Affordable Health Insurance in Alabama 2026: Subsidies, Costs and Strategies

This guide covers what affordable health insurance in Alabama costs in 2026 and what financial help is available to Alabama residents. The average subsidized Alabama enrollee pays $121 per month — up sharply from $44 in 2025 after enhanced subsidies expired — but most Alabamians below 250% FPL can still find genuinely affordable coverage through the right combination of premium tax credits and cost-sharing reductions on Silver plans.

What are you trying to figure out?

What Changed for Affordable Coverage in 2026

Premiums for affordable health insurance in Alabama rose 19% to 25% for 2026 and the average after-subsidy premium tripled from $44 to $121 per month as enhanced federal subsidies expired. All four Alabama carriers increased base rates, and the expiration of the Inflation Reduction Act’s enhanced premium tax credits removed meaningful financial help from enrollees earning 300% to 400% FPL. Affordable health insurance in Alabama still exists for most residents through the right combination of plan tier and income documentation.

Average after-subsidy premium — 2025

With enhanced ARP/IRA subsidies in place — available 2021 through 2025 for Alabama marketplace enrollees.

Average after-subsidy premium — 2026

After enhanced subsidies expired December 31, 2025. Original ACA APTC formula applies for 2026 — lower credits at 300%–400% FPL.

Enrollees who still qualify for subsidies

Per CMS 2025 enrollment data. Most Alabama marketplace enrollees still receive federal premium tax credits that meaningfully reduce their monthly cost.

Rate increase range — 2026

Blue Cross +19.3%, UnitedHealthcare +20%, Oscar new entrant, Ambetter +25%. All carriers increased for 2026.

How Subsidies Work for Alabama Residents

Federal premium tax credits reduce your monthly marketplace premium based on household income relative to the Federal Poverty Level. The lower your income within the eligible range, the larger your credit. For Alabama residents, the credit is applied automatically through HealthCare.gov enrollment — no separate application. Alabama has no state-funded subsidies beyond the federal APTC, and no Medicaid expansion to catch residents below the subsidy floor.

| Income (Single Adult) | FPL % | Max Premium % of Income | Estimated Monthly APTC |

|---|---|---|---|

| $15,060 – $22,590 | 100%–150% | 2.0% – 4.0% | $375 – $480/mo credit |

| $22,590 – $30,120 | 150%–200% | 4.0% – 6.6% | $300 – $375/mo credit |

| $30,120 – $39,125 | 200%–250% | 6.6% – 8.44% | $200 – $300/mo credit |

| $39,125 – $46,950 | 250%–300% | 8.44% – 9.96% | $100 – $200/mo credit |

| $46,950 – $62,400 | 300%–400% | 9.96% | $50 – $130/mo credit |

| Above $62,400 | 400%+ | No cap | No subsidy — full sticker price |

Source: HealthCare.gov premium tax credit tables and 2026 Federal Poverty Level guidelines.

The subsidy cliff is back for 2026: Enhanced subsidies had removed the hard income cutoff at 400% FPL — any income level could receive some credit. That ended December 31, 2025. For 2026, Alabama residents earning above $62,400 (single) or $129,600 (family of four) receive zero federal premium assistance. If your income is near this threshold, underestimating projected annual income in your enrollment application by $1 could cost you the entire subsidy at tax time — IRS Form 8962 reconciles actual vs estimated income and requires repayment of excess credits.

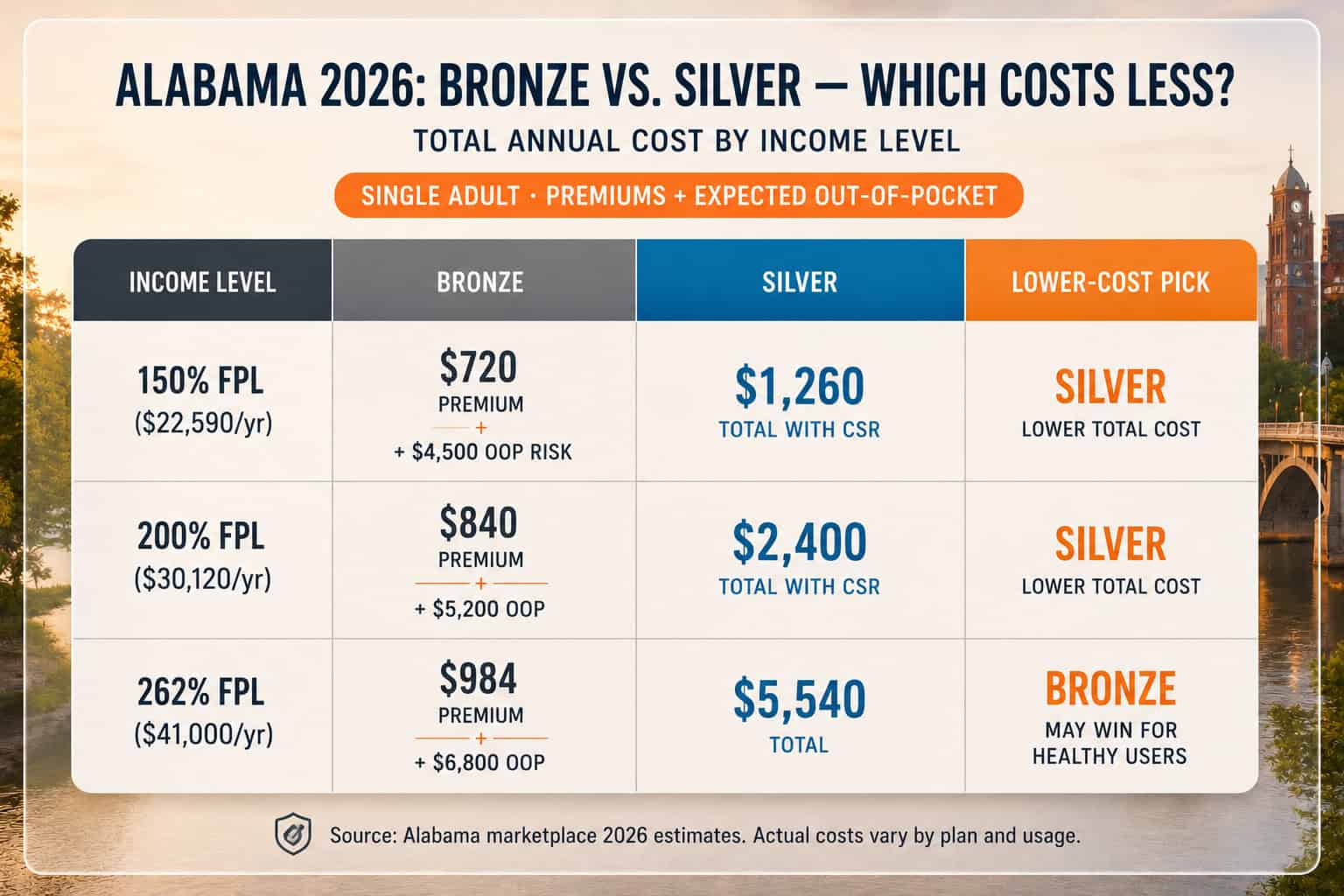

The Silver CSR Advantage: Why Silver Beats Bronze for Most Alabama Enrollees

Cost-sharing reductions automatically lower the deductible, copay, and out-of-pocket maximum on Silver plans for Alabama enrollees earning below 250% FPL. Bronze costs less monthly but has deductibles up to $9,100 — one ER visit or outpatient procedure can wipe out a full year of premium savings. For most Alabamians below 250% FPL, Silver with CSR delivers the best combination of low monthly premium and manageable out-of-pocket risk.

| Income Level | Silver Deductible with CSR | Silver OOP Max with CSR | Bronze Deductible (no CSR) |

|---|---|---|---|

| 100%–150% FPL ($15,060–$22,590) | $100 – $300 | $1,300 – $2,700 | $6,000 – $9,100 |

| 150%–200% FPL ($22,590–$30,120) | $300 – $700 | $2,700 – $4,250 | $6,000 – $9,100 |

| 200%–250% FPL ($30,120–$39,125) | $700 – $1,500 | $4,250 – $6,000 | $6,000 – $9,100 |

| Above 250% FPL ($39,125+) | $3,000 – $5,500 (no CSR) | $8,000 – $9,100 | $6,000 – $9,100 |

Source: ACA cost-sharing reduction (CSR) standards and 2026 Alabama Silver plan benchmarks.

Scenario: Marcus, Birmingham freelancer, age 35, $41,000 income

Marcus earns $41,000 — 262% of the 2026 FPL, just above the CSR threshold of $39,125. He is on the marketplace as a self-employed graphic designer in Birmingham’s Avondale neighborhood. His APTC reduces the Blue Cross Silver sticker price from $398/month to approximately $170/month. Because he is above 250% FPL, he does not receive CSR — his Silver deductible is the standard $3,500. He considers Bronze at $82/month after APTC, but the $7,500 Bronze deductible means a single urgent care visit and follow-up could cost him $1,200 out of pocket before insurance pays anything. He chooses Silver: $1,044 more per year in premiums, but protected against a mid-year health event wiping out his savings.

When Marketplace Coverage Beats Alabama Employer Plans

Employer-sponsored coverage is not always the most affordable option for Alabama workers. If your share of the employer plan premium exceeds 9.02% of your household income — the 2026 ACA affordability threshold — and your household income qualifies for marketplace subsidies, you may pay significantly less on the Alabama marketplace. This most commonly applies to workers at small Alabama businesses where employer contributions are low.

Scenario: Patricia, Huntsville, age 58, $52,000 salary

Patricia works for a small Huntsville engineering firm. Her employer offers group coverage, but her share of the monthly premium is $485 — $5,820 per year, or about 11.2% of her salary. This is above the 9.02% ACA affordability threshold, which means she may be able to access marketplace subsidies even with employer coverage available. On the marketplace, a Blue Cross Silver plan after APTC costs her approximately $210 per month at her income level. She saves $275 per month — $3,300 per year — by switching to the marketplace. A licensed agent ran this comparison for Patricia before she made the switch and confirmed she qualifies for marketplace APTC because her employer plan fails the affordability test.

The affordability test: Your employer coverage is “unaffordable” under ACA rules if your share of the employee-only premium for the lowest-cost employer plan exceeds 9.02% of your household income in 2026. If it does, you may qualify for marketplace APTC even while employed. This calculation only considers the employee-only premium — not the cost to add a spouse or children — which means a family could be in a hybrid situation where the employee uses employer coverage and dependents use the marketplace.

See what affordable coverage actually costs you in Alabama

A licensed agent runs your APTC calculation, compares all four carriers, and shows you the real monthly cost — at no charge.

Strategies to Keep Alabama Coverage Affordable

The most effective strategies for keeping affordable health insurance in Alabama within reach are income management, correct plan tier selection, and HSA pairing for those above the CSR threshold. Accurate income projection on your HealthCare.gov application is critical — underestimating income lowers your monthly premium but increases year-end repayment risk on IRS Form 8962. Overestimating costs you money every month in foregone APTC.

For self-employed Alabamians, the Schedule 1 premium deduction reduces adjusted gross income — which directly increases APTC eligibility. A freelancer earning $45,000 gross who deducts $3,600 in premiums on Schedule 1 has an effective income of $41,400 for APTC purposes, pushing them into a higher subsidy bracket. See the individual health insurance Alabama guide for the full self-employed tax strategy. For Alabama small business owners considering group coverage, the Alabama small business health insurance guide covers the 2026 small group rate changes and ICHRA options.

For Alabamians above 250% FPL who choose Bronze, pairing a high-deductible Bronze plan with a Health Savings Account (HSA) adds pre-tax savings: the 2026 HSA limit is $4,300 for self-only coverage. The combination of lower Bronze premium plus HSA tax savings can make Bronze genuinely cheaper than Silver for healthy higher-income Alabamians who rarely need care. The IRS Publication 969 covers HSA eligibility rules.

Frequently Asked Questions

How much does health insurance cost in Alabama after subsidies in 2026?

The average subsidized Alabama marketplace enrollee pays approximately $121 per month for 2026 coverage — up from $44 per month in 2025 after enhanced federal subsidies expired. Most subsidized enrollees paying under 200% FPL (about $30,120 for a single adult) pay under $100 per month after federal premium tax credits. Specific costs depend on income, plan tier, and which of the four Alabama carriers you choose.

What income qualifies for affordable health insurance in Alabama?

Federal premium tax credits are available for Alabama residents with household income between 100% and 400% FPL — approximately $15,060 to $62,400 for a single adult in 2026. Residents below $15,060 fall into Alabama’s Medicaid coverage gap since Alabama has not expanded Medicaid. There are no state-funded subsidies in Alabama beyond the federal tax credit.

Why is Silver the most affordable plan tier in Alabama for most people?

Silver plans are the only tier eligible for cost-sharing reductions (CSR), which lower your deductible and out-of-pocket maximum if your income is below 250% FPL (about $37,650 single). A Silver plan with CSR can have a deductible as low as $300 and an out-of-pocket maximum around $2,700 — comparable to employer coverage — while the after-APTC premium is often under $150 per month. Bronze costs less monthly but has deductibles up to $9,100.

Can marketplace coverage be cheaper than employer coverage in Alabama?

Yes, in some situations. If your employer’s plan costs you more than 9.02% of your household income (the ACA affordability threshold for 2026), and the marketplace plan with subsidies is cheaper, the marketplace may be better. This is most common for workers at small Alabama businesses where the employer contribution is low and the employee’s share of the group premium is high.

What happened to Alabama health insurance costs in 2026?

Alabama individual market premiums rose 19% to 25% in 2026 as all four carriers increased rates after enhanced federal subsidies expired at the end of 2025. The average after-subsidy premium nearly tripled from $44 to $121 per month. Alabamians who previously received large enhanced APTC amounts saw the biggest cost increases, particularly those earning 300% to 400% FPL.

How do cost-sharing reductions work in Alabama?

Cost-sharing reductions (CSR) are automatic discounts on deductibles, copays, and out-of-pocket maximums for Silver plan enrollees with income below 250% FPL. They are applied automatically when you enroll in a Silver plan on the Alabama marketplace — no separate application is needed. CSR is not available on Bronze, Gold, or Platinum plans. The lower your income relative to 250% FPL, the stronger the CSR benefit.

Related Alabama Health Insurance Resources

Complete 2026 overview — BCBS and UnitedHealthcare plans, Medicaid, and subsidy eligibility

Best Health Insurance in AlabamaCarrier-by-carrier comparison with 2026 premium benchmarks and network depth

Alabama Health Insurance MarketplaceEnrollment, deadlines, and subsidy eligibility on the HealthCare.gov marketplace

Short-Term Health Insurance AlabamaBridge and gap coverage options for Alabama residents between plans

Alabama Small Business Health InsuranceGroup plans, the SHOP tax credit, and ICHRA for Alabama employers

Individual Health Insurance AlabamaSelf-employed and individual coverage options through HealthCare.gov for 2026

Ready to find affordable Alabama coverage?

Compare all four Alabama carriers with subsidies applied. A licensed agent finds the most affordable plan for your income at no cost to you.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Alabama residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.