Montana Health Insurance: 2026 Plans, Carriers & Costs

Montana health insurance for 2026 is shaped by three statewide carriers, a voter-approved children’s program, a Medicaid expansion that nearly expired, and a reinsurance program that has kept unsubsidized premiums lower than they would otherwise be. Blue Cross Blue Shield of Montana (the largest at 44,116 members), Mountain Health CO-OP (one of just three ACA-created co-ops still operating nationally, with 23,974 members), and PacificSource (an Oregon-based regional carrier estimated at 17,000 members) all serve every county. The weighted average rate increase for 2026 is 29.1% — steep, but lower than many states because Montana’s reinsurance waiver absorbs some of the pressure. About 73,255 Montanans enrolled in marketplace coverage for 2026, down roughly 5% from 2025. This guide covers carriers, costs by city, the HELP Program Medicaid expansion, subsidies, small-group and short-term options, and how to navigate a market changing faster than most.

What brings you to Montana coverage today?

Three Carriers, Every County: How Montana’s Market Is Structured

Montana health insurance is sold through HealthCare.gov — the federal marketplace — because Montana does not run a state-based exchange. Three carriers offer plans statewide for 2026: Blue Cross Blue Shield of Montana, Mountain Health CO-OP, and PacificSource. Unlike many states where rural counties have only one carrier, every Montana county has access to all three. The Commissioner of Securities and Insurance, James Brown, regulates carrier rates and consumer protections.

Montana’s three-carrier marketplace is unusually competitive for a rural, low-population state. BCBS of Montana is the largest individual-market insurer with 44,116 enrollees and offers both POS and PPO plans — the PPO adding $126–$162/month in premium for nationwide out-of-network access. Mountain Health CO-OP is a nonprofit, member-owned cooperative, one of only three ACA-created CO-OPs still operating nationwide, and offers PPO plans with the cheapest Silver premiums in the state at about $639/month for a 40-year-old. PacificSource, based in Oregon, offers EPO plans but is eliminating out-of-network benefits entirely for 2026.

Montana also benefits from a state reinsurance program launched in 2020 under a 1332 State Innovation Waiver. The program subsidizes high-cost claims, keeping premiums for unsubsidized enrollees lower than they would be without the waiver — an estimated 10–15% lower than the market would otherwise produce. For Montanans who earn too much to qualify for premium tax credits, that is meaningful relief. Enrollment happens through HealthCare.gov during Open Enrollment (Nov 1 – Jan 15 for 2026; shortened to Nov 1 – Dec 15 for 2027), or year-round for enrolled members of federally recognized tribes, Medicaid-eligible residents, and those with a Qualifying Life Event.

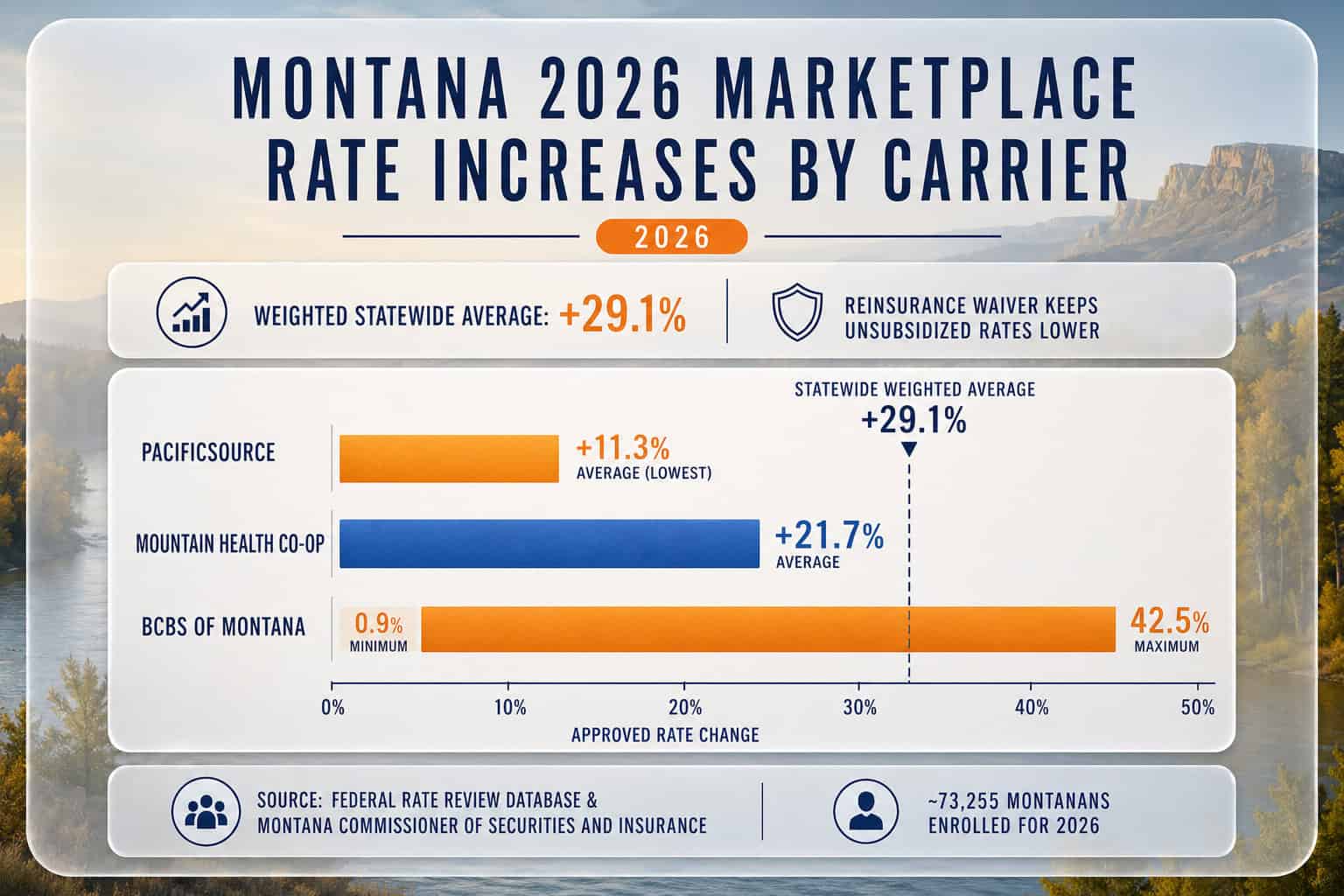

BCBS Montana, the CO-OP & PacificSource: 2026 Rate Filings

All three Montana health insurance carriers raised rates for 2026, but the increases vary widely. BCBS of Montana filed increases ranging from 0.9% to 42.5% across its plan portfolio (44,116 members affected). Mountain Health CO-OP filed an average 21.7% increase (23,974 members). PacificSource filed an average 11.3% increase, driven by medical inflation and its decision to eliminate out-of-network benefits. The weighted statewide average increase is about 29.1%.

| Carrier | 2026 Rate Change | Enrollees | Network Type | 40yo Silver |

|---|---|---|---|---|

| Blue Cross Blue Shield of Montana | +0.9% to +42.5% (varies by plan) | 44,116 | POS + PPO | $663 POS / $789 PPO |

| Mountain Health CO-OP | +21.7% average | 23,974 | PPO | $639 (cheapest Silver) |

| PacificSource | +11.3% average | ~17,000 est. | EPO (no out-of-network for 2026) | $754 |

Mountain Health CO-OP deserves particular attention. As a member-owned cooperative whose board is elected by policyholders, it operates as a nonprofit focused on member value rather than shareholder returns, and it holds about 40% of Montana’s individual market — second only to BCBS MT. The CO-OP provides free coverage for 250+ preventative drugs including insulin and blood-pressure medication, a benefit few traditional carriers match. For 2026, however, the CO-OP is limiting coverage to services within Montana and Idaho — out-of-state care (except emergencies and approved Utah referrals) will no longer be covered. The Montana carrier comparison guide breaks down network differences in detail.

What Montanans Pay in 2026 — Before and After Subsidies

Montana health insurance costs vary by carrier, metal tier, age, and county — but subsidies transform the math for most enrollees. Mountain Health CO-OP Silver at $639/month is the cheapest Silver for a 40-year-old; BCBS MT POS Silver runs $663/month, and PacificSource EPO Silver runs $754/month. About 89% of marketplace enrollees receive premium tax credits averaging $495/month in savings, and Montanans who don’t qualify for subsidies still benefit from the state’s reinsurance waiver.

| Scenario (40yo Silver) | Full Premium | Est. Subsidy | Net Cost |

|---|---|---|---|

| Billings, $38,000 income | ~$639/mo (CO-OP) | ~$450/mo | ~$189/mo |

| Missoula, $45,000 income | ~$663/mo (BCBS POS) | ~$395/mo | ~$268/mo |

| Great Falls, $52,000 income | ~$639/mo (CO-OP) | ~$320/mo | ~$319/mo |

| Bozeman, $60,000 income | ~$754/mo (PacificSource) | ~$350/mo | ~$404/mo |

| 60yo couple, Helena, $78,000 | ~$2,810/mo (CO-OP) | ~$2,210/mo | ~$600/mo |

City-by-city Montana health insurance quotes shift with income and age more than geography, since all three carriers price statewide. The subsidy cliff, though, hits Montana hard: a single 40-year-old in Missoula earning $62,600 (just above 400% FPL) would pay the full $663/month BCBS POS premium — $7,956/year — with no tax credit, while at $62,000 the same person might qualify for over $3,000/year in credits. Managing projected income through HSA contributions, traditional IRA contributions, or business-expense timing can keep MAGI below the threshold. The Montana affordable coverage guide details subsidy-optimization strategies, and a licensed assistant can pull exact Montana health insurance quotes for your county and household.

Example — a Billings single adult, age 40, earning $38,000: On this page’s cost table, the Billings $38,000 scenario pairs the cheapest Silver — Mountain Health CO-OP PPO at about $639/month full price — with an estimated $450/month premium tax credit, landing near $189/month net. At roughly 250% FPL, this enrollee also sits right at the cost-sharing-reduction line, so choosing Silver keeps CSR benefits in play, and the CO-OP’s free insulin and 250+ preventive drugs add value the premium alone doesn’t show. It’s a clear illustration of why about 89% of Montana enrollees take a subsidized plan over full price.

Compare Montana Coverage for Your County

See 2026 plans from all three statewide carriers — BCBS MT, Mountain Health CO-OP, and PacificSource. Check subsidy eligibility and after-subsidy pricing with a licensed enrollment assistant at no cost — serving Billings, Missoula, Great Falls, Helena, Bozeman, Kalispell, and rural Montana.

Premium Tax Credits and the Reinsurance Safety Net

About 89% of Montana marketplace enrollees receive premium tax credits, with average savings of $495/month. Eligibility runs from 100% to 400% FPL under baseline ACA rules, with enhanced subsidies through 2025 extending above 400% FPL by capping premiums at 8.5% of income. Montana’s 1332 reinsurance waiver adds a second layer of protection, subsidizing high-cost claims so unsubsidized premiums stay lower than the national average for a state this rural.

Premium tax credits reconcile annually at tax time via IRS Form 8962. Cost-sharing reductions apply automatically to Silver plans for enrollees under 250% FPL — about 33% of Montana marketplace enrollees received CSR benefits in 2025, according to HealthCare.gov data. For variable-income Montanans — ranchers, seasonal tourism workers in the Glacier and Yellowstone gateway communities, self-employed outfitters — projecting income accurately prevents year-end clawback.

Montana subsidy cliff warning: A 60-year-old couple in Helena earning $82,000 could see premiums jump from about $600/month to over $2,800/month if enhanced subsidies expire — a $26,400/year increase. The reinsurance waiver cushions unsubsidized rates but cannot fully replace the tax credit. Montanans near the cliff should model projected MAGI carefully with a licensed broker or Cover Montana navigator; HSA and IRA contributions can lower MAGI below the threshold.

The HELP Program: Montana’s Medicaid Expansion

Montana expanded Medicaid in 2016 through the HELP Program (Health and Economic Livelihood Partnership), covering adults ages 19–64 with income up to 138% FPL — about $21,597 for a single adult or $42,780 for a family of four. Roughly 75,318 Montanans are enrolled through the expansion as of June 2025, and total Medicaid and CHIP enrollment stood near 219,000 in late 2024. The federal government reimburses Montana $9 of every $10 spent on HELP expansion enrollees.

Montana’s expansion almost expired. The original HELP Program waiver required legislative reauthorization, and the program came within months of sunsetting in mid-2025 before lawmakers extended it. The 2021 legislature also removed 12-month continuous eligibility for most adult enrollees — meaning the state now reassesses eligibility whenever it discovers a change in income or household size, not just annually. Montanans on HELP should keep employment documentation current and report income changes promptly to avoid coverage gaps. Apply through Montana DPHHS at apply.mt.gov or by calling 1-888-706-1535.

Healthy Montana Kids — Montana’s voter-approved CHIP program, passed via Ballot Initiative I-155 in 2008 — covers children up to 143% FPL through Medicaid and up to 261% FPL through CHIP. About 120,000 Montana children (roughly half of all children in the state) receive coverage through it, including preventive care, dental, vision, and mental health services. Enrolled members of federally recognized tribes can join Medicaid or marketplace coverage year-round without a Qualifying Life Event — a significant provision in Montana, where about 9.3% of the population is Native American.

Covering a Montana Team: Small-Group, SHOP & ICHRA

Montana small-group rates rose about 11.7% for 2026 — far below the individual market’s 29.1% — and employers with 1–50 workers have three paths: a traditional small-group plan, the federal SHOP marketplace with its Small Business Health Care Tax Credit, or an ICHRA that reimburses employees for individual plans. ICHRA fits Montana’s three-carrier market especially well, giving staff more network choice than most group plans offer.

| Approach | Best For | 2026 Notes |

|---|---|---|

| Traditional small group | Employers wanting one carrier plan for all staff | ~11.7% average increase; starts the first of any month |

| SHOP marketplace | Under 25 FTEs seeking the tax credit | Up to 50% premium credit (35% for tax-exempt) |

| ICHRA | Employers wanting fixed, predictable cost | ~$400–$600/mo per employee; tax-free reimbursement |

Montana businesses purchasing through the federal SHOP marketplace may qualify for the Small Business Health Care Tax Credit — worth up to 50% of premium contributions (35% for tax-exempt organizations) for employers with fewer than 25 full-time-equivalent employees, average annual wages under $62,000, and at least 50% of employee-only premiums covered. For a qualifying 8-employee business, that credit can save $3,000–$9,000 a year. An ICHRA, meanwhile, lets an employer set a fixed monthly amount per employee — tax-deductible to the business, tax-free to the worker — applied to individual plans from any of the three statewide carriers. Montana has no state employer mandate, and the federal ACA mandate applies only to employers with 50 or more FTEs, so coverage is voluntary for most Montana businesses.

Short-Term Plans vs Real Montana Coverage

Most Montanans weighing short-term health insurance actually qualify for a Special Enrollment Period — job loss, a move, marriage, birth, or losing Medicaid each opens a 60-day window on HealthCare.gov, and tribal members and HELP-eligible adults can enroll year-round. Short-term plans aren’t ACA-compliant: they exclude pre-existing conditions, cap benefits, and skip preventive care, maternity, and mental health. For most Montanans, a subsidized plan costs less and covers far more.

Short-term coverage fills a genuinely narrow gap — a healthy Montanan who missed Open Enrollment, has no Qualifying Life Event, earns too much for HELP Medicaid, and needs catastrophic protection for 30 to 90 days until a new job’s plan begins. Even then, the math rarely favors it. A short-term plan typically runs $100–$250/month for a 40-year-old, but a 40-year-old in Billings earning $38,000 pays about $189/month for a Mountain Health CO-OP Silver PPO with full ACA benefits — comparable to or cheaper than a short-term plan that excludes pre-existing conditions, caps benefits, and provides no preventive care. Before settling for less, check a Special Enrollment Period and HELP eligibility at apply.mt.gov; the Montana marketplace guide shows how quickly a real plan can start.

Enrolling in Big Sky Coverage for 2026 and Beyond

Enrolled members of Montana’s federally recognized tribes can enroll or change plans year-round — a critical provision in a state that is 9.3% Native American — while everyone else uses HealthCare.gov during Open Enrollment. The 2026 window ran November 1, 2025 through January 15, 2026; for 2027, the federal window shortens to November 1 – December 15, 2026. Outside these windows, Montanans need a Qualifying Life Event for a 60-day Special Enrollment Period.

Cover Montana — the state’s navigator program at (844) 682-6837 — provides free enrollment assistance statewide, including virtual and phone appointments. Congress reduced navigator funding by 90% in early 2025, however, sharply cutting Cover Montana’s capacity heading into the shortened 2027 window. Tribal communities have additional support through IHS, Tribal Health Departments, and Urban Indian Health Centers. Licensed brokers like ForHealthInsurance.com access all three carriers and provide network verification and subsidy calculations at no cost. The Montana marketplace guide walks through step-by-step enrollment.

Montana Coverage From Billings to Glacier Country

Because all three carriers serve every county, Montana health insurance availability is uniform — the practical differences are provider networks. Billings Clinic and St. Vincent Healthcare anchor eastern Montana. In Missoula, Community Medical Center and Providence St. Patrick Hospital are the major systems. Benefis Health System serves Great Falls, Bozeman Health serves the Gallatin Valley, and Logan Health (formerly Kalispell Regional) anchors the Flathead. Network verification matters because not every hospital contracts with every carrier.

Billings is Montana’s largest city and the regional healthcare hub for eastern Montana, Wyoming, and the western Dakotas; Billings Clinic, a physician-led organization with over 4,000 employees, is in-network for all three carriers. Missoula is the second-largest city and home to the University of Montana. Bozeman is the fastest-growing city in the state, driven by remote-worker migration and a booming tech and outdoor economy — newcomers from states with more carriers should note the three-carrier limit. Great Falls sits between Glacier National Park and the Hi-Line and anchors north-central Montana, while Helena, the capital, and Butte round out the western corridor — and Montana health insurance from all three carriers reaches each of them.

Common Questions From Montana Residents

How much does Montana health insurance cost in 2026?

A 40-year-old Silver plan runs about $639/month (Mountain Health CO-OP PPO, cheapest), $663/month (BCBS MT POS), or $754/month (PacificSource EPO) at full price. After subsidies, about 89% of marketplace enrollees pay significantly less — average savings of $495/month. The statewide weighted average rate increase for 2026 is 29.1%, and Montana’s reinsurance waiver keeps unsubsidized premiums lower than most states.

Which carriers sell Montana health insurance?

Three carriers serve every Montana county: BCBS of Montana (POS + PPO, 44,116 enrollees), Mountain Health CO-OP (PPO, 23,974 enrollees, one of three surviving ACA co-ops nationally), and PacificSource (EPO, ~17,000 enrollees). PacificSource eliminated out-of-network coverage for 2026. BCBS MT’s PPO adds $126–$162/month over POS for nationwide out-of-network access.

Did Montana expand Medicaid?

Yes. Montana expanded Medicaid in 2016 through the HELP Program, covering adults ages 19–64 with income up to 138% FPL (about $21,597 single / $42,780 family of four). About 75,318 Montanans are enrolled through expansion as of June 2025, and the federal government reimburses Montana $9 of every $10 spent on expansion enrollees. Apply at apply.mt.gov or call 1-888-706-1535.

What is Healthy Montana Kids?

Healthy Montana Kids (HMK) is Montana’s voter-approved CHIP program (Ballot Initiative I-155, 2008), covering children up to 143% FPL through Medicaid and up to 261% FPL through CHIP. About 120,000 Montana children — roughly half of all children in the state — receive coverage through it. Benefits include preventive care, dental, vision, and mental health services.

Can tribal members enroll year-round in Montana?

Yes. Enrolled members of federally recognized tribes can enroll in or change HealthCare.gov marketplace plans year-round — no Open Enrollment restriction. Native American Medicaid and CHIP enrollment is also year-round, and AI/AN enrollees under 300% FPL qualify for zero-cost-sharing plans regardless of metal tier. Montana is about 9.3% Native American, the fourth-highest share nationally.

What is Montana’s reinsurance program?

Montana implemented a 1332 State Innovation Waiver reinsurance program in 2020. It subsidizes high-cost claims, keeping unsubsidized individual-market premiums an estimated 10–15% lower than they would otherwise be. The waiver produced overall average rate decreases in 2020 and relatively flat rates the next year. It does not affect subsidized enrollees directly but benefits unsubsidized Montanans above the subsidy threshold.

Do Montana small businesses have to offer health insurance?

No. Montana has no state employer mandate, and the federal ACA mandate applies only to employers with 50 or more full-time-equivalent employees. Most Montana businesses fall below that threshold and face no penalty. Employers that do offer coverage can choose a traditional small-group plan, the SHOP marketplace with its tax credit, or an ICHRA that reimburses employees for individual plans — small-group rates rose about 11.7% for 2026.

When does Open Enrollment end for Montana?

Open Enrollment for 2026 ran November 1, 2025 through January 15, 2026. For 2027 coverage, the window shortens to November 1 – December 15, 2026 (six weeks instead of ten). Cover Montana navigators provide free enrollment help at (844) 682-6837, though navigator capacity was reduced after a 90% cut in federal funding in early 2025.

Related Montana Health Insurance Resources

This overview links out to every focused Montana guide — HealthCare.gov enrollment, the three-carrier comparison, affordability pathways, and nationwide PPO options.

How HealthCare.gov works for Montanans — plans, subsidies, and deadlines.

BCBS MT, the CO-OP & PacificSourceMontana’s three carriers compared on price, network, and plan design.

HELP Medicaid, Subsidies & Low-Cost OptionsEvery affordability pathway — Medicaid, tax credits, and the reinsurance waiver.

PPO Health Insurance PlansNationwide PPO coverage options for individuals and families.

Find Your 2026 Montana Coverage

Compare all three statewide carriers, check HELP Program Medicaid eligibility, and get after-subsidy pricing from a licensed enrollment assistant. Free, no cost — serving Billings, Missoula, Great Falls, Helena, Bozeman, Kalispell, and every Montana county.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Montana residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.