Mississippi Health Insurance 2026: Plans, Carriers & Costs

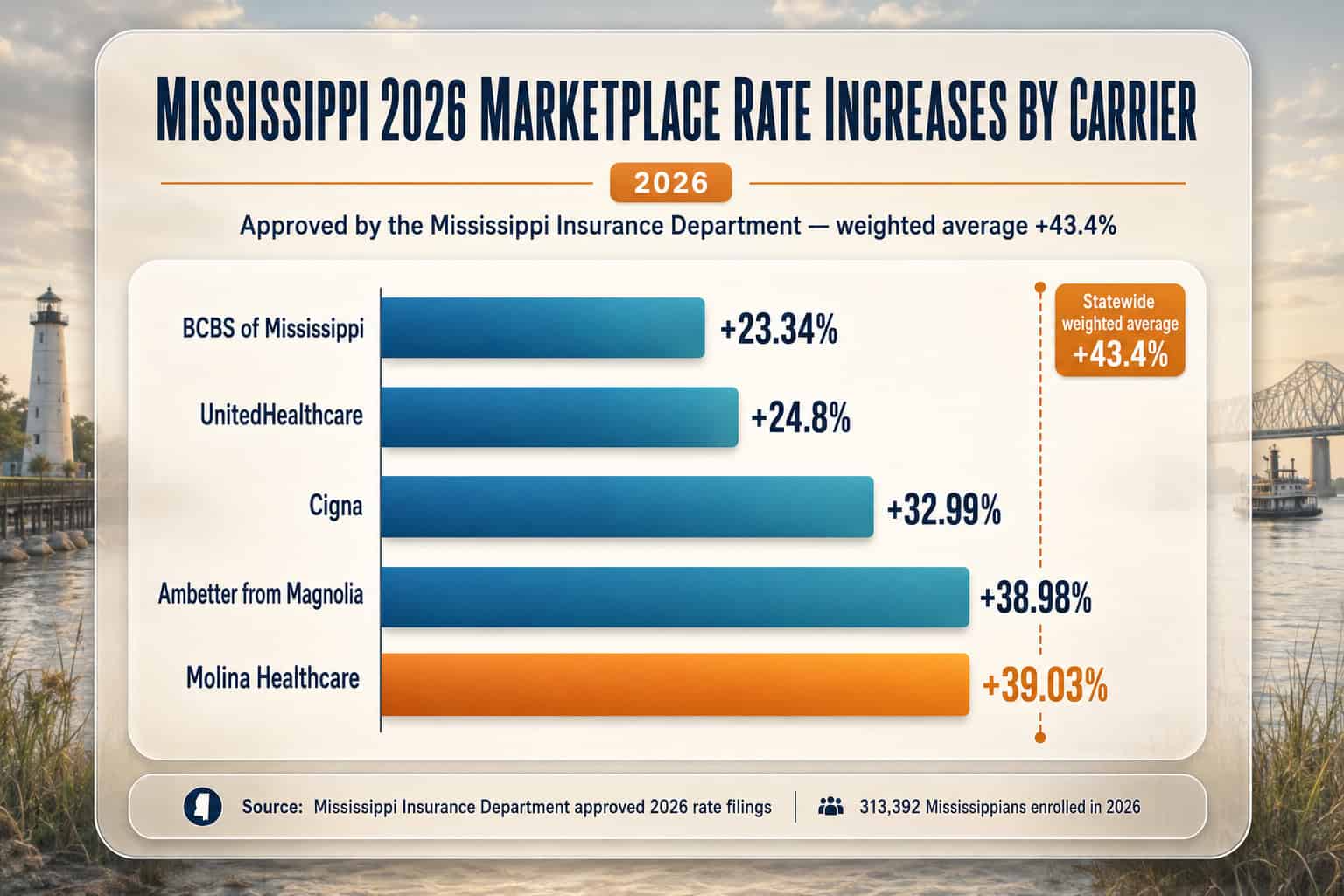

Mississippi health insurance enters one of the most turbulent years in marketplace history for 2026. Five carriers offer plans on HealthCare.gov, but every one is raising rates, producing a weighted statewide average increase of 43.4% — among the steepest in the nation. Ambetter from Magnolia Health is up 38.98%, Molina 39.03%, Cigna 32.99%, UnitedHealthcare 24.8%, and Blue Cross Blue Shield of Mississippi 23.34%. Roughly 313,392 Mississippians enrolled in marketplace coverage for 2026, yet the Mississippi Insurance Department projects up to 200,000 could drop coverage if enhanced subsidies expire. This guide to Mississippi health insurance covers what’s available, who qualifies for Medicaid in a state that has not expanded it, what small employers can offer, and how to find the best path through a difficult 2026.

What brings you to Mississippi health insurance today?

Mississippi’s Marketplace Under Pressure in 2026

Ambetter from Magnolia Health, the Mississippi marketplace’s largest carrier, sells alongside four others on HealthCare.gov — the federal exchange Mississippi uses because it runs no state-based platform. Five carriers offer 2026 plans: Ambetter, Blue Cross Blue Shield of Mississippi, Cigna, Molina Healthcare, and UnitedHealthcare, with Oscar Health newly entering 11 counties. The Mississippi Insurance Department regulates every approved rate.

Mississippi health insurance is sold through HealthCare.gov because the state does not operate its own exchange. Mississippi enacted HB1647 in May 2024, authorizing the Insurance Commissioner to build a state-based exchange platform, but the state still used the federal marketplace for 2026. Under federal CMS rules, a state must run a state-based exchange on the federal platform for at least one year before transitioning to a fully independent system — meaning the earliest Mississippi could enroll residents through its own exchange would be fall 2027 for 2028 coverage.

Residents enroll through HealthCare.gov during Open Enrollment, and Oscar Health’s 2026 entry into 11 counties marked the first new carrier in years even as Primewell Health Services exited. The Mississippi marketplace guide walks through how the federal exchange works step by step, including which plans appear in each county and how subsidies are applied at checkout.

The 2026 Marketplace Carriers in Mississippi

Five carriers offer Mississippi health insurance through HealthCare.gov for 2026: Ambetter from Magnolia Health (largest, 142,324 enrollees, +38.98%), Blue Cross Blue Shield of Mississippi (+23.34%, the state’s only true PPO), Cigna (+32.99% EPO, 53,064 enrollees), Molina Healthcare (+39.03%), and UnitedHealthcare (+24.8%). Oscar Health newly enters 11 counties around Jackson and northern Mississippi. Celtic sells only off-exchange.

| Carrier | 2026 Rate Change | Coverage Area | Network Type |

|---|---|---|---|

| Ambetter from Magnolia Health | +38.98% | Statewide (largest, 142,324 enrollees) | HMO |

| Blue Cross Blue Shield of Mississippi | +23.34% | Statewide (on- and off-exchange) | PPO + HMO |

| Cigna | +32.99% | Select counties (53,064 enrollees) | EPO |

| Molina Healthcare | +39.03% | Select counties | HMO |

| UnitedHealthcare | +24.8% | Select counties | HMO |

| Oscar Health (NEW for 2026) | New entrant | 11 counties — Jackson & northern MS | HMO |

| Celtic (off-exchange only) | Off-exchange | Select counties | HMO |

Ambetter from Magnolia Health dominates Mississippi health insurance by enrollment and holds a 5-star customer-experience rating on HealthCare.gov despite its steep 2026 increase. Blue Cross Blue Shield of Mississippi is the only true PPO option in the state and markets heavily off-exchange, where subsidies do not apply — making it most attractive to higher-income, unsubsidized households that value network flexibility. Because network breadth and PPO access are the deciding factor for many shoppers, the Mississippi carrier comparison guide ranks each plan on PPO availability, provider directories, and 2026 value.

What Mississippians Will Actually Pay in 2026

Mississippi health insurance averages roughly $756/month at full price for a 40-year-old Silver plan in 2026 — among the highest nationally — but most subsidized enrollees pay closer to $85/month. Oscar Health offers the cheapest Silver near $630/month before subsidy in its 11-county area, Cigna EPO Silver about $692, and Ambetter HMO Silver about $695. Costs vary by county, age, and tobacco use.

| Scenario (40yo Silver) | Full Premium | Est. Subsidy | Net Cost |

|---|---|---|---|

| Hinds County (Jackson), $38,000 income | ~$695/mo | ~$510/mo | ~$185/mo |

| Harrison County (Gulfport), $42,000 income | ~$720/mo | ~$485/mo | ~$235/mo |

| Forrest County (Hattiesburg), $50,000 income | ~$705/mo | ~$385/mo | ~$320/mo |

| DeSoto County (Southaven), $55,000 income | ~$680/mo | ~$315/mo | ~$365/mo |

| 62yo couple, $82,000 income (subsidy cliff) | ~$2,265/mo | ~$1,580/mo | ~$685/mo |

Full-price Mississippi health insurance premiums sit among the highest in the country, but subsidies historically absorb most of the cost for roughly 90% of marketplace enrollees who qualify. The subsidy cliff is especially painful here: an unsubsidized 40-year-old earning $62,600 or more would pay the full $9,072 a year for an average Silver plan if enhanced credits expire. For households just above the threshold, an Ambetter or BCBS Mississippi off-exchange plan paired with HSA contributions to lower taxable income can unlock real savings. Shoppers buying on their own should also review the Mississippi individual coverage guide, and the affordable coverage guide walks through every subsidy strategy.

Example — Hinds County single adult, age 40, $38,000 income: A Jackson resident earning about 250% FPL shops the 2026 marketplace, where the benchmark Silver lists near $695 per month at full price. An estimated premium tax credit of roughly $510 per month brings the net cost to about $185 per month. Because Oscar Health newly serves Hinds County, the same shopper can compare Oscar’s cheaper $630 full-price Silver against Ambetter’s 5-star-rated HMO before enrolling — verifying that their doctors are in-network either way. The subsidy does the heavy lifting: without it, that $695 premium would cost more than $8,300 a year.

See Mississippi Coverage Options for Your County

Compare 2026 plans from all five Mississippi marketplace carriers — including Oscar Health’s new 11-county entry. Check subsidy eligibility, see after-subsidy pricing, and find coverage that fits your household budget despite the steep 2026 rate increases.

Premium Tax Credits and Subsidies in Mississippi

The Mississippi Insurance Department projects up to 200,000 residents could lose coverage if enhanced premium tax credits expire — a warning that frames how subsidies work statewide. Premium tax credits cap a household’s benchmark Silver premium at a set share of income for those between 100% and 400% of the Federal Poverty Level, while cost-sharing reductions add further discounts on deductibles and copays for Silver enrollees under 250% FPL.

Premium tax credits are the single biggest lever on Mississippi health insurance costs, capping the amount a household pays for the benchmark second-lowest-cost Silver plan as a percentage of income. Mississippi residents who lose subsidies in 2026 may qualify for CMS-expanded catastrophic plan eligibility under the new hardship exemption — a path designed for households facing the subsidy cliff. Credits reconcile annually at tax time on IRS Form 8962.

Mississippi subsidy cliff warning for 2026: Mississippi faces one of the largest projected subsidy-loss impacts in the nation. If enhanced credits expire, a 60-year-old Mississippi couple earning $82,000 — just above 400% FPL for two — could see premiums jump from roughly $685/month to more than $2,200/month, an increase near $18,000 a year. Households near the cliff should model projected income with a Help Health Mississippi navigator or a licensed broker; HSA and traditional IRA contributions can keep income below the threshold and preserve thousands in subsidies.

Mississippi Medicaid and the Coverage Gap

Mississippi Medicaid, run by the Mississippi Division of Medicaid, covers roughly 590,816 residents through the MississippiCAN managed-care program as of October 2025. Mississippi has not expanded Medicaid under the ACA — one of just 10 remaining non-expansion states. About 71,000 low-income adults sit in the coverage gap: too poor for marketplace subsidies yet ineligible for Mississippi Medicaid.

Mississippi Medicaid eligibility is among the strictest in the country. Adults with dependent children qualify only at incomes up to roughly 22% FPL — about $488/month for a family of three — one of the lowest thresholds in the nation. Childless non-disabled adults under 65 do not qualify regardless of income. Children qualify up to 209% FPL through Medicaid, and CHIP extends to 214% FPL ($65,486 for a family of four). Pregnant women qualify up to 194% FPL with newly extended 12-month postpartum coverage.

For Mississippians in the coverage gap, options are limited but real. More than 21 Federally Qualified Health Centers provide sliding-scale primary care statewide, rural hospitals run charity-care programs, and nonprofit free clinics operate in most metros. Marketplace plans through HealthCare.gov remain available to households at or above 100% FPL even when Medicaid is not. Apply through the Mississippi Division of Medicaid or call 1-800-421-2408. The affordable coverage guide details every pathway for low-income Mississippi residents.

Carrier Choice by Mississippi Region — Jackson, Coast, Delta

Mississippi health insurance options vary sharply by region. Jackson metro now has the most competition — Oscar Health joins Ambetter, BCBS MS, Cigna, Molina, and UnitedHealthcare for six carriers. The Gulf Coast around Gulfport and Biloxi typically has five, North Mississippi (DeSoto, Oxford, Tupelo) gained Oscar for six, the Pine Belt around Hattiesburg has three, and rural Delta counties have the fewest.

Jackson is the most competitive Mississippi health insurance market for 2026, with Oscar’s entry bringing six carriers to Hinds, Madison, Rankin, and surrounding counties. The major systems include the University of Mississippi Medical Center, Baptist Memorial Health Care, and Merit Health Central. Blue Cross Blue Shield of Mississippi offers the broadest PPO network statewide, particularly attractive to Jackson-area professionals who want academic medical center access.

The Gulf Coast — Harrison, Hancock, and Jackson counties — relies on Ambetter, BCBS MS, Cigna, Molina, and UHC, anchored by Memorial Hospital at Gulfport, Singing River Health System, and Ocean Springs Hospital. North Mississippi residents benefit from proximity to Memphis-area hospitals and from Baptist Memorial Hospital-North Mississippi in Oxford, while Hattiesburg’s Forrest General Hospital anchors the Pine Belt. Rural Delta residents face the most limited choice, often only Ambetter and BCBS MS. The Mississippi carrier comparison guide covers network strength and PPO access region by region.

Small-Group Coverage for Mississippi Employers

Blue Cross Blue Shield of Mississippi anchors most small-group plans in the state, the practical starting point for Mississippi employers weighing coverage. The federal Small Business Health Care Tax Credit is worth up to 50% of premiums for employers with fewer than 25 full-time-equivalent employees, average wages under roughly $62,000, that contribute at least 50% and buy through SHOP. Mississippi businesses under 50 employees face no federal coverage mandate.

Small employers in Mississippi most often build group plans around Blue Cross Blue Shield of Mississippi’s PPO network, with Ambetter and UnitedHealthcare offering HMO group products in select counties. Because group PPO plans give employees the out-of-network flexibility that dominant HMO marketplace options lack, many Mississippi businesses treat network breadth as the deciding factor — the same PPO-access question covered in the Mississippi carrier comparison guide. Employers with fewer than 25 employees should calculate the federal tax credit before assuming group coverage is unaffordable; the credit is highest for the smallest, lowest-wage firms and phases out as headcount and wages rise.

For very small Mississippi employers, an alternative to a group plan is reimbursing employees for individual coverage through a QSEHRA or ICHRA, letting staff buy their own HealthCare.gov plans tax-free up to a set monthly amount. Mississippi sole proprietors and 1099 contractors without employees are not eligible for group plans at all and should shop the individual Mississippi health insurance market instead.

Enrolling in Mississippi Marketplace Coverage for 2026

Help Health Mississippi, operated by the Mississippi Health Advocacy Program, offers free enrollment help statewide at 601-376-9000 — the local front door to a federal process. Open Enrollment for 2026 coverage ran November 1, 2025 through January 15, 2026; for 2027 the federal window shortens to November 1 through December 15, 2026. Outside that window, a Qualifying Life Event opens a 60-day Special Enrollment Period.

For 2027 coverage the federal government shortened Open Enrollment by about four weeks, and there is no automatic renewal — every household must actively reselect a plan, update income and household details, and reconfirm subsidy eligibility. Qualifying Life Events that trigger a Special Enrollment Period include marriage, the birth of a child, job loss, loss of Medicaid, and moving to Mississippi. The Mississippi marketplace guide walks through enrollment step by step, and a licensed broker can confirm which Mississippi health insurance plans match your providers before you submit.

Common Questions From Mississippi Enrollees

How much does Mississippi health insurance cost in 2026?

Mississippi marketplace premiums average roughly $756/month at full price for a 40-year-old Silver plan in 2026 — among the highest in the country. After premium tax credits, most subsidized Mississippians pay closer to $85/month. Oscar Health offers the cheapest Silver near $630/month full price in its 11-county service area. The 2026 weighted statewide average rate increase is 43.4%.

Which carriers offer Mississippi health insurance for 2026?

Five carriers offer marketplace plans on HealthCare.gov: Ambetter from Magnolia Health (largest), Blue Cross Blue Shield of Mississippi, Cigna (EPO), Molina Healthcare, and UnitedHealthcare. Oscar Health newly entered 11 counties around Jackson and northern Mississippi for 2026. Celtic sells only off-exchange, where premium subsidies cannot be applied.

Did Mississippi expand Medicaid?

No. Mississippi is one of just 10 remaining non-expansion states. Mississippi Medicaid covers children up to 209% FPL, pregnant women up to 194% FPL, and parents only at incomes up to roughly 22% FPL — about $488/month for a family of three. Childless non-disabled adults under 65 do not qualify regardless of income, leaving about 71,000 Mississippians in the coverage gap.

Does Mississippi have its own health insurance exchange?

Not yet. Mississippi uses HealthCare.gov, the federally facilitated marketplace. The Mississippi Insurance Commissioner gained authority to create a state-based exchange under HB1647 in 2024, but the state still used HealthCare.gov for the 2026 plan year. Under federal CMS rules, the earliest Mississippi could enroll residents through its own exchange would be fall 2027 for 2028 coverage.

Why are Mississippi 2026 rate increases so high?

The 43.4% weighted statewide average reflects three forces: the anticipated expiration of enhanced premium tax credits, which pushes healthier members to drop coverage; rising medical and prescription drug costs; and Mississippi’s already-elevated risk pool from non-expansion. Cigna cited subsidy expiration directly when filing its 32.99% increase. Subsidized enrollees may not feel the full impact because tax credits adjust to cap the household premium share.

Can a small business in Mississippi get a tax credit for offering coverage?

Possibly. The federal Small Business Health Care Tax Credit is worth up to 50% of premiums for an employer with fewer than 25 full-time-equivalent employees, average annual wages under roughly $62,000, that contributes at least 50% of premium cost and buys through SHOP. Blue Cross Blue Shield of Mississippi anchors most small-group plans in the state. Businesses with fewer than 50 employees face no federal requirement to offer coverage.

Can I keep my doctor with a Mississippi marketplace plan?

It depends on whether your provider is in the plan’s network. Blue Cross Blue Shield of Mississippi offers the broadest PPO network with out-of-network coverage. Cigna offers an EPO (in-network only, but generally larger than HMOs). Ambetter, Molina, UnitedHealthcare, and Oscar are HMOs requiring in-network care except for emergencies. Verify your specific doctors in each carrier’s directory before enrolling.

Related Mississippi Health Insurance Resources

Explore the rest of the Mississippi coverage cluster — marketplace enrollment, the best carriers compared, the coverage gap and affordability options, and PPO plan flexibility — to go deeper on any part of this guide.

HealthCare.gov enrollment, deadlines, subsidies, and qualifying life events.

Best Plans & CarriersAmbetter, Blue Cross Blue Shield of Mississippi, Cigna, and Oscar compared.

Affordable Coverage & the GapPremium tax credits, the coverage gap, Medicaid, and CHIP alternatives.

PPO PlansReferral-free specialist access and out-of-network coverage nationwide.

Compare 2026 Mississippi Coverage Plans

See all five Mississippi marketplace carriers including the new Oscar Health entry, check Medicaid eligibility, and get after-subsidy pricing from a licensed enrollment assistant. Free, with no cost to you.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Mississippi residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.