PPO Silver plans for a 40-year-old in Cook County run roughly $150 above a comparable BCBSIL HMO Silver in 2026. For households eligible for premium tax credits, the after-subsidy difference is much smaller because APTC caps the household contribution to the benchmark Silver plan.

Does an Illinois PPO cover out-of-network care?

Yes — partial out-of-network coverage is the defining feature of a PPO. PPO plans pay a lower percentage of the bill for out-of-network providers and apply a separate out-of-network deductible and out-of-pocket maximum. Out-of-network providers can also balance-bill for amounts above the plan’s reference rate, so out-of-network care still costs significantly more than in-network. The exact split varies by plan and metal tier.

Do I need a referral with an Illinois PPO?

No. PPO plans do not require a primary care referral to see in-network specialists. This is the practical difference most Illinois residents notice between PPO and HMO — patients can schedule an in-network cardiologist, orthopedist, or other specialist directly without a primary care visit first. The freedom-to-choose flexibility is the main reason people pay the PPO premium.

Is a PPO worth the higher cost in Illinois?

PPO is worth the premium for three Illinois household profiles: residents who travel out of state frequently or split time between Illinois and another state, households who want to keep specific out-of-network specialists, and people who prefer skipping the primary care referral step before seeing specialists. For households who already have a primary care preference, rarely travel, and use in-network providers, HMO usually wins on annual math.

Does BCBSIL PPO cover all 102 Illinois counties?

Yes. The BCBSIL PPO network reaches all 102 Illinois counties and includes most major hospital systems statewide — Northwestern Medicine, Rush, UChicago Medicine, Advocate Health Care, OSF HealthCare, Memorial Health, and Carle Health. Provider participation can vary by specific plan within the BCBSIL portfolio, so individual plan networks should be verified at the carrier directory before enrolling.

Illinois Health Insurance Resources

Statewide overview of carriers, costs, and coverage paths for 2026

Illinois Marketplace GuideGet Covered Illinois enrollment steps, deadlines, and the new state-based platform

Best Illinois Health InsuranceTop-ranked carriers and plan options for Illinois residents in 2026

Family Health InsuranceAll Kids, marketplace splits, and mixed-status coverage for Illinois households

Affordable Illinois PlansSubsidy strategies and lowest-cost coverage paths after the 2026 rate jump

Private Medical InsuranceOff-exchange and private health coverage for unsubsidized Illinois buyers

Small Business CoverageGroup health insurance options for Illinois employers under 50 employees

Short-Term CoverageGap coverage rules and marketplace alternatives for Illinois residents

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required

Find Your Illinois PPO Plan

BCBSIL PPO offers all 102 counties of network coverage, no referral requirements, and partial out-of-network coverage — at a premium that varies by metal tier and county. ForHealthInsurance.com compares BCBSIL PPO Silver, Gold, and Bronze and verifies provider participation at no cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Illinois residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.