Short-Term Health Insurance in Michigan: 2026 Rules, Limits, and Better Options

Short-term health insurance in Michigan is temporary coverage capped at 185 days in any 365-day period, with no renewal beyond that. At least six insurers sell it in Michigan, but it does not cover pre-existing conditions and is not ACA-compliant. It works only as a stopgap between real plans — this guide explains the rules and your better options.

How Short-Term Health Insurance Works in Michigan

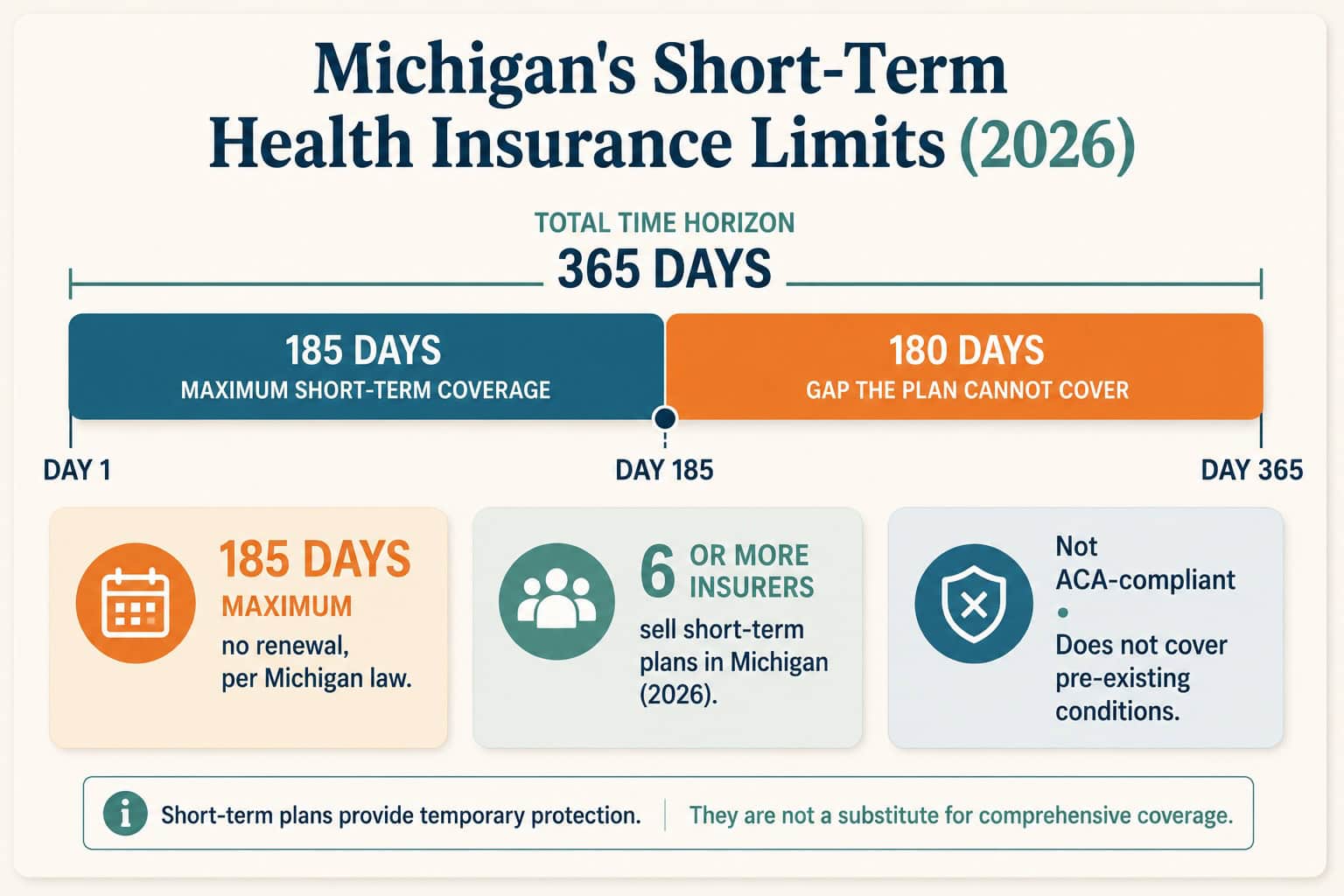

Short-term health insurance in Michigan is limited by state law to 185 days — about six months — within any 365-day period with the same insurer, and it cannot be renewed or extended beyond that. At least six insurers sold these plans in Michigan as of early 2026, and Michigan requires them to be issued immediately upon a completed application.

Michigan’s 185-day cap is stricter than the current federal limit, and state rules govern. Because a short-term plan in Michigan is issued without medical underwriting up front, you can get covered quickly — but insurers can use post-claims review to deny anything tied to a pre-existing condition. This is why temporary health insurance in Michigan is best treated as a true bridge, not a replacement for a full plan.

You cannot stack short-term plans to stay covered all year. Michigan limits you to 185 days of short-term coverage from the same insurer in any 365-day period, with no renewal. If you need coverage beyond that, you will need a comprehensive plan — see the alternatives below.

What Short-Term Plans Do and Don’t Cover in Michigan

A short-term health insurance plan in Michigan can cover unexpected illness or injury at a lower premium, but it does not cover pre-existing conditions and is not required to cover the ten essential health benefits. It is not minimum essential coverage, so it can exclude maternity, mental health, and prescription drugs, and may impose dollar limits.

| Feature | Short-term plan (Michigan) | ACA comprehensive plan |

|---|---|---|

| Pre-existing conditions | Not covered | Always covered |

| Essential health benefits | Not guaranteed | All 10 covered |

| Maximum duration | 185 days, no renewal | Full year, renewable |

| Counts as minimum coverage | No | Yes |

| Premium subsidies | Not eligible | Eligible up to 400% FPL |

Because a short-term plan skips these protections, its premium is lower — which is the whole appeal — but a single serious claim can leave you exposed. Read the disclosure notice Michigan requires on every short-term application before you buy.

Who Short-Term Coverage in Michigan Suits

Short-term health insurance in Michigan suits a narrow group: healthy people who need to bridge a gap of a few months and do not qualify for a subsidy. Common cases are waiting for an employer plan to start, missing open enrollment without a qualifying event, or covering the weeks before Medicare begins.

Waiting for an employer plan

Starting a new job with a coverage waiting period? A short-term plan can bridge the few weeks until benefits begin.

Missed open enrollment

No qualifying life event and open enrollment has closed? Temporary health insurance in Michigan can hold you over until the next enrollment window.

Just before Medicare

Turning 65 soon? A short gap plan can cover the weeks before your Medicare coverage starts.

Not who it suits

If you have any ongoing condition, take regular medications, or need coverage past six months, short-term is the wrong tool.

Not Sure Short-Term Is Right?

Compare short-term and comprehensive Michigan plans side by side and see which fits your situation.

Better Options Than Short-Term for Most Michiganders

For most people, a comprehensive plan beats short-term health insurance in Michigan. If you lost coverage, a job loss or move opens a 60-day Special Enrollment Period on HealthCare.gov. If your income is low, the Healthy Michigan Plan (Medicaid) may cover you at little cost — both give real protection short-term plans cannot.

Even with premiums up a state-approved 20.2% for 2026, an ACA plan covers pre-existing conditions and essential health benefits, and you may qualify for a subsidy up to 400% of the poverty level. Before defaulting to a short-term plan, check whether you qualify for a Michigan individual plan through a Special Enrollment Period or for a lower-cost comprehensive plan. You can confirm Michigan’s short-term rules directly with the Michigan Department of Insurance and Financial Services.

Buying Short-Term Health Insurance in Michigan

If a short gap plan is genuinely the right fit, you buy short-term health insurance in Michigan directly from an insurer or through a licensed agent — not on HealthCare.gov, since it is not a Marketplace product. Coverage is issued immediately on a completed application, but read the pre-existing-condition and duration terms first.

Compare the premium against what you would pay for a comprehensive plan after any subsidy — sometimes the real plan costs less than expected. If you do buy short-term, note your 185-day limit and plan your transition to full coverage before it ends. You can also enroll through HealthCare.gov the moment you qualify for a Special Enrollment Period.

Example — a Detroit worker between jobs. A healthy 27-year-old starts a new job in five weeks with a coverage waiting period. A short-term plan bridges the gap cheaply — but because his new employer plan starts soon, he sets a reminder to drop the short-term plan the day his real coverage begins, so he is never relying on it for anything serious.

Related Michigan Health Insurance Resources

The statewide guide to 2026 plans, costs, and how coverage works in Michigan.

Michigan Marketplace & SubsidiesHow HealthCare.gov works for Michigan and who qualifies for premium tax credits.

Individual Health Insurance MichiganComprehensive coverage you buy for yourself, with real ACA protections.

Affordable Health Insurance MichiganLower-cost 2026 options and ways to reduce your monthly premium.

Michigan Health Insurance PlansPlan types, metal tiers, and how Michigan coverage is structured.

Michigan Health Insurance CompaniesWho the insurers are, their networks, and where they operate across Michigan.

Private Health Insurance MichiganOff-exchange private plans, including PPO options, for buyers without subsidies.

Michigan Health Insurance QuotesCompare personalized 2026 plan pricing for your ZIP code in minutes.

Frequently Asked Questions About Short-Term Health Insurance in Michigan

How long can short-term health insurance last in Michigan?

Short-term health insurance in Michigan is limited to 185 days — about six months — within any 365-day period with the same insurer, and it cannot be renewed or extended beyond that. Michigan’s cap is stricter than the federal limit, and you cannot stack plans to stay covered longer.

Does short-term health insurance in Michigan cover pre-existing conditions?

No. Short-term plans in Michigan do not cover pre-existing conditions. They are issued immediately without underwriting, but insurers can review your records after a claim and deny anything tied to a pre-existing condition, leaving you responsible for the cost.

Is short-term coverage ACA-compliant?

No. Short-term health insurance in Michigan is not ACA-compliant and is not minimum essential coverage. It is not required to cover the ten essential health benefits, can exclude maternity, mental health, and prescription drugs, and does not qualify for premium subsidies.

Who should buy temporary health insurance in Michigan?

It suits healthy people bridging a short gap — waiting for an employer plan, between jobs, or covering the weeks before Medicare — who do not qualify for a subsidy. Anyone with an ongoing condition or a need for coverage beyond six months should choose a comprehensive plan instead.

How do I buy short-term health insurance in Michigan?

You buy it directly from an insurer or through a licensed agent, not on HealthCare.gov, since it is not a Marketplace product. Coverage starts immediately on a completed application. Before buying, compare it against a comprehensive plan, which may cost less after any subsidy you qualify for.

Compare Short-Term and Comprehensive Plans

Get quotes for both and enroll with help from a licensed agent — at no extra cost to you.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Michigan residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.