Private Medical Insurance Illinois 2026: Off-Exchange & Unsubsidized Plans

Private medical insurance in Illinois for 2026 is the right path for a specific set of buyers — households above 400 percent of the federal poverty level who receive no premium tax credits, buyers who want Platinum-tier coverage that no on-exchange carrier filed this year, and residents who need provider networks or carriers the Get Covered Illinois marketplace cannot offer. For everyone else, the marketplace with subsidies almost always wins on total annual cost. This guide explains exactly when private off-exchange coverage is the better choice and which Illinois carriers offer it.

What brings you here today?

I’m self-employed and want tax guidance

Deduction and HSA strategies for Illinois filers

See tax info ↓What Private Medical Insurance Means in Illinois

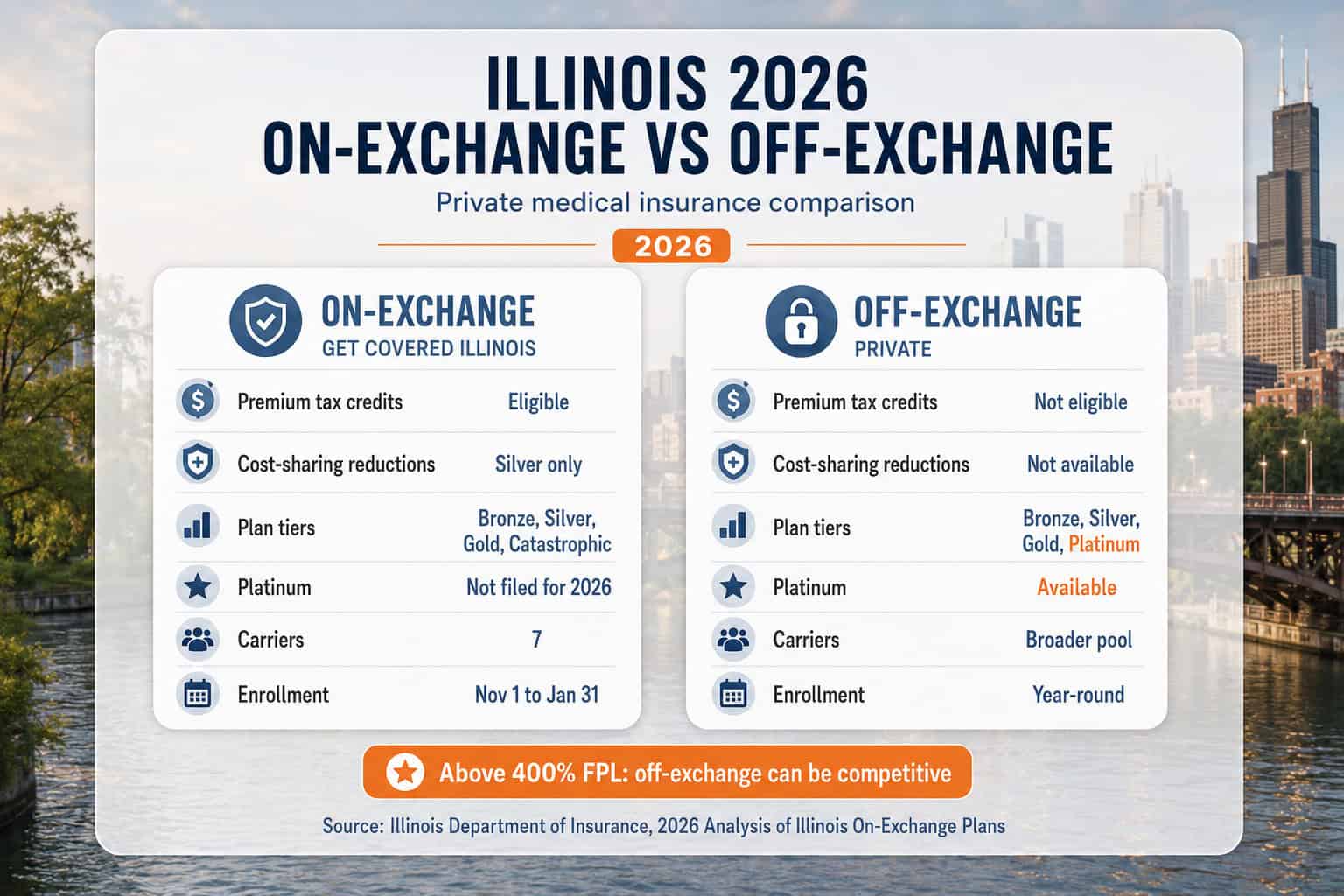

Private medical insurance in Illinois refers to health insurance plans purchased directly from a carrier or licensed broker outside the Get Covered Illinois marketplace. These off-exchange plans use the same Affordable Care Act underwriting rules, consumer protections, and essential health benefit requirements as on-exchange plans — guaranteed issue, no medical underwriting, and the same minimum coverage standards. What they cannot offer is premium tax credits or cost-sharing reductions, which are reserved for on-exchange purchases.

| Feature | On-Exchange (GCI) | Off-Exchange (Private) |

|---|---|---|

| ACA consumer protections | Yes | Yes |

| Premium tax credits (APTC) | Eligible | Not eligible |

| Cost-sharing reductions (CSR) | Silver, eligible | Not available |

| Platinum-tier coverage (2026) | None filed | Available from select carriers |

| Enrollment window | Nov 1 – Jan 31 (plus SEPs) | Year-round (ACA-compliant) |

| Provider networks | Seven on-exchange carriers | Broader carrier pool |

Private medical insurance is distinct from short-term health insurance, healthshare ministries, fixed indemnity products, and other non-ACA alternatives. Off-exchange ACA-compliant plans remain subject to the full Affordable Care Act consumer protection framework — they just sell outside the marketplace interface. The Illinois Department of Insurance regulates both on-exchange and off-exchange ACA plans under the same standards and reviews carrier rate filings annually for both markets.

Who Needs Private Medical Insurance in Illinois

Private medical insurance Illinois shoppers consider for 2026 fits three specific household profiles. For most marketplace-eligible households, Get Covered Illinois with subsidies wins on total annual cost. Off-exchange private coverage is the right answer when subsidies are unavailable, when the marketplace lacks the plan tier or carrier the household wants, or when network breadth requirements exceed what on-exchange carriers offer.

Profile 1: Households above 400 percent of FPL. Premium tax credits phase out at 400 percent of the federal poverty level — roughly $124,800 for a family of four in 2026. The narrower 8.5 percent income cap that replaced the expired enhanced subsidies still provides relief if the benchmark Silver plan would exceed that share of income, but many higher-earning households see no subsidy at all. For these households, off-exchange premiums match on-exchange premiums at similar tiers and sometimes offer better network or plan-tier options.

Profile 2: Households who want Platinum-level coverage. No on-exchange carrier filed Platinum-tier plans for the Illinois marketplace in 2026. Gold is the richest tier available through Get Covered Illinois. Households who want approximately 90 percent of expected costs covered — typically because of chronic conditions, anticipated major procedures, or simple preference for low out-of-pocket exposure — can find Platinum-level plans only off-exchange.

Profile 3: Households needing broader provider networks. The Illinois marketplace narrowed from eleven carriers in 2025 to seven in 2026 after Aetna CVS, Aetna Life, Health Alliance, and Quartz exited the state. Off-exchange products from national carriers sometimes include provider networks that no on-exchange Illinois carrier matches — particularly relevant for households with established specialists in academic medical centers or in multi-state networks.

On-Exchange vs Off-Exchange in Illinois for 2026

The economic decision between on-exchange and off-exchange private medical insurance Illinois shoppers face comes down to subsidy eligibility. Premium tax credits cap the household contribution to the benchmark Silver plan as a percentage of income, regardless of carrier or specific plan. Off-exchange plans cannot receive APTC, so any household eligible for a meaningful credit almost always comes out ahead on Get Covered Illinois — the after-credit cost is lower even when the off-exchange pre-subsidy price looks comparable.

| Household Income (Family of 4) | On-Exchange Likely Win | Off-Exchange Likely Win |

|---|---|---|

| Under $43,000 (138% FPL) | Medicaid (free) | Rarely |

| $43,000–$78,000 (138–250%) | Silver + APTC + Full CSR | No |

| $78,000–$124,800 (250–400%) | APTC only | Only for Platinum-tier or network breadth |

| $124,800–$170,000 (over 400%) | If 8.5% cap applies | Often competitive |

| Over $170,000 | Rare | Yes (no subsidy advantage) |

The expiration of the enhanced premium tax credits at the end of 2025 shifted some households into the off-exchange consideration zone. Under the enhanced subsidies, no household paid more than 8.5 percent of income for the benchmark Silver plan regardless of FPL. The original ACA structure that returned for 2026 puts the 8.5 percent cap back on a narrower basis, and the 400 percent FPL cliff partially returns. Get Covered Illinois publishes an eligibility checker that confirms subsidy status before any plan selection, which is the right first step before deciding between on-exchange and off-exchange options.

Private Platinum-Level Coverage in Illinois

Platinum-tier coverage — approximately 90 percent of expected costs covered by the plan — is unavailable through Get Covered Illinois for 2026. No on-exchange carrier filed Platinum products this plan year, per the Illinois Department of Insurance annual analysis. Households who want Platinum-level protection have one path: off-exchange purchase directly from carriers that offer Platinum-tier ACA-compliant products in Illinois.

| Metal Tier | Plan Covers | Typical Deductible (Family) | Availability 2026 |

|---|---|---|---|

| Bronze | ~60% | $14,000–$18,400 | On-exchange + off-exchange |

| Silver | ~70% | $9,000–$11,000 | On-exchange + off-exchange |

| Gold | ~80% | $3,000–$6,000 | On-exchange + off-exchange |

| Platinum | ~90% | $0–$2,000 | Off-exchange only |

The economics of off-exchange Platinum favor specific household profiles. Households expecting major surgeries or maternity care, families managing multiple chronic conditions, and adults nearing Medicare eligibility who want maximum coverage for the bridge years sometimes save money over the year with Platinum despite the higher premium. The math hinges on expected out-of-pocket spending — Platinum’s $0–2,000 deductible compared to Silver’s $9,000–11,000 only pays off when the household will actually use enough care to clear the Silver deductible regardless.

Private Medical Insurance Carriers Serving Illinois

Several national and regional carriers sell ACA-compliant private medical insurance off-exchange in Illinois for 2026. The carrier list overlaps partially with the on-exchange seven but extends to insurers that withdrew from the marketplace, never participated, or maintain off-exchange-only product lines targeted at unsubsidized buyers. Provider networks vary significantly between off-exchange products from the same carrier — a UnitedHealthcare off-exchange plan may have a different network than the same carrier’s on-exchange plan.

UnitedHealthcare

National ReachSells ACA-compliant off-exchange products in Illinois with broader provider networks than its on-exchange counterpart. Strong digital tools, useful for households with members who travel frequently or split residence between states. Off-exchange plans sometimes include Platinum-tier options not available on Get Covered Illinois.

BCBSIL Off-Exchange

Same HCSC NetworksBlue Cross Blue Shield of Illinois sells off-exchange products that use the same statewide BCBSIL networks as the on-exchange plans. For households above 400 percent FPL, BCBSIL off-exchange is often the simplest path to BCBSIL provider access without the marketplace subsidy structure.

Cigna Off-Exchange

Cook County PathCigna pulled out of Cook County on the Get Covered Illinois exchange for 2026 but maintains off-exchange products that serve Cook County buyers. Off-exchange Cigna is one of the few paths for Chicago-area residents who want Cigna network access in 2026 without changing carriers entirely.

Anthem and National Carriers

Broader Network OptionsNational carriers including Anthem (where licensed to sell in Illinois), Humana, and select regional insurers offer off-exchange ACA-compliant products. Plan availability varies by county and product line; verification through a licensed Illinois broker confirms which off-exchange options are filed in a specific ZIP code.

Find Private Medical Insurance in Illinois

Households above 400 percent FPL who want Platinum coverage or broader networks have off-exchange options that Get Covered Illinois cannot match. A licensed Illinois broker compares on-exchange and off-exchange plans side by side and finds the best fit at no cost.

Cost of Private Medical Insurance in Illinois

Private medical insurance Illinois premiums are set the same way as on-exchange premiums: age-rated within ACA limits, no medical underwriting, modified-community rating with a 3:1 maximum age band ratio, and a 50 percent maximum tobacco surcharge. The base rates are similar for the same carrier’s on-exchange and off-exchange products at the same metal tier. The practical cost difference shows up after subsidies — on-exchange shoppers eligible for APTC pay less; off-exchange shoppers pay the full premium.

| Household Profile | Tier | Typical Monthly Premium (Unsubsidized) |

|---|---|---|

| 30-year-old single | Silver | $420–$550 |

| 40-year-old single | Silver | $485–$635 |

| 50-year-old single | Silver | $695–$920 |

| 60-year-old single | Silver | $1,050–$1,395 |

| Family of 4 (parents 40) | Silver | $1,650–$2,100 |

| Family of 4 (parents 50) | Platinum (off-exchange) | $2,400–$3,100 |

Premium ranges reflect typical 2026 Illinois filings across rating areas. Cook County and the surrounding collar counties generally fall in the lower end of each range; downstate rural counties trend higher because of narrower provider networks and smaller risk pools. Off-exchange Platinum premiums run roughly 15–25 percent above off-exchange Gold for the same household composition — a substantial premium for the deductible reduction Platinum provides.

Self-Employed and 1099 Workers in Illinois

Self-employed Illinois residents — sole proprietors, partners, S-corp owner-employees, and independent contractors — have specific tax advantages when purchasing private medical insurance. The Self-Employed Health Insurance Deduction lets these households deduct premiums as an above-the-line adjustment on the federal tax return, lowering both adjusted gross income and Illinois state tax liability. The deduction applies to both on-exchange and off-exchange ACA-compliant plans.

Self-employed tax considerations

The Self-Employed Health Insurance Deduction (IRS Form 1040 Schedule 1) is an above-the-line deduction available to self-employed filers whose business shows a profit and who are not eligible for an employer-subsidized plan through a spouse. The deduction reduces both federal income tax and the self-employment tax base. Combining this deduction with an HSA-eligible HDHP can compound the tax benefit substantially.

HSA pairing matters for self-employed Illinois residents above subsidy thresholds. A high-deductible health plan (HDHP) with a deductible of at least $1,650 for individual coverage or $3,300 for family coverage in 2026 qualifies for HSA contributions of up to $4,300 individual or $8,550 family — fully tax-deductible. For a self-employed household paying $25,000 in annual premiums and contributing $8,550 to an HSA, the combined federal tax savings can exceed $7,000 depending on marginal tax bracket. This stacking effect makes off-exchange HSA-eligible HDHPs particularly attractive for self-employed Illinois filers who do not qualify for marketplace subsidies.

When Private Off-Exchange Beats the Illinois Marketplace

For most Illinois households eligible for premium tax credits, Get Covered Illinois beats off-exchange private medical insurance on total annual cost. The subsidy math is hard to overcome — APTC plus Silver CSR can cut effective premiums to under $50 per month for households at 138–200 percent FPL, far below any off-exchange equivalent. Off-exchange wins in specific situations where the marketplace structure cannot match the household’s actual coverage needs.

Four situations where private off-exchange wins

- Household income exceeds the 8.5 percent of income cap. When the benchmark Silver plan would cost less than 8.5 percent of household income (typically households well above 400 percent FPL with multiple earners), no subsidy applies and off-exchange premiums are competitive on similar networks.

- Platinum-tier coverage is required. No on-exchange carrier filed Platinum in Illinois for 2026. Households who want 90 percent actuarial value must shop off-exchange — the marketplace has no equivalent option.

- Specific provider network is essential. When a particular specialist, academic medical center, or multi-state network is non-negotiable and no on-exchange carrier includes it, off-exchange products from national carriers sometimes include the needed network.

- Year-round enrollment flexibility is needed. Off-exchange ACA-compliant plans do not have open enrollment windows — they accept applications year-round. Households between job changes, relocating mid-year, or recovering from a missed marketplace SEP can purchase off-exchange immediately.

Common Private Medical Insurance Mistakes in Illinois

Four mistakes push Illinois residents toward private off-exchange coverage when marketplace coverage would serve them better — or into the wrong off-exchange product when they do belong off-exchange. Each one reflects a misunderstanding of subsidy eligibility, plan-tier math, or the ACA framework that governs both markets.

Shopping off-exchange without checking subsidy eligibility first

Many Illinois residents assume they earn too much for subsidies without checking. The 8.5 percent income cap means even households at 400–500 percent FPL sometimes qualify for modest APTC. Always verify eligibility on Get Covered Illinois before committing to off-exchange.

Confusing off-exchange ACA plans with short-term or non-ACA products

Off-exchange ACA-compliant plans carry the same consumer protections as marketplace plans — guaranteed issue, essential health benefits, no pre-existing condition exclusions. Short-term and fixed-indemnity products do not. Verify the plan is ACA-compliant before purchase.

Choosing Gold off-exchange when Platinum is actually cheaper net

For households with high expected medical utilization, Platinum’s lower deductible can produce lower total annual cost even with the higher premium. Run the full-year out-of-pocket projection before defaulting to Gold because the monthly premium is lower.

Switching to off-exchange mid-year while still subsidized

Switching from an on-exchange plan to an off-exchange plan mid-year means giving up APTC already advanced for that year — which triggers full reconciliation at tax time. This only makes financial sense for households that received no subsidy in the first place.

Frequently Asked Questions About Illinois Private Medical Insurance

The most common questions Illinois residents ask about off-exchange private medical insurance — covering who should buy it, Platinum availability, cost comparisons with the marketplace, and self-employed tax deductions for 2026.

What is private medical insurance in Illinois?

Private medical insurance in Illinois refers to health insurance plans purchased directly from a carrier or broker outside the Get Covered Illinois marketplace. These off-exchange plans use the same underwriting rules and Affordable Care Act consumer protections as on-exchange plans but cannot receive premium tax credits or cost-sharing reductions. Off-exchange products often include broader provider networks and richer plan tiers — including Platinum-level coverage that no on-exchange carrier filed in Illinois for 2026.

Who should buy private medical insurance in Illinois?

Private off-exchange medical insurance in Illinois makes sense for three household profiles: residents with income above 400 percent of the federal poverty level who do not qualify for premium tax credits, households who want Platinum-level coverage (not available on Get Covered Illinois for 2026), and buyers who need broader provider networks than the seven on-exchange carriers offer. For households below 400 percent FPL, the marketplace almost always wins on total annual cost because of subsidies.

Can I get Platinum-level coverage in Illinois for 2026?

Yes, but only off-exchange. No on-exchange carrier filed Platinum-tier plans for the Illinois marketplace in 2026, per the Illinois Department of Insurance annual analysis. Gold is the richest tier available through Get Covered Illinois. Households who want Platinum-level coverage — approximately 90 percent of expected costs covered — must shop off-exchange directly from carriers, which forfeits premium tax credit eligibility.

Are off-exchange private plans in Illinois cheaper than marketplace plans?

Before subsidies, off-exchange premiums are typically similar to on-exchange premiums at the same metal tier — the underwriting and rate filing rules are the same. After subsidies, marketplace plans almost always cost less for households eligible for premium tax credits. For households above 400 percent FPL who do not qualify for any APTC, off-exchange plans sometimes offer better network or plan-tier value at similar unsubsidized prices.

Is private medical insurance tax-deductible for self-employed Illinois residents?

Yes. Self-employed Illinois residents — sole proprietors, partners, and S-corp owner-employees — can deduct private medical insurance premiums as an above-the-line adjustment on the federal tax return, lowering both adjusted gross income and Illinois state tax liability. The deduction applies whether the plan is purchased on the marketplace or off-exchange and whether premium tax credits are claimed or not.

Can I switch from a marketplace plan to private medical insurance mid-year?

Off-exchange ACA-compliant plans are available year-round without an open enrollment period — private plans do not have the November–January enrollment window that applies to Get Covered Illinois. Switching from a marketplace plan to an off-exchange plan mid-year means giving up premium tax credits already received for that year, which may trigger reconciliation at tax time. The math usually works only for households above 400 percent FPL who received no subsidy anyway.

Illinois Health Insurance Resources

Statewide overview of carriers, costs, and coverage paths for 2026

Illinois Marketplace GuideGet Covered Illinois enrollment steps, deadlines, and the new state-based platform

Best Illinois Health InsuranceTop-ranked carriers and plan options for Illinois residents in 2026

Illinois PPO PlansBCBSIL PPO options and other flexible network choices statewide

Family Health InsuranceAll Kids, marketplace splits, and mixed-status coverage for Illinois households

Affordable Illinois PlansSubsidy strategies and lowest-cost coverage paths after the 2026 rate jump

Small Business CoverageGroup health insurance options for Illinois employers under 50 employees

Short-Term CoverageGap coverage rules and marketplace alternatives for Illinois residents

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required

Compare Private Medical Insurance Options

Off-exchange private medical insurance in Illinois offers Platinum-tier coverage, broader networks, and year-round enrollment that Get Covered Illinois cannot match. A licensed Illinois broker maps on-exchange and off-exchange options to household needs and completes enrollment at no cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Illinois residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.