Short Term Health Insurance Iowa 2026: STLDI Plans, Limits, and ACA Alternatives

Short term health insurance in Iowa is available — unlike California and Hawaii, which ban short-term limited duration insurance (STLDI) plans entirely, Iowa permits STLDI plans with initial terms up to 364 days, renewable to a total of up to three years under current Iowa regulations. For Iowa residents between jobs, missing open enrollment, or waiting for employer benefits to begin, short term health insurance Iowa plans can bridge a coverage gap at lower premium cost than COBRA. This guide covers how short term health insurance Iowa plans work and their significant limitations, the Iowa Farm Bureau Health Plan as a non-ACA alternative, and when switching to an ACA marketplace plan through HealthCare.gov is the better decision.

What brings you here today?

Understand STLDI limits in Iowa

364-day initial terms, renewable to 3 years — what’s covered and excluded

How it works →Compare STLDI vs ACA marketplace

Side-by-side decision guide — when to choose short-term and when to avoid it

Compare options →Missed open enrollment

IA Health Link, SEP, COBRA, and Wellmark year-round alternatives

See alternatives →How Short-Term Health Insurance Works in Iowa

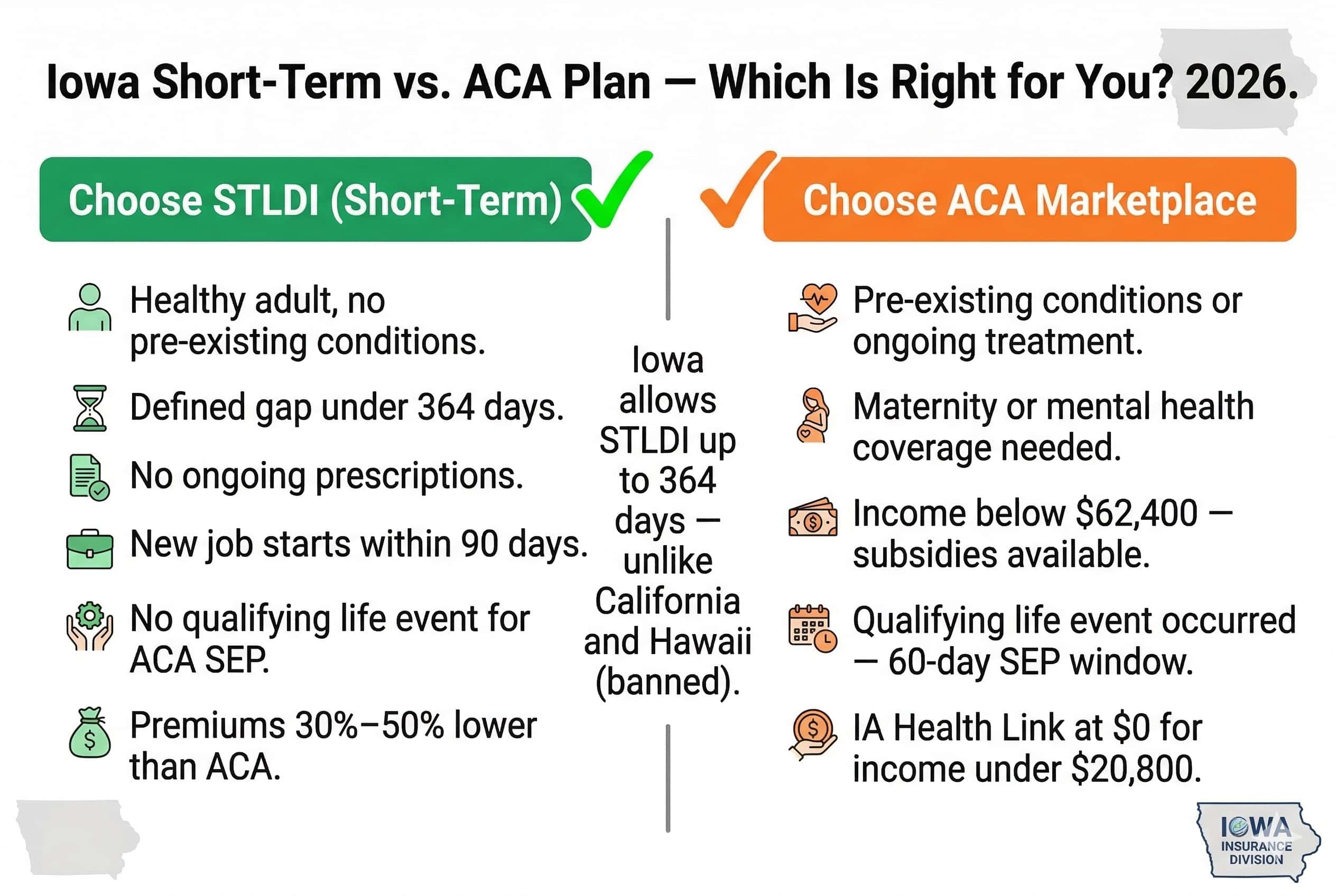

Iowa allows STLDI plans with initial terms up to 364 days, renewable up to a total of three years — one of the more permissive states for short-term coverage. STLDI plans are not ACA-compliant: they can exclude pre-existing conditions, cap annual benefits, and deny claims for conditions not disclosed at enrollment. No federal penalty applies for lacking ACA coverage since 2019, and Iowa has no state individual mandate. Premiums are typically 30%–50% lower than ACA plans for healthy adults.

Iowa’s permissive STLDI rules stem from federal regulations allowing states to expand beyond the federal default of 3-month initial terms. Iowa adopted rules allowing STLDI initial terms up to 364 days, with renewals permitted to a total of 36 months — consistent with Iowa Insurance Division Bulletin 25-05. Short term health insurance Iowa residents purchase through STLDI carriers is regulated by the Iowa Insurance Division but is not subject to ACA essential health benefit requirements, meaning these plans do not have to cover maternity care, mental health services, prescription drugs, or preventive care at the same standards as marketplace plans.

STLDI Plan Limitations Iowa Residents Must Understand

Iowa STLDI plans carry significant limitations every resident must understand before enrolling. Pre-existing conditions are excluded — any condition treated in the past 2–5 years may be denied. Annual benefit caps often range from $250,000 to $1,000,000. Mental health, maternity, and preventive care are often excluded or limited. The Iowa Insurance Division regulates STLDI but cannot require ACA essential health benefit compliance.

Critical STLDI Limitations for Iowa Residents

Pre-existing condition exclusions — any condition treated in the past 24–60 months (varies by plan) can be excluded from coverage. Annual or lifetime benefit caps — some plans cap benefits at $250,000 or less. No guaranteed coverage of essential health benefits — maternity, mental health, substance use disorder, and prescription drugs may be excluded or limited. Rescission risk — if a claim reveals an undisclosed condition, the insurer can rescind the policy retroactively. STLDI renewal beyond the initial term requires reapplying and passing new medical underwriting each time; total duration can reach 36 months in Iowa under current state rules.

| Coverage Feature | Iowa STLDI Plan | Iowa ACA Marketplace Plan |

|---|---|---|

| Pre-existing conditions | Typically excluded (2–5 year lookback) | Fully covered — no exclusions |

| Essential health benefits | Not required — varies by plan | All 10 EHBs required by law |

| Annual benefit cap | Often $250,000–$1,000,000 | No annual cap allowed |

| Premium (healthy adult) | 30%–50% below ACA plans | Full premium; subsidies available |

| Guaranteed issue | No — medical underwriting applies | Yes — cannot be denied |

| Minimum essential coverage | No | Yes |

| Max duration in Iowa | Up to 364-day initial term; renewable to 36 months total | Annual plan year (renews) |

Iowa Farm Bureau Health Plan — A Non-ACA Alternative

Iowa Farm Bureau members have access to the Iowa Farm Bureau Health Plan — a non-ACA health benefit plan sponsored by the Iowa Farm Bureau agricultural nonprofit. Like STLDI plans, Farm Bureau Health Plans are not ACA-compliant and may exclude pre-existing conditions. Unlike STLDI, Farm Bureau plans are available only to Iowa Farm Bureau members and are governed by Iowa state law rather than federal insurance regulations. They serve as a longer-term non-ACA option for farming households.

The Iowa Farm Bureau Health Plan serves Iowa’s approximately 87,000 farm operations — residents who may not qualify for subsidized marketplace plans (above $62,600 single income) but find full-price ACA premiums unaffordable. When evaluating short term health insurance Iowa alternatives, Farm Bureau plans are not sold through HealthCare.gov and do not qualify for premium tax credits. Iowa Farm Bureau members should compare benefit structures — particularly pre-existing condition exclusions and annual caps — against off-exchange Wellmark PPO plans. Iowans comparing short term health insurance Iowa STLDI plans against Farm Bureau options should review 2026 premium cost comparisons in the Iowa affordable health insurance guide. For PPO options, see the Iowa carrier comparison and PPO guide.

When Iowa Residents Should Choose ACA Instead of STLDI

Short-term plans are appropriate for healthy Iowa adults with a coverage gap and no pre-existing conditions. Iowa residents with chronic conditions, prescription drug needs, mental health care, or pregnancy should always choose an ACA marketplace plan or IA Health Link instead. A qualifying life event — job loss, divorce, moving to Iowa — triggers a Special Enrollment Period on HealthCare.gov regardless of the time of year.

Choose STLDI when:

Gap is under 364 days (or longer if renewals expected — Iowa allows up to 36 months total). Iowa resident is healthy with no ongoing prescriptions or treatment. No pre-existing conditions in the past 2–5 years. Need for basic accident and illness coverage only. Between employer plans with new job starting in 60–90 days. No qualifying life event available for ACA Special Enrollment Period.

Choose ACA marketplace instead when:

Pre-existing conditions exist — diabetes, heart disease, cancer history, mental health treatment. Prescription drugs are needed regularly. Maternity coverage required. Income qualifies for IA Health Link at $0 (under $22,020 single) or marketplace subsidies (under $62,600 single). A qualifying life event has occurred — enroll within 60 days at HealthCare.gov.

Compare Iowa Coverage Options for Your Gap

IA Health Link at $0 up to $22,020, Oscar Silver from ~$496/month with SEP, Wellmark PPO year-round — find the right bridge coverage for your Iowa situation before considering STLDI.

ACA Alternatives to Short-Term Coverage in Iowa

Iowa residents facing a coverage gap have four ACA-compliant alternatives to STLDI: IA Health Link Medicaid at $0 for incomes up to $22,020, Special Enrollment Period marketplace plans triggered by a qualifying life event, COBRA continuation of prior employer coverage for up to 18 months, and off-exchange Wellmark PPO plans purchasable year-round without a qualifying event.

IA Health Link — $0 for Qualifying Iowans

Iowa’s Medicaid managed care program covers adults earning up to $22,020 (single) or $45,540 (family of four) at $0 premium. Year-round enrollment — no qualifying event needed. Covers all ACA essential health benefits including pre-existing conditions. Best option for low-income Iowans in any coverage gap situation. Apply through Iowa HHS or HealthCare.gov.

Special Enrollment Period — 60-Day Window

Job loss — including seasonal layoff — is a qualifying life event that opens a 60-day Special Enrollment Period on HealthCare.gov. Iowa residents can enroll in Oscar (~$496/mo Silver, 75 counties) or Wellmark plans during this window. Subsidies apply based on annual income. Starting the HealthCare.gov application immediately after losing coverage prevents gap days.

COBRA — Continue Prior Employer Coverage

Available for up to 18 months after leaving a job. Preserves the same plan and provider network. Premiums include the full employer + employee share plus a 2% admin fee — typically $500–$800/month for Iowa employer plans. More expensive than STLDI but fully ACA-compliant. Best for Iowa residents with pre-existing conditions or mid-treatment who cannot risk a coverage gap.

Off-Exchange Wellmark PPO — Year-Round

Wellmark’s off-exchange PPO plans can be purchased directly at any time — no qualifying event, no enrollment period. Full ACA compliance and BCBS national network. Premiums comparable to full-price marketplace plans (~$524/mo Silver for a 40-year-old). No subsidy eligibility. Best for Iowa residents above the $62,600 subsidy threshold who want PPO flexibility without STLDI’s coverage gaps.

Real Scenario: Seasonal Agricultural Worker, Story County — Coverage Gap

A seasonal farm equipment operator near Ames loses employer coverage when seasonal work ends in November. Open enrollment on HealthCare.gov runs November 1 through January 15 — the worker is within the open enrollment window and should enroll in an Oscar or Wellmark marketplace plan rather than purchasing STLDI. Oscar’s Silver plan in Story County runs approximately $496/month before subsidies; at 200% FPL ($31,300 for a single adult), the subsidy would reduce the contribution to under $200/month. If the worker’s income drops below $22,020 in the off-season, IA Health Link is available at $0 with year-round enrollment — far better protection than STLDI at any price.

Frequently Asked Questions — Short-Term Health Insurance in Iowa

Common Iowa STLDI questions for 2026 — covering short-term coverage limits, Farm Bureau plans, and ACA alternatives — including Iowa’s STLDI rules (up to 364-day initial terms, renewable to 3 years), plan limitations, Iowa Farm Bureau Health Plan, and how to get ACA coverage when you’ve missed open enrollment.

Is short-term health insurance available in Iowa?

Yes. Iowa permits short-term limited duration health insurance (STLDI) plans with initial terms up to 364 days, renewable to a total of up to three years — making it one of the more permissive states for short-term coverage. This contrasts with California and Hawaii, which ban STLDI plans entirely. Iowa STLDI plans are regulated by the Iowa Insurance Division but are not ACA-compliant, meaning they can exclude pre-existing conditions, cap annual benefits, and limit or exclude essential health benefits like maternity care, mental health services, and prescription drugs. No federal penalty applies for lacking ACA-compliant coverage since 2019, and Iowa has no state individual mandate.

What are the limitations of short-term health insurance in Iowa?

Iowa STLDI plans have significant coverage limitations that residents must understand before enrolling. Pre-existing conditions are typically excluded — any condition diagnosed or treated in the past 24 to 60 months may be denied coverage depending on the plan. Annual benefit caps often range from $250,000 to $1,000,000, well below the unlimited coverage ACA plans provide. Essential health benefits including maternity care, mental health and substance use disorder treatment, and comprehensive prescription drug coverage are not required. Medical underwriting applies at enrollment — Iowans with health conditions may be denied coverage or charged higher rates. STLDI plans can be renewed beyond the initial term with new medical underwriting; total coverage in Iowa can reach 36 months under current state regulations.

Who should consider short-term health insurance in Iowa?

STLDI plans are best suited for a narrow group of Iowa residents: healthy adults with no pre-existing conditions and no ongoing prescriptions who need gap coverage — Iowa allows initial terms up to 364 days, renewable to 36 months total. Common situations include waiting for a new employer’s benefits to begin, between seasonal jobs in Iowa’s agricultural economy, or missing open enrollment without a qualifying life event. Iowans with any pre-existing condition, ongoing treatment, prescription drug needs, or mental health care should choose an ACA marketplace plan through HealthCare.gov or IA Health Link — short term health insurance Iowa STLDI exclusions create serious financial risk for these residents.

What is the Iowa Farm Bureau Health Plan?

The Iowa Farm Bureau Health Plan is a health benefit plan offered to Iowa Farm Bureau members through the Iowa Farm Bureau agricultural nonprofit organization. It is a non-ACA plan governed by Iowa state law rather than federal ACA requirements. Like STLDI plans, Farm Bureau Health Plans may exclude pre-existing conditions and do not have to cover all ACA essential health benefits. The plan is available only to Iowa Farm Bureau members and cannot be purchased on HealthCare.gov. It does not qualify for premium tax credits. Iowa Farm Bureau members should compare the plan’s benefit structure and exclusions carefully against ACA marketplace plans and off-exchange Wellmark PPO options before enrolling. Short term health insurance Iowa STLDI plans and Farm Bureau plans share the common limitation of excluding pre-existing conditions.

How can I get health coverage in Iowa if I missed open enrollment?

Iowa residents seeking short term health insurance Iowa coverage or who missed open enrollment have several options. A qualifying life event — job loss, marriage, birth of a child, divorce, or moving to Iowa — triggers a 60-day Special Enrollment Period on HealthCare.gov regardless of time of year. IA Health Link (Medicaid) enrolls year-round for Iowa adults earning up to $22,020 (single) — no qualifying event required. Off-exchange Wellmark PPO plans can be purchased directly from Wellmark at any time without an enrollment period — they do not qualify for subsidies but offer full ACA-compliant PPO coverage year-round. COBRA extends prior employer coverage for up to 18 months. STLDI is the final option for healthy Iowans with no qualifying event and no Medicaid eligibility — plans can be issued for up to 364-day initial terms and renewed up to 36 months total under current Iowa rules.

Iowa Health Insurance Resources

Complete 2026 guide — all 6 Iowa carriers, IA Health Link, Hawk-I, and county coverage.

Iowa Health Insurance MarketplaceHealthCare.gov enrollment, Special Enrollment Periods, and 2026 subsidy changes.

Best Health Insurance in IowaWellmark PPO vs. Oscar — Iowa carrier comparison and off-exchange PPO plan guide.

Affordable Health Insurance IowaIA Health Link at $0, Hawk-I, and premium tables — lowest-cost Iowa options for 2026.

Individual Health Insurance IowaIowa Farm Bureau plans, off-exchange Wellmark, and self-employed coverage options.

PPO Health Insurance PlansHow PPO networks work, Wellmark BlueCard access, and PPO vs. HMO for Iowa residents.

Find the Right Iowa Coverage for Your Gap in 2026

Iowa allows STLDI with initial terms up to 364 days, renewable to 3 years — but IA Health Link at $0 up to $22,020, Oscar SEP plans from ~$496/month, and Wellmark PPO year-round are often better choices. Compare all Iowa options before choosing short-term.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Iowa residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.