Wisconsin Health Insurance 2026: Plans, Costs & Carriers

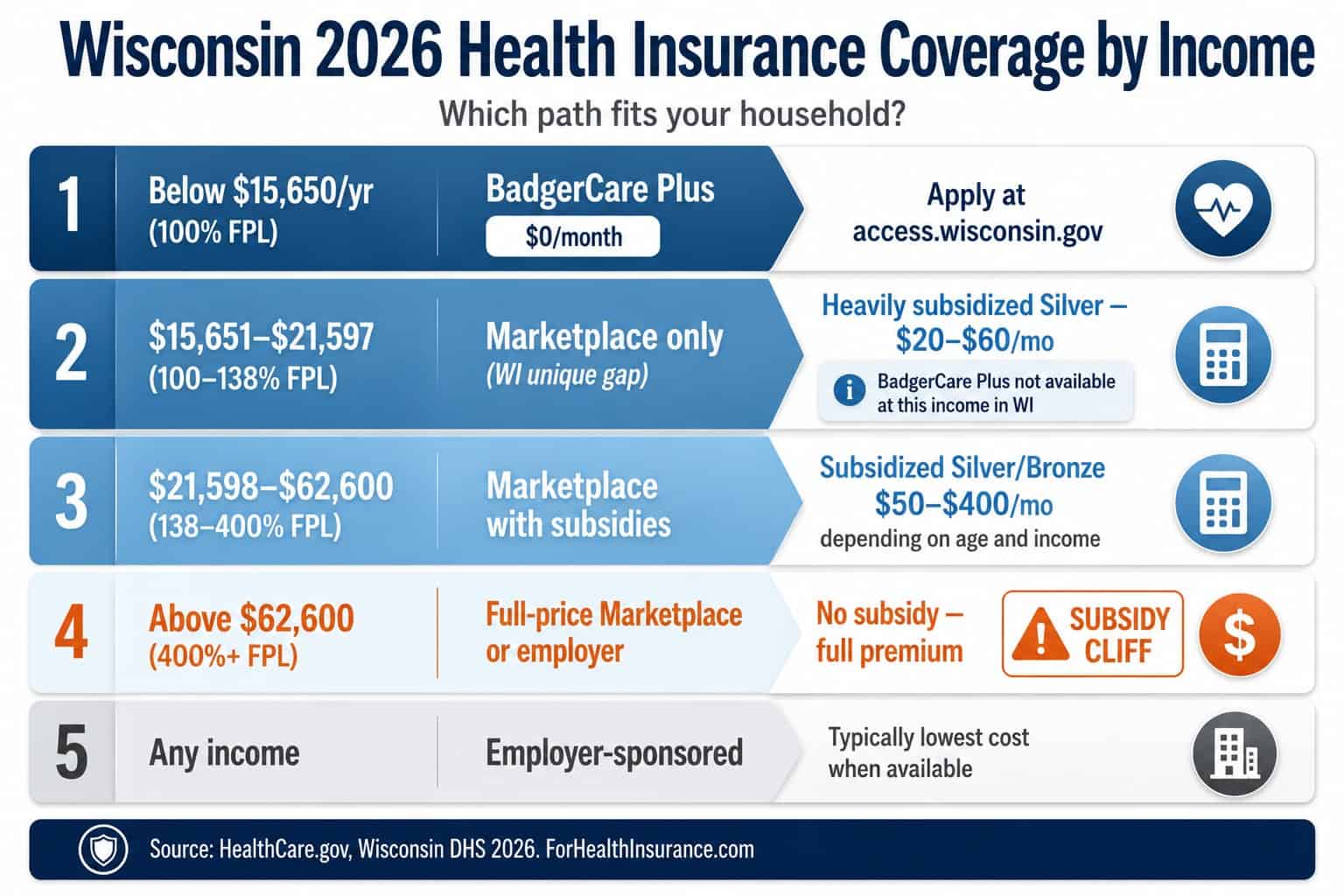

Health insurance Wisconsin residents can access in 2026 falls into four primary buckets: BadgerCare Plus (the state’s Medicaid program operating through the ForwardHealth system, covering adults to 100 percent of the federal poverty level and children to approximately 300 percent of FPL); marketplace plans on HealthCare.gov from twelve carriers — down from fourteen in 2025; employer-sponsored coverage through Wisconsin businesses; and short-term plans for transitions. The 2026 plan year brought significant disruption — a weighted average rate increase of 22.8 percent across the marketplace, the exit of Chorus Community Health Plans (which left approximately 11,000 eastern Wisconsin members searching for new coverage), and significant county-level pullouts from Anthem, Quartz, and Common Ground Healthcare Cooperative. Wisconsin is also one of the few states that did not adopt full ACA Medicaid expansion to 138 percent of FPL — instead using a federal waiver to cover adults to 100 percent of FPL — which means Wisconsin’s 100-to-138 percent FPL band depends entirely on the marketplace. This guide maps every part of the Wisconsin health insurance landscape for 2026: BadgerCare Plus eligibility, carrier-by-carrier marketplace breakdown, individual and small business options, short-term coverage, real premium examples, and the decision framework that fits each household’s situation.

What brings you here today?

Do I qualify for BadgerCare Plus?

Wisconsin Medicaid income limits and ForwardHealth enrollment

Check eligibility ↓See 2026 marketplace carriers

Anthem, Quartz, Dean, HealthPartners, MercyCare, and more

See carriers ↓Wisconsin Health Insurance Coverage Options at a Glance

Health insurance Wisconsin residents can access falls into four main categories: BadgerCare Plus Medicaid (free coverage for income-eligible Wisconsin households), marketplace plans on HealthCare.gov (subsidy-eligible coverage from twelve carriers), employer-sponsored insurance (group plans from Wisconsin businesses), and short-term medical plans (limited-duration coverage outside the ACA framework). Eligibility for each path is driven by household income, employment status, and life circumstances.

BadgerCare Plus (Wisconsin Medicaid)

Wisconsin’s Medicaid program — branded BadgerCare Plus and administered through the ForwardHealth system — covers adults to 100 percent of the federal poverty level and children and pregnant women to approximately 300 percent of FPL. Wisconsin did not adopt full ACA Medicaid expansion but uses a federal waiver to cover adults at the 100 percent threshold. Year-round enrollment through ACCESS Wisconsin.

- Adults: up to 100% FPL ($15,650 single)

- Children/pregnant: up to ~300% FPL

- Year-round enrollment

- Apply at access.wisconsin.gov

Wisconsin Marketplace (HealthCare.gov)

Twelve carriers offer 2026 marketplace plans in Wisconsin through HealthCare.gov, the federally facilitated platform. Premium tax credits offset costs for households between 100 and 400 percent of FPL. Wisconsin’s 100-138 percent FPL band relies entirely on marketplace coverage since BadgerCare Plus stops at 100 percent of FPL for adults.

- 12 carriers participating in 2026

- +22.8% weighted avg rate increase

- HealthCare.gov enrollment

- Open enrollment Nov 1 – Jan 15

Wisconsin Group Health Insurance

Most insured Wisconsin residents under 65 get coverage through an employer. Wisconsin small employers can offer fully-insured group plans, ICHRA, or QSEHRA arrangements. Major Wisconsin employers including UW System, Aurora Health Care, Northwestern Mutual, Kohl’s, and Fiserv provide health benefits to large workforces; small Wisconsin businesses can purchase through SHOP for tax credit eligibility.

- Pre-tax payroll deduction

- Often lower cost than marketplace

- Network typically broader than marketplace

- SHOP tax credit for <25 FTE employers

Short-Term Health Insurance

Short-term health insurance plans in Wisconsin are limited-duration medical coverage outside the ACA framework. They are not minimum essential coverage and do not satisfy ACA requirements for premium tax credits. Maximum federal terms are now 4 months initial plus 1-month renewal under 2024 federal rule changes. Useful for genuine coverage gaps but inappropriate for ongoing health insurance needs.

- Limited duration (4+1 months federal max)

- Not ACA-compliant

- Pre-existing conditions can be excluded

- For genuine coverage gaps only

Wisconsin State Group Health Insurance

The State of Wisconsin Group Health Insurance Program — administered by the Department of Employee Trust Funds (ETF) — provides health benefits to approximately 250,000 state employees, retirees, UW System employees, and local government employees who participate. ETF contracts with multiple commercial carriers including Quartz, Dean Health Plan, Network Health, and Group Health Cooperative for coverage delivery.

- Administered by ETF

- ~250,000 state and UW employees

- Multiple commercial carriers

- Significant employer subsidy

Medicare in Wisconsin

About one in five Wisconsin residents is 65 or older and Medicare-eligible. Wisconsin offers 113 Medicare Advantage plans for 2026, and major Wisconsin Medicare Advantage carriers include Aspirus Health Plan, Dean Advantage, Group Health Cooperative of Eau Claire, HealthPartners, Network Health, Quartz Medicare Advantage, Security Health Plan of Wisconsin, and UnitedHealthcare. The 2026 Wisconsin Medicare Advantage premium average is $23.44 per month.

- 113 Medicare Advantage plans for 2026

- $23.44 avg monthly premium

- $0 premium plans available statewide

- Multiple regional carriers

The choice between these health insurance Wisconsin paths is primarily driven by income, age, and employment. BadgerCare Plus is free for income-eligible Wisconsin residents and is almost always the right choice for those who qualify. Wisconsin marketplace plans become the right choice for adults above 100 percent of FPL who do not have employer coverage — the federal premium tax credits make subsidized coverage substantially cheaper than full-price plans. Employer-sponsored coverage almost always wins on cost when available, because the employer absorbs a substantial portion of the premium and contributions are pre-tax. Short-term plans are appropriate only for genuine coverage gaps — between jobs, waiting for marketplace effective date, or similar transitional situations — and should not be confused with ongoing health insurance.

BadgerCare Plus and ForwardHealth: Wisconsin’s Medicaid Program

BadgerCare Plus is Wisconsin’s Medicaid program, administered through the ForwardHealth system by the Wisconsin Department of Health Services. Adults aged 19 to 64 qualify up to 100 percent of FPL — approximately $15,650 for a single adult and $32,150 for a family of four in 2026. Children and pregnant women qualify up to approximately 300 percent of FPL. Wisconsin uses a federal waiver to cover adults at 100 percent of FPL rather than adopting full ACA expansion at 138 percent.

Wisconsin’s Medicaid structure is unusual among states and shapes the entire health insurance Wisconsin landscape. The Affordable Care Act gave states the option to expand Medicaid eligibility to 138 percent of the federal poverty level for non-disabled adults; about 40 states plus DC accepted full expansion. Wisconsin chose a different path — it did not adopt the ACA expansion to 138 percent, but it used a separate federal waiver under section 1115 to cover adults to 100 percent of FPL through BadgerCare Plus. This means Wisconsin has no traditional coverage gap (where adults below the federal poverty level have no affordable option), but adults between 100 and 138 percent of FPL must rely on the marketplace rather than Medicaid. In a true expansion state, those same adults would be on Medicaid. The Wisconsin Department of Health Services maintains BadgerCare Plus eligibility information at dhs.wisconsin.gov.

2026 BadgerCare Plus income limits (100% FPL for adults)

Single adult: up to $15,650/year ($1,304/month). Household of 2: up to $21,150/year. Household of 3: up to $26,650/year. Family of 4: up to $32,150/year. Children and pregnant women qualify at approximately 300 percent of FPL — about $96,450 for a family of four. Wisconsin’s parent and caretaker eligibility extends slightly higher. Income is calculated as Modified Adjusted Gross Income (MAGI) per federal Medicaid rules. Apply through ACCESS Wisconsin at access.wisconsin.gov or by calling 1-800-362-3002. Coverage is generally retroactive up to three months prior to application date for documented medical needs.

The ForwardHealth system is the foundation of public health insurance Wisconsin Medicaid members rely on for eligibility, enrollment, and benefits management. Wisconsin Medicaid members receive a ForwardHealth ID card used at any Wisconsin provider that accepts Medicaid, and most BadgerCare Plus members receive their care through managed care health plans contracted by the state. UnitedHealthcare Community Plan, Anthem Blue Cross Blue Shield, Children’s Community Health Plan, MercyCare Health Plans, Molina Healthcare, Network Health, Security Health Plan, and Trilogy Health Solutions all operate as BadgerCare Plus managed care organizations in different Wisconsin regions. Members in areas without managed care options receive coverage through fee-for-service Medicaid.

Wisconsin operates four Long-Term Care programs for adults with disabilities and elderly residents needing long-term services and supports, which is more pathways than most states offer. Family Care is a managed long-term care program providing home and community-based services. Family Care Partnership integrates Medicare and Medicaid for dual-eligible adults. IRIS (Include, Respect, I Self-Direct) is a self-directed long-term care program. The Medicaid Purchase Plan (MAPP) allows working adults with disabilities to buy into Medicaid above standard income limits. The Wisconsin Department of Health Services Aging and Disability Resource Centers (ADRCs) help applicants navigate which long-term care pathway fits their situation. For most working-age non-disabled Wisconsin residents, the relevant Medicaid program is BadgerCare Plus.

Get a Wisconsin Health Insurance Quote

A licensed Wisconsin agent screens for BadgerCare Plus eligibility, calculates your exact 2026 marketplace subsidy, compares all 12 carriers across UW Health, Aurora, Froedtert, Marshfield, and Bellin networks, and confirms your providers before enrollment. Free, no obligation for Wisconsin residents.

Wisconsin Health Insurance Marketplace: 2026 Carriers and Rates

The Wisconsin health insurance marketplace operates through HealthCare.gov for 2026, offering plans from twelve carriers — down from fourteen in 2025. The weighted average rate increase for 2026 was 22.8 percent. Anthem (Compcare), Quartz Health Benefit Plans, and Common Ground Healthcare Cooperative withdrew from multiple counties; Chorus Community Health Plans (owned by Children’s Wisconsin) exited the marketplace entirely, displacing approximately 11,000 eastern Wisconsin members.

Wisconsin uses HealthCare.gov rather than operating its own state-based exchange — making the federally facilitated platform the central hub for marketplace health insurance Wisconsin residents purchase. The Wisconsin Office of the Commissioner of Insurance (OCI) approves carrier rate filings; the Wisconsin Healthcare Stability Plan reinsurance program, in effect since 2019, has helped keep underlying premiums lower than they would otherwise be. Despite that reinsurance backstop, the 2026 weighted average rate increase landed at 22.8 percent — driven primarily by federal cost-sharing reduction non-funding, medical inflation, and adverse selection from the post-pandemic risk pool. The Wisconsin OCI publishes consumer rate review data at oci.wi.gov and operates the WisCovered.com consumer site for plan comparison and enrollment help.

| 2026 Wisconsin Carrier | Coverage Area | Network Anchor | 2026 Rate Change |

|---|---|---|---|

| Anthem Blue Cross Blue Shield (Compcare) | Statewide minus 10 counties | BlueCard national reciprocity | +31.4% |

| Quartz Health Benefit Plans | Madison-anchored, ~50 counties | UW Health, UnityPoint-Meriter, Aurora | Variable (county exits) |

| Dean Health Plan | South-central Wisconsin | Dean Medical Group, SSM Health | +13.14% |

| HealthPartners | Western and northwest WI | HealthPartners network, MN reciprocity | Variable |

| MercyCare Health Plans | Southern Wisconsin | Mercy Health, lowest 2026 Silver HMO | Variable |

| Group Health Cooperative | South-central Wisconsin | GHC-SCW providers | Variable |

| Security Health Plan | Northern and central WI | Marshfield Clinic Health System | Variable |

| Aspirus Arise Health Plan | Wausau-anchored, north-central WI | Aspirus Health | +12.6% |

| Common Ground Healthcare Cooperative (CareSource) | Statewide minus 11 counties | CareSource-operated co-op | Variable |

| Network Health | Northeast Wisconsin | Aurora, Bellin, ThedaCare, Door County Medical | Variable |

| Molina Healthcare | Select southeastern counties | Molina national network | Variable |

| Together with CCHP | Select counties | Children’s Community Health Plan partnership | Variable |

Coverage area is the most important factor in carrier selection. Multiple Wisconsin marketplace carriers serve only a subset of counties — the lowest premium you see in a quote tool may not be available at your ZIP code. Quartz, the UW Health-affiliated carrier serving Madison and south-central Wisconsin, withdrew from approximately 20 counties for 2026 including Brown, Milwaukee, Outagamie, Kenosha, and Marinette. Anthem (operating as Compcare in Wisconsin) withdrew from 10 counties for 2026 including Columbia, Dane, Green, and Walworth — meaning Madison-area Anthem members lost access. Common Ground Healthcare Cooperative, operated by CareSource, withdrew from 11 counties including Milwaukee, Racine, Kenosha, Sheboygan, and Fond du Lac. Chorus Community Health Plans exited entirely, displacing approximately 11,000 enrollees concentrated in eastern Wisconsin.

The 2026 health insurance Wisconsin marketplace exit pattern reflects a broader pressure: post-2025 federal policy changes — including the expiration of enhanced premium tax credits and the federal rule shortening the open enrollment window — combined with utilization patterns that emerged after the unwinding of the COVID-era continuous Medicaid coverage protections, made certain county footprints unprofitable for some carriers. For affected Wisconsin residents, the practical implication: if you were previously enrolled with Anthem, Quartz, Common Ground, or Chorus and your county was on the exit list, you needed to select a new carrier during 2026 open enrollment. Wisconsin residents who took no action during open enrollment may have been auto-mapped to a new carrier by HealthCare.gov, but verifying the new plan covers your providers is critical.

For complete coverage of marketplace structure, enrollment dates, subsidy calculation, and how to enroll, see the dedicated Wisconsin marketplace guide.

Individual and Family Health Insurance in Wisconsin

Individual health insurance Wisconsin residents purchase outside of an employer or BadgerCare Plus is available through the marketplace on HealthCare.gov (subsidy-eligible) or directly from carriers off-exchange (no premium tax credits). Family plans on the Wisconsin marketplace cover spouses and dependent children to age 26 under the same plan. Self-employed Wisconsinites — common in the state’s agricultural, construction, and professional services sectors — most often qualify for marketplace subsidies based on their Schedule C net income.

Individual health insurance Wisconsin marketplace coverage is the right path for working-age adults without an employer offer who earn between 100 and 400 percent of FPL. Within that band, federal premium tax credits make subsidized Silver plans dramatically more affordable than full-price coverage — and the 100-138 percent FPL band specifically depends on the marketplace because BadgerCare Plus stops at 100 percent for adults. Wisconsin’s marketplace allows enrollees to apply premium tax credits to any metal tier (Bronze, Silver, Gold, Platinum, or catastrophic for those under 30 with hardship exemption). Cost-sharing reductions — which lower deductibles and out-of-pocket maximums — are only available on Silver plans for households between 100 and 250 percent of FPL.

Self-employed Wisconsin residents — farmers, contractors, consultants, and small-business owners filing Schedule C — face the same individual marketplace options as W-2 workers without employer coverage. The key planning point: the IRS allows self-employed health insurance premiums to be deducted as an above-the-line adjustment to income on Form 1040, which can lower modified adjusted gross income and increase marketplace subsidy eligibility. A self-employed Wisconsin consultant with $80,000 of gross 1099 income who deducts $12,000 of marketplace premiums lowers MAGI to $68,000, which can shift them under the subsidy cliff and qualify them for premium tax credits they would otherwise miss. For self-employed and family-specific guidance, see the Wisconsin individual health insurance guide.

Small Business and Group Health Insurance in Wisconsin

Small business health insurance Wisconsin employers offer covers most of the state’s insured workforce. Wisconsin’s largest employers — Aurora Health Care, the UW System, Northwestern Mutual, Kohl’s, Fiserv, and Mercury Marine — provide group coverage to large workforces; small Wisconsin employers can purchase fully-insured group plans, use the SHOP marketplace for tax credit eligibility, or set up an ICHRA or QSEHRA. Wisconsin small group rates are governed by community rating rules under the ACA.

Wisconsin’s group health insurance market is among the largest and most diverse in the upper Midwest. Major Wisconsin employers offer comprehensive group coverage through commercial carriers including Anthem, Quartz, Dean Health Plan, HealthPartners, Network Health, Security Health Plan, and UnitedHealthcare. The State of Wisconsin Group Health Insurance Program — administered by the Department of Employee Trust Funds (ETF) — provides health benefits to approximately 250,000 state employees, retirees, UW System employees, and participating local government employees through multiple commercial carriers. Wisconsin small employers (1-50 full-time-equivalent employees) face no ACA employer mandate but commonly offer coverage to compete for talent.

The SHOP (Small Business Health Options Program) marketplace operates through HealthCare.gov for Wisconsin small employers seeking the Small Business Health Care Tax Credit. The credit — worth up to 50 percent of employer premium contributions — is available to Wisconsin businesses with fewer than 25 full-time-equivalent employees paying average wages below approximately $62,000 in 2026 who purchase coverage through SHOP. Alternatively, ICHRA (Individual Coverage Health Reimbursement Arrangement) became available January 1, 2020 and allows Wisconsin employers of any size to reimburse employees tax-free for individual marketplace plans rather than offering a traditional group plan. ICHRA has gained traction among Wisconsin small businesses with diverse workforces or remote employees spread across the state. For a complete look at small group, ICHRA, QSEHRA, and SHOP for Wisconsin businesses, see the Wisconsin small business guide.

Short-Term Health Insurance in Wisconsin

Short-term health insurance in Wisconsin provides limited-duration medical coverage outside the ACA framework, useful for transitions between jobs or while waiting for marketplace coverage to take effect. Federal rules effective in 2024 limit short-term plans to a maximum of 4 months initial term plus 1-month renewal. Short-term plans in Wisconsin can decline applicants for pre-existing conditions and exclude essential health benefits — they are not a substitute for ACA-compliant coverage.

Short-term health insurance Wisconsin residents most commonly use comes up in three situations: between W-2 jobs (when employer coverage has ended and the new employer’s coverage hasn’t started); waiting for marketplace coverage to take effect (between enrollment date and the first of the next month); and recent college graduates aging off a parent’s plan at 26 who haven’t yet enrolled in employer coverage. Short-term plans are inappropriate for anyone with a chronic health condition, pregnant women, or those needing mental health or substance use treatment — any of which can be excluded under short-term plan terms. Wisconsin residents whose income makes them subsidy-eligible should almost always choose a marketplace plan over short-term coverage, since a subsidized Silver or Bronze plan is typically lower-cost and provides full ACA essential health benefits. For situational guidance on when short-term Wisconsin coverage makes sense, see the Wisconsin short-term guide.

How Much Does Health Insurance Cost in Wisconsin in 2026?

Wisconsin 2026 marketplace premiums vary widely by carrier, geography, and age. For a 40-year-old, sample 2026 Silver monthly premiums include MercyCare HMO at $547 (lowest), Dean Health Plan EPO at $576, Group Health Cooperative at $605, HealthPartners PPO at $619, Anthem Silver POS at $716, and Security Health Plan at $766 (highest). Premium tax credits substantially offset these costs for most marketplace enrollees — and BadgerCare Plus is free for income-eligible Wisconsin residents.

| 2026 Wisconsin Plan (40-yr-old, Silver) | Plan Type | Monthly Premium | Notes |

|---|---|---|---|

| MercyCare | HMO | $547 | Lowest 2026 WI Silver HMO |

| Dean Health Plan | EPO | $576 | South-central WI |

| Group Health Cooperative | HMO | $605 | Madison-area |

| HealthPartners | PPO | $619 | Cheapest WI Silver PPO |

| Anthem (Compcare) | POS | $716 | Cheapest WI Silver POS |

| Quartz | HMO | ~$700–$760 | UW Health network |

| Security Health Plan | HMO | $766 | Marshfield Clinic, highest 2026 WI Silver HMO |

Age dramatically affects health insurance Wisconsin marketplace premiums — and Wisconsin’s age cost curve is steeper than many states. A 60-year-old pays roughly $1,161 per month for MercyCare’s Silver HMO compared with $547 for a 40-year-old on the same plan, a $614 monthly difference. By contrast, a 26-year-old typically pays around $438 per month for the same MercyCare plan. The federal age curve allows insurers to charge older enrollees up to three times what they charge younger enrollees, and Wisconsin’s curve generally hits the federal maximum. For Wisconsin pre-retirement adults aged 55-64 not yet Medicare-eligible, the combination of high age-rated premiums and the 400 percent FPL subsidy cliff (post-2025 enhanced credit expiration) creates the most expensive coverage exposure in the Wisconsin marketplace.

Geography also matters significantly. Wisconsin marketplace plans are priced by rating area — different premiums apply in Milwaukee, Madison, Green Bay, Eau Claire, La Crosse, and rural northern Wisconsin counties. The Milwaukee metro typically prices higher than south-central Wisconsin (Madison area), and northern rural counties served by Aspirus, Marshfield Clinic, and Security Health Plan often have fewer carriers competing, which affects both rates and plan availability. For affordability strategies and the full subsidy math, including the 100-138 percent FPL gap that depends on marketplace coverage in Wisconsin, see the affordable Wisconsin coverage guide.

How to Choose the Right Wisconsin Health Insurance Plan

Choosing the right health insurance Wisconsin plan starts with checking BadgerCare Plus eligibility (free coverage for income-eligible households), then evaluating employer coverage if available (typically lowest cost), then comparing marketplace plans across the state’s 12 carriers with subsidies factored in. Verify your specific providers — UW Health, Aurora, Froedtert, Marshfield Clinic, Bellin, ThedaCare, or Aspirus — are in-network for any plan you’re considering before enrollment.

The single most important step before plan selection is verifying which carriers serve your specific Wisconsin county. Multiple 2026 carrier exits and county pullouts mean that the cheapest plan you see in a generic premium comparison may not be available at your address. The HealthCare.gov plan comparison tool filters by ZIP code automatically, but the additional verification step is to confirm that the carrier’s network includes the hospitals and physicians you actually use. Wisconsin’s hospital and clinic systems vary by region: UW Health and UnityPoint-Meriter dominate in Madison and Dane County; Aurora Health Care and Froedtert & the Medical College of Wisconsin lead in Milwaukee; Marshfield Clinic Health System anchors central and northern Wisconsin; ThedaCare and Bellin Health serve the Fox Valley and northeast Wisconsin; Aspirus serves Wausau and the north-central region; Children’s Wisconsin in Milwaukee handles pediatric specialty care statewide. Match the network to your existing providers, then compare premium and out-of-pocket costs across the available health insurance Wisconsin plans for your county.

Out-of-pocket maximums matter as much as monthly premiums for Wisconsin shoppers planning around health risk. The two most expensive 2026 Wisconsin Silver HMO plans by monthly premium — Security Health Plan and Quartz — also carry the two highest out-of-pocket maximums, meaning a high-utilization year does not buy a lower financial ceiling despite the higher monthly cost. The lowest-premium Wisconsin Silver HMO from MercyCare frequently pairs with a moderate out-of-pocket maximum. For a Wisconsin household expecting low utilization (younger adults, no chronic conditions), a Bronze plan with a higher out-of-pocket max but lower premium often produces lower total annual cost. For a Wisconsin household expecting high utilization (chronic condition management, expected surgeries, family with young children), a Silver plan with cost-sharing reductions (if income-eligible) or a Gold plan typically wins on total cost despite higher monthly premium.

Frequently Asked Questions

Common questions about health insurance Wisconsin residents face cover 2026 marketplace premium costs, BadgerCare Plus eligibility under Wisconsin’s unique waiver structure, which carriers participate in the 2026 marketplace after the major exits, when open enrollment runs, whether Wisconsin has a coverage penalty, and how the ForwardHealth system works for Wisconsin Medicaid members.

How much does health insurance cost in Wisconsin in 2026?

Wisconsin individual marketplace premiums for 2026 averaged a 22.8 percent weighted increase over 2025 rates after final approval by the Wisconsin Office of the Commissioner of Insurance. Sample 2026 Silver plan monthly premiums for a 40-year-old include MercyCare HMO at $547, Dean Health Plan EPO at $576, Group Health Cooperative at $605, HealthPartners PPO at $619, Anthem Silver POS at $716, and Security Health Plan at $766. Wisconsin’s Healthcare Stability Plan reinsurance program, in effect since 2019, has helped keep underlying premiums lower than they would otherwise be. Most marketplace enrollees qualify for federal premium tax credits that offset a substantial portion of these costs.

Did Wisconsin expand Medicaid under the ACA?

No — Wisconsin did not adopt full ACA Medicaid expansion to 138 percent of the federal poverty level, but uses a federal waiver to cover adults under BadgerCare Plus up to 100 percent of FPL. This means Wisconsin has no traditional coverage gap (unlike non-expansion states such as Texas and Florida), because adults between 100 and 138 percent of FPL can access subsidized marketplace plans through HealthCare.gov. Children and pregnant women in Wisconsin qualify for BadgerCare Plus up to approximately 300 percent of FPL, which is more generous than most expansion states.

Which carriers sell health insurance in Wisconsin for 2026?

Twelve carriers offer 2026 marketplace plans in Wisconsin, down from 14 in 2025. Participating carriers include Anthem Blue Cross Blue Shield (Compcare), Quartz Health Benefit Plans, Dean Health Plan, HealthPartners, MercyCare, Group Health Cooperative of South Central Wisconsin, Security Health Plan, Aspirus Arise Health Plan, Common Ground Healthcare Cooperative (operated by CareSource), Network Health, Molina Healthcare, and Together with CCHP. Chorus Community Health Plans, owned by Children’s Wisconsin, exited the marketplace for 2026, displacing approximately 11,000 enrollees in eastern Wisconsin who needed to select a new carrier.

When is open enrollment for Wisconsin health insurance?

Open enrollment for 2026 Wisconsin marketplace coverage ran from November 1, 2025 through January 15, 2026 — that window is now closed. The federally facilitated marketplace at HealthCare.gov is the platform for Wisconsin individual enrollment. Open enrollment for 2027 plan coverage is scheduled to run November 1, 2026 through December 15, 2026 under the federal rule change shortening the window. Outside open enrollment, Wisconsin residents can only enroll through a Special Enrollment Period triggered by qualifying life events. BadgerCare Plus enrollment is open year-round through ACCESS Wisconsin at access.wisconsin.gov.

Does Wisconsin have a health insurance penalty for being uninsured?

No. Wisconsin does not have a state individual mandate penalty for being uninsured, and the federal individual mandate penalty has been $0 since 2019. Wisconsin is among the majority of states that have not enacted their own coverage requirement — unlike California, Massachusetts, New Jersey, Rhode Island, Vermont, and the District of Columbia. Wisconsin residents who go without qualifying health insurance face no tax penalty at the state or federal level, though they remain liable for any medical costs incurred while uninsured. Wisconsin’s emergency room costs and hospital billing rates are typical of the upper Midwest and a single uncovered hospitalization can run tens of thousands of dollars.

What is BadgerCare Plus and who qualifies?

BadgerCare Plus is the Wisconsin Department of Health Services Medicaid program, administered through the ForwardHealth system. Adults aged 19 to 64 qualify with household income up to 100 percent of the federal poverty level (approximately $15,650 for a single adult and $32,150 for a family of four in 2026). Children and pregnant women qualify up to approximately 300 percent of FPL. Enrollment is year-round through ACCESS Wisconsin at access.wisconsin.gov or by calling 1-800-362-3002. Wisconsin’s Long-Term Care programs include Family Care, Family Care Partnership, IRIS, and the Medicaid Purchase Plan (MAPP), which together serve adults with disabilities and elderly residents needing long-term services and supports.

Compare All Wisconsin Health Insurance Options

A licensed Wisconsin agent screens for BadgerCare Plus eligibility, calculates your exact subsidy, compares all 12 marketplace carriers across UW Health, Aurora, Froedtert, Marshfield, Bellin, ThedaCare, and Aspirus networks, and confirms your providers before enrollment. Free, no obligation.

Free Wisconsin coverage comparison covers BadgerCare Plus, marketplace, employer, and short-term in one call.

More on Wisconsin Health Insurance

HealthCare.gov enrollment, 12 carriers, 2026 subsidies, and open enrollment dates.

Wisconsin Individual & Family PlansIndividual and family marketplace plans, self-employed coverage strategies for Wisconsin.

Affordable Wisconsin Health InsuranceBadgerCare Plus, the 100-138% FPL gap, subsidies, and the 2026 cost landscape.

Wisconsin Small Business Health InsuranceGroup plans, ICHRA, QSEHRA, SHOP, and the Small Business Health Care Tax Credit for WI employers.

Wisconsin Short-Term Health InsuranceLimited-duration plans for genuine coverage gaps — federal 4+1 month limits explained.

Best Health Insurance in WisconsinCarrier-by-carrier comparison and PPO options for Wisconsin residents in 2026.

HealthCare.gov (Official)The federal Marketplace enrollment portal used by Wisconsin residents.

PPO Health Insurance PlansNational PPO options for Wisconsin residents who need out-of-state or multi-system provider access.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Wisconsin residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.