Individual Health Insurance in Louisiana: 2026 Private & Marketplace Plans

About one in nine Louisiana adults between 19 and 64 purchases individual health insurance Louisiana carriers offer — either through HealthCare.gov or directly from a carrier. This guide covers how individual coverage works in Louisiana for 2026, including the difference between on-exchange and off-exchange plans, options for self-employed residents and freelancers, and how to decide between marketplace subsidies and private plan flexibility.

What’s your situation?

On-Exchange vs. Off-Exchange Individual Plans in Louisiana

Individual health insurance Louisiana residents can buy is available both on-exchange (through HealthCare.gov) and off-exchange (purchased directly from a carrier). The key difference: premium tax credits and cost-sharing reductions are only available on-exchange. For Louisiana residents earning under 400% FPL ($60,240/individual), on-exchange plans are almost always cheaper after subsidies — during the 2025 plan year, 96% of Louisiana marketplace enrollees received an average subsidy of $593/month — 2026 amounts are lower with enhanced subsidies expired.

| Feature | On-Exchange (HealthCare.gov) | Off-Exchange (Direct from Carrier) |

|---|---|---|

| Subsidies available | Yes — premium tax credits + CSR | No subsidies available |

| Carriers in Louisiana | 5 (BCBS-LA, HMO LA, Ambetter, UHC, AmeriHealth) | BCBS-LA + additional off-exchange carriers |

| Plan types | HMO, POS, EPO | POS, PPO, indemnity options available |

| Enrollment period | OEP (Nov 1–Jan 15) or qualifying life event | OEP for ACA-compliant; year-round for non-ACA |

| Best for | Anyone earning under 400% FPL who qualifies for subsidies | Higher earners who want PPO flexibility or specific carrier access |

The trade-off is straightforward for most Louisiana residents: if you qualify for subsidies, marketplace coverage through HealthCare.gov costs less than the same plan purchased directly from the carrier. An Ambetter Silver EPO that costs $620/month off-exchange might cost $80/month after subsidies on-exchange for someone earning $30,000/year. The only scenario where off-exchange makes sense is when your income exceeds subsidy eligibility (above 400% FPL in 2026 if enhanced credits expire) and you want plan types — such as a true PPO — that are not available on the Louisiana marketplace.

Off-exchange individual plans in Louisiana are available from Blue Cross Blue Shield of Louisiana, UnitedHealthcare (Golden Rule), and through private brokers who offer plans from Cigna, Aetna, and other national carriers. These plans follow the same ACA essential health benefit requirements if they are ACA-compliant, but they may offer PPO network structures and broader provider access than the HMO and POS plans that dominate HealthCare.gov. Non-ACA-compliant plans (short-term, health sharing ministries, indemnity) are also available off-exchange but do not cover pre-existing conditions and have significant coverage limitations.

Individual Health Insurance Costs in Louisiana for 2026

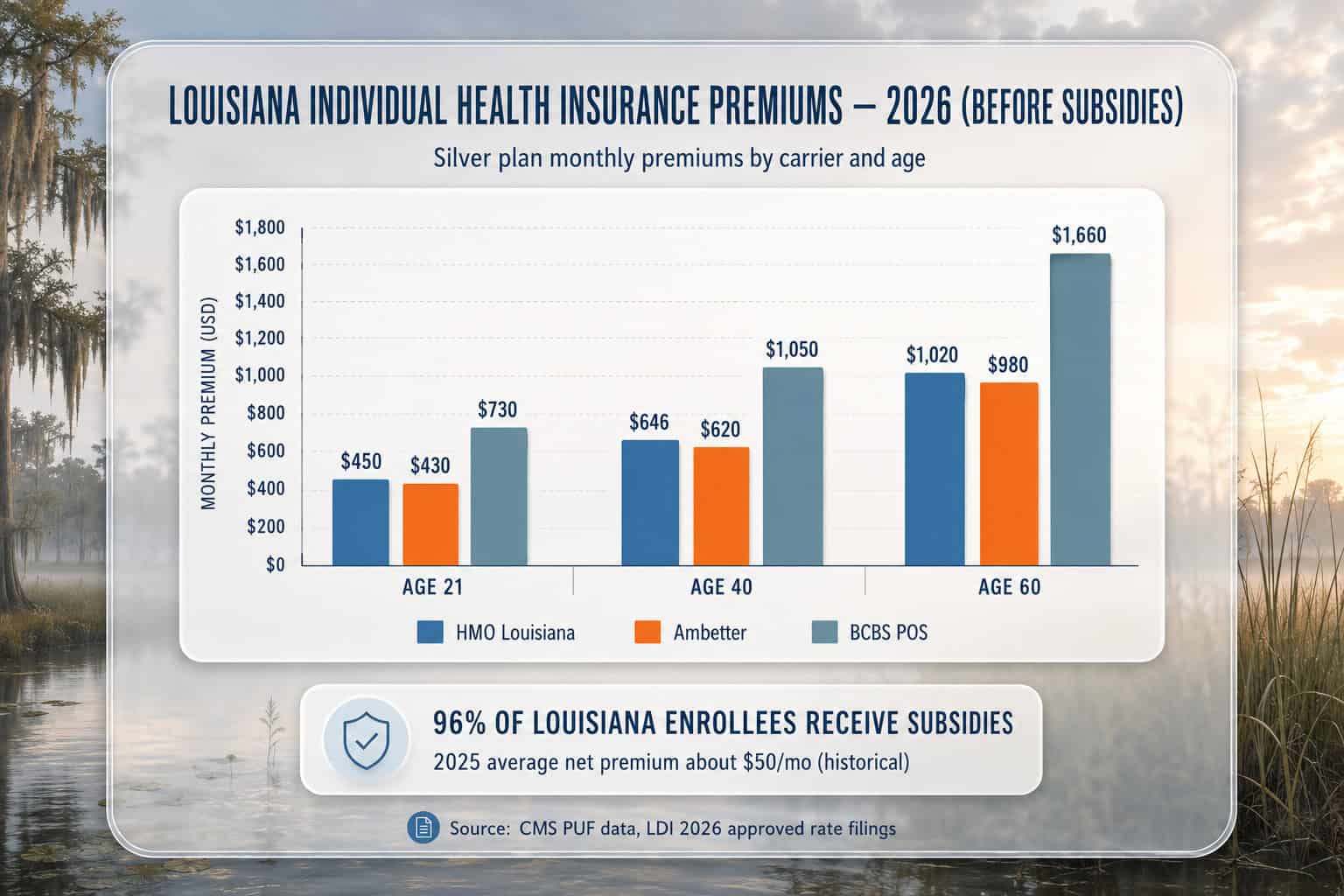

Individual health insurance in Louisiana averages approximately $685/month for a Silver plan (age 40) before subsidies — up 23.9% from 2025 per approved LDI rate filings. After subsidies, the average net premium drops to approximately $50/month. Costs vary significantly by carrier: HMO Louisiana Silver averages $646/month, Ambetter EPO Silver $620/month, and BCBS POS Silver $1,050/month — all before subsidies.

Age is the largest non-subsidy factor in individual plan pricing in Louisiana. ACA rules allow carriers to charge older enrollees up to 3x more than younger enrollees for the same plan. A 21-year-old in Caddo Parish (Shreveport) paying $410/month for an Ambetter Silver EPO would pay approximately $935/month for the same plan at age 60 — before subsidies, reflecting the ACA’s age rating curve. This age-based pricing makes subsidies especially critical for Louisiana residents over 50, where the subsidy often covers 70%–85% of the unsubsidized premium.

Example: Self-Employed Photographer in St. Tammany Parish, Age 42

A freelance photographer on the Northshore earning $48,000/year (approximately 319% FPL) enrolls in a Blue Cross Blue Connect Silver POS plan. Unsubsidized premium: approximately $1,050/month. With a premium tax credit of ~$720/month, the net cost is approximately $330/month. The self-employed health insurance deduction allows deducting the full $3,960/year in net premiums from adjusted gross income on the federal tax return — further reducing the effective cost. If this photographer’s income were $38,000/year, CSR would also apply, dropping the Silver deductible from $5,500 to roughly $2,500.

Compare Individual Health Insurance Plans in Louisiana

Five carriers offer individual health insurance Louisiana residents can compare across 64 parishes — Ambetter, BCBS-LA, HMO Louisiana, UnitedHealthcare, and AmeriHealth Caritas. Unsubsidized Silver premiums average $646–$1,050/month depending on carrier; subsidies drop the net cost to under $100/month for most enrollees.

Individual Health Insurance for Self-Employed Louisiana Residents

Self-employed individual health insurance Louisiana residents seek is available through HealthCare.gov — freelancers, 1099 contractors, gig workers, and sole proprietors can purchase coverage and qualify for the same subsidies as any other enrollee. Additionally, self-employed individuals can deduct 100% of their health insurance premiums from adjusted gross income on their federal tax return, and HSA contributions of up to $4,400/individual or $8,750/family are tax-deductible for 2026.

The self-employed health insurance deduction is an “above-the-line” deduction on Form 1040, meaning it reduces adjusted gross income regardless of whether the filer itemizes deductions. For a self-employed Louisiana resident paying $4,000/year in net premiums (after subsidies), the deduction saves roughly $600–$1,000 in combined federal and state taxes depending on the marginal tax rate. Louisiana does not have a state individual mandate, so self-employed residents who choose not to purchase coverage face no state-level tax penalty.

New for 2026: all marketplace Bronze and Catastrophic plans are now automatically considered high-deductible health plans (HDHPs), making them eligible for HSA pairing. A self-employed Louisiana resident choosing an Ambetter Expanded Bronze plan at ~$507/month before subsidies can pair it with an HSA and contribute up to $4,400/individual pre-tax. The IRS Publication 502 covers qualified medical expenses for HSA withdrawals.

LaHIPP for dual-eligible residents

Louisiana’s Health Insurance Premium Payment (LaHIPP) program reimburses premiums for Medicaid-eligible individuals who also have access to employer-sponsored or private coverage. If you qualify for both Medicaid and a private plan in Louisiana, LaHIPP can cover your premiums, copays, coinsurance, and deductibles. Contact LaHIPP at 1-877-697-6703 or visit ldh.la.gov/lahipp.

Who Buys Individual Health Insurance in Louisiana?

Approximately 307,000 Louisiana residents carry individual health insurance Louisiana carriers provide — roughly 293,000 on-exchange through HealthCare.gov and an estimated 14,000 off-exchange. The typical individual plan buyer in Louisiana is self-employed, works for a small business that does not offer group coverage, is between jobs, or is an early retiree under 65 not yet eligible for Medicare. Louisiana’s overall uninsured rate is approximately 7%, per 2023 American Community Survey data.

Self-employed & freelancers

No employer coverage available. Eligible for marketplace subsidies based on net self-employment income. Can deduct premiums above the line. Louisiana’s gig economy — including oil and gas contractors, musicians, hospitality workers, and fishing industry freelancers — drives significant individual plan enrollment in Orleans, East Baton Rouge, and Lafayette parishes.

Between jobs or transitioning

Job loss triggers a 60-day special enrollment period. Marketplace coverage through HealthCare.gov is typically cheaper than COBRA continuation for Louisiana residents who qualify for subsidies. COBRA preserves the existing employer plan but at full cost (employer + employee share) — often $600–$800/month for individual coverage.

Early retirees (under 65)

Bridge coverage between employer retirement and Medicare at 65. Private plan costs rise significantly with age — a 62-year-old in Louisiana pays roughly 2.5x what a 40-year-old pays for the same plan. Subsidies can offset most of the age-based increase for retirees with income below 400% FPL ($60,240/individual).

Post-Medicaid transition

Over 112,000 Louisiana residents moved from Healthy Louisiana Medicaid to individual marketplace plans during the post-pandemic unwinding. Former Medicaid enrollees whose income now exceeds 138% FPL ($21,597/individual) qualify for subsidized individual coverage through HealthCare.gov with a 60-day special enrollment period.

How to Choose an Individual Plan in Louisiana

Choosing the right plan in Louisiana starts with income — if you earn under 400% FPL ($60,240/individual), marketplace plans with subsidies are almost always the best value. Next, match a carrier to your parish’s hospital system: Blue Connect for Ochsner, Signature Blue for LCMC, Precision Blue for FMOLHS, or Ambetter/HMO Louisiana for the lowest premiums regardless of system alignment.

For Louisiana residents comparing individual plans, the total annual cost matters more than the monthly premium. A Bronze plan at $0/month after subsidies with a $10,600 out-of-pocket max costs up to $10,600/year if you need significant care. A Silver plan at $80/month after subsidies with CSR reducing the out-of-pocket max to $3,350 costs a maximum of $4,310/year (premiums + out-of-pocket). The Silver plan saves up to $6,290 in a worst-case year. The Affordable Health Insurance in Louisiana guide covers cost-saving strategies in detail, and the Best Health Insurance in Louisiana guide profiles each carrier’s network by region.

Individual Health Insurance FAQ for Louisiana

Common questions about individual health insurance Louisiana residents ask — including when off-exchange plans beat HealthCare.gov on cost for earners above 400% FPL ($60,240), how the self-employed deduction reduces the effective cost of the $3,960 net annual premium, how COBRA compares to subsidized marketplace coverage at $35,000 income, and how Louisiana’s 92 marketplace plans are distributed across 64 parishes.

Can I buy coverage outside of HealthCare.gov in Louisiana?

Yes. Off-exchange plans are available directly from carriers like Blue Cross Blue Shield of Louisiana and through brokers offering plans from UnitedHealthcare (Golden Rule), Cigna, and Aetna. However, off-exchange plans do not qualify for premium tax credits or cost-sharing reductions. For Louisiana residents earning under 400% FPL ($60,240/individual), on-exchange plans are almost always cheaper after subsidies.

Can self-employed people in Louisiana deduct health insurance premiums?

Yes. Self-employed Louisiana residents can deduct 100% of their health insurance premiums (net of any advance premium tax credits) as an above-the-line deduction on Form 1040. This reduces adjusted gross income regardless of itemization. For 2026, HSA contributions are also deductible up to $4,400/individual or $8,750/family, and all marketplace Bronze and Catastrophic plans now qualify as HDHPs for HSA eligibility.

Is COBRA or individual marketplace coverage cheaper in Louisiana?

For most Louisiana residents who qualify for marketplace subsidies, individual coverage through HealthCare.gov is significantly cheaper than COBRA. COBRA continuation requires paying the full premium (employer + employee share), often $600–$800/month for individual coverage. A subsidized Silver marketplace plan for someone earning $35,000/year might cost $60–$100/month after credits. COBRA makes sense only when the employer plan has unique network value or when income exceeds subsidy eligibility.

How many marketplace plans are available in Louisiana?

According to CMS data, approximately 92 marketplace plans are available in Louisiana for 2026 across five carriers. The exact number in your parish depends on which carriers serve your area — metro parishes like Orleans and East Baton Rouge may have 40+ plan options, while rural parishes may have 15–20. Off-exchange plans add additional options beyond the marketplace count.

What is LaHIPP and how does it help with individual coverage?

The Louisiana Health Insurance Premium Payment (LaHIPP) program reimburses premiums for Medicaid-eligible individuals who also have employer or private coverage. If you qualify for both Medicaid and a private plan, LaHIPP can cover your premiums, copays, and deductibles. Contact LaHIPP at 1-877-697-6703 or visit ldh.la.gov/lahipp to apply.

Louisiana Health Insurance Resources

Complete 2026 overview — carriers, costs, Medicaid, and enrollment

Marketplace & Enrollment GuideHealthCare.gov enrollment, deadlines, and plan comparison

Best Louisiana Health InsuranceCompare BCBS, Ambetter, UHC, and AmeriHealth by parish

Affordable Coverage & SubsidiesTax credits, CSR savings, and low-cost plan options

Short-Term Health InsuranceTemporary and bridge coverage options in Louisiana

Small Business Group PlansGroup coverage, SHOP enrollment, and ICHRA options

Get Louisiana QuotesCompare 2026 plans and prices for your household

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals

Find Individual Health Insurance in Louisiana

Compare individual health insurance Louisiana carriers offer across all 64 parishes — Ambetter HMO, BCBS Blue Connect, HMO Louisiana, UnitedHealthcare, and AmeriHealth. During the 2025 plan year, 96% of Louisiana enrollees paid under $100/month after subsidies.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Louisiana residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.