Short-Term Health Insurance in Louisiana: 2026 Temporary Coverage Guide

Short-term health insurance in Louisiana provides temporary coverage for residents facing a gap between plans — whether due to job transitions, aging off a parent’s plan, or missing open enrollment. These plans are available year-round but come with significant limitations compared to ACA-compliant marketplace coverage. This guide covers what Louisiana’s short-term plans include, what they exclude, how much they cost, and when a marketplace plan is the better choice.

What’s your coverage gap?

How Short-Term Health Insurance Works in Louisiana

Short-term health insurance in Louisiana follows federal duration limits — a maximum initial term of 3 months with one 1-month renewal for a total of 4 months. Louisiana does not impose its own state-level short-term duration restrictions beyond the federal rule. At least six insurers offered short-term plans in Louisiana as of 2024, including UnitedHealthcare (Golden Rule), the largest short-term carrier in the state.

| Feature | Short-Term Plan (Louisiana) | ACA Marketplace Plan |

|---|---|---|

| Maximum duration | 3 months initial + 1 month renewal = 4 months total | 12 months (annual renewal) |

| Pre-existing conditions | Not covered; medical underwriting required | Fully covered; guaranteed issue |

| Essential health benefits | Not required — many excluded (maternity, mental health, Rx) | All 10 EHBs required |

| Subsidies available | No — full price only | Yes — during 2025 OEP, 96% of LA enrollees qualified |

| Enrollment period | Year-round; coverage can start next day | OEP (Nov 1–Jan 15) or qualifying life event |

| Typical monthly premium (age 28, New Orleans) | ~$100–$180/month | ~$475/month before subsidies; ~$40–$80 after subsidies |

Short-term plans in Louisiana are medically underwritten — the insurer reviews your health history and can deny coverage or exclude specific conditions. Louisiana has no state protections beyond federal rules: at least six carriers offered these plans as of 2024, with premiums starting around $100/month for healthy applicants in their 20s. Plans generally cover doctor visits, emergency room visits, and surgery for new injuries or illnesses but exclude prescription drugs, maternity care, mental health services, and preventive care — benefits all five Louisiana marketplace carriers are required to provide.

Federal rule change (September 2024)

Short-term plans issued or sold on or after September 1, 2024, are limited to a maximum of 4 months total including renewals. Louisiana follows this federal rule — there is no state law extending the duration. Previous rules allowed plans up to 12 months with renewals up to 36 months. Existing plans issued before September 2024 may still have longer terms. Confirm the duration with the carrier before purchasing.

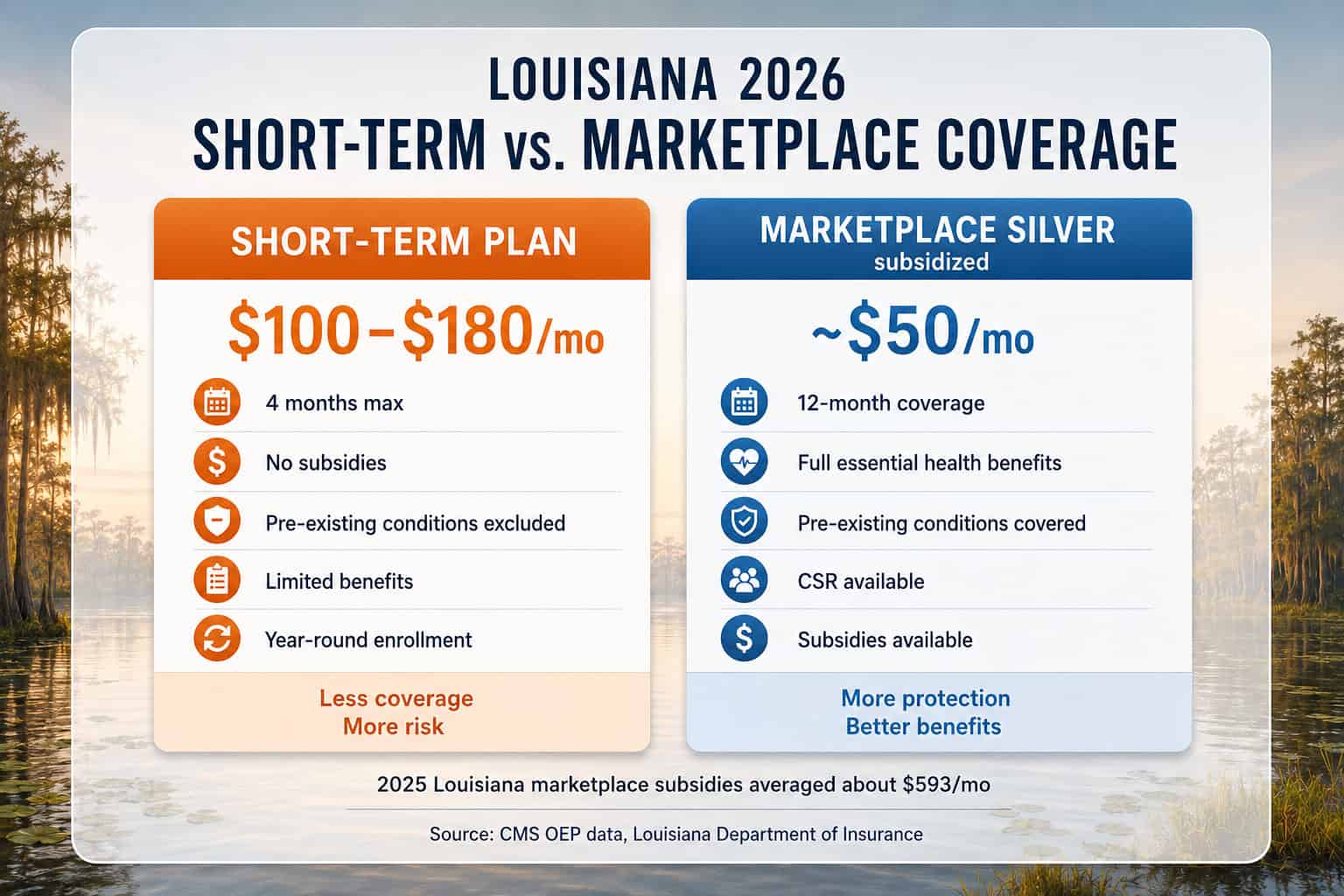

Short-Term vs. Marketplace Plans in Louisiana

For most Louisiana residents, marketplace plans through HealthCare.gov are a better value than short-term health insurance — even if the monthly premium appears higher. A subsidized Silver marketplace plan in Louisiana averaged approximately $50/month after the $593/month average subsidy during the 2025 plan year, covers all essential health benefits, and cannot deny coverage for pre-existing conditions. Short-term plans cost $100–$180/month with no subsidies and exclude many common medical needs.

The cost comparison shifts dramatically based on subsidy eligibility. A 28-year-old in Orleans Parish earning $30,000/year would pay approximately $140/month for a UHC Golden Rule short-term plan that excludes pre-existing conditions, prescription drugs, and mental health care — and expires after 4 months. At 2025 subsidy levels, the same person would have qualified for approximately $500/month in marketplace subsidies, bringing an Ambetter Silver EPO to roughly $35/month with full essential health benefit coverage and no pre-existing condition exclusions. The marketplace plan costs less, covers more, and lasts 12 months.

Short-term health insurance in Louisiana makes financial sense only when the enrollee does not qualify for marketplace subsidies (income above 400% FPL or $60,240/individual in 2026 if enhanced credits expire), has no pre-existing conditions, and needs coverage for a defined short period — such as 2 months between jobs. In every other scenario, a marketplace plan through HealthCare.gov is likely cheaper and more protective. The Louisiana Marketplace Enrollment Guide covers how to enroll, and the HealthCare.gov application determines subsidy eligibility in minutes.

For most Louisiana residents who qualify for subsidies, the numbers favor the marketplace: a 28-year-old in Orleans Parish earning $30,000 pays roughly $140/month for 4-month short-term coverage with no Rx or mental health benefits, versus approximately $35/month for a full-year Ambetter Silver EPO through HealthCare.gov at 2025 subsidy levels.

Compare Short-Term and Marketplace Plans in Louisiana

For a 28-year-old in Orleans Parish earning $30,000, a 4-month UHC Golden Rule short-term plan costs roughly $140/month with no prescription coverage — while a subsidized Ambetter Silver EPO costs approximately $35/month and covers all essential health benefits. Enter your parish and income to see your specific comparison.

Who Should Consider Short-Term Health Insurance in Louisiana?

Short-term health insurance in Louisiana is for healthy individuals with a temporary gap — typically 1–4 months — who earn above 400% FPL ($60,240/individual) and have no pre-existing conditions. Louisiana has no state individual mandate and no tax penalty for using short-term coverage. For the roughly 293,000 Louisiana residents who enrolled on the marketplace in 2025, a subsidized plan was almost always cheaper — short-term only makes sense for the narrow slice above the subsidy threshold.

Between jobs (no qualifying life event)

If you left a job voluntarily and your coverage ended, you have a 60-day window to enroll in a marketplace plan via qualifying life event. If that window has passed and open enrollment is months away, a 3-month short-term plan bridges the gap. Louisiana residents who lost coverage involuntarily (layoff, termination) always have a QLE — marketplace is the better path.

Recent graduate aging off parent’s plan

Coverage under a parent’s plan ends at age 26. If the birthday falls outside open enrollment and the graduate doesn’t have employer coverage, losing parent coverage triggers a 60-day SEP for marketplace enrollment. Short-term is only needed if that 60-day window was missed — otherwise, a subsidized marketplace plan is cheaper and more comprehensive for most Louisiana residents.

Waiting for employer coverage to start

Many Louisiana employers impose a 60–90 day waiting period before group coverage begins. A 2–3 month short-term plan covers the gap. At ~$130/month for a healthy applicant in the Baton Rouge area, this costs $260–$390 total — reasonable catastrophic protection during the waiting period. Confirm the short-term plan end date aligns with your group coverage start date.

High earners who don’t qualify for subsidies

Louisiana residents earning above 400% FPL ($60,240/individual) who face a coverage gap may find short-term plans cheaper than unsubsidized marketplace premiums. A $140/month short-term plan vs. a $620/month unsubsidized Ambetter Silver EPO saves $480/month — but only if the enrollee is healthy and needs coverage for 4 months or less. Pre-existing conditions make this option unavailable.

What Short-Term Plans Don’t Cover in Louisiana

Short-term health insurance plans in Louisiana are exempt from ACA essential health benefit requirements — unlike the five marketplace carriers serving Louisiana’s 64 parishes, which must cover all 10 EHBs. Most short-term plans exclude prescription drugs, maternity care, mental health services, preventive care, and rehabilitative services. Dollar limits on annual and lifetime benefits are permitted, which means a Louisiana resident with a $300/month brand-name medication pays full cost out of pocket.

| Coverage Area | Short-Term Plan (Typical) | ACA Marketplace Plan |

|---|---|---|

| Pre-existing conditions | Excluded | Fully covered |

| Prescription drugs | Usually excluded or severely limited | Covered (formulary applies) |

| Maternity care | Excluded | Covered as essential health benefit |

| Mental health / substance abuse | Excluded | Covered at parity with medical |

| Preventive care | Not covered or limited | Free preventive services in-network |

| Annual / lifetime benefit limits | Permitted (e.g., $1M or $2M lifetime max) | Prohibited — no dollar limits |

The exclusion list makes short-term health insurance in Louisiana unsuitable for anyone who takes ongoing medications, has a chronic condition, is pregnant or planning to become pregnant, or needs mental health services. A Louisiana resident taking a $300/month brand-name medication would pay full cost out of pocket on a short-term plan — effectively adding $300 to the monthly premium and making the plan more expensive than a subsidized marketplace Silver plan that covers prescriptions. According to CMS enrollment data, over four in five Louisiana marketplace enrollees earn below $37,650/year, making subsidized ACA plans cheaper than short-term for the vast majority of the state’s uninsured population.

No state penalty in Louisiana

Louisiana has no individual mandate — there is no state or federal tax penalty for carrying short-term coverage instead of ACA-compliant insurance. However, short-term plans do not count as “minimum essential coverage” and purchasing one during open enrollment does not satisfy the requirement for subsidized marketplace coverage. If you buy short-term during OEP and later want a marketplace plan, you must wait for the next OEP or a qualifying life event.

Alternatives to Short-Term Health Insurance in Louisiana

Before purchasing short-term health insurance in Louisiana, check whether you qualify for Medicaid through Healthy Louisiana (income up to 138% FPL, year-round enrollment), a marketplace special enrollment period (60 days after losing other coverage), COBRA continuation from a former employer, or the new expanded catastrophic plan eligibility for 2026 that extends access to anyone not eligible for marketplace subsidies.

Marketplace special enrollment

Losing other coverage, moving to a new Louisiana parish, getting married, or having a child triggers a 60-day SEP. Over 112,000 Louisiana residents used the Medicaid-to-marketplace SEP during the Healthy Louisiana unwinding. If you have a qualifying event, a marketplace plan with subsidies is almost always cheaper than short-term coverage.

Catastrophic plans (expanded for 2026)

New for 2026: catastrophic plans on HealthCare.gov are available to anyone with a hardship exemption — including individuals who earn too much for subsidies. Catastrophic plans in Louisiana have premiums around $320/month with a $10,600 deductible and cover three primary care visits before the deductible. They are ACA-compliant, cover pre-existing conditions, and last 12 months.

COBRA continuation coverage is another alternative for Louisiana residents who recently left an employer with group health insurance. Louisiana law requires businesses with 2–19 employees to offer 12 months of COBRA continuation, while federal COBRA applies to businesses with 20+ employees for up to 18 months. COBRA means paying the full combined cost — what you paid plus what your employer contributed — typically running $600–$800/month for a single employee in Louisiana. For residents who qualify for marketplace subsidies, a subsidized plan is significantly cheaper than COBRA. The Affordable Health Insurance in Louisiana guide covers all low-cost options.

Louisiana Health Insurance Resources

Complete 2026 overview — carriers, costs, Medicaid, and enrollment

Marketplace & Enrollment GuideHealthCare.gov enrollment, deadlines, and plan comparison

Best Louisiana Health InsuranceCompare BCBS, Ambetter, UHC, and AmeriHealth by parish

Affordable Coverage & SubsidiesTax credits, CSR savings, and low-cost plan options

Small Business Group PlansGroup coverage, SHOP enrollment, and ICHRA options

Get Louisiana QuotesCompare 2026 plans and prices for your household

Individual Health InsurancePrivate and off-exchange plans for Louisiana individuals

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals

Short-Term Health Insurance FAQ for Louisiana

Common questions about temporary health insurance in Louisiana — including federal duration limits, what short-term plans exclude, carrier options like UHC Golden Rule, and how they compare to marketplace and Medicaid coverage for 2026.

How long can a short-term health insurance plan last in Louisiana?

Louisiana follows federal rules: short-term plans issued on or after September 1, 2024, are limited to a 3-month initial term with one 1-month renewal for a total of 4 months. Plans cannot be “stacked” — purchasing consecutive policies from the same carrier or affiliated carriers within 12 months is prohibited. Existing plans issued before September 2024 may have longer terms under the previous rules.

Does Louisiana require health insurance?

No. Louisiana has no state individual mandate, and the federal penalty for being uninsured was eliminated in 2019. There is no tax penalty for having short-term coverage instead of an ACA-compliant plan. However, short-term plans do not count as minimum essential coverage and are not eligible for premium tax credits or cost-sharing reductions available through HealthCare.gov.

Is short-term cheaper than marketplace coverage in Louisiana?

Usually not, if you qualify for subsidies. Short-term plans cost approximately $100–$180/month for a healthy applicant with no subsidies. A subsidized marketplace Silver plan in Louisiana averaged approximately $50/month after subsidies during the 2025 plan year — 2026 net costs are higher with enhanced subsidies expired. Short-term is only cheaper for Louisiana residents earning above 400% FPL ($60,240/individual) who do not qualify for marketplace subsidies and have no pre-existing conditions.

What carriers offer short-term plans in Louisiana?

At least six insurers offered short-term plans in Louisiana as of 2024. UnitedHealthcare (Golden Rule Insurance Company) is the largest short-term carrier nationally and offers plans in Louisiana. The Louisiana Department of Insurance maintains information on approved carriers. Short-term plans are medically underwritten — applicants can be denied based on health history.

Can I get short-term insurance if I have a pre-existing condition?

Likely not. Short-term plans in Louisiana are medically underwritten, and insurers can deny coverage for applicants with pre-existing conditions such as diabetes, heart disease, cancer, HIV/AIDS, or recent surgeries. If you have a pre-existing condition, Healthy Louisiana Medicaid (income up to 138% FPL) or a marketplace plan through HealthCare.gov — both guaranteed-issue — are the appropriate options. Neither can deny coverage for health status.

Find the Right Temporary Coverage in Louisiana

During the 2025 plan year, 96% of Louisiana marketplace enrollees paid an average of $50/month after subsidies — far less than the $100–$180/month short-term plans cost without any subsidy assistance. Enter your parish and income to compare both options and see your 2026 cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Louisiana residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.