PPO Health Insurance Plans for Individuals & Families

PPO health insurance plans give individuals and families the widest provider access of any plan type — any doctor or specialist without a referral, plus partial coverage for out-of-network care. That flexibility matters more than ever in 2026, when the December 31, 2025 expiration of enhanced federal premium tax credits pushed average marketplace premiums up about 20 percent and narrowed plan choices in many areas. True PPO plans have also become scarcer on the ACA exchange, where more than eight in ten plans are now HMOs or EPOs. This guide compares PPO health insurance plans for individuals and families: what they cost in 2026, how PPO coverage differs from HMO, EPO, and POS plans, the national carriers that still sell individual PPOs, and how to find PPO options both on and off the exchange.

What PPO Health Insurance Plans Offer in 2026

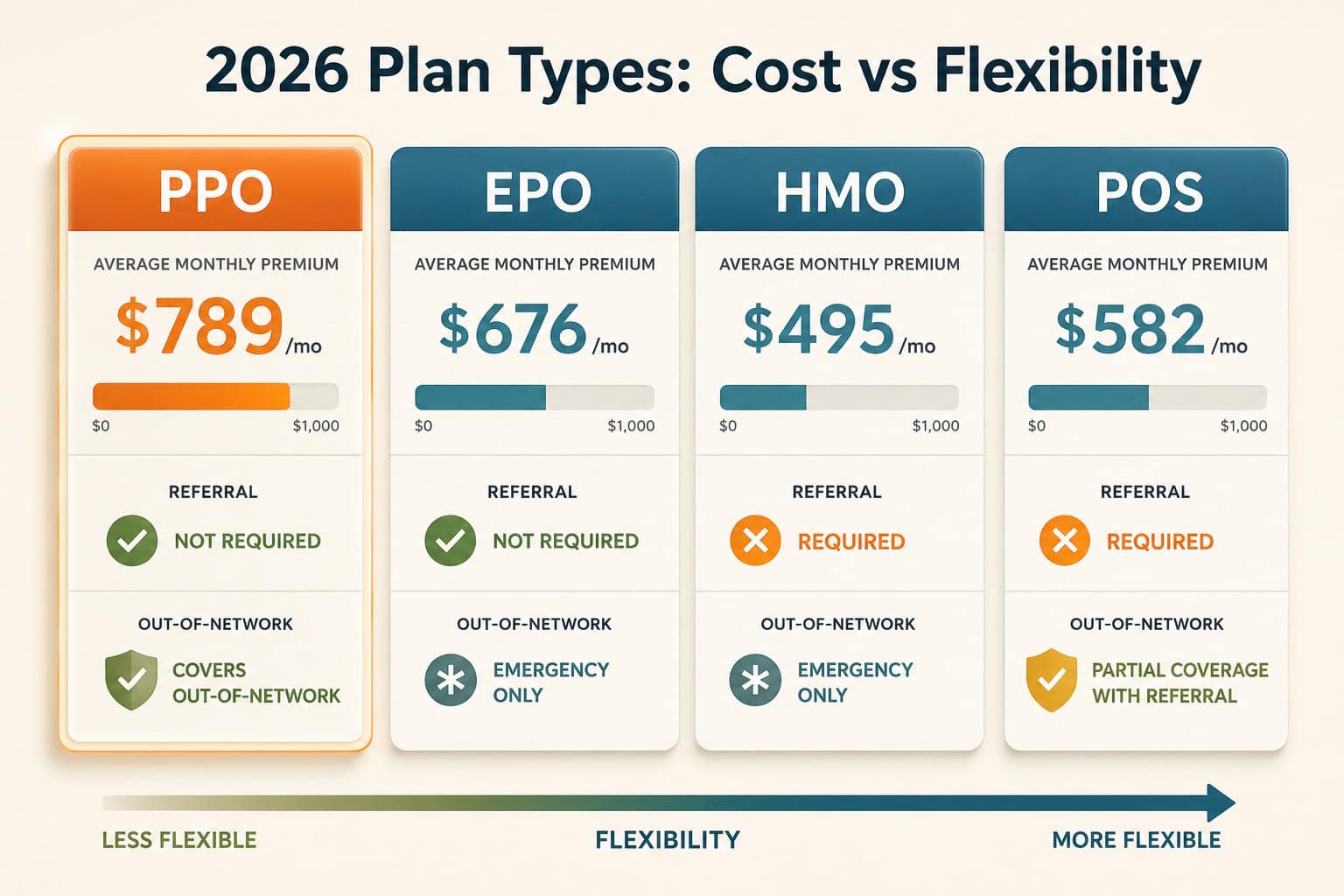

A PPO (Preferred Provider Organization) is the most flexible plan type: you can see any doctor or specialist without a referral, and it still pays a share of out-of-network care. That freedom carries the highest premium — a 2026 Silver marketplace PPO averages roughly $789 a month for a 31-to-45-year-old, about $113 over a comparable EPO. PPO health insurance fits people who value provider choice, travel often, or manage care across states.

- No referrals. See specialists directly, in or out of network.

- Out-of-network coverage. The plan pays a share even when you go outside the network — at a higher cost share.

- Broad, often national networks. Large national carriers contract thousands of providers across state lines.

- Best for multi-state and specialist-heavy needs. Useful for travelers, the self-employed, and households juggling several specialists.

The trade-off is cost. Because a PPO pays toward out-of-network claims, insurers price it above HMO and EPO designs. For households whose providers are all local and in-network, a lower-premium HMO or EPO may deliver the same in-network care for less — the PPO premium buys flexibility that not every household uses.

How Much Do PPO Health Insurance Plans Cost in 2026?

PPO health insurance plans carry the highest premiums because they cover out-of-network care. A 2026 Silver marketplace PPO averages about $789 per month for a 31-to-45-year-old, versus roughly $676 for an EPO. The 2026 out-of-pocket maximum is capped at $10,600 for an individual and $21,200 for a family, and the average marketplace in-network deductible sits just under $3,000. Premium tax credits can still lower on-exchange costs for households under 400 percent of the federal poverty level.

| 2026 Cost Factor | Figure / Impact | Source |

|---|---|---|

| Silver PPO average premium (age 31–45) | ~$789/month | Analysis of CMS plan data |

| Silver EPO average premium (same age) | ~$676/month | Analysis of CMS plan data |

| Average marketplace gross premium increase | ~20% for 2026 | Peterson-KFF |

| Net premium after subsidy (all enrollees) | $113 → $178/mo (+58%) | KFF |

| 2026 out-of-pocket maximum | $10,600 individual / $21,200 family | HealthCare.gov |

| Average in-network deductible | just under $3,000 | KFF |

The biggest 2026 cost story is not the PPO premium itself but the loss of enhanced subsidies. According to KFF, the average premium consumers pay net of tax credits rose 58 percent — from $113 to $178 per month — between 2025 and 2026, and the average deductible grew by about $1,000 per person as more enrollees shifted to higher-deductible plans. Insurers raised gross premiums about 20 percent on average for 2026, according to the Peterson-KFF Health System Tracker, citing drug costs, utilization, and the expected exit of healthier enrollees. When comparing PPO costs, weigh the monthly premium against the deductible, out-of-network coinsurance, in-network specialist copays, and prescription tiers.

PPO vs HMO, EPO, and POS Plans

PPO plans differ from the other three managed-care types on two axes: whether a referral is required, and whether out-of-network care is covered. PPOs require no referral and cover out-of-network care; HMOs require both a primary care provider and referrals; EPOs drop the referral but cover no out-of-network care except emergencies; POS plans sit in between. This is the core reason most marketplace shoppers see HMOs and EPOs first — they are cheaper to build.

| Plan Type | Referral Required | Out-of-Network | Premium Level |

|---|---|---|---|

| PPO | No | Covered (higher cost share) | Highest |

| POS | Yes for out-of-network | Partial with referral | Mid |

| EPO | No | Emergency only | Mid |

| HMO | Yes (PCP-led) | Emergency only | Lowest |

The practical decision usually comes down to out-of-network need. A PPO and an EPO both let you book specialists directly, but only the PPO pays toward care outside the network. The plan-type definitions are standardized by HealthCare.gov. For a deeper side-by-side, see the full PPO vs HMO vs EPO vs POS comparison.

Why PPO Plans Are Harder to Find on the Marketplace

True PPO plans have grown scarce on the ACA exchange. As of 2023, more than eight in ten marketplace plans nationwide were HMOs or EPOs, and the trend has continued — Blue Cross Blue Shield of Arizona dropped its marketplace PPOs at the end of 2025. PPOs cost insurers more because they pay a share of out-of-network claims, so carriers favor narrower-network designs. The result: many of the strongest individual PPO options are now sold off the exchange.

This is where comparing both channels matters. A buyer who shops only the marketplace may conclude PPOs are unavailable, when a national off-exchange PPO covers their ZIP code. Explore nationwide PPO plans for multi-state network options that are not tied to a single state’s exchange.

National Carriers That Offer Individual PPO Plans

A handful of national carriers account for most individual PPO availability in the United States, each with a large multi-state provider network. PPOs are also the most common employer plan — 46 percent of covered workers were enrolled in a PPO in 2025 — so these carriers maintain deep PPO networks that individual buyers can tap off the exchange. Availability and plan design vary by state and ZIP code.

UnitedHealthcare

National ReachOne of the largest national networks, useful for households that travel or have family in other states. Strong digital tools and pharmacy benefits. Individual PPO and PPO-style availability varies by market.

Blue Cross Blue Shield

BlueCard NationwideThe BlueCard program links independent Blue plans into near-nationwide access, a practical advantage for multi-state coverage. PPO availability differs by state Blue plan, and some markets have shifted toward HMO-only individual lineups.

Aetna

Multi-State NetworksNational carrier with broad provider participation and strong out-of-state access for households with ties in more than one region. Plan types offered on the individual market vary by state.

Cigna

PPO / POS FocusOne of the carriers more likely to offer traditional PPO and POS designs to individual buyers. Premiums tend to run higher, but the out-of-network flexibility is real for households that need it.

Every plan compared through ForHealthInsurance.com meets ACA compliance standards and includes the ten essential health benefits required under federal law. ForHealthInsurance.com is an independent brokerage, A+ rated by the Better Business Bureau, and quotes these carriers without upselling or pressure.

Compare PPO Plans in Your ZIP Code

Enter a ZIP code and date of birth to see PPO health insurance options on and off the exchange in about 60 seconds. Licensed agents are available to help compare networks and out-of-pocket costs at no extra charge.

Get a Quote Call 888-215-4045Who Should Choose a PPO Health Insurance Plan

PPO plans are not the cheapest option, so they pay off most for specific situations rather than every buyer. The common thread is a need for provider flexibility — across geography, specialists, or carriers — that a narrow-network HMO or EPO cannot satisfy. Three buyer profiles capture most of the people for whom a PPO is worth the higher premium.

What to Check in PPO Plan Fine Print

A PPO’s flexibility comes with details that change the real cost of care. Out-of-network services are covered but reimbursed at a lower rate, and balance billing — where a provider bills the difference between their charge and the plan’s allowed amount — is possible out of network. The 2026 out-of-pocket maximum of $10,600 for an individual applies only to in-network essential benefits; out-of-network costs can run higher. Read the plan documents for these four points before enrolling.

- Separate out-of-network deductible. Many PPOs apply a higher, separate deductible to out-of-network care before paying anything.

- Out-of-network coinsurance and balance billing. Confirm the coinsurance percentage and whether the provider can balance-bill you.

- Pre-authorization. Some major procedures require prior approval even on a no-referral PPO.

- Tiered networks. Some PPOs charge less for “preferred” in-network providers than for standard in-network ones.

Explore PPO Health Insurance Plans

Compare PPO health insurance by situation or by state — top-rated plans, self-employed and nationwide coverage, plan-type comparisons, and dedicated state guides.

Explore PPO Plans & Related Guides

Top-rated individual PPO options and how to compare them for 2026.

Nationwide PPO PlansMulti-state national networks for travelers and remote workers.

Self-Employed Health InsuranceIndividual coverage for 1099 income and work across state lines, PPO included.

PPO vs HMO vs EPO vs POSA full side-by-side of the four managed-care plan types.

PPO Health Insurance Plans by State

PPO availability and networks vary by state. Compare a dedicated PPO guide for your state:

How to Compare and Buy PPO Health Insurance

Buying a PPO plan as an individual takes four steps, and comparing both on-exchange and off-exchange options is what surfaces the widest PPO selection. Because more than eight in ten marketplace plans are HMOs or EPOs, a buyer who checks only the exchange may miss national PPOs that cover their ZIP code. The process below takes about 60 seconds to start and ends with licensed-agent help at no extra cost.

- Enter ZIP code and date of birth into the quote tool to pull available plans.

- Compare PPO options on and off the exchange — premium, network breadth, and out-of-network terms.

- Check in-network providers, out-of-pocket costs, and drug coverage for each plan.

- Apply online with licensed-agent support — no referral is required for PPO enrollment.

Frequently Asked Questions About PPO Health Insurance

Can I buy a PPO health insurance plan as an individual?

Yes. Individuals and families can buy PPO health insurance directly, either through the ACA marketplace where PPOs are available or off-exchange through national carriers. Because more than eight in ten marketplace plans are now HMOs or EPOs, many individual PPO buyers find their widest selection of true PPO plans off the exchange, where availability does not depend on a single state’s marketplace participation.

How much does a PPO health insurance plan cost in 2026?

For 2026, a Silver-tier PPO on the marketplace averages roughly $789 per month for a 31-to-45-year-old based on analysis of CMS plan data, compared with about $676 per month for a comparable EPO. PPOs carry the highest premiums of the main plan types because they cover out-of-network care. Actual cost depends on age, ZIP code, plan tier, and tobacco use, and any premium tax credit eligibility under 400 percent of the federal poverty level.

Why are PPO plans harder to find on the ACA marketplace?

PPOs cost insurers more because they pay a share of out-of-network care, so most carriers default to HMO and EPO designs to hold premiums down. As of 2023, more than eight in ten marketplace plans nationwide were HMOs or EPOs, and some carriers have continued to drop individual PPOs — Blue Cross Blue Shield of Arizona terminated its marketplace PPOs at the end of 2025. Many of the strongest individual PPO options are sold off the exchange through national carriers.

Do PPO plans require referrals to see a specialist?

No. PPO plans let you see specialists directly without a referral from a primary care doctor, in or out of network. This is the main practical difference from HMO plans, which require a referral before a specialist visit is covered. EPO plans also drop the referral requirement but, unlike PPOs, cover no out-of-network care except emergencies.

Are PPO health insurance plans available in every state?

PPO availability varies by state and county. Some marketplaces offer only HMOs and EPOs, while others list PPO options. National off-exchange PPO carriers extend coverage into areas where the marketplace lists few or no PPOs, which is why many multi-state households and frequent travelers compare both on-exchange and off-exchange PPO plans before enrolling.

What is the difference between a PPO and an EPO plan?

Both PPO and EPO plans let you see specialists without a referral, but a PPO pays a share of out-of-network care while an EPO covers out-of-network care for emergencies only. That difference is why PPOs cost more — roughly $113 more per month than EPOs for a 2026 Silver marketplace plan. For households that travel or manage chronic conditions with multiple specialists, the PPO’s out-of-network coverage can outweigh the higher premium.

Find a PPO Plan That Fits

Compare PPO health insurance plans for individuals and families on and off the exchange. ForHealthInsurance.com runs the comparison, checks network and out-of-pocket details, and completes enrollment at no extra cost.

Get a Quote Call 888-215-4045Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving individuals and families nationwide. ForHealthInsurance.com is not affiliated with HealthCare.gov, the Centers for Medicare & Medicaid Services, or any insurance carrier. The agency helps you compare PPO plans and enroll in coverage that meets your needs at no extra cost to you.