Individual Health Insurance Iowa 2026: Self-Employed, Farms, and Off-Exchange Options

Individual health insurance in Iowa for 2026 serves residents outside employer plans, below Medicare age, and not enrolled in IA Health Link Medicaid. Iowa’s individual market is dominated by the self-employed, agricultural workers and farm operators, college students at Iowa State University and the University of Iowa, and residents between jobs or aging off parents’ plans. This guide covers every individual health insurance Iowa pathway for 2026 — including the Iowa Farm Bureau Health Plan, a non-ACA alternative available only to Iowa Farm Bureau members.

What brings you here today?

Find my coverage pathway

IA Health Link, subsidized marketplace, or off-exchange by income

See pathways →Self-employed or farm operator

Farm Bureau plans, premium deductions, IA Health Link eligibility

See options →I missed open enrollment

Special enrollment periods, off-exchange Wellmark, IA Health Link

Check options →Who Needs Individual Health Insurance in Iowa?

Individual health insurance in Iowa for 2026 covers residents outside employer plans and below Medicare age. Iowa’s largest individual market segments are self-employed residents including farm operators, freelancers, part-time workers without employer benefits, college students at Iowa State University and the University of Iowa, dependents aging off parents’ plans at 26, and residents between jobs. Iowa’s approximately 87,000 farms make self-employed agricultural workers a distinct individual coverage group.

Iowa has no state employer mandate — the federal ACA employer mandate applies only to businesses with 50 or more full-time equivalent employees. Most individual health insurance Iowa purchases come from residents at these smaller employers. Iowa businesses with fewer than 50 FTE have no legal obligation to offer coverage, leaving a substantial share of employees at Iowa’s many small agricultural businesses to find individual health insurance Iowa options independently. Residents who lose employer coverage, age off a parent’s plan, or see income changes that affect Medicaid eligibility all enter the individual market through HealthCare.gov or off-exchange options.

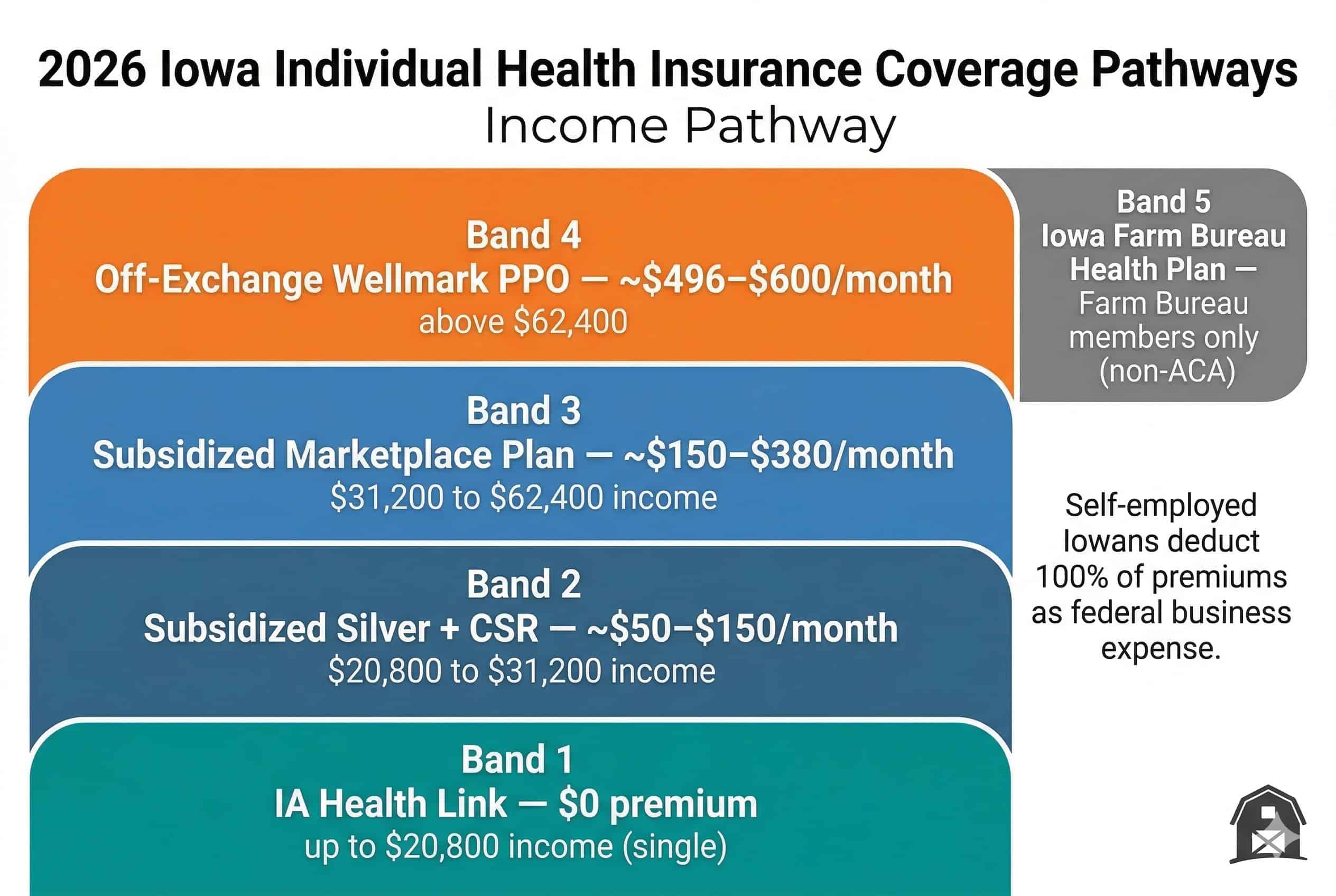

Iowa Individual Market Coverage Pathways

Iowa’s individual health insurance market has four main coverage pathways based on income. IA Health Link Medicaid covers adults earning up to $22,020 (single) at $0 premium. Subsidized marketplace plans through HealthCare.gov serve incomes from 138% to 400% of FPL. Full-price marketplace and off-exchange Wellmark PPO plans apply above $62,600. Iowa Farm Bureau members have an additional non-ACA option available year-round.

| Income Level (Single, 2026) | Coverage Pathway | Est. Monthly Cost | Enrollment |

|---|---|---|---|

| Up to $22,020 (138% FPL) | IA Health Link (Medicaid) | $0 | Year-round |

| $22,020–$31,300 (138–200% FPL) | Subsidized Silver + CSR | ~$50–$150/mo after credits | Nov 1–Jan 15 or SEP |

| $31,300–$62,600 (200–400% FPL) | Subsidized marketplace plan | ~$150–$380/mo after credits | Nov 1–Jan 15 or SEP |

| Above $62,600 (400%+ FPL) | Full-price marketplace or off-exchange Wellmark PPO | ~$496–$600/mo | Marketplace: Nov 1–Jan 15 / Wellmark: year-round |

| Iowa Farm Bureau members (any income) | Iowa Farm Bureau Health Plan (non-ACA) | Varies by plan | During Farm Bureau enrollment period |

Self-Employed and Farm Operator Coverage in Iowa

Self-employed Iowans — including farm operators, independent contractors, and freelancers — can deduct 100% of health insurance premiums as a federal above-the-line business deduction using IRS Form 7206. Iowa has approximately 87,000 farms, making agricultural self-employment one of the largest individual insurance markets in the state. Self-employed Iowans compare IA Health Link eligibility, subsidized marketplace plans, and off-exchange Wellmark PPO options based on net farm income.

Farm income volatility is a key factor in individual health insurance Iowa coverage decisions for agricultural operators. A year with strong commodity prices may push net farm income above the subsidy threshold; a poor crop year may push income below the IA Health Link limit. Iowa farm operators should check IA Health Link eligibility annually — if net farm income drops below $22,020 (single) or approximately $29,200 (two-person household), IA Health Link is available at $0 with year-round enrollment and no waiting period.

Iowa Farm Bureau Health Plan

Iowa Farm Bureau members have access to a non-ACA health benefit plan through the Iowa Farm Bureau — a nonprofit agricultural organization. Farm Bureau Health Plans are not ACA-compliant, meaning they do not cover all essential health benefits and may exclude pre-existing conditions. However, they may offer lower premiums for healthy farm operators who are Iowa Farm Bureau members. These plans are governed by Iowa state law rather than ACA federal rules and are not available on HealthCare.gov. Iowa Farm Bureau members should compare Farm Bureau plan benefits carefully against marketplace alternatives, particularly if they have pre-existing conditions or need comprehensive prescription drug coverage.

Real Scenario: Iowa Farm Operator in Ames, Age 47

An Iowa farm operator near Ames, Story County earns $58,000 net farm income in 2026 — above the $22,020 IA Health Link threshold but below the $62,600 subsidy cliff. At approximately 370% FPL for a single adult, this operator qualifies for a partial premium tax credit on HealthCare.gov for individual health insurance Iowa marketplace plans. A Wellmark Silver plan at ~$520/month before subsidies drops to approximately $310/month after credits. In a low-income year where net farm income falls below $22,020, the same operator qualifies for IA Health Link at $0. Checking eligibility each year at HealthCare.gov or Iowa HHS prevents coverage gaps during income swings.

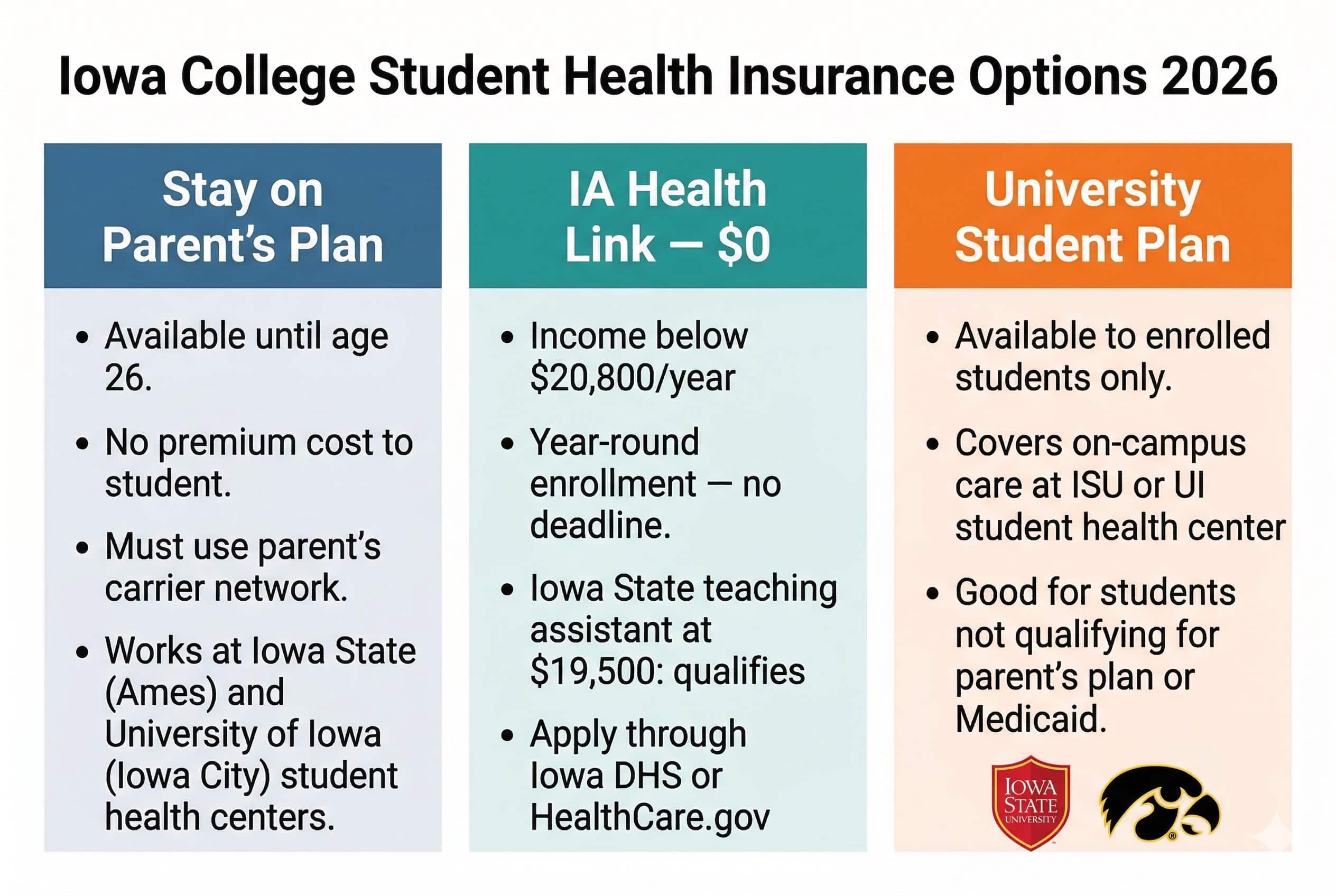

Student Health Insurance at Iowa State University and University of Iowa

Students at Iowa State University (Ames) and the University of Iowa (Iowa City) have three coverage options: staying on a parent’s plan until age 26, enrolling in a university-sponsored student plan, or purchasing an individual marketplace plan through HealthCare.gov. Students earning below $22,020 annually may qualify for IA Health Link at $0. Both universities offer student health plans through their student health centers.

Iowa State University in Ames and the University of Iowa in Iowa City both operate student health centers with affiliated student health insurance plans covering on-campus care and outside referrals. Students considering individual health insurance Iowa marketplace plans who are claimed as dependents on their parents’ federal tax return may still qualify for IA Health Link independently based on their own income. A student earning below $22,020 through part-time work or a teaching assistantship qualifies for IA Health Link regardless of their parents’ income, as Medicaid eligibility is based on the individual’s own household income.

Real Scenario: Iowa State University Graduate Student, Ames, Age 24

An Iowa State University graduate student in Ames earns $19,500 annually through a teaching assistantship — below the $22,020 IA Health Link threshold. This student qualifies for IA Health Link at $0 premium. Iowa State’s student health insurance plan is an alternative, but IA Health Link provides comparable coverage at no premium cost. The student should apply through HealthCare.gov or directly through Iowa HHS — enrollment is year-round with no deadline. IA Health Link through Iowa’s managed care contractors covers Ames-area providers including Mary Greeley Medical Center and Iowa State student health center referrals.

Qualifying Life Events and Special Enrollment for Iowa Residents

Iowa residents buying individual coverage outside open enrollment must have a qualifying life event (QLE) that triggers a Special Enrollment Period. Common Iowa QLEs include losing employer coverage, aging off a parent’s plan at 26, moving to Iowa from another state, marriage, divorce, birth of a child, and loss of IA Health Link eligibility. Each QLE opens a 60-day enrollment window on HealthCare.gov. IA Health Link enrolls year-round with no QLE required.

Loss of Employer Coverage

Losing job-based coverage — including leaving a job voluntarily — is the most common QLE for Iowa individual market enrollees. The 60-day SEP window begins on the date coverage ends, not the date of the job loss. Iowa residents should not wait until coverage lapses to begin the HealthCare.gov application — starting early prevents coverage gaps.

Aging Off Parent’s Plan at 26

Dependents lose coverage on or around their 26th birthday depending on the plan. This triggers a 60-day SEP. Iowa residents aging off a parent’s plan should compare IA Health Link (if income below $22,020), subsidized marketplace plans through HealthCare.gov, and university student plans if still enrolled at Iowa State or University of Iowa.

Moving to Iowa

Relocating to Iowa from another state triggers a SEP if the resident had prior coverage. New Iowa residents can enroll in Wellmark, Oscar, Medica, or other Iowa marketplace carriers through HealthCare.gov. County matters — Avera serves only 7 northwest Iowa counties; Oscar is not available in all 99 counties. Check carrier availability for your specific Iowa county before selecting a plan.

Loss of IA Health Link Eligibility

Iowa residents whose income rises above the IA Health Link threshold ($22,020 single) lose Medicaid eligibility. This triggers a SEP to enroll in a marketplace plan within 60 days. Iowa HHS notifies residents when IA Health Link eligibility ends. Apply on HealthCare.gov immediately — subsidy eligibility begins where IA Health Link ends at 138% FPL. For 2026 premium tables by income, see the Iowa affordable health insurance guide.

Iowa residents seeking individual health insurance Iowa coverage who miss open enrollment and have no qualifying life event have two options: wait for the next open enrollment period (November 1) or purchase an off-exchange Wellmark plan directly. Off-exchange Wellmark PPO plans are available year-round with no enrollment period requirement and no QLE needed. They do not qualify for premium tax credits but offer year-round access and PPO flexibility for residents above the subsidy threshold. See the Iowa PPO and carrier comparison guide for Wellmark’s off-exchange individual health insurance Iowa plan details.

Get Individual Health Insurance Quotes in Iowa for 2026

IA Health Link at $0 up to $22,020, Oscar Silver from ~$496/month, Wellmark PPO off-exchange year-round — compare all Iowa individual options by county and income.

Frequently Asked Questions — Individual Health Insurance in Iowa

Common questions about individual health insurance in Iowa for 2026 — including who needs individual coverage, the self-employed premium deduction, Iowa Farm Bureau plans, student eligibility for IA Health Link, and special enrollment rules for Iowa residents.

Who needs to buy individual health insurance in Iowa?

Individual health insurance in Iowa is needed by residents not covered through an employer plan, not yet on Medicare, and not enrolled in IA Health Link Medicaid. Iowa’s largest individual market groups include self-employed residents, farm operators (Iowa has approximately 87,000 farms), part-time workers at small businesses with fewer than 50 employees, college students at Iowa State University and the University of Iowa who are no longer on their parents’ plans, and residents between jobs. Iowa has no state employer mandate — the federal ACA employer requirement applies only to businesses with 50 or more full-time equivalent employees.

Can self-employed Iowans deduct health insurance premiums?

Yes. Self-employed Iowa residents — sole proprietors, farm operators, freelancers, and independent contractors — can deduct 100% of health insurance premiums paid for themselves, their spouse, and dependents as a federal above-the-line deduction using IRS Form 7206. This deduction reduces adjusted gross income and does not require itemizing. It applies to premiums paid for marketplace plans through HealthCare.gov, off-exchange Wellmark plans, or Iowa Farm Bureau Health Plans. The deduction cannot exceed the net profit from self-employment. Iowa farm operators should calculate the deduction against net Schedule F income. A tax advisor familiar with Iowa agricultural income can optimize this deduction for farm households with volatile annual income.

What is the Iowa Farm Bureau Health Plan?

The Iowa Farm Bureau Health Plan is a health benefit plan offered by the Iowa Farm Bureau — a nonprofit agricultural organization — to its members. It is not an ACA-compliant plan, meaning it does not cover all ACA essential health benefits and may have different rules regarding pre-existing conditions. The plan is available only to Iowa Farm Bureau members and is governed by Iowa state law rather than federal ACA marketplace rules. It is not available on HealthCare.gov and does not qualify for premium tax credits. Iowa Farm Bureau members should compare the plan’s benefits and exclusions carefully against ACA marketplace alternatives, particularly if they have pre-existing conditions or need prescription drug coverage.

Do Iowa college students qualify for IA Health Link?

Iowa college students may qualify for IA Health Link (Medicaid) based on their own individual income — not their parents’ income — if they file their own tax return and are not claimed as a dependent. A student earning below $22,020 annually through part-time work, stipends, or teaching assistantships qualifies for IA Health Link at $0 premium with year-round enrollment. Students at Iowa State University in Ames and the University of Iowa in Iowa City who qualify for IA Health Link can use it alongside their university student health center — IA Health Link covers outside referrals beyond on-campus care. Students still claimed as dependents on their parents’ returns should check whether they qualify under their parents’ household income for Hawk-I or a family marketplace plan.

Can I buy individual health insurance in Iowa outside of open enrollment?

Iowa residents can enroll in individual health insurance Iowa marketplace plans outside open enrollment only through a qualifying life event (QLE) that triggers a Special Enrollment Period. Common QLEs include losing employer coverage, aging off a parent’s plan at 26, moving to Iowa from another state, getting married or divorced, having a child, or losing IA Health Link eligibility. Each QLE opens a 60-day enrollment window on HealthCare.gov. IA Health Link and Hawk-I enroll year-round with no QLE required. Off-exchange Wellmark PPO plans can also be purchased directly from Wellmark at any time without a QLE — they do not qualify for premium tax credits but offer year-round access and PPO flexibility.

Iowa Health Insurance Resources

Complete 2026 guide — all 6 carriers, IA Health Link, Hawk-I, and county coverage.

Iowa Health Insurance MarketplaceHealthCare.gov enrollment, 2026 subsidy changes, and Iowa carrier county availability.

Best Health Insurance in IowaCarrier comparison, PPO guide, and Wellmark off-exchange options for Iowa residents.

Small Business Health Insurance IowaGroup plans, SHOP tax credits, and ICHRA for Iowa’s small employers and farms.

Short-Term Health Insurance IowaIowa allows STLDI initial terms up to 364 days, renewable to 3 years — bridge coverage between employer plans.

PPO Health Insurance PlansHow PPO networks work, Wellmark BlueCard access, and PPO vs. HMO for Iowa residents.

Compare Individual Health Insurance Plans in Iowa for 2026

Iowa Farm Bureau plans for members, IA Health Link at $0 up to $22,020, Oscar Silver from ~$496/month, and Wellmark PPO off-exchange — find the right individual plan for your Iowa county and situation.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Iowa residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.