Michigan Health Insurance Marketplace: 2026 HealthCare.gov Enrollment Guide

The Michigan health insurance marketplace operates through HealthCare.gov, the federally-facilitated exchange for the 30+ states without a state-based marketplace. Michiganders use the same federal portal as residents of Texas, Florida, and other federal-marketplace states, but with seven Michigan-specific carriers — down from ten in 2025 — and Michigan-approved rate filings. This guide covers how the federal exchange works for Michigan residents in 2026, who qualifies for subsidies, when Open Enrollment runs, and how to enroll without missing the deadline.

Where are you in the enrollment process?

How the Michigan Health Insurance Marketplace Works

The Michigan health insurance marketplace is operated by the federal government through HealthCare.gov, not by the state of Michigan directly. Michigan opted not to build its own state-based exchange when the Affordable Care Act launched, so all individual marketplace enrollment, plan shopping, and subsidy applications happen on the federal platform. The Michigan Department of Insurance and Financial Services (DIFS) regulates carrier rates and plan filings, while HealthCare.gov handles consumer-facing enrollment.

For 2026, seven carriers offer plans on HealthCare.gov for Michigan residents: Blue Cross Blue Shield of Michigan, Blue Care Network, Priority Health, Meridian Health Plan (Ambetter), McLaren Health Plan, Oscar Health, and UnitedHealthcare Community Plan. Plan availability varies dramatically by county — Detroit metro residents typically see all seven carriers while Upper Peninsula residents may have only two. The exchange displays each plan with the same standardized information (premium, deductible, out-of-pocket maximum, network type, covered drug list) to allow apples-to-apples comparison.

HealthCare.gov also screens for Healthy Michigan Plan and Medicaid eligibility during the application process. Households earning under 138% of the Federal Poverty Level are routed to the Michigan Department of Health and Human Services for Medicaid enrollment instead of being shown marketplace plans. This single-portal eligibility check prevents Michiganders from accidentally enrolling in marketplace coverage when they qualify for free Medicaid.

How to Enroll in a Michigan Marketplace Plan for 2026

Enrolling through the Michigan health insurance marketplace involves five steps: create or log into a HealthCare.gov account, complete the eligibility application with household and income information, review available plans from the seven Michigan carriers in your county, select a plan, and pay the first month’s premium to activate coverage. The entire process typically takes 30–60 minutes for a first-time enrollee with all required information ready.

Gather required information

Have ready: Social Security numbers for everyone in the household, employer and income details, current health insurance information (if any), and projected 2026 household income. Self-employed Michiganders should have their best income estimate based on prior-year returns and expected changes.

Create a HealthCare.gov account

Visit HealthCare.gov and create an account or log in to your existing one. The federal portal serves all Michiganders applying for marketplace coverage. You’ll verify your identity through Experian’s verification system — most enrollees clear this step in under five minutes.

Complete the eligibility application

Enter household composition, projected income, and current coverage status. The application screens for Medicaid, Healthy Michigan Plan, and CHIP eligibility automatically. If you’re routed to MDHHS for Medicaid, you can complete that application separately. If you qualify for marketplace subsidies, the system calculates your estimated premium tax credit.

Compare and select a plan

Filter by metal tier (Bronze, Silver, Gold, Platinum), carrier, premium range, deductible, and total annual cost. Verify your doctors and prescription drugs are in-network for any plan you’re considering. Subsidized enrollees should focus on after-subsidy cost rather than sticker price. To compare the carriers head-to-head before you filter, see the Michigan carrier ranking guide.

Pay first premium and activate

Coverage activates only when the carrier receives your first premium payment, not when you select the plan on HealthCare.gov. Most carriers require payment within 30 days. After payment, ID cards arrive within 7–14 days and you can begin using your coverage on the effective date.

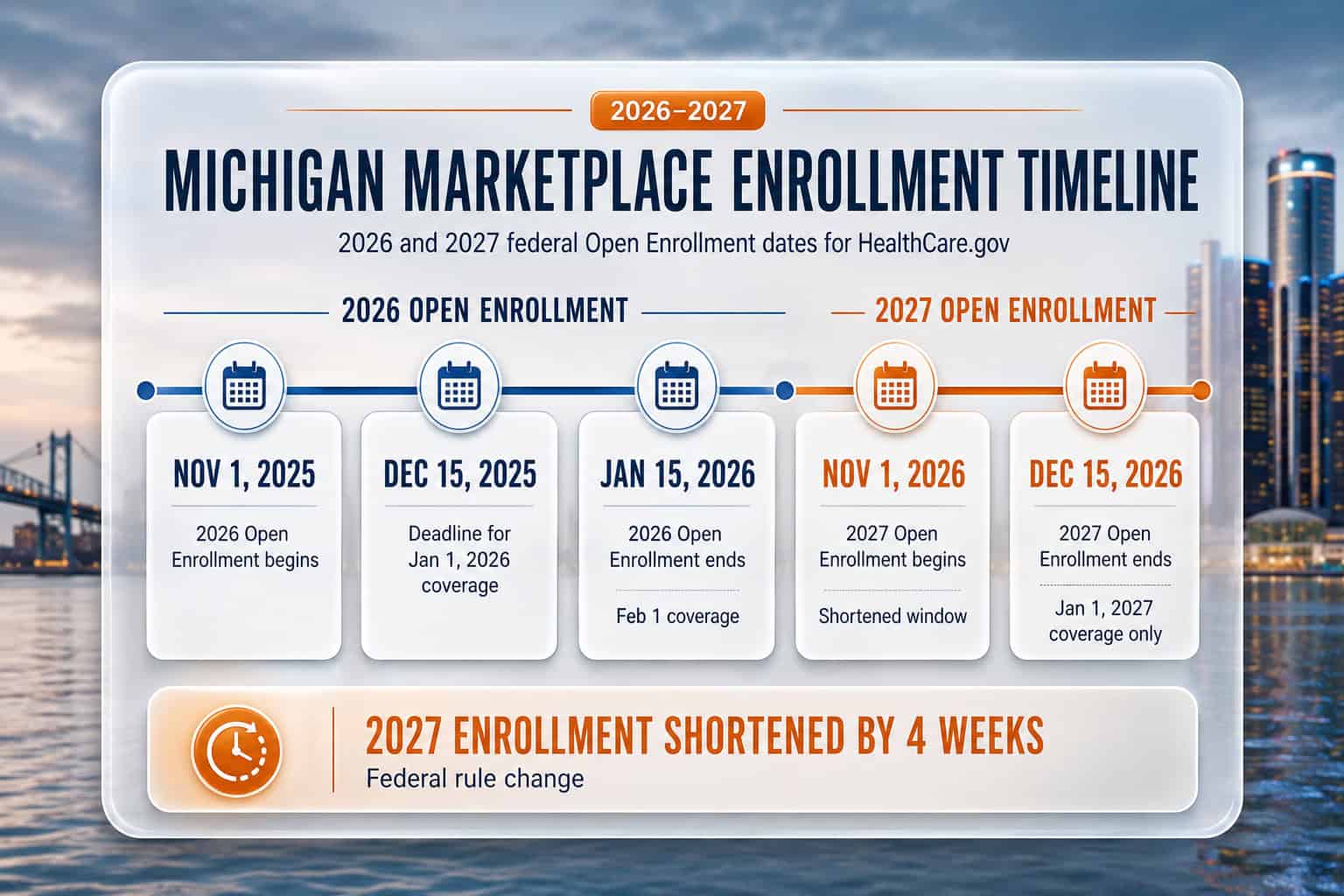

Michigan Marketplace Open Enrollment Dates

Open Enrollment for 2026 Michigan marketplace coverage ran November 1, 2025 through January 15, 2026. For 2027 coverage, the federal government shortened the window to November 1 through December 15, 2026 — six weeks instead of the previous ten-week period. All plans selected during the 2027 enrollment window will take effect January 1, 2027. There is no automatic renewal; every household must actively confirm or change their plan and update income information.

| Plan Year | Open Enrollment Window | Coverage Effective |

|---|---|---|

| 2026 (current) | Nov 1, 2025 – Jan 15, 2026 | Jan 1 or Feb 1, 2026 |

| 2027 (upcoming) | Nov 1 – Dec 15, 2026 | Jan 1, 2027 |

| Special Enrollment | 60 days from Qualifying Life Event | First of following month |

| Medicaid / Healthy Michigan Plan | Year-round (no OEP restriction) | Within 45 days of approval |

Shorter 2027 enrollment window: The federal rule change shortens Open Enrollment by approximately four weeks starting with the 2027 plan year. December 15, 2026 is the absolute deadline for 2027 marketplace coverage — no extensions and no January enrollment window. Michiganders who miss December 15 without a Qualifying Life Event will be uninsured until the 2028 Open Enrollment window. Mark calendars early.

Special Enrollment Periods for Michigan Marketplace Plans

Special Enrollment Periods (SEPs) allow Michigan marketplace enrollment outside the annual Open Enrollment window when a Qualifying Life Event occurs. Common Michigan SEP triggers include marriage, birth or adoption of a child, loss of other coverage (job-based plan ending, COBRA expiring, aging off a parent’s plan at 26), losing Healthy Michigan Plan eligibility, moving to Michigan, or becoming a U.S. citizen. SEPs typically allow 60 days from the qualifying event to enroll.

Qualifying Life Events that trigger SEP

Marriage, birth, adoption, divorce, death of family member, loss of job-based coverage, loss of Medicaid or Healthy Michigan Plan, moving to Michigan from another state, becoming a U.S. citizen, leaving incarceration. Documentation of the event is typically required.

Events that do NOT trigger SEP

Voluntarily dropping coverage, missing payments and losing coverage, changing your mind about a plan you selected, getting fired and refusing COBRA. These do not qualify — Michiganders in these situations typically wait until the next Open Enrollment.

Get Help Enrolling in Michigan Marketplace Plans

Free, licensed assistance with Michigan marketplace enrollment. A licensed broker helps you compare carriers, check subsidy eligibility, and avoid common enrollment mistakes that cost time and money.

Renewing Michigan Marketplace Coverage for 2026 and Beyond

Michigan marketplace plans do not automatically renew with subsidies preserved. Every enrollee must actively log into HealthCare.gov each year, update household income and composition, and confirm or change their plan. For 2026 specifically, this was critical because three carriers (Molina, HAP CareSource, UM Health Plan) exited the market — auto-renewal would have placed displaced enrollees into a different carrier without their explicit selection. Active renewal ensures the right plan and the correct subsidy amount.

The renewal process is shorter than initial enrollment. Returning enrollees verify income (which determines 2026 subsidy amounts), confirm household members, review plan availability for the upcoming year, and either renew the same plan if available or select a new one. Income changes since the prior year — promotions, job loss, self-employment income shifts — must be reported because they directly affect premium tax credit calculations. Underestimating income means paying too little upfront and owing back at tax time; overestimating means paying more than necessary throughout the year.

Subsidies and Premium Tax Credits on the Michigan Marketplace

Approximately 90% of Michigan marketplace enrollees receive premium tax credits, with average savings of more than $380/month per enrollee. Subsidies scale by household income and the cost of the benchmark Silver plan in your county. A Wayne County resident earning $35,000 typically qualifies for approximately $380/month in premium tax credits, bringing a Silver plan from $486/month to about $106/month after subsidy.

Two types of financial assistance flow through the Michigan health insurance marketplace: Premium Tax Credits (which lower monthly premiums) and Cost-Sharing Reductions (which lower deductibles and copays for enrollees under 250% FPL who choose Silver plans). Enhanced subsidies enacted under the American Rescue Plan and extended by the Inflation Reduction Act expanded eligibility above 400% FPL — but are scheduled to revert to pre-2021 rules without Congressional extension. The IRS Premium Tax Credit rules govern how subsidies reconcile at tax time. The affordable coverage guide details subsidy eligibility by household size and income.

Example: Grand Rapids Family of 4, $68,000 Income

A Grand Rapids family of four (two adults ages 38, two children) earning $68,000/year is at approximately 211% FPL. Their estimated 2026 marketplace options: Priority Health Silver family plan at approximately $1,280/month full price minus approximately $920/month in premium tax credits = about $360/month after subsidy. A Bronze plan would run closer to $190/month after the same subsidy but with a higher deductible. Because the household is under 250% FPL, the Silver plan also qualifies for cost-sharing reductions that lower deductibles and copays significantly.

Frequently Asked Questions About the Michigan Marketplace

Where do I sign up for the Michigan health insurance marketplace?

Michigan residents enroll through HealthCare.gov, the federal marketplace. Michigan does not operate its own state-based exchange. The HealthCare.gov platform handles all aspects of enrollment — eligibility screening, plan comparison, subsidy calculation, and plan selection. Free, licensed enrollment assistance is also available through brokers and Navigators.

When is Michigan marketplace Open Enrollment?

Open Enrollment for 2026 Michigan marketplace coverage ran November 1, 2025 through January 15, 2026. For 2027 coverage, the window is shortened to November 1 through December 15, 2026 — about six weeks. Outside Open Enrollment, a Qualifying Life Event is needed to enroll. Healthy Michigan Plan and Medicaid allow year-round enrollment.

How do I qualify for Michigan marketplace subsidies?

Subsidy eligibility is determined by household income relative to the Federal Poverty Level. Households earning between 100% and 400% FPL typically qualify for premium tax credits — approximately $15,650 to $62,600 for a single adult or $32,150 to $128,600 for a family of four in 2026 reference figures. Enhanced subsidies extended eligibility above 400% FPL through 2025, but federal extension for 2026 and beyond is uncertain.

Can I enroll in a Michigan marketplace plan if I lost my Molina or HAP CareSource coverage?

Yes. Molina Healthcare and HAP CareSource exited the Michigan individual market for 2026, which qualifies former enrollees for a Special Enrollment Period. Affected enrollees should have selected a new plan during 2026 Open Enrollment (November 1, 2025 – January 15, 2026). If you missed that window because of the carrier exit, contact a licensed enrollment assistant about loss-of-coverage SEP eligibility.

Is there a separate Michigan marketplace, or just HealthCare.gov?

HealthCare.gov is the only official Michigan marketplace. Michigan opted not to build a state-based exchange when the ACA launched, so all individual marketplace enrollment runs through the federal portal. The Michigan Department of Insurance and Financial Services regulates carrier rates and plan filings, but enrollment itself is federal. Any third-party site claiming to be the “Michigan marketplace” should be verified before enrollment.

What if my income changes during the year?

Report income changes to HealthCare.gov as soon as they occur. Income increases reduce your premium tax credit (so you’ll owe less or nothing back at tax time). Income decreases increase your subsidy and lower your monthly premium. Failing to report changes can result in either a tax bill in April or paying more than necessary throughout the year. The IRS reconciles subsidies annually using Form 8962.

Michigan Health Insurance Resources

Explore related guides for Michigan coverage overall, strategies for finding affordable coverage, small business and group plans, and PPO options to help navigate health insurance decisions across the Great Lakes State.

Plans, costs, carriers, and enrollment basics for the whole state.

Affordable CoverageSubsidies, tax credits, Healthy Michigan Plan, and low-cost plans.

Small Business & Group PlansSHOP, ICHRA, and group coverage options for Michigan employers.

PPO Health Insurance PlansNationwide out-of-network flexibility for specialists and travel.

Enroll in Your 2026 Michigan Marketplace Plan

Get free, licensed help with HealthCare.gov enrollment. Licensed brokers compare all seven Michigan carriers, check subsidy eligibility, and walk you through every step of the application.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Michigan residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.