Small Business Health Insurance Illinois 2026: Group Plans & ICHRA Options

Small business health insurance in Illinois for 2026 looks different from the individual marketplace covered elsewhere in this cluster. Illinois employers under 50 full-time equivalents can choose between traditional group plans, defined-contribution reimbursement models like ICHRA and QSEHRA, and SHOP plans that may qualify for the federal Small Business Health Care Tax Credit. Carrier participation in the small group market remained more stable than the individual marketplace through the 2025–2026 transition. This guide walks through every coverage path for Illinois small employers and identifies which structure fits which business profile.

What brings you here today?

What Small Business Health Insurance Means in Illinois

Small business health insurance in Illinois covers employers from sole proprietors with one W-2 employee through 50 full-time equivalent employees. ACA small group rules govern this market, the Illinois Department of Insurance regulates carrier filings, and the small group market followed a more stable carrier path through 2026 than the individual marketplace did. Three primary coverage models exist: traditional group plans, defined-contribution reimbursement arrangements, and SHOP-eligible plans that may qualify for the federal Small Business Health Care Tax Credit.

| Employer Size | Mandate | Coverage Path |

|---|---|---|

| 1–24 FTEs | No mandate | Group, ICHRA, QSEHRA, or SHOP (with tax credit) |

| 25–49 FTEs | No mandate | Group, ICHRA, or SHOP (no tax credit above 25) |

| 50+ FTEs | Employer mandate applies | Group or ICHRA (large group rules) |

The full-time equivalent (FTE) calculation matters for both mandate exposure and tax credit eligibility. Two part-time employees working 20 hours each count as one full-time equivalent. Seasonal workers under 120 days per year are excluded. An Illinois small business with fifteen full-time employees and ten half-time employees calculates to twenty FTEs — well under the mandate threshold and inside the tax credit range. Misclassifying FTE counts is one of the most common compliance issues Illinois small employers face.

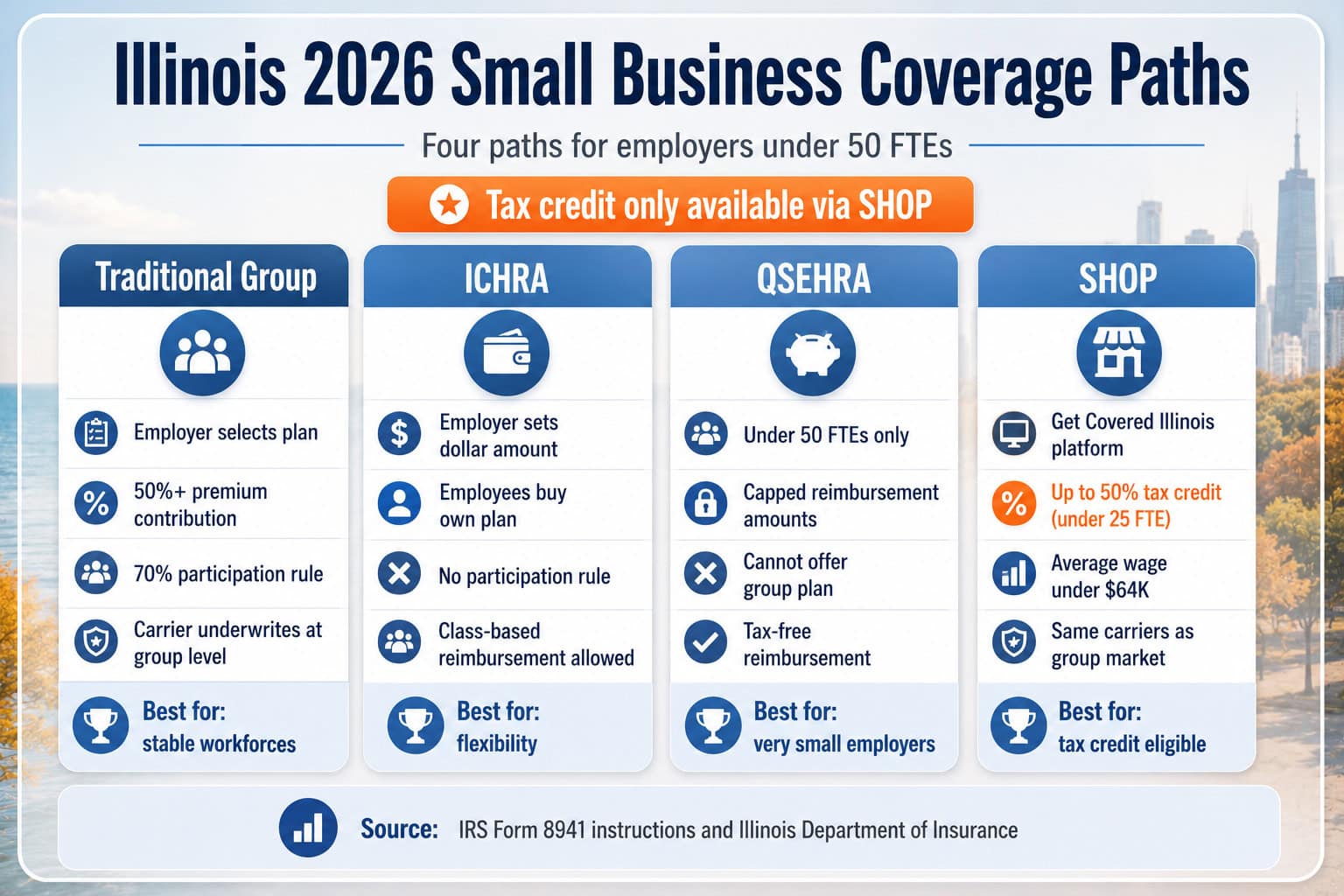

Traditional Group Health Insurance in Illinois

Traditional group health insurance Illinois small business owners shop for 2026 works the way it has for decades: the employer selects one or more plans, the carrier underwrites at the group level, employees enroll, and the employer pays at least 50 percent of premium for tax credit eligibility. The Illinois small group carrier roster stayed stable through the individual marketplace transition — Aetna continues small group plans for 2026 despite exiting the individual exchange.

Blue Cross Blue Shield of Illinois

Largest NetworkHCSC-operated BCBSIL offers the broadest small group plan portfolio in Illinois with statewide network reach across all 102 counties. HMO, POS, and PPO options available at the small group level. The dominant choice for Illinois small businesses with employees distributed across multiple regions of the state.

UnitedHealthcare

National CarrierNational carrier strong on small group product variety in Illinois. Offers broader out-of-state network reciprocity than regional carriers — useful for Illinois businesses with employees who travel frequently or who have remote workers in other states. Strong digital tools for benefits administration.

Cigna

Wellness ProgramsCigna small group plans remain available across Illinois including Cook County (unlike its individual market exit from Cook County for 2026). Strong focus on integrated wellness programs and telehealth, which appeals to small employers offering benefits packages designed to attract and retain talent.

Aetna and Humana

Group-Only PathAetna exited the Illinois individual marketplace at the end of 2025 but continues to offer group coverage — both Aetna CVS and Aetna Life small group products remain available. Humana similarly maintains a strong small group presence in Illinois despite limited individual market participation.

Group plan structure matters as much as carrier choice. Composite rating (one premium per family tier regardless of employee age) simplifies budgeting but may cost the employer more for younger workforces. Age-rated pricing reflects actual carrier risk and often produces lower total premium for businesses with a younger employee mix. Employee contribution structure — flat dollar amount versus percentage of premium — has compliance and budgeting implications that benefit from a broker review before plan selection.

ICHRA: Individual Coverage Reimbursement

ICHRA — Individual Coverage Health Reimbursement Arrangement — is a defined-contribution alternative to traditional group coverage that has grown rapidly among Illinois small employers since federal rules authorized it in 2020. Instead of selecting a group plan, the employer sets a monthly dollar reimbursement amount, and each employee uses that money to purchase their own marketplace or off-exchange plan. The employer’s cost is fixed; the employee gets plan choice; both sides benefit from predictability that traditional group lacks.

How ICHRA works for Illinois small businesses

The employer designates an annual ICHRA budget and divides it across employee classes (full-time, part-time, salaried, hourly, geographic, family status, age band). Each employee enrolls in an individual ACA-compliant plan — typically through Get Covered Illinois — and submits proof of coverage. The employer reimburses up to the designated monthly amount tax-free. Employees who choose plans costing less than the reimbursement keep the difference as taxable income.

ICHRA’s flexibility is its biggest advantage. Employers can offer different reimbursement amounts to different employee classes — including age-banded amounts that recognize older employees face higher premiums — without violating ACA non-discrimination rules. A Chicago tech startup might offer $400 per month to engineers under 30 and $700 per month to senior staff over 50 without running afoul of any small group fairness requirement. Traditional group plans cannot legally make these distinctions.

| Factor | ICHRA Advantage | Group Advantage |

|---|---|---|

| Cost predictability | Fixed employer cost | Renewal-dependent |

| Employee choice | Full marketplace selection | Limited to plans offered |

| Participation requirement | None | Typically 70% |

| Plan portability | Employee keeps plan if leaves | Lost on separation |

| Administrative burden | Verification + reimbursement | Carrier handles enrollment |

Compare Illinois Small Business Coverage Paths

Four coverage paths — traditional group, ICHRA, QSEHRA, and SHOP — each fit a different Illinois employer profile. A licensed Illinois broker maps the business to the right structure and compares carrier and plan options at no extra cost.

QSEHRA: Reimbursement for Very Small Employers

QSEHRA — Qualified Small Employer Health Reimbursement Arrangement — predates ICHRA and serves the smallest Illinois employers. QSEHRA is available only to employers with fewer than 50 FTEs who do not offer any group health plan. The structure works like ICHRA: the employer sets a monthly reimbursement amount, the employee buys an individual plan, and the employer reimburses up to the cap tax-free. QSEHRA reimbursement amounts are capped at federal limits ($6,350 individual / $12,800 family annually for 2026).

QSEHRA fits Illinois businesses with five to twenty-five employees that want to offer a benefit without the administrative overhead of traditional group coverage. Sole proprietorships and small partnerships with a few employees often choose QSEHRA because the cap on annual reimbursement makes the budget exposure smaller than ICHRA’s open-ended design. The tradeoff: QSEHRA limits reimbursement amounts, while ICHRA does not. For larger small businesses or those wanting to offer richer benefits, ICHRA usually wins.

⚠️ QSEHRA vs ICHRA — choose carefully

A QSEHRA cannot coexist with any group health plan. Employers offering even a limited group plan to any employee class are ineligible for QSEHRA but can offer ICHRA. QSEHRA also requires uniform reimbursement amounts (no class-based differentiation by age, family status, or work category), while ICHRA explicitly allows class-based reimbursement variation.

SHOP and the Small Business Health Care Tax Credit

The Small Business Health Options Program (SHOP) is the small group equivalent of the individual marketplace. In Illinois for 2026, SHOP enrollment runs through Get Covered Illinois rather than HealthCare.gov, following the state’s transition to a state-based marketplace. SHOP plans use the same carriers and underwriting rules as off-SHOP small group plans — the practical advantage is tax credit eligibility for qualifying employers.

| Tax Credit Requirement | Threshold | Note |

|---|---|---|

| Full-time equivalents | Fewer than 25 | 50% phase-out above 10 FTEs |

| Average annual wages | Under $64,000 (2026) | Phase-out begins at $32,000 |

| Employer premium share | At least 50% | Employee-only premium minimum |

| Plan purchase channel | SHOP only | Get Covered Illinois SHOP for 2026 |

| Credit amount | Up to 50% of contribution | Two-year limit; claim on Form 8941 |

The tax credit is meaningful for the smallest Illinois employers. A business with 10 FTEs and $40,000 average wages paying $80,000 annually for group coverage (50 percent of $160,000 total premium) can receive up to $40,000 in tax credit over two years. The credit is non-refundable for for-profit employers and refundable for tax-exempt organizations. Eligibility verification and Form 8941 filing benefit from CPA review during the year the credit is claimed.

Illinois Small Business Coverage Compliance

Illinois small business health insurance comes with state and federal compliance requirements beyond carrier selection. ACA non-discrimination rules apply to all employer-sponsored coverage. ERISA preemption affects which state laws govern self-funded versus fully-insured plans. Illinois state law adds specific small employer protections that supplement federal rules — particularly around continuation coverage and small group rate stability.

Key compliance areas for Illinois small employers

- FTE calculation accuracy. Misclassifying part-time hours or seasonal workers can trigger employer mandate exposure for businesses that thought they were under 50 FTEs. The IRS look-back measurement method requires consistent application.

- Affordability and minimum value. Plans offered must meet ACA affordability (employee-only premium under 9.78 percent of household income in 2026) and minimum value (60 percent actuarial value) standards to satisfy employer mandate for businesses at 50+ FTEs.

- Illinois small group continuation. Illinois state continuation coverage law extends federal COBRA rules to employers with 2–19 employees not covered by federal COBRA, requiring up to 12 months of continuation for qualifying events.

- ICHRA class structure documentation. Employers offering ICHRA must document class definitions and reimbursement amounts in writing. Class structures cannot be designed to discriminate against high-cost employees.

Cost of Small Business Health Insurance in Illinois

Small business health insurance Illinois employers pay varies significantly by carrier, plan type, employee demographics, and geographic rating area. The 2026 small group market did not see the same 50 percent premium spike that hit the individual marketplace because enhanced subsidies never applied to group coverage. Small group premiums rose modestly between 2025 and 2026 in line with normal medical inflation rather than the subsidy expiration shock.

| Coverage Tier | Typical Monthly Premium per Employee | Employer 50% Share |

|---|---|---|

| Employee-only HMO Silver | $440–$620 | $220–$310 |

| Employee-only PPO Silver | $580–$780 | $290–$390 |

| Employee + spouse HMO Silver | $960–$1,350 | $480–$675 |

| Family HMO Silver | $1,350–$1,950 | $675–$975 |

| Family PPO Gold | $1,950–$2,650 | $975–$1,325 |

ICHRA reimbursement amounts have no federal floor or ceiling — employers can set monthly amounts from $200 to $2,000 or more depending on budget and workforce composition. QSEHRA’s federal caps for 2026 are $6,350 individual / $12,800 family annually, equivalent to roughly $529 individual / $1,067 family per month. For businesses with younger employees, an ICHRA budget that matches typical Bronze or Silver marketplace premiums often produces meaningfully lower total employer cost than equivalent group coverage.

Common Small Business Coverage Mistakes in Illinois

Four mistakes consistently push Illinois small employers into worse coverage outcomes — higher costs, employee dissatisfaction, or compliance exposure. Each one reflects a reasonable instinct applied without understanding the small group market specifics or the ICHRA-versus-group structural tradeoffs.

Defaulting to group when ICHRA fits better

Small businesses with diverse employee ages, varied geographic locations, or high turnover often save 20–30 percent with ICHRA versus traditional group — but reflexively choose group because it is familiar. Run the comparison before committing to a carrier.

Missing the SHOP tax credit eligibility window

The Small Business Health Care Tax Credit is available only for plans purchased through SHOP (Get Covered Illinois for 2026) and only for two consecutive years. Employers eligible for the credit who buy off-SHOP forfeit thousands in potential savings.

Misclassifying FTE counts

Seasonal workers, part-time hours aggregation, and contractor relationships have specific FTE counting rules. Misclassification can either trigger unexpected employer mandate exposure or invalidate small group and tax credit eligibility.

Ignoring the 70 percent participation requirement

Traditional group plans require 70 percent employee participation in most cases. Small businesses with employees who decline coverage (because they’re on a spouse’s plan, for example) sometimes fail this threshold mid-year. The November 15 – December 15 special enrollment window waives this rule annually.

Frequently Asked Questions About Illinois Small Business Health Insurance

The most common questions Illinois small business owners ask about group coverage eligibility, tax credits, ICHRA versus group tradeoffs, carrier options, and enrollment timing for 2026.

How many employees do I need for small business health insurance in Illinois?

Illinois small business health insurance is available to employers with at least one common-law employee and is governed by ACA small group rules for businesses with up to 50 full-time equivalent employees. There is no minimum employee count for ICHRA or QSEHRA reimbursement arrangements — sole proprietors with at least one W-2 employee can offer either. Businesses with 50 or more full-time equivalents fall under large group rules and the employer mandate.

What is the Illinois Small Business Health Care Tax Credit?

The federal Small Business Health Care Tax Credit is available to Illinois employers with fewer than 25 full-time equivalent employees, average annual wages under $64,000, and who pay at least 50 percent of employee-only premium costs. The credit equals up to 50 percent of the employer’s premium contribution and is claimed on IRS Form 8941. Eligibility requires plans purchased through SHOP, which in Illinois runs through Get Covered Illinois for 2026.

What is the difference between group health insurance and ICHRA in Illinois?

Group health insurance is an employer-selected plan offered uniformly to eligible employees, with the employer paying a defined percentage of premiums. ICHRA — Individual Coverage Health Reimbursement Arrangement — is an alternative where the employer sets a monthly dollar reimbursement amount and each employee chooses their own marketplace or off-exchange plan. ICHRA offers more flexibility and predictable employer costs; group offers simpler employee choice and stronger participation.

Which carriers offer small business health insurance in Illinois for 2026?

Major small group carriers in Illinois for 2026 include Blue Cross Blue Shield of Illinois (HCSC), UnitedHealthcare, Cigna, Humana, and Aetna. The small group market is more stable than the individual marketplace — Aetna remains available for small group and large group coverage in Illinois even though it exited the individual marketplace at the end of 2025. The Illinois Department of Insurance regulates small group plans under the same ACA framework as individual plans.

Can my Illinois small business offer different plans to different employees?

Yes, but with constraints. Traditional group plans must be offered uniformly to all eligible employees within defined class structures — typically full-time vs part-time, salaried vs hourly, or geographic location. ICHRA explicitly allows different reimbursement amounts by employee class, including by age band, which is one of its main flexibility advantages. The class structure rules require careful documentation to avoid discrimination claims and ACA penalties.

When can I enroll my Illinois small business in health insurance?

Illinois small group health insurance can be set up year-round, with most carriers offering monthly effective dates. The federal small group special enrollment period from November 15 through December 15 each year removes the typical 70 percent participation requirement, making it the easiest window for smaller employers or those with employees who may decline coverage. ICHRA and QSEHRA can be established at any time during the year.

Illinois Health Insurance Resources

Statewide overview of carriers, costs, and coverage paths for 2026

Illinois Marketplace GuideGet Covered Illinois enrollment steps, deadlines, and the new state-based platform

Best Illinois Health InsuranceTop-ranked carriers and plan options for Illinois residents in 2026

Illinois PPO PlansBCBSIL PPO options and other flexible network choices statewide

Family Health InsuranceAll Kids, marketplace splits, and mixed-status coverage for Illinois households

Affordable Illinois PlansSubsidy strategies and lowest-cost coverage paths after the 2026 rate jump

Private Medical InsuranceOff-exchange and private health coverage for unsubsidized Illinois buyers

Short-Term CoverageGap coverage rules and marketplace alternatives for Illinois residents

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required

Set Up Illinois Small Business Coverage

Whether traditional group, ICHRA, QSEHRA, or SHOP makes sense depends on workforce composition, budget predictability needs, and tax credit eligibility. ForHealthInsurance.com runs all four comparisons side by side and handles enrollment at no extra cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Illinois businesses. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.