Self-Employed Health Insurance

When you work for yourself there is no employer plan and no HR department to enroll you — self-employed health insurance is coverage you buy on your own, as an individual or family, through the ACA marketplace or directly from a carrier. The upside is full control over the plan and network; the trade-off is that you pay the whole premium, though premium tax credits and the self-employed health insurance deduction can bring the real cost down substantially. This guide covers what self-employed health insurance costs in 2026, how the tax deduction works, which plan types fit 1099 and freelance income, and exactly how to enroll. Because PPO networks travel well across state lines, they are a common fit for self-employed buyers who work in more than one place.

How Self-Employed Health Insurance Works in 2026

Self-employed health insurance is individual-market coverage you buy directly rather than through an employer. You can shop the ACA marketplace, where plans qualify for premium tax credits if your income fits, or buy off the exchange from a carrier, where PPO selection is widest. Either way the coverage is ACA-compliant and includes the ten essential health benefits, and you choose the plan, tier, and network yourself.

- You buy as an individual or family. No group plan — sole proprietors, freelancers, and 1099 contractors all use the individual market.

- Two channels. On-exchange plans unlock premium tax credits; off-exchange plans from national carriers widen PPO choice.

- Same rules as any ACA plan. Guaranteed issue, no medical underwriting, and coverage of pre-existing conditions.

- Tax breaks stack. Premium tax credits lower the bill up front; the self-employed health insurance deduction lowers taxable income on the rest.

About 16 million Americans are self-employed, and a wave of freelance and 1099 work has pushed more buyers into the individual market. For a side-by-side of how the plan types compare, see the best PPO health insurance plans guide. The federal marketplace also publishes a dedicated walkthrough for the self-employed at HealthCare.gov.

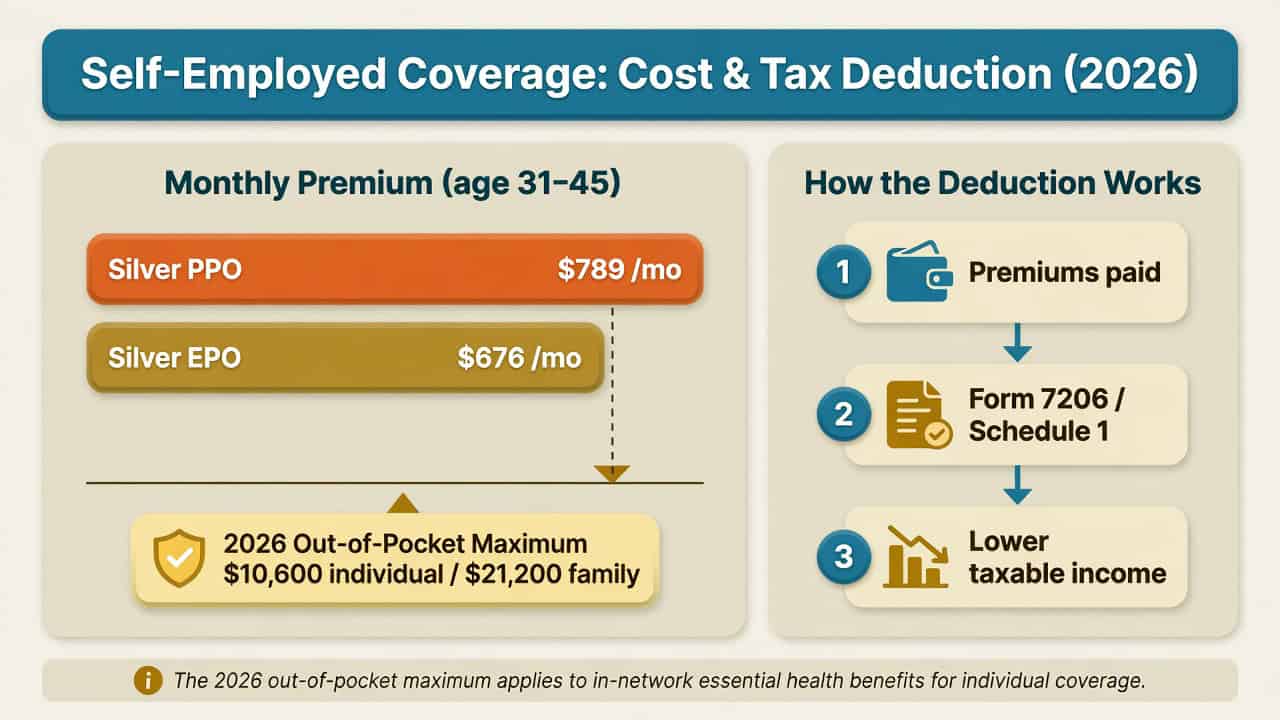

How Much Self-Employed Health Insurance Costs in 2026

The self-employed pay the entire premium, with no employer contribution, so sticker prices look higher than a job-based plan. A 2026 Silver marketplace PPO averages about $789 per month for a 31-to-45-year-old, versus roughly $676 for an EPO. But two offsets change the real number: premium tax credits cut the monthly cost when income qualifies, and the self-employed health insurance deduction lowers taxable income on whatever you pay after credits.

| 2026 Cost Benchmark (Individual) | Figure | Source |

|---|---|---|

| Silver PPO average premium (age 31–45) | ~$789/month | CMS plan-data analysis |

| Silver EPO average premium (same age) | ~$676/month | CMS plan-data analysis |

| 2026 out-of-pocket maximum | $10,600 individual / $21,200 family | HealthCare.gov |

| Average in-network deductible | just under $3,000 | KFF |

| Premiums paid | deductible from AGI | IRS Form 7206 |

| Premium tax credit | available when income qualifies | HealthCare.gov |

The figure that decides value is total annual cost after credits and the deduction, not the headline premium. The 2026 out-of-pocket maximum is set by HealthCare.gov, and average deductibles and premium trends are tracked by KFF. For variable 1099 income, estimating annual income carefully matters, because premium tax credits are reconciled at tax time and a low estimate can mean paying some credit back.

The Self-Employed Health Insurance Deduction

The self-employed health insurance deduction is the biggest tax break tied to self-employed health insurance. It lets you deduct premiums for medical, dental, and qualifying long-term care coverage for yourself, your spouse, your dependents, and children under 27 as an adjustment to income — an above-the-line deduction you get even without itemizing. It is computed on Form 7206 and carried to Schedule 1, lowering your adjusted gross income.

- Above-the-line. It reduces AGI directly, so you claim it whether or not you itemize.

- Profit-limited. The deduction cannot exceed your net profit from the business under which the plan is established.

- No employer-plan months. It is not allowed for any month you (or your spouse) were eligible for an employer-subsidized health plan.

- Interacts with credits. If you also receive a premium tax credit, the deduction and the credit are coordinated so the same dollars are not counted twice.

Because the rules around profit limits, S-corp ownership, and the credit interaction get technical, the IRS walkthrough on Form 7206 is the authoritative reference, and a tax professional can confirm how the deduction applies to your return. The takeaway for planning: self-employed health insurance is one of the few personal premiums the tax code lets you subtract from income, which narrows the gap between the self-employed premium and what an employee effectively pays.

Best Plan Types for the Self-Employed: PPO, HSA, and More

The right plan type for self-employed health insurance depends on how you work and how you use care. PPOs fit buyers who travel or work across state lines; HSA-eligible high-deductible plans fit healthy buyers who want a tax-advantaged cushion; and lower-tier plans fit those who mainly want catastrophic protection. Because the self-employed control the choice entirely, matching the plan type to the work pattern is where most of the value is won or lost.

PPO

Best for Multi-State WorkCovers a share of out-of-network care with no referrals, so it travels well for consultants, contractors, and remote workers who cross state lines. The broadest PPO networks are often sold off the exchange by national carriers.

HSA-Eligible HDHP

Best for Tax SavingsA high-deductible plan paired with a Health Savings Account gives the self-employed a triple-tax-advantaged way to save for care — useful for healthy buyers with steady cash flow who want to bank pre-tax dollars.

EPO / HMO

Best for Lower PremiumsIf your providers are all local and in network, an EPO or HMO usually costs less than a PPO for the same care. The trade-off is little or no out-of-network coverage and, for HMOs, referral requirements.

Short-Term

Stopgap OnlyShort-term plans can bridge a gap between coverage but are not ACA-compliant, can deny pre-existing conditions, and do not qualify for the deduction or tax credits. Treat them as a temporary fallback, not a primary plan.

Every plan compared through ForHealthInsurance.com meets ACA compliance standards and includes the ten essential health benefits required under federal law. ForHealthInsurance.com is an independent brokerage, A+ rated by the Better Business Bureau, and quotes these options without upselling or pressure.

Self-Employed Health Insurance by Situation

Because self-employed health insurance is a personal choice rather than a one-size group plan, it helps to match coverage to the situation. Freelancers and 1099 contractors weigh deductibility and provider continuity; sole proprietors lean on tax credits plus the deduction; multi-state and remote workers prioritize network reach; and healthy, cost-focused buyers favor tax-advantaged savings. The table maps common situations to the coverage traits that matter most.

| Situation | Prioritize | Best-Fit Coverage |

|---|---|---|

| Freelancer / 1099 contractor | Provider continuity, deductibility | Marketplace or off-exchange PPO |

| Sole proprietor | Premium tax credit + deduction | Marketplace Silver or Gold |

| Multi-state / remote | Nationwide network | BlueCard or national-carrier PPO |

| Healthy, cost-focused | Lower premium, tax-advantaged savings | HSA-eligible HDHP |

| Managing a condition | No referrals, specialist access | PPO with broad specialist network |

Multi-state and remote self-employed workers in particular gain from a national network — see nationwide PPO plans for how BlueCard and national-carrier PPOs keep care in network across state lines.

Compare Self-Employed Plans in Your ZIP Code

Enter a ZIP code and date of birth to see self-employed health insurance options on and off the exchange in about 60 seconds. Licensed agents can check networks, premium tax credit eligibility, and out-of-pocket costs at no extra charge.

Get a Quote Call 888-215-4045How to Get Health Insurance When You’re Self-Employed

Getting self-employed health insurance takes four steps, and comparing both on-exchange and off-exchange options is what surfaces the widest selection. On-exchange plans unlock premium tax credits; off-exchange plans from national carriers widen PPO choice. The process starts in about 60 seconds and ends with licensed-agent help at no extra cost, with enrollment during open enrollment or a special enrollment period.

- Estimate your annual income — this sets premium tax credit eligibility, so estimate variable 1099 income carefully.

- Enter ZIP code and date of birth to pull available plans on and off the exchange.

- Check your providers and compare total cost — premium, deductible, out-of-network terms, and out-of-pocket maximum.

- Apply with licensed-agent support during open enrollment (Nov 1–Jan 15 in most states) or a special enrollment period.

Self-Employed Coverage Mistakes to Avoid

Most self-employed health insurance mistakes come from treating the individual market like a job-based plan or from leaving tax breaks on the table. The plan is yours to design, which means the responsibility for getting income estimates, networks, and timing right falls on you. Three traps account for most of the avoidable cost.

- Lowballing income for bigger credits. Premium tax credits are reconciled at tax time — underestimate variable 1099 income and you may repay part of the credit.

- Skipping the deduction. Many self-employed buyers never claim the self-employed health insurance deduction, leaving a legitimate above-the-line write-off unused.

- Defaulting to short-term plans. They look cheap but are not ACA-compliant, can exclude pre-existing conditions, and do not qualify for credits or the deduction.

Related Guides

Compare PPO coverage, the best PPO carriers, nationwide networks, and how the plan types differ.

A state-level example of PPO carriers and networks.

Best PPO Health Insurance PlansTop national PPO carriers and how to choose the best plan.

Nationwide PPO PlansMulti-state national networks for travelers and remote workers.

PPO vs HMO vs EPO vs POSA full side-by-side of the four managed-care plan types.

Frequently Asked Questions About Self-Employed Health Insurance

How do self-employed people get health insurance?

Self-employed people buy individual health insurance on their own — through the ACA marketplace, which qualifies them for premium tax credits if their income fits, or off the exchange directly from a carrier, where PPO selection is often widest. There is no group plan, so the buyer compares plans by ZIP code, checks that their doctors are in network, and enrolls during open enrollment or a special enrollment period.

Is health insurance tax deductible for the self-employed?

Yes. The self-employed health insurance deduction lets you deduct premiums for medical, dental, and qualifying long-term care coverage for yourself, your spouse, and dependents as an adjustment to income on Schedule 1, computed on IRS Form 7206. It lowers your adjusted gross income without itemizing, but it cannot exceed your net self-employment profit and is not allowed for any month you were eligible for an employer plan.

How much does self-employed health insurance cost in 2026?

A 2026 Silver-tier marketplace PPO averages about $789 per month for a 31-to-45-year-old, versus roughly $676 for a comparable EPO. The self-employed pay the full premium themselves, but premium tax credits can cut the net cost sharply when income qualifies, and the self-employed health insurance deduction lowers taxable income on what remains. Final cost depends on age, ZIP code, plan tier, and tobacco use.

Can self-employed people get a PPO plan?

Yes. The self-employed can buy PPO plans, and many of the broadest PPO networks are sold off the exchange by national carriers. A PPO suits self-employed buyers who travel, work across state lines, or want to keep specific specialists, because it covers a share of out-of-network care and requires no referrals. On the marketplace, PPOs are scarcer, since more than eight in ten plans there are HMOs or EPOs.

When can the self-employed enroll in health insurance?

The self-employed enroll during the annual open enrollment period, which in most states runs from November 1 to January 15, or during a special enrollment period triggered by a qualifying life event such as losing other coverage, moving, marriage, or the birth of a child. Off-exchange ACA plans follow the same windows. Outside those windows, short-term plans are the main stopgap, though they are not ACA-compliant.

Do I need an LLC or business to buy self-employed health insurance?

No. You do not need an LLC, S-corp, or registered business to buy self-employed health insurance — sole proprietors and 1099 contractors qualify for individual coverage and the self-employed health insurance deduction based on net business profit. A business entity can change how the deduction is claimed, especially for S-corp owners, but it is never a requirement for buying an individual or family plan.

Find Self-Employed Coverage That Fits

Compare self-employed health insurance for individuals and families on and off the exchange. ForHealthInsurance.com runs the comparison, checks networks, premium tax credits, and out-of-pocket costs, and completes enrollment at no extra cost.

Get a Quote Call 888-215-4045Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving individuals and families nationwide. ForHealthInsurance.com is not affiliated with HealthCare.gov, the Centers for Medicare & Medicaid Services, or any insurance carrier. The agency helps you compare PPO plans and enroll in coverage that meets your needs at no extra cost to you.