PPO vs HMO vs EPO vs POS: How the Plan Types Compare

PPO, HMO, EPO, and POS are the four main managed-care health plan types, and they differ on just two questions: do you need a referral to see a specialist, and does the plan cover out-of-network care? Those two answers drive everything else — premium, flexibility, and who each plan suits. A PPO is the most flexible and the most expensive; an HMO is the most restrictive and the cheapest; EPO and POS sit in between. This guide compares PPO vs HMO vs EPO vs POS for 2026, including the often-confused question of a high-deductible health plan vs a PPO, and shows which plan type fits different needs.

The Four Plan Types at a Glance

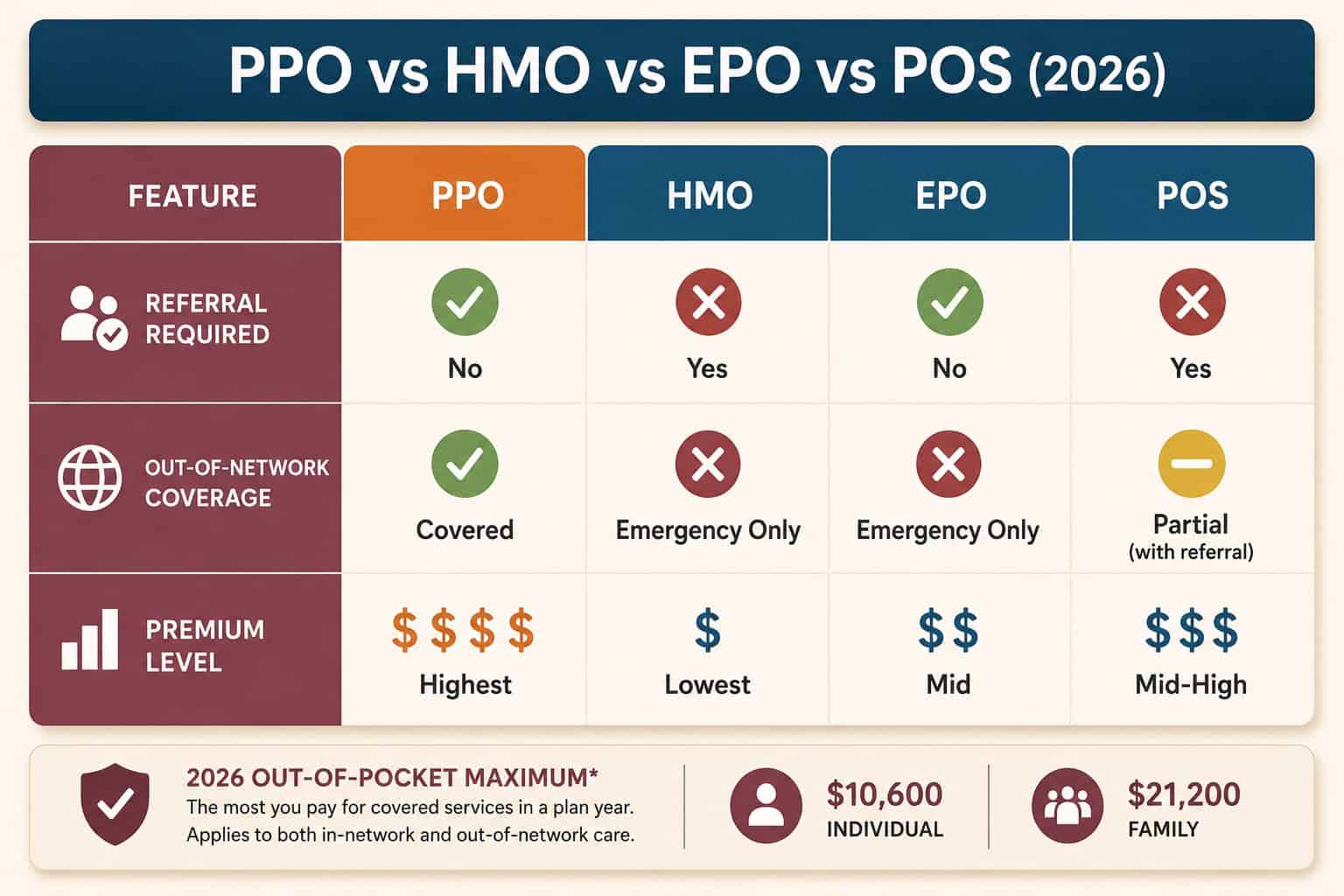

The fastest way to compare PPO vs HMO vs EPO vs POS is on two axes: whether a referral is required and whether out-of-network care is covered. A PPO needs no referral and covers out-of-network care; an HMO requires both a primary care provider and referrals; an EPO drops the referral but covers no out-of-network care except emergencies; a POS sits between, needing referrals but covering some out-of-network care. Premium follows flexibility — PPO highest, HMO lowest.

| Plan Type | Referral Required | Out-of-Network | Premium Level |

|---|---|---|---|

| PPO | No | Covered (higher cost share) | Highest |

| POS | Yes (for out-of-network) | Partial, with referral | Mid |

| EPO | No | Emergency only | Mid |

| HMO | Yes (PCP-led) | Emergency only | Lowest |

PPO vs HMO

PPO vs HMO is the most common comparison, and it comes down to flexibility versus cost. A PPO lets you see any specialist without a referral and pays a share of out-of-network care; an HMO requires a primary care provider, requires referrals to specialists, and covers no out-of-network care except emergencies. HMOs carry the lowest premiums of any plan type, while PPOs carry the highest. For identical in-network care, an HMO usually costs less — the PPO premium buys flexibility.

An HMO works well for someone whose doctors are all local and in network and who does not mind referrals. A PPO fits people who travel, want direct specialist access, or keep an out-of-network provider. The HMO saves money up front; the PPO removes friction and extends coverage across state lines, which matters most for mobile households and those managing care with several specialists.

EPO vs PPO and POS vs PPO

EPO and POS plans sit between HMO and PPO. An EPO, like a PPO, needs no referral, but like an HMO it covers no out-of-network care except emergencies — which is why an EPO costs less than a PPO, about $113 a month less for a 2026 Silver marketplace plan. A POS plan flips the trade-off: it requires referrals like an HMO but covers some out-of-network care with a referral, landing between the two on premium. Both are middle-ground options.

- EPO vs PPO. Same no-referral freedom; the PPO adds out-of-network coverage, the EPO does not. Choose EPO to save premium if care stays in network.

- POS vs PPO. A POS covers some out-of-network care but requires referrals; a PPO drops referrals entirely. The PPO is more flexible, the POS usually cheaper.

- Common thread. Out-of-network coverage and referral rules are what separate all four plan types.

High-Deductible Health Plan vs PPO

A high-deductible health plan vs a PPO is not an apples-to-apples comparison, because they describe different things. A high-deductible health plan (HDHP) is a cost structure — a higher deductible and lower premium, often HSA-eligible — while PPO describes the network type. A single plan can be both an HDHP and a PPO. What people usually mean is a low-premium, HSA-eligible HDHP versus a traditional lower-deductible PPO, and the choice turns on expected usage.

Which Plan Type Is Right for You

The right plan type follows how a household actually uses care. The more care happens out of network, across state lines, or with multiple specialists, the more a PPO’s flexibility is worth its premium; the more care stays local and in network, the more an HMO or EPO saves. Three quick situations point most people to the right plan type.

Compare Plan Types in Your ZIP Code

Enter a ZIP code and date of birth to see PPO, HMO, EPO, and POS options side by side in about 60 seconds. Licensed agents can compare networks and out-of-pocket costs at no extra charge.

Get a Quote Call 888-215-4045Cost Differences in 2026

Premium tracks flexibility across the four plan types. A 2026 Silver PPO averages about $789 a month for a 31-to-45-year-old, versus roughly $676 for an EPO, with HMOs lower still and POS plans in the middle. PPO premiums typically run 15 to 30 percent above an HMO at the same metal tier. The 2026 out-of-pocket maximum is $10,600 for an individual and $21,200 for a family, regardless of plan type.

| Plan Type | 2026 Premium (relative) | Out-of-Network |

|---|---|---|

| PPO | Highest (~$789/mo Silver, age 31–45) | Covered, higher share |

| POS | Mid | Partial, with referral |

| EPO | Mid (~$676/mo Silver) | Emergency only |

| HMO | Lowest | Emergency only |

The cheapest plan by premium is not always cheapest overall. Plan-type definitions are standardized by HealthCare.gov, and the 2026 out-of-pocket maximum applies to every type. For someone who uses a lot of care, a higher-premium PPO with a lower deductible can cost less in total than a cheap HMO with a high deductible.

Related Guides

Compare the top-rated PPO plans, nationwide multi-state networks, self-employed coverage, and a state-level PPO example.

The complete guide to PPO health insurance: how it works, costs, and coverage.

Best PPO PlansTop-rated individual PPO options and how to compare them for 2026.

Nationwide PPO PlansMulti-state national networks for travelers and remote workers.

Self-Employed Health InsuranceCoverage options for 1099 income and solo business owners.

Frequently Asked Questions About Plan Types

What is the difference between a PPO and an HMO?

A PPO lets you see specialists without a referral and covers a share of out-of-network care; an HMO requires a primary care provider and referrals and covers no out-of-network care except emergencies. The trade-off is cost: HMOs carry the lowest premiums, while PPOs carry the highest because they pay toward out-of-network claims. The right choice depends on whether you value provider flexibility or lower premiums.

Is a PPO better than an HMO?

Neither is universally better. A PPO is better for people who travel, want no referrals, or keep out-of-network specialists, while an HMO is better for those who keep care local and in-network and want to pay less. For identical in-network care, an HMO usually costs less; the PPO premium buys flexibility that not every household uses.

What is the difference between an EPO and a PPO?

Both EPO and PPO plans let you see specialists without a referral, but an EPO covers no out-of-network care except emergencies, while a PPO pays a share of out-of-network care. That difference is why a PPO costs more — about $113 a month more than an EPO for a 2026 Silver marketplace plan. An EPO suits people who want no referrals but keep care in network.

What is a POS plan?

A POS (Point of Service) plan blends HMO and PPO features: it requires a primary care provider and referrals like an HMO, but covers some out-of-network care with a referral like a PPO. POS premiums typically fall between HMO and PPO. It suits people who want some out-of-network flexibility but accept the referral requirement in exchange for a lower premium than a PPO.

What is the difference between a high-deductible health plan and a PPO?

They describe different things. A high-deductible health plan (HDHP) is a cost structure — a higher deductible and lower premium, often HSA-eligible — while PPO describes the network type. A plan can be both an HDHP and a PPO. The common comparison is between a low-premium HSA-eligible HDHP and a traditional lower-deductible PPO; the HDHP saves on premium and adds tax-advantaged saving, while the PPO lowers out-of-pocket costs when care is frequent.

Which plan type is the cheapest?

HMO plans carry the lowest premiums because they use narrow networks and require referrals, followed by EPO and POS plans in the middle, with PPO plans the most expensive because they cover out-of-network care. The cheapest plan by premium is not always the cheapest overall — a higher-premium plan with a lower deductible can cost less in total for someone who uses a lot of care.

Compare PPO, HMO, EPO, and POS Plans

See how the plan types compare for your ZIP code and budget. ForHealthInsurance.com runs the comparison, checks networks and out-of-pocket costs, and completes enrollment at no extra cost.

Get a Quote Call 888-215-4045Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving individuals and families nationwide. ForHealthInsurance.com is not affiliated with HealthCare.gov, the Centers for Medicare & Medicaid Services, or any insurance carrier. The agency helps you compare plans and enroll in coverage that meets your needs at no extra cost to you.