Small Business Health Insurance Iowa 2026: Group Plans, SHOP Credits, and Agricultural Employers

Small business health insurance Iowa options for 2026 include traditional group plans through carriers like Wellmark and Medica, the SHOP marketplace for employers seeking federal tax credits, and HRA alternatives like ICHRA and QSEHRA for businesses that prefer reimbursement over traditional group coverage. Iowa has no state-level employer mandate — the ACA requires coverage only for businesses with 50 or more full-time equivalent employees. Iowa’s agricultural economy adds a distinctive layer: farm operations with full-time hired labor, grain cooperatives, and rural service businesses across the state’s 99 counties all have coverage options suited to their size and structure.

What brings you here today?

ICHRA & QSEHRA alternatives

Reimbursement-based options — no traditional group plan required

Learn more →Iowa Small Business Health Insurance Options Overview

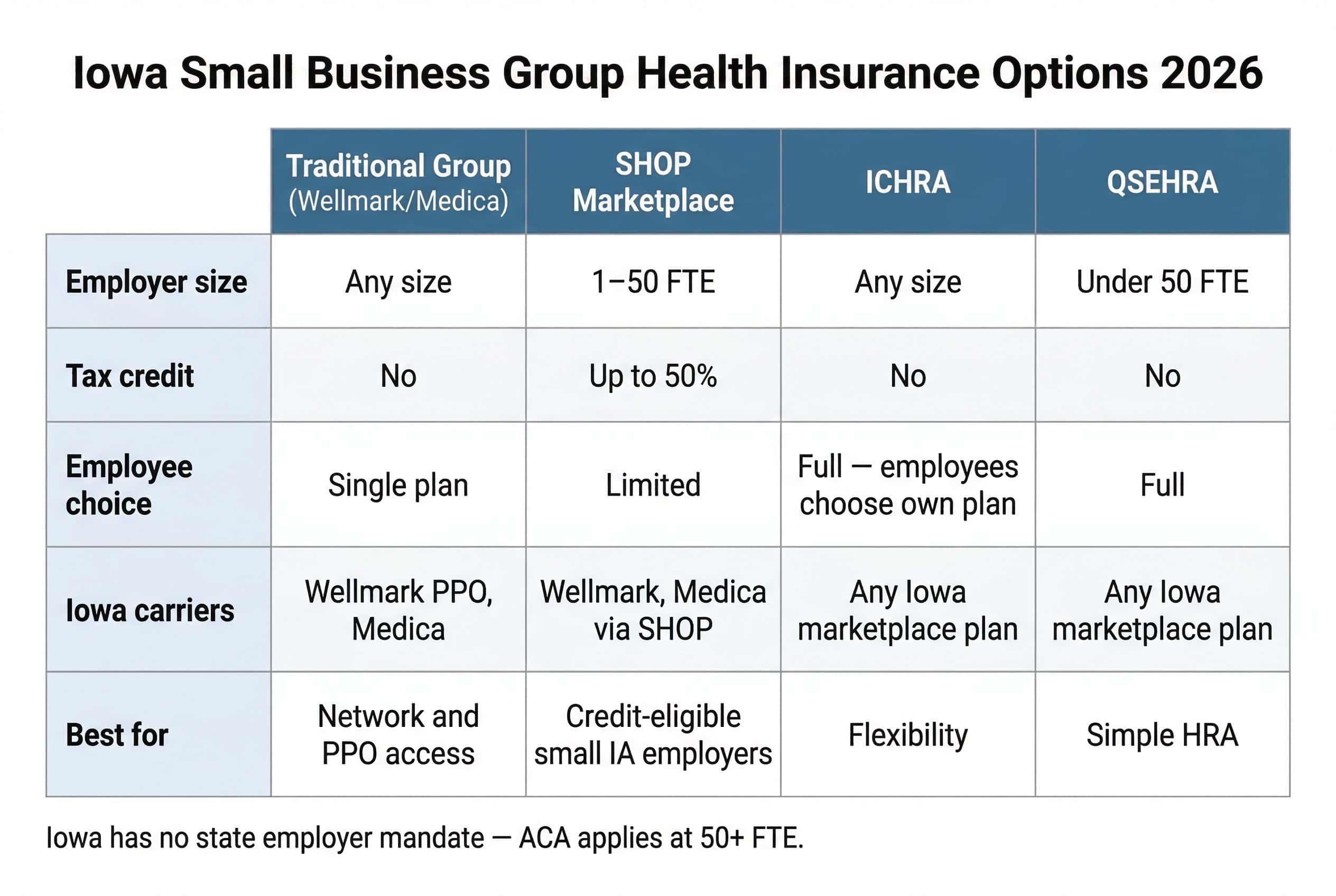

Iowa employers in 2026 can choose from four group coverage approaches: traditional plans through Wellmark, Medica, or Principal; the SHOP marketplace for employers under 50 FTE seeking federal tax credits; ICHRA allowing employees to choose their own individual plan; and QSEHRA for businesses with fewer than 50 FTE. Iowa has no state employer mandate — the ACA employer mandate applies only at 50 or more FTE.

| Option | Best For | Employer Size | Tax Benefit |

|---|---|---|---|

| Traditional Group Plan | Businesses wanting one plan with statewide PPO access | Any size | Premiums deductible as business expense |

| SHOP Marketplace | Small Iowa employers seeking the federal Small Business Health Care Tax Credit | 1–50 FTE | Up to 50% of premiums as tax credit |

| ICHRA | Employers wanting flexibility — employees choose own Iowa marketplace plans | Any size | Tax-free reimbursements to employees |

| QSEHRA | Very small Iowa businesses wanting simple HRA with IRS contribution limits | Under 50 FTE | Tax-free reimbursements up to IRS cap |

SHOP Marketplace and Small Business Tax Credits in Iowa

Iowa employers with fewer than 25 FTE paying average wages below approximately $65,000 qualify for the Small Business Health Care Tax Credit — up to 50% of premiums — but only when coverage is purchased through HealthCare.gov SHOP. The full credit applies below 10 FTE with average wages at or below $34,100. Iowa carriers available through SHOP include Wellmark and Medica.

SHOP Tax Credit Eligibility for Iowa Employers

To qualify for the full 50% Small Business Health Care Tax Credit, an Iowa employer must have fewer than 10 full-time equivalent employees, pay average annual wages at or below $34,100 (the 2026 inflation-adjusted phase-out threshold per IRS Rev. Proc. 2025-32), and purchase coverage through HealthCare.gov SHOP. The credit phases out as employee count approaches 25 FTE and as average wages approach approximately $65,000, where it disappears entirely. Iowa employers above these thresholds still have access to SHOP enrollment but without the tax credit. Per the IRS Small Business Health Care Tax Credit guide, employers must offer SHOP coverage to all full-time employees to qualify for the credit.

Real Scenario: Iowa Grain Cooperative in Harlan — 12 Employees

A small grain cooperative in Harlan, Shelby County has 12 full-time employees with average wages of $38,000 annually. At 12 FTE and $38,000 average wages, this employer is in the phase-out range on both dimensions — employee count exceeds 10 FTE and average wages exceed the 2026 phase-out threshold of $34,100 — so the tax credit would be partial rather than the full 50%. Wellmark and Medica plans are available through HealthCare.gov SHOP in Shelby County. A licensed broker can calculate the exact credit amount and compare SHOP plan costs against direct Wellmark group plans — when the credit is small, a direct group plan may offer more carrier and plan-design flexibility.

Compare Iowa Small Business Health Insurance Quotes for 2026

Compare Wellmark group PPO plans, SHOP marketplace tax credits up to 50% for qualifying Iowa employers, and ICHRA and QSEHRA alternatives — a licensed Iowa broker can calculate your exact tax credit eligibility and compare all options at no cost.

Wellmark Group PPO — Iowa’s Dominant Small Business Carrier

Wellmark Health Plan of Iowa is the primary group health insurance carrier for Iowa small businesses. Wellmark’s group PPO plans give Iowa employees access to any Wellmark network provider without a referral, plus the BlueCross BlueShield national network for out-of-state care. Wellmark group plans are available for all Iowa counties — not just through SHOP — and can be customized with different deductible and copay structures.

Wellmark’s dominance in Iowa’s small group market reflects its statewide network and BCBS affiliation, which matters for Iowa businesses whose employees work across multiple locations or travel. According to the Iowa Insurance Division’s rate filing data, Wellmark filed a 12.6% rate adjustment for 2026 — relevant context when comparing small business health insurance Iowa group plan renewal costs against SHOP or ICHRA alternatives. Iowa agricultural businesses benefit especially from Wellmark’s rural provider network: the carrier covers critical access hospitals in remote Iowa counties that smaller carriers may not include. For small business health insurance Iowa employers prioritizing cost, Medica is the second major statewide group carrier, with competitive HMO-style plans for employers who prioritize cost over network breadth. For individual employee coverage options, see the Iowa affordable health insurance guide.

ICHRA and QSEHRA for Iowa Small Businesses

Iowa employers that find traditional group plans cost-prohibitive can use ICHRA or QSEHRA to reimburse employees for individual marketplace plans. ICHRA has no employer size limit and no contribution cap. QSEHRA is for employers with fewer than 50 FTE, with 2026 IRS limits of $6,450 per year for employee-only or $13,100 per year for family coverage. Both arrangements are tax-free for employer and employee.

ICHRA — Individual Coverage HRA

No employer size limit. Employer sets any monthly reimbursement amount. Iowa employees purchase their own Wellmark, Oscar, or Medica individual plan on or off HealthCare.gov and submit premiums for tax-free reimbursement.

ICHRA reimbursements reduce marketplace subsidy eligibility dollar-for-dollar — employees currently receiving ACA premium tax credits should compare ICHRA offers carefully with a broker. Best for Iowa businesses with varied workforces or employees spread across multiple counties with different carrier availability.

QSEHRA — Qualified Small Employer HRA

For Iowa employers with fewer than 50 full-time employees. 2026 IRS limits per Rev. Proc. 2025-32: $6,450 per year for employee-only coverage ($537.50/month) or $13,100 per year for family coverage ($1,091.66/month).

Employees purchase individual plans and submit receipts. QSEHRA allowances reduce ACA marketplace subsidy eligibility dollar-for-dollar. Cannot be offered alongside a traditional group plan. Best for very small Iowa businesses — farm operations, rural retail — that want to offer a health benefit without group plan complexity.

Coverage for Iowa’s Agricultural Small Businesses

Iowa’s agricultural economy creates a distinct group coverage market. Approximately 87,000 farms, grain cooperatives, livestock operations, and agribusinesses employ full-time hired labor across the state’s 99 counties. These employers generally fall below the ACA’s 50 FTE threshold, making coverage voluntary but strategically important for retaining skilled farm workers. Wellmark’s statewide rural network is the primary group plan choice for agricultural Iowa employers.

Iowa farm operations seeking small business health insurance Iowa coverage face unique challenges: seasonal employment fluctuations, workers in remote rural counties with limited carrier options, and income volatility that affects benefit affordability year to year. ICHRA and QSEHRA arrangements work well for agricultural employers because contribution amounts can flex with farm income — a fixed reimbursement ceiling helps manage costs in low-commodity-price years. Iowa Farm Bureau members can explore Farm Bureau-sponsored benefit offerings alongside or instead of ACA group plans, though Farm Bureau plans are not ACA-compliant and do not satisfy employer mandate requirements for businesses with 50 or more FTE. For self-employed farm operators seeking small business health insurance in Iowa without employees, see the Iowa individual health insurance guide for solo coverage options.

Iowa ACA Employer Mandate at 50+ FTE

Iowa agricultural businesses that grow beyond 50 full-time equivalent employees become subject to the ACA’s employer shared responsibility provisions. At 50+ FTE, employers must offer affordable, minimum-value coverage to full-time employees or face a potential excise tax. Iowa businesses approaching the 50 FTE threshold should consult a licensed broker to evaluate group plan options before mandate obligations take effect. For bridge coverage during employment transitions, see the Iowa short-term health insurance guide.

Frequently Asked Questions — Small Business Health Insurance in Iowa

Common questions about small business health insurance in Iowa for 2026 — including employer mandate thresholds, SHOP tax credit eligibility, group carrier options, ICHRA structure, and coverage for Iowa farm operations with full-time hired labor.

Is health insurance required for small businesses in Iowa?

Iowa has no state employer health insurance mandate for small business health insurance Iowa coverage. The only applicable requirement is the federal ACA employer shared responsibility provision, which applies to businesses with 50 or more full-time equivalent employees. For small business health insurance in Iowa, businesses with fewer than 50 FTE have no legal obligation to offer health coverage. However, offering coverage is an important tool for employee recruitment and retention, particularly in Iowa’s competitive agricultural and rural labor markets where skilled farm operators and tradespeople have multiple employer options.

What group health insurance carriers serve Iowa small businesses?

The primary small business health insurance Iowa group carriers are Wellmark Health Plan of Iowa (BCBS affiliate, statewide PPO and HMO, dominant in Iowa’s group market), Medica (statewide, HMO-style group plans), and Principal Financial Group (Des Moines-based, strong Iowa small group presence). Iowa Total Care, Oscar, and UnitedHealthcare primarily serve the individual marketplace rather than the small group market. For Iowa businesses that want PPO plans with statewide rural network coverage — essential for agricultural employers across Iowa’s 99 counties — Wellmark is the standard choice in 2026.

How does the Small Business Health Care Tax Credit work in Iowa?

The Small Business Health Care Tax Credit covers up to 50% of premiums paid by eligible Iowa employers — but only when coverage is purchased through HealthCare.gov SHOP. To qualify for the full credit, an Iowa employer must have fewer than 10 full-time equivalent employees, pay average annual wages at or below $34,100 (the 2026 IRS phase-out threshold per Rev. Proc. 2025-32), and pay at least 50% of employee-only premium costs. The credit phases out as employee count approaches 25 FTE and as average wages approach approximately $65,000. For a grain cooperative or rural Iowa retail business with 12 employees earning $38,000 average wages, the credit would be partial — a licensed broker can calculate the exact amount and compare SHOP costs against direct Wellmark group plans.

Can Iowa farm operations offer health insurance to hired workers?

Yes. Iowa farm operations seeking small business health insurance Iowa coverage can offer group health insurance, ICHRA, or QSEHRA benefits. Most Iowa farms fall well below the ACA’s 50 FTE employer mandate threshold, so offering coverage is voluntary but strategically valuable for retaining skilled farm labor. Wellmark’s group PPO plans are the most common choice for Iowa agricultural employers — the statewide rural network covers critical access hospitals in remote Iowa counties. ICHRA arrangements work well for farm operations with variable employment and income, as the employer can set monthly reimbursement amounts that flex with the farm’s financial position.

What is ICHRA and how does it work for Iowa small businesses?

An Individual Coverage HRA (ICHRA) is an employer-funded arrangement where Iowa small businesses reimburse employees for individual health insurance premiums — employees choose their own Wellmark, Oscar, Medica, or other Iowa marketplace plan and submit premiums for tax-free reimbursement. ICHRA has no employer size limit and no contribution cap. The employer sets a monthly reimbursement amount — for example, $400/month for employee-only or $800/month for family coverage. Iowa employees receiving ICHRA reimbursements above certain thresholds lose access to marketplace premium tax credits, so employees who currently receive subsidies should compare ICHRA offers carefully with a licensed broker before enrolling.

Iowa Health Insurance Resources

Complete 2026 guide — all 6 carriers, IA Health Link, Hawk-I, and county coverage.

Iowa Health Insurance MarketplaceHealthCare.gov enrollment, 2026 subsidy changes, and Iowa carrier county availability.

Affordable Health Insurance IowaIA Health Link, Hawk-I, and premium tables for Iowa residents and self-employed.

Individual Health Insurance IowaIowa Farm Bureau plans, off-exchange Wellmark PPO, and self-employed coverage options.

Short-Term Health Insurance IowaIowa allows STLDI with initial terms up to 364 days, renewable to 3 years — bridge coverage for seasonal agricultural workers.

PPO Health Insurance PlansHow PPO networks work, Wellmark BlueCard access, and PPO vs. HMO for Iowa employers.

Compare Iowa Small Business Health Insurance Plans for 2026

Wellmark group PPO plans for all 99 Iowa counties, SHOP tax credits for under-25-FTE employers, and ICHRA or QSEHRA for farm operations and small businesses — compare all 2026 Iowa options with a licensed broker at no cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Iowa businesses. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.