Michigan Health Insurance Plans: 2026 Types, Tiers, and How to Compare

Michigan health insurance plans fall into four metal tiers (Bronze, Silver, Gold, and Platinum) and several network types — PPO, HMO, EPO, and POS. For 2026 there are 116 plans on the HealthCare.gov Marketplace and 191 plans across the full individual market. This guide explains what plans exist and how they are structured so you can compare them.

What Health Insurance Plans Are Available in Michigan in 2026?

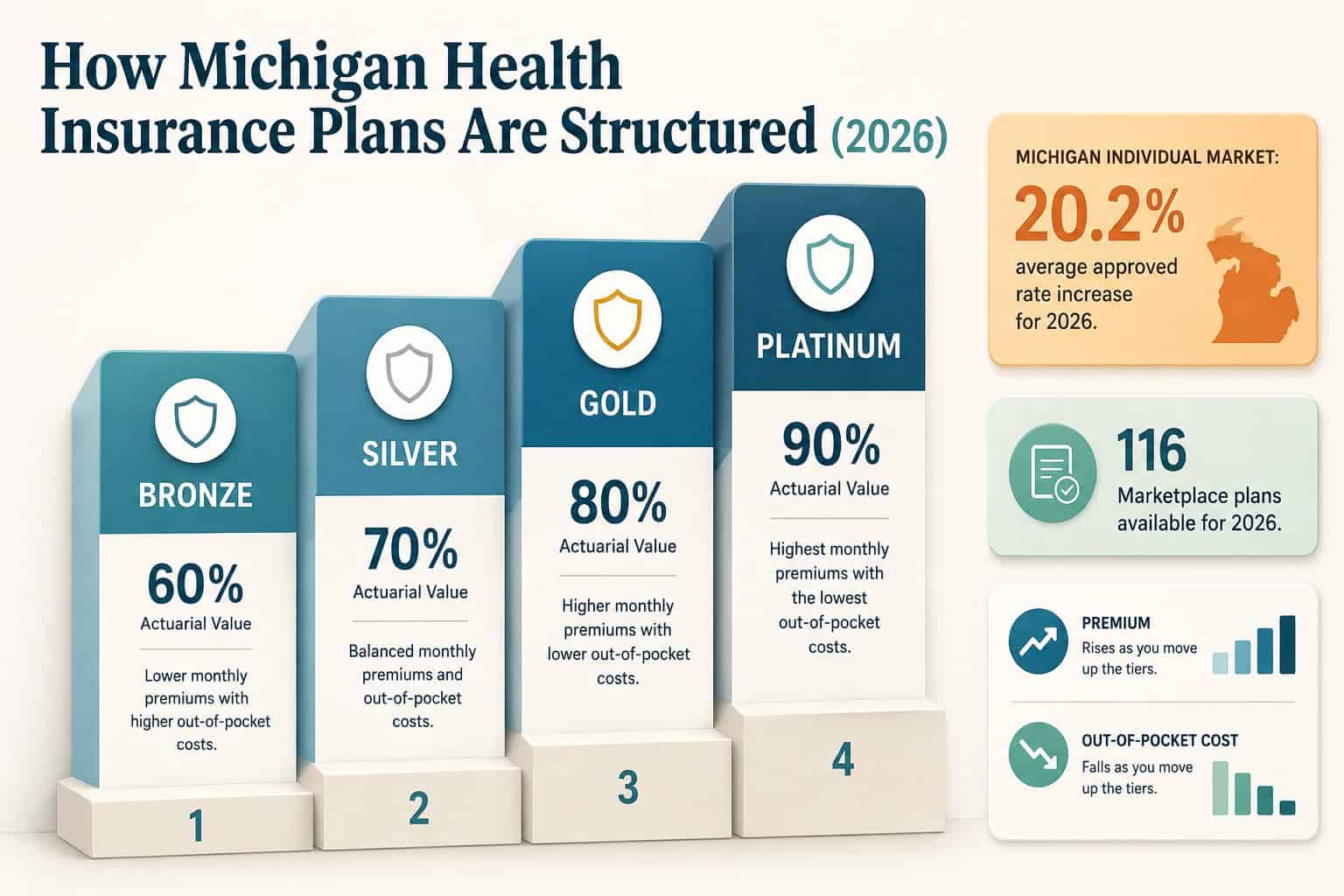

Michigan offers 116 health insurance plans on the 2026 HealthCare.gov Marketplace — down from 162 in 2025 — plus off-Marketplace options for 191 total individual-market plans. Seven insurers participate this year, down from ten. Every plan sits in one of four metal tiers and uses one of several network types.

Michigan is a federal-exchange state, so residents shop and enroll through HealthCare.gov rather than a state-run marketplace. The insurers offering Michigan health insurance plans for 2026 include Blue Cross Blue Shield of Michigan, Blue Care Network, Priority Health, Meridian, and McLaren Health Plan. When you compare health insurance plans in Michigan, the two structural choices that matter most are the network type (how you access doctors and hospitals) and the metal tier (how you and the plan split costs).

Check that your plan is still offered for 2026. The Michigan market contracted this year: Molina discontinued its on-exchange individual plans (about 35,000 members), HAP CareSource withdrew, and Meridian’s Ambetter plans pulled out of Macomb, Monroe, Oakland, and Wayne counties. If your 2025 plan disappeared, you were not automatically matched to an identical one — review your options during open enrollment. See which insurers offer Michigan plans for the full carrier picture.

Michigan Plan Types: PPO, HMO, EPO, and POS

Most Michigan health insurance plans are HMOs, but PPO plans — the most flexible network type — are sold statewide primarily through Blue Cross Blue Shield of Michigan, which holds roughly 45% of the state insurance market. HMO-led carriers such as Priority Health (about 122,000 individual enrollees) and Blue Care Network dominate by membership.

Choosing a network type is the first decision when you compare health insurance plans in Michigan. A PPO lets you see specialists without referrals and offers some out-of-network coverage — useful across a state where provider systems vary by region. An HMO keeps premiums lower by requiring a primary care physician and in-network care. An EPO is a middle ground (no referrals, but no out-of-network coverage), and a POS blends HMO and PPO rules.

PPO

Broadest access, no referrals, partial out-of-network coverage. In Michigan, PPO plans are offered statewide mainly through Blue Cross Blue Shield of Michigan. Best for people who want flexibility or travel within the state.

HMO

Lower premiums, in-network care with a primary care physician and referrals. The most common Michigan plan type — Priority Health, Blue Care Network, and Meridian are HMO-led.

EPO

No referrals needed, but no out-of-network coverage except emergencies. A cost-conscious middle option where available.

POS

Point-of-service plans combine HMO structure with limited out-of-network access at higher cost. Less common in Michigan’s individual market.

If you specifically want a PPO and do not qualify for subsidies, you can also buy a Michigan PPO outside the Marketplace.

How Michigan Plans Are Structured: Bronze to Platinum

Every Michigan Marketplace plan falls into one of four metal tiers set by actuarial value — Bronze (about 60%), Silver (70%), Gold (80%), and Platinum (90%). With individual premiums rising a 20.2% increase approved by the Michigan Department of Insurance and Financial Services (DIFS) for 2026, tier choice drives the premium-versus-out-of-pocket trade-off more than in prior years.

Metal tiers describe how you and the plan share costs, not the quality of care. A Bronze plan has the lowest premium but the highest deductible; a Platinum plan reverses that. Silver is the tier tied to extra cost-sharing reductions for lower-income enrollees and is the “benchmark” used to set subsidies. When you compare health insurance plans in Michigan, match the tier to how much care you expect to use, then compare premiums within that tier.

| Metal tier | Actuarial value (plan pays) | Premium | Out-of-pocket when you get care |

|---|---|---|---|

| Bronze | ~60% | Lowest | Highest deductible |

| Silver | ~70% | Moderate | Lower with CSR (income-based) |

| Gold | ~80% | Higher | Lower deductible |

| Platinum | ~90% | Highest | Lowest out-of-pocket |

Compare Michigan Plans in Minutes

See the Michigan health insurance plans available in your ZIP code and what they cost for 2026.

On-Exchange vs. Off-Exchange Michigan Plans

Michigan plans sell two ways: on HealthCare.gov (the only place to use ACA subsidies) or off-exchange directly from insurers. For 2026 the enhanced premium tax credits have expired and subsidies reverted to the ACA’s original 100%–400% of the federal poverty level rules, so many of Michigan’s roughly 533,000 individual-market enrollees are re-checking both routes.

If your income is above 400% of the poverty level, you no longer receive a federal subsidy for 2026, and Michigan — unlike a few state-run exchanges — does not add its own premium assistance. In that situation, off-Marketplace private health insurance plans in Michigan are worth comparing directly. See how Michigan Marketplace subsidies work.

How to Compare Michigan Health Insurance Plans

The biggest factor when you compare health insurance plans in Michigan is the provider network: three hospital systems control about 64% of the market, so confirm your plan includes your system — Corewell Health, University of Michigan Health, Henry Ford Health, or McLaren. Then weigh drug formularies, deductibles, and total 2026 cost.

1. Match the network

Confirm your hospital system and doctors are in-network. Michigan networks differ sharply by region — Corewell Health and University of Michigan Health anchor different parts of the state.

2. Check the drug formulary

Verify your prescriptions are covered and at what tier. Formulary differences are a common reason two similar plans cost very differently.

3. Compare total cost, not just premium

Add the deductible and out-of-pocket maximum to the premium. A low-premium Bronze plan can cost more overall if you use care regularly.

4. Confirm 2026 availability

After this year’s carrier exits, make sure the plan is still offered in your county before you enroll.

Example — Grand Rapids vs. Detroit metro. A Grand Rapids family loyal to a Corewell Health hospital may prioritize an HMO plan whose network centers on West Michigan, while a Detroit-metro shopper who wants access to multiple systems and no referrals may prefer a statewide PPO. Same metal tier, very different best-fit plan. For a ranked view of carriers, see the top-rated Michigan carriers.

Related Michigan Health Insurance Resources

The statewide guide to 2026 plans, costs, and how coverage works in Michigan.

Michigan Marketplace & SubsidiesHow HealthCare.gov works for Michigan and who still qualifies for premium tax credits.

Best Health Insurance in MichiganA ranked comparison of Michigan’s top-rated carriers for 2026.

Michigan Health Insurance CompaniesWho the insurers are, their networks, and where they operate across Michigan.

Individual Health Insurance MichiganBuying coverage for yourself when you are not offered an employer plan.

Private Health Insurance MichiganOff-exchange private plans, including PPO options, for buyers without subsidies.

Affordable Health Insurance MichiganLower-cost 2026 options and ways to reduce your monthly premium.

Michigan Health Insurance QuotesCompare personalized 2026 plan pricing for your ZIP code in minutes.

Frequently Asked Questions About Michigan Health Insurance Plans

How many health insurance plans are available in Michigan for 2026?

For 2026 there are 116 health insurance plans on Michigan’s HealthCare.gov Marketplace, down from 162 in 2025, and 191 plans across the full individual market when off-Marketplace options are included. Seven insurers participate, down from ten the year before.

What is the difference between an HMO and a PPO plan in Michigan?

A Michigan HMO plan keeps premiums lower but requires you to use in-network providers and get referrals through a primary care physician. A PPO plan costs more but lets you see specialists without referrals and covers some out-of-network care. Most Michigan plans are HMOs; PPOs are offered statewide mainly through Blue Cross Blue Shield of Michigan.

Which metal tier is best for me?

Match the tier to how much care you expect to use. Bronze plans have the lowest premium and highest deductible, Platinum reverses that, and Silver (about 70% actuarial value) is the tier tied to income-based cost-sharing reductions. If you use care often, a Gold or Silver plan usually costs less overall than a low-premium Bronze plan.

Can I buy a Michigan health insurance plan off the Marketplace?

Yes. You can buy private health insurance plans in Michigan directly from insurers off-exchange, but you can only use ACA premium subsidies on HealthCare.gov. Off-exchange plans make the most sense for people who do not qualify for a 2026 subsidy, such as those with income above 400% of the federal poverty level.

Did any insurers stop offering Michigan plans in 2026?

Yes. Molina discontinued its on-exchange individual plans for 2026, HAP CareSource withdrew from the individual market, and Meridian’s Ambetter plans exited Macomb, Monroe, Oakland, and Wayne counties. Always confirm your plan is still offered in your county before you enroll.

Ready to Choose a Michigan Plan?

Compare Michigan health insurance plans side by side and enroll with help from a licensed agent — at no extra cost to you.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Michigan residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.