Individual Health Insurance in Michigan: Your 2026 Guide to Buying Your Own Coverage

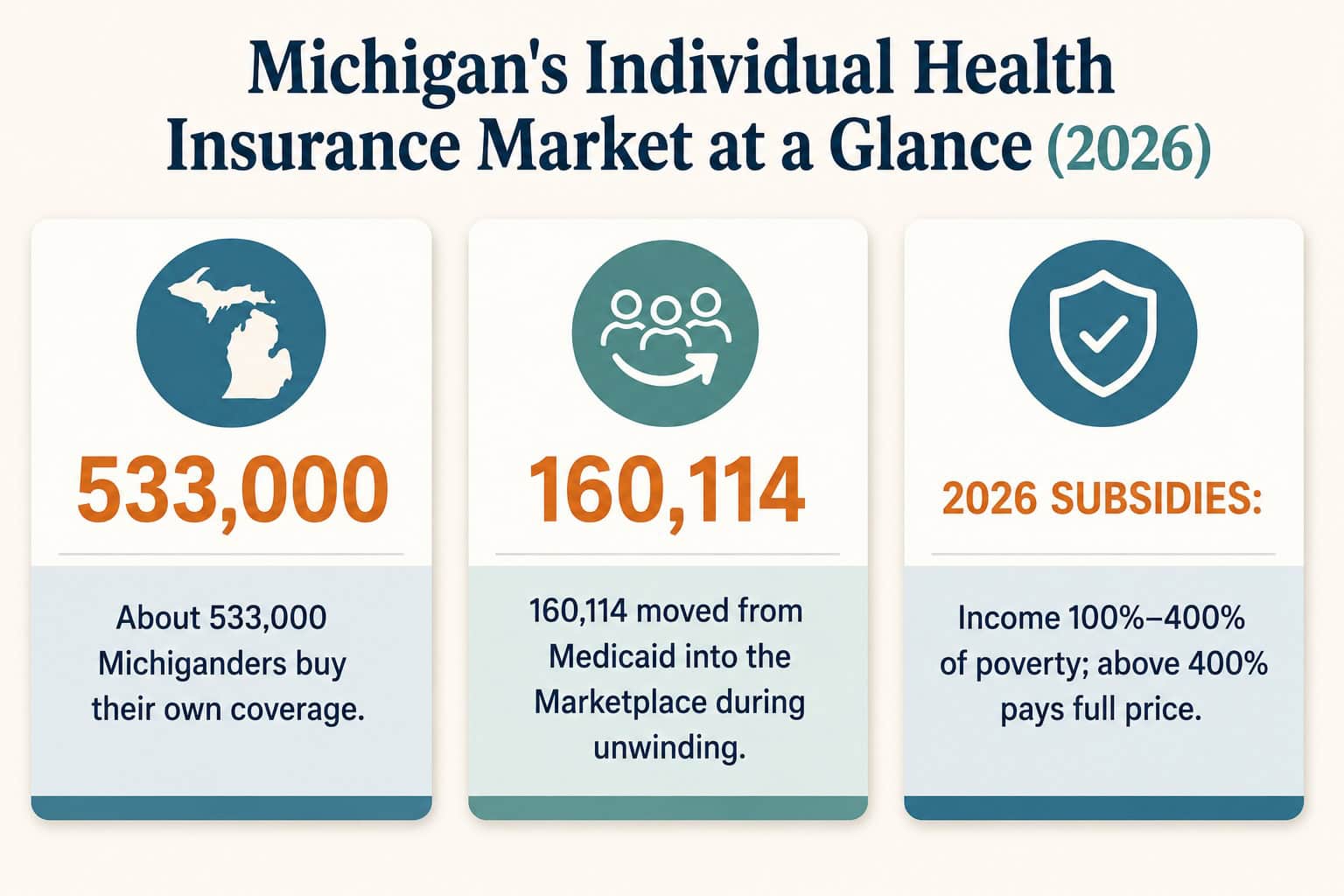

Individual health insurance in Michigan is coverage you buy for yourself rather than getting it through an employer. About 533,000 Michiganders are in the individual market. You enroll through HealthCare.gov during open enrollment or after a qualifying life event, and this guide walks through who needs it, how to enroll, and what subsidies remain for 2026.

Who Needs Individual Health Insurance in Michigan?

You need individual health insurance in Michigan if you do not get coverage through an employer, Medicare, or Medicaid — including the self-employed, gig and contract workers, early retirees, and anyone between jobs. Roughly 533,000 Michiganders buy their own coverage, and 160,114 moved into this market from Medicaid during the recent eligibility unwinding.

An individual plan in Michigan is the same ACA-regulated coverage sold on the Marketplace, just purchased by you rather than an employer. It covers the ten essential health benefits, cannot deny you for pre-existing conditions, and renews each year. If your employer offers affordable coverage, that is usually the better route; if not, an individual plan is how you stay insured.

Self-employed & freelancers

Business owners, gig workers, and contractors without a group plan make up a large share of Michigan’s individual market.

No employer coverage

Part-time workers or employees whose job does not offer health benefits buy individual coverage instead.

Early retirees

Retired before 65 and not yet Medicare-eligible? An individual plan bridges the gap until you qualify.

Between jobs

Losing job-based coverage triggers a Special Enrollment Period to buy an individual plan in Michigan.

How to Enroll in Individual Health Insurance in Michigan

Michigan uses the federal Marketplace, so you enroll in individual coverage through HealthCare.gov, not a state exchange. Open enrollment runs each fall — November 1 to December 15 for 2026 coverage under the new shorter federal window. Outside that window, you need a qualifying life event to enroll.

To buy an individual plan, create or log in to your account at HealthCare.gov, enter your Michigan ZIP code and household income, and compare the plans available in your county. A qualifying life event — losing coverage, moving, marriage, or a new baby — opens a 60-day Special Enrollment Period so you can enroll outside open enrollment.

Open enrollment is shorter now. A recent federal change moved the deadline up by about a month, ending December 15 in every state instead of January 15. If you miss it without a qualifying life event, you generally cannot buy individual coverage until the next fall — so mark the date.

Subsidies for Individuals in Michigan in 2026

For 2026, the enhanced premium tax credits that boosted subsidies since 2021 have expired, so Michigan subsidies reverted to the ACA’s original rules: households between 100% and 400% of the federal poverty level can qualify, while those above 400% now pay full price. Michigan adds no state subsidy of its own, and individual premiums rose a state-approved 20.2% this year.

Subsidies still exist — they are just smaller, and the income cap returned. When you apply for an individual plan, HealthCare.gov calculates your premium tax credit from your estimated income. Because the math changed for 2026, it is worth re-checking your subsidy even if you were covered last year.

| Your household income | 2026 subsidy status in Michigan |

|---|---|

| Under 100% FPL | May qualify for Healthy Michigan Plan (Medicaid) instead |

| 100%–250% FPL | Premium tax credit plus cost-sharing reductions on Silver plans |

| 250%–400% FPL | Premium tax credit, no cost-sharing reductions |

| Over 400% FPL | No subsidy for 2026 — pays full premium |

See Your Individual Plan Options

Compare individual plans in Michigan and any subsidy you qualify for, in minutes.

Individual Coverage for Self-Employed Michiganders

The self-employed are the core buyers of individual health insurance in Michigan. If you run your own business or work as a contractor, you can buy an individual plan on HealthCare.gov and may deduct your premiums on your federal taxes. Nationally, more than 80% of self-employed and small-business owners have claimed the premium tax credit.

Being self-employed does not change the plans available — you choose from the same Michigan individual market — but it does affect the tax side. Talk to a tax professional about the self-employed health insurance deduction, which can lower the true cost of your coverage. If you have employees, a group plan may be worth comparing instead; see Michigan small business coverage.

How to Choose Your Individual Plan in Michigan

Choosing individual health insurance in Michigan comes down to network, drug coverage, and total cost. Three hospital systems control about 64% of the state’s market, so confirm your doctors are in-network first, then compare metal tiers and premiums. Match the plan to how much care you expect to use over the year.

Start with the network, then the formulary, then the full 2026 cost — premium, deductible, and out-of-pocket maximum together. To understand how plan types and tiers are structured, see Michigan plan types and metal tiers; to compare carriers, see the health insurance companies in Michigan.

Example — a Traverse City freelancer. A self-employed designer earning about 350% of the poverty level still qualifies for a premium tax credit in 2026, so she compares Silver and Gold plans that include her Traverse City clinic, then picks the one with the lowest total yearly cost. For lower-cost options, she checks affordable Michigan plans.

Related Michigan Health Insurance Resources

The statewide guide to 2026 plans, costs, and how coverage works in Michigan.

Michigan Marketplace & SubsidiesHow HealthCare.gov works for Michigan and who qualifies for premium tax credits.

Michigan Health Insurance PlansPlan types, metal tiers, and how Michigan coverage is structured.

Michigan Health Insurance CompaniesWho the insurers are, their networks, and where they operate across Michigan.

Private Health Insurance MichiganOff-exchange private plans, including PPO options, for buyers without subsidies.

Affordable Health Insurance MichiganLower-cost 2026 options and ways to reduce your monthly premium.

Small Business Health Insurance MichiganGroup coverage options if you have employees rather than buying solo.

Michigan Health Insurance QuotesCompare personalized 2026 plan pricing for your ZIP code in minutes.

Frequently Asked Questions About Individual Health Insurance in Michigan

What is individual health insurance in Michigan?

Individual health insurance in Michigan is ACA-regulated coverage you buy for yourself through HealthCare.gov instead of getting it from an employer. It covers essential health benefits, cannot deny you for pre-existing conditions, and is the main option for the self-employed and people without job-based coverage.

How do I get individual health insurance in Michigan?

You enroll through HealthCare.gov, since Michigan uses the federal Marketplace. Open enrollment runs from November 1 to December 15 for 2026 coverage. Outside that window, a qualifying life event such as losing coverage, moving, or having a baby opens a 60-day Special Enrollment Period.

Can I still get a subsidy for individual coverage in 2026?

Yes, but the enhanced subsidies expired. For 2026, premium tax credits follow the ACA’s original rules: households between 100% and 400% of the federal poverty level can qualify, while those above 400% pay full price. Michigan does not add a state subsidy.

Is individual health insurance good for the self-employed in Michigan?

Yes. The self-employed are the core buyers of this coverage, and premiums may be deductible on your federal taxes. You choose from the same Michigan individual plans as everyone else, so focus on network fit and total cost.

How much does individual coverage cost in Michigan?

It depends on your age, county, plan tier, and any subsidy. Michigan individual premiums rose a state-approved 20.2% for 2026, so compare total cost — premium plus deductible and out-of-pocket maximum — rather than premium alone. A quote shows your exact price after subsidies.

Ready to Buy Your Own Coverage?

Compare individual coverage in Michigan and enroll with help from a licensed agent — at no extra cost to you.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Michigan residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.