Best Health Insurance Illinois 2026: Top Carriers & Plans Ranked

Finding the best health insurance Illinois residents can buy for 2026 starts with three questions: which doctors and hospitals matter most to the household, how much medical care does the family realistically expect to use, and what household income level applies for subsidies. Premium alone is rarely the right ranking. This guide breaks down the seven carriers competing for Illinois enrollees, identifies the best fit by coverage need and life stage, and flags the 2026 carrier exits that reshaped the state market.

What brings you here today?

How to Choose the Best Health Insurance in Illinois

The best health insurance in Illinois depends on three variables in roughly this order: provider preferences, expected medical use, and subsidy eligibility. Ranking carriers without those inputs produces generic answers that rarely match a specific household’s situation. The right plan for a healthy 28-year-old in Chicago is almost never the right plan for a 55-year-old couple in Springfield managing diabetes — and not because one carrier is better than another, but because the inputs are different.

Start with the provider check. Make a short list of the doctors, specialists, and hospitals that matter — primary care, pediatrician, any specialists currently in use, and the hospital system the household would prefer for emergency care. Then check each candidate plan’s 2026 network directly through the carrier directory or the Get Covered Illinois plan finder. The Illinois Department of Insurance publishes the annual on-exchange analysis confirming which carriers offer which plan types in which counties, but plan-level network participation must be verified at the carrier directory level.

| Evaluation Factor | What to Check | Where |

|---|---|---|

| Provider network | Specific doctors and hospitals in-network for 2026 | Carrier directory + call doctor’s office |

| Total annual cost | Premium × 12 + expected out-of-pocket | Get Covered Illinois plan finder |

| Prescription formulary | All current medications covered at acceptable tier | Carrier formulary lookup by drug name |

| Subsidy eligibility | APTC amount + CSR qualification at Silver | Get Covered Illinois eligibility checker |

| Network type | HMO, POS, or PPO — referral requirements | Plan summary documents |

Premium alone is misleading. A Bronze plan at $90 a month can cost more annually than a Silver plan at $250 a month if expected medical use triggers the Bronze deductible. The fair comparison is annualized total cost: premium times twelve plus an honest estimate of out-of-pocket spending based on the household’s medical history. Households who consistently maxed deductibles last year should expect to do so again — choose accordingly.

Top Carriers in Illinois for 2026

Seven carriers compete for Illinois marketplace enrollees in 2026, down from eleven in 2025 after Aetna CVS, Aetna Life, Health Alliance, and Quartz exited the state. The remaining carriers offer 285 unique plan combinations across Bronze, Silver, Gold, and Catastrophic tiers. Service areas vary significantly by county — a carrier that ranks well in Cook County may not even participate in a downstate rating area, and vice versa.

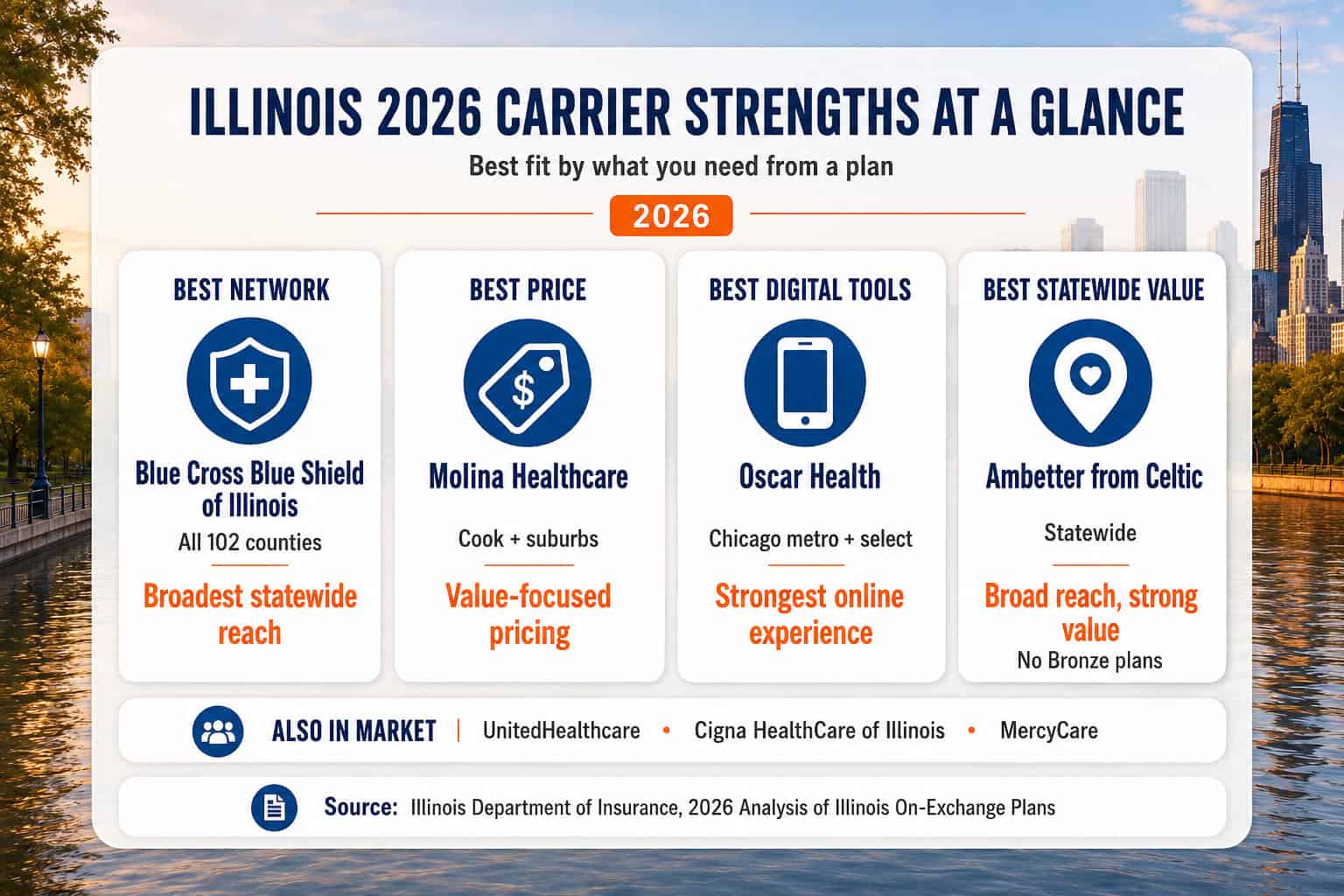

Blue Cross Blue Shield of Illinois

Statewide #1Operated by Health Care Service Corporation. The dominant Illinois carrier — only on-exchange option offering HMO, POS, and PPO plans for 2026. Network covers all 102 counties and includes Northwestern Medicine, Rush, UChicago Medicine, Advocate, OSF, Memorial Health, and Carle Health. Best for residents who prioritize network breadth and provider choice.

Molina Healthcare of Illinois

Lowest PremiumFrequently the cheapest monthly premium on Get Covered Illinois, particularly in Cook County and surrounding suburbs. HMO-only with a narrower network and stricter referral requirements. Best for households who prioritize keeping monthly costs lowest and are comfortable with a smaller in-network provider list.

Ambetter from Celtic

Cost-FocusedMarketed under the Ambetter brand by Celtic Insurance. Popular cost-conscious choice for Illinois families on Silver and Gold tiers. Bronze plans are no longer offered in Illinois for 2026, narrowing the budget options from this carrier. Best for households at 138–250 percent of FPL who qualify for Silver cost-sharing reductions.

Oscar Health Plan

Digital-FirstTech-focused carrier with a strong telehealth platform and concierge support model. Operates in Chicago metro and select downstate counties. Often a competitive choice for residents under 40 who prefer app-based plan management and virtual primary care. HMO network.

UnitedHealthcare

National ReachNational carrier offering ACA plans in select Illinois counties for 2026. Strong digital tools, broader out-of-network coverage on certain plan tiers, and useful for households with members who travel frequently or who split time between Illinois and another state.

Cigna HealthCare of Illinois

No Cook CountyOffers HMO plans in most non-Cook Illinois counties for 2026 but pulled out of Cook County effective January 1, 2026. Emphasizes preventive care and telehealth in suburban and downstate markets. Chicago-area Cigna members from 2025 had to switch carriers for 2026.

MercyCare

Northern IllinoisRegional faith-based carrier operating in northern Illinois with a network anchored to Mercyhealth System hospitals. Best for residents in Rockford, Belvidere, and surrounding northern Illinois counties where Mercyhealth is the primary system.

Best Plan by Coverage Need

The best health insurance Illinois plan for a given household depends on who is being covered and what kind of care they expect to use. The same carrier and metal tier can be the right answer for a family of four and the wrong answer for a self-employed single adult. The four most common Illinois household profiles cover the majority of marketplace shoppers.

Best for families with children: Silver or Gold BCBSIL HMO or PPO. The broad BCBSIL network includes most major pediatric providers — Lurie Children’s, Advocate Children’s, OSF Children’s — across both Chicago and downstate. Silver makes sense for households at 138–250 percent of FPL because cost-sharing reductions lower deductibles substantially. Above 250 percent FPL with regular pediatric visits, Gold’s lower deductible often wins on annual math.

Best for self-employed and freelancers: Silver or Gold with telehealth. Oscar Health and BCBSIL both offer strong telehealth platforms. Self-employed Illinois residents typically have variable income, which makes Silver with potential CSR a smart hedge against lower-income years. The premium tax credit is fully deductible for self-employed filers, lowering effective annual cost further.

Best for healthy young adults under 30: Bronze or Catastrophic. Ambetter has no Bronze in 2026, narrowing the field to BCBSIL, Molina, Oscar, and UnitedHealthcare. Healthy adults with no regular medications and no expected medical use minimize premium spend with Bronze. Anyone with even occasional medical needs should compare Silver totals before defaulting to Bronze.

Best for adults nearing Medicare eligibility: Gold BCBSIL PPO. Adults aged 60–64 typically have the highest unsubsidized premiums on the marketplace and the most predictable medical use. Gold’s lower deductible smooths out-of-pocket spending in the run-up to Medicare enrollment, and BCBSIL PPO provider continuity transfers naturally to Medicare Advantage products from the same carrier family.

Compare Top Illinois Plans by Network

Verifying that preferred doctors and hospitals participate in a specific 2026 plan is faster with a licensed Illinois broker. ForHealthInsurance.com runs plan comparisons across all seven carriers and confirms network participation at the carrier and plan level at no cost.

Best Plans by Metal Tier in Illinois

Illinois on-exchange plans for 2026 come in four metal tiers: Bronze, Silver, Gold, and Catastrophic. Platinum-tier plans were not filed by any carrier for the Illinois on-exchange market in 2026, making Gold the richest tier available through Get Covered Illinois. Each tier suits a different combination of expected medical use and subsidy eligibility.

| Metal Tier | Carrier Covers | Best For |

|---|---|---|

| Bronze | ~60% | Healthy adults; emergency-only protection; no CSR available |

| Silver | ~70% | Households 100–250% FPL — only tier with cost-sharing reductions |

| Gold | ~80% | Regular medical use, chronic conditions, predictable cost preference |

| Catastrophic | ~60% (worst-case) | Under 30 or hardship exemption; no premium tax credit eligibility |

Silver-tier cost-sharing reductions deserve specific attention. Households between 100 and 250 percent of the federal poverty level who choose a Silver plan get reductions on deductibles, copays, and out-of-pocket maximums on top of premium tax credits. A Silver plan with full CSR for a family of four near 150 percent of poverty can have an effective deductible under $500 rather than the standard $5,000-plus. CSRs do not transfer to Bronze, Gold, or Catastrophic — anyone eligible should choose Silver to capture the benefit.

Bronze remains a legitimate choice for healthy households well above subsidy thresholds who want low monthly costs and accept high deductibles as worst-case protection. Ambetter no longer offers Bronze plans in Illinois for 2026, narrowing the Bronze field to BCBSIL, Molina, Oscar, UnitedHealthcare, and the regional carriers. Catastrophic plans serve a narrow audience — under-30 enrollees or hardship-exemption holders who want the lowest possible premium and have minimal expected medical use.

Best Network Type for Illinois Residents

Illinois on-exchange plans come in three network types — HMO, POS, and PPO — and only Blue Cross Blue Shield of Illinois offers all three on the exchange for 2026. The other six carriers offer HMOs with limited POS variants. The best network type depends on how much provider flexibility matters versus how much premium savings matters.

PPO

Most FlexibilityPreferred Provider Organization plans allow in-network access without referrals and provide partial out-of-network coverage. In Illinois, BCBSIL is the primary on-exchange PPO option for 2026. Best for residents who travel frequently, want maximum provider choice, or prefer to avoid the referral system. See the Illinois PPO plans guide for carrier specifics.

HMO

Lowest PremiumHealth Maintenance Organization plans require staying in-network and getting a primary care referral for specialists. Most Illinois on-exchange carriers — Molina, Ambetter, Oscar, MercyCare — offer HMOs exclusively. Premiums run $80–200 below PPO equivalents for similar metal tiers, making HMO the most common choice for cost-conscious enrollees who already have a primary care preference.

POS

Middle GroundPoint-of-Service plans blend HMO and PPO features. A primary care doctor coordinates in-network care, but out-of-network specialists are covered at a reduced rate. BCBSIL offers POS variants for 2026. Less common than HMO or PPO but useful for households who want some network flexibility without paying full PPO premiums.

Catastrophic

HMO OnlyCatastrophic plans for under-30 enrollees and hardship-exemption holders are HMO-only in Illinois for 2026. Network restrictions match standard HMO plans from the same carrier, but the deductible equals the federal annual out-of-pocket maximum. Premium tax credits cannot be applied.

2026 Carrier Changes That Affect Your Choice

The Illinois market changed substantially between 2025 and 2026 plan years. Four carriers exited the on-exchange market entirely, one major carrier pulled out of the state’s largest county, and one carrier discontinued its lowest metal tier. These changes determine which carriers can even be considered for many households — anyone shopping the Illinois marketplace needs to know what changed before evaluating plans.

Aetna CVS, Aetna Life, Health Alliance, and Quartz exited Illinois

Members of all four carriers needed to actively select a new plan during open enrollment — auto-renewal was not possible. Aetna remains active in Illinois Medicare Advantage and group/employer markets, but not on the individual marketplace.

Cigna pulled out of Cook County for 2026

Cigna remains available in most non-Cook Illinois counties. Chicago-area Cigna members from 2025 were auto-renewed to a different carrier and need to verify network participation for their preferred doctors.

Ambetter from Celtic discontinued its Bronze tier

Bronze shoppers who held Ambetter in 2025 had to move up to Silver with Ambetter or switch carriers entirely. Silver and Gold Ambetter plans remain available statewide.

No on-exchange Platinum plans filed for 2026

No carrier filed Platinum-tier plans for the Illinois marketplace in 2026. Households wanting Platinum-level coverage must shop off-exchange, which forfeits premium tax credit eligibility.

The carrier exits affected roughly 90,000 Illinois marketplace enrollees according to CMS enrollment data. Most got auto-renewed to a different carrier — but auto-renewal does not verify network continuity. Anyone whose 2025 carrier is no longer in the Illinois market should verify their preferred doctors and hospitals participate in the auto-assigned 2026 plan before assuming the transition is seamless.

Common Selection Mistakes in Illinois

Four patterns trip up Illinois marketplace shoppers. Sticking with an auto-renewed plan, choosing on premium alone, ignoring the prescription formulary, and misapplying the Silver-vs-Gold decision are the most common and most correctable errors before the plan year locks in.

Accepting auto-renewal without checking the network

Auto-renewed plans from discontinued or county-exited carriers may have substantially different in-network providers than the prior plan. Verify preferred doctors and hospitals before the new plan year starts.

Ranking by premium alone

Total annual cost — premium × 12 plus expected out-of-pocket — is the right ranking. A $90 Bronze plan with a $9,000 deductible costs more than a $250 Silver plan with a $2,500 deductible if expected medical use is even moderate.

Not checking the prescription formulary

Each carrier has its own formulary list and tier structure. A medication covered at tier 1 with one carrier may sit at tier 4 with another, producing copay differences of $100 or more per fill.

Picking Silver without qualifying for CSR — or skipping Silver when you do

Silver is the right tier for households at 100–250 percent FPL because of cost-sharing reductions. For households well above 250 percent FPL, Gold often beats Silver on annual math because the lower deductible compensates for the higher premium.

Frequently Asked Questions About Illinois Health Insurance

The most common questions Illinois residents ask about which carrier is best, how many carriers operate in 2026, the best plan for families, how to check provider networks, and whether Platinum is available this year.

Which health insurance carrier is best in Illinois for 2026?

Blue Cross Blue Shield of Illinois (operated by Health Care Service Corporation) is the strongest single carrier for most Illinois residents in 2026 because it offers the broadest statewide network across all 102 counties and is the only on-exchange insurer offering HMO, POS, and PPO plan types. Best by need varies: Molina or Ambetter typically lead on price, Oscar leads on digital tools and telehealth, and BCBSIL leads on network breadth and provider choice.

How many carriers offer health insurance in Illinois in 2026?

Seven carriers offer on-exchange health insurance in Illinois for 2026: Blue Cross Blue Shield of Illinois, Cigna HealthCare of Illinois, Ambetter from Celtic, Molina Healthcare, Oscar Health Plan, UnitedHealthcare, and MercyCare. This is down from eleven carriers in 2025 after Aetna CVS, Aetna Life, Health Alliance, and Quartz exited the state at the end of 2025.

What is the best plan for a family in Illinois?

Most Illinois families do best with a Silver or Gold plan from Blue Cross Blue Shield of Illinois because the BCBSIL network includes most major hospital systems and pediatric providers across the state. Families with household income between 100 and 250 percent of the federal poverty level should choose Silver specifically to capture cost-sharing reductions that lower deductibles and out-of-pocket maximums. Families above 250 percent of FPL who expect routine medical use often save more over the year with Gold.

Should I pick the cheapest plan or the best network?

Premium alone does not determine total cost. A Bronze plan with $90 monthly premiums can cost more than a Silver plan at $250 monthly if expected medical use triggers the higher Bronze deductible. The right comparison is total annual cost — premium times twelve plus expected out-of-pocket. Confirm preferred doctors and hospitals are in-network before choosing — switching mid-year is rarely possible, so the network decision lasts the full plan year.

Are Platinum plans available in Illinois for 2026?

No on-exchange carrier filed Platinum-tier plans for the Illinois marketplace in 2026, per the Illinois Department of Insurance annual analysis. Gold became the richest tier available through Get Covered Illinois. Off-exchange Platinum-level products remain available from select carriers for residents who want the highest level of coverage and do not qualify for premium tax credits.

How do I check if my doctor takes a specific Illinois plan?

Three reliable methods: use the carrier’s online provider directory for the specific plan and year (network names change between plan years), use the Get Covered Illinois plan finder which surfaces provider participation by ZIP, or call the doctor’s office and ask which 2026 Illinois plans they accept. Calling the office is the most reliable check because directories often lag actual contract changes by weeks or months.

Illinois Health Insurance Resources

Statewide overview of carriers, costs, and coverage paths for 2026

Illinois Marketplace GuideGet Covered Illinois enrollment steps, deadlines, and the new state-based platform

Illinois PPO PlansBCBSIL PPO options and other flexible network choices statewide

Family Health InsuranceAll Kids, marketplace splits, and mixed-status coverage for Illinois households

Affordable Illinois PlansSubsidy strategies and lowest-cost coverage paths after the 2026 rate jump

Private Medical InsuranceOff-exchange and private health coverage for unsubsidized Illinois buyers

Small Business CoverageGroup health insurance options for Illinois employers under 50 employees

Short-Term CoverageGap coverage rules and marketplace alternatives for Illinois residents

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required

Compare Top Illinois Health Plans

Comparing seven carriers, four metal tiers, and three network types across Get Covered Illinois is faster with a licensed Illinois broker. ForHealthInsurance.com runs plan comparisons, verifies network participation, and helps complete enrollment at no extra cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Illinois residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.