Alabama Health Insurance Marketplace 2026: Enrollment, Carriers and Subsidies

Alabama uses the federal marketplace at HealthCare.gov — there is no state-based exchange. Four carriers compete on the Alabama marketplace for 2026: Blue Cross Blue Shield of Alabama, UnitedHealthcare, Ambetter, and Oscar, which entered Alabama for the first time this year. This guide covers enrollment dates, subsidy eligibility by income, metal tier selection, and how to enroll outside open enrollment using a special enrollment period.

What brings you here today?

Alabama Marketplace Enrollment Dates and How to Enroll

Open enrollment for 2026 Alabama marketplace coverage ran November 1, 2025 through January 15, 2026. Alabama uses the federal marketplace at HealthCare.gov — enrollment goes through HealthCare.gov directly, through a certified navigator, or through a licensed agent. Starting with 2027 coverage, open enrollment ends December 15 — the January 15 extension is ending. Plans selected by December 15 take effect January 1; plans selected between December 16 and January 15 took effect February 1 for 2026.

Enrolling through a licensed agent costs the same as enrolling directly on HealthCare.gov — premiums are identical regardless of channel. Agents can access HealthCare.gov systems on your behalf, compare all four Alabama carriers side by side, and apply subsidy calculations based on your income before you make a decision. The enrollment process typically takes 20 to 40 minutes with supporting income documentation ready.

2027 enrollment deadline change: Starting with the 2027 plan year, Alabama open enrollment ends December 15. The January 15 extension was a pandemic-era policy that is expiring. If you are planning 2027 coverage, set a reminder for November 1, 2026 — the December 15 deadline gives you only 45 days to compare and enroll, versus the 75-day window that existed for 2026.

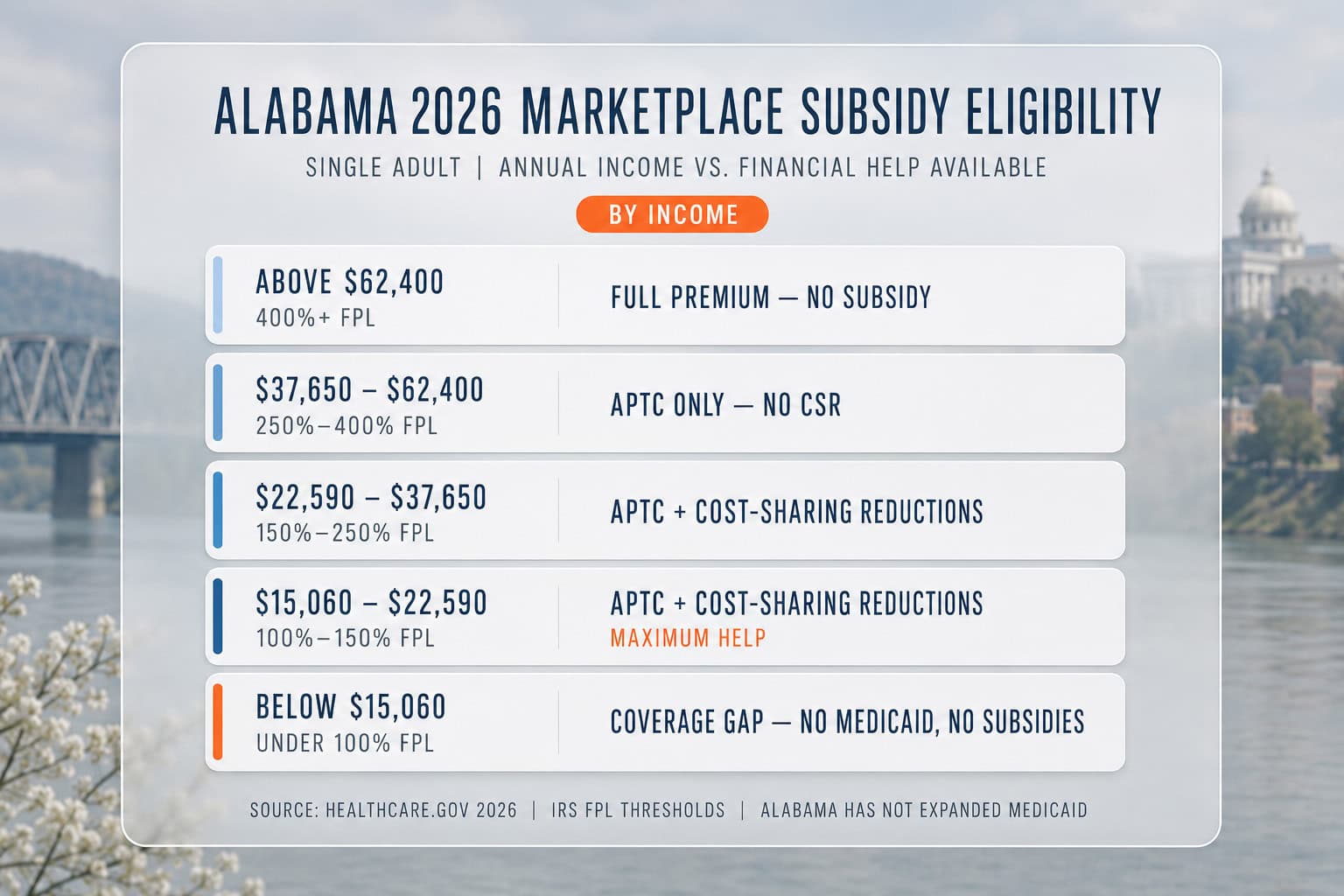

Subsidy Eligibility on the Alabama Marketplace

Federal premium tax credits are available to Alabama residents with household income between 100% and 400% of the Federal Poverty Level — approximately $15,060 to $62,400 for a single adult in 2026. Alabama has not expanded Medicaid and has no state-funded subsidies, so residents below $15,060 fall into a coverage gap with no marketplace assistance. Per CMS open enrollment data, 92% of Alabama marketplace enrollees qualified for subsidies in 2025.

| Income (Single Adult) | FPL % | Marketplace Eligibility |

|---|---|---|

| Below $15,060 | Below 100% FPL | Coverage gap — no subsidies, no Medicaid expansion |

| $15,060 – $22,590 | 100% – 150% FPL | APTC + CSR on Silver plans (maximum subsidy) |

| $22,590 – $37,650 | 150% – 250% FPL | APTC + CSR on Silver plans |

| $37,650 – $62,400 | 250% – 400% FPL | APTC — no CSR above 250% FPL |

| Above $62,400 | Above 400% FPL | No federal subsidy — full sticker price |

Source: HealthCare.gov premium tax credit tables and 2026 Federal Poverty Level guidelines.

Cost-sharing reductions (CSR) lower your deductible and out-of-pocket maximum on Silver plans if your income falls below 250% FPL (about $37,650 single). CSR is only available on Silver-tier marketplace plans — it does not apply to Bronze, Gold, or Platinum tiers. The combination of APTC and CSR makes Silver plans the best financial value for most subsidized Alabama enrollees below 250% FPL, per IRS premium tax credit rules. See the affordable Alabama health insurance guide for income-specific cost examples.

Alabama’s coverage gap: Alabama is one of 10 states that has not expanded Medicaid. Residents earning below $15,060 as a single adult earn too little to qualify for marketplace subsidies but do not meet Alabama’s traditional Medicaid income limits. These roughly 90,000 Alabamians are not eligible for financial help on the marketplace. See the Alabama health insurance guide for alternatives including short-term plans and community health centers.

Special Enrollment Periods: Enrolling Outside Open Enrollment

If you miss Alabama’s open enrollment window, you can still enroll within 60 days of a qualifying life event. The most common triggers are losing job-based coverage, getting married or divorced, having a baby, moving to Alabama from another state or county, and aging off a parent’s plan at 26. The 60-day window starts on the date of the qualifying event — not the date you contact an agent or visit HealthCare.gov.

Losing Job-Based Coverage

Most common SEP trigger. Losing employer coverage — whether through layoff, resignation, or hours reduction — qualifies. The 60-day window starts on the last day of your employer coverage. Keep your termination notice or COBRA election letter as documentation.

Marriage or Divorce

Marriage triggers a 60-day SEP for both spouses. Divorce also qualifies if it results in loss of coverage. A marriage certificate or divorce decree is required as documentation during the SEP enrollment process.

Birth or Adoption

Having a baby or adopting a child opens a 60-day enrollment window. The new dependent can be added immediately without waiting for the next open enrollment. A birth certificate or adoption finalization document is required.

Moving to Alabama

Moving to Alabama from another state or to a new county within Alabama that has different plan options qualifies for a 60-day SEP. Documentation includes a new lease, utility bill, or official mail at the new Alabama address.

Aging off a parent’s plan at 26: Turning 26 triggers a 60-day SEP. Coverage under a parent’s plan ends on your 26th birthday (or the end of that month, depending on the plan). You can enroll in your own Alabama marketplace plan within 60 days of that date. Many 26-year-olds qualify for substantial APTC subsidies as new individual market entrants with early-career incomes.

Choosing the Right Metal Tier on the Alabama Marketplace

Alabama marketplace plans come in four metal tiers — Bronze, Silver, Gold, and Platinum. For most subsidized Alabama enrollees below 250% FPL, Silver is the best choice because cost-sharing reductions only apply to Silver plans. Above 250% FPL, Bronze gives the lowest monthly premium if you rarely use healthcare; Gold is better if you expect frequent care and the monthly premium difference over Silver is smaller than your expected cost-sharing savings.

| Tier | Monthly Premium | Deductible (typical) | Best For |

|---|---|---|---|

| Bronze | Lowest | $5,000 – $9,100 | Healthy adults above 250% FPL who rarely use care; HSA-eligible plans |

| Silver | Mid-range | $300 – $3,500 with CSR; $3,000 – $5,500 without | Most subsidized enrollees — only tier eligible for CSR |

| Gold | Higher | $500 – $1,500 | Frequent healthcare users; chronic conditions; families with predictable costs |

| Platinum | Highest | $0 – $500 | Very high healthcare users; limited availability on Alabama marketplace |

Source: HealthCare.gov metal tier standards and typical 2026 Alabama marketplace plan parameters.

The Silver CSR advantage at 200% FPL

An Alabama resident earning $30,200 — exactly 200% of the 2026 FPL — qualifies for both APTC and CSR. On a standard Silver plan, the deductible might be $3,500. With the CSR benefit applied at 200% FPL, that same Silver plan’s deductible drops to approximately $500, and the out-of-pocket maximum falls from $9,100 to around $2,700. The monthly premium after APTC is typically under $100. This is why financial advisors consistently recommend Silver for subsidized Alabama enrollees below 250% FPL — the CSR makes it dramatically more valuable than the sticker premium difference suggests.

Get a free Alabama marketplace quote

A licensed agent compares all four Alabama carriers with subsidies applied — at no cost to you.

The Four Alabama Marketplace Carriers for 2026

Blue Cross Blue Shield of Alabama, UnitedHealthcare, Ambetter, and Oscar compete on Alabama’s marketplace for 2026. Blue Cross dominates with over 90% market share and the deepest statewide network — essential for rural Alabama residents. Oscar entered Alabama for the first time in 2026, adding a fourth option in urban markets. The right carrier depends on your location, your current providers, and whether network breadth or premium price is the priority.

Blue Cross has served Alabama for over 90 years and integrates deeply with UAB Health System in Birmingham — the state’s academic medical center for complex care. Rural Alabamians in the Black Belt region and northern Alabama counties typically have only Blue Cross as a viable in-network option. UnitedHealthcare competes effectively in Birmingham, Huntsville, and Mobile but has limited rural presence. Ambetter (Centene) offers the lowest premiums on some tiers but a narrower network. Oscar is new to Alabama and its network is still being established — worth considering for tech-comfortable urban enrollees who want virtual care features but risky for anyone relying on specific providers being in-network.

Frequently Asked Questions

Does Alabama have its own health insurance marketplace?

No. Alabama uses the federal marketplace at HealthCare.gov — there is no state-based exchange. All individual marketplace enrollment for Alabama goes through HealthCare.gov. Four carriers compete on the Alabama marketplace for 2026: Blue Cross Blue Shield of Alabama, UnitedHealthcare, Ambetter, and Oscar, which entered Alabama for the first time in 2026.

When is open enrollment for the Alabama marketplace in 2026?

Open enrollment for 2026 coverage ran November 1, 2025 through January 15, 2026. If you missed open enrollment, you can still enroll within 60 days of a qualifying life event — job loss, marriage, divorce, having a baby, or moving to Alabama. Starting with 2027 coverage, open enrollment will end December 15 instead of January 15.

What income qualifies for subsidies on the Alabama marketplace?

Federal premium tax credits are available to Alabama residents with household income between 100% and 400% of the Federal Poverty Level — approximately $15,060 to $62,400 for a single adult in 2026. Residents below $15,060 may fall into Alabama’s Medicaid coverage gap since Alabama has not expanded Medicaid. There are no state-funded subsidies beyond the federal tax credit.

Which metal tier should I choose on the Alabama marketplace?

If your income is below 250% FPL (about $37,650 single), a Silver plan is almost always the best choice because cost-sharing reductions only apply to Silver tier — they lower your deductible and out-of-pocket maximum significantly. If you’re above 250% FPL and healthy, Bronze gives the lowest monthly premium. Gold makes financial sense if you use healthcare frequently and the monthly premium difference over Silver is smaller than your expected cost-sharing savings.

What qualifies as a special enrollment period in Alabama?

Qualifying life events that trigger a 60-day special enrollment window include: losing job-based coverage, losing Medicaid or CHIP eligibility, getting married, getting divorced, having a baby or adopting a child, moving to a new state or county, aging off a parent’s plan at 26, and certain income changes that affect subsidy eligibility. The 60-day window starts on the date of the qualifying event, not the date you apply.

How does the Alabama coverage gap affect marketplace enrollment?

Alabama has not expanded Medicaid, leaving roughly 90,000 residents in a coverage gap — earning below $15,060 as a single adult but not qualifying for traditional Medicaid. These residents are not eligible for marketplace subsidies, making full-price marketplace plans ($400 to $600 per month) unaffordable. They do not qualify for marketplace tax credits and must look at short-term plans or community health centers instead.

Related Alabama Health Insurance Resources

Complete 2026 overview — BCBS and UnitedHealthcare plans, Medicaid, and subsidy eligibility

Best Health Insurance in AlabamaCarrier-by-carrier comparison with 2026 premium benchmarks and network depth

Individual Health Insurance AlabamaSelf-employed and individual coverage options through HealthCare.gov for 2026

Affordable Health Insurance AlabamaHow subsidies cut premiums for the 92% of Alabama enrollees who qualify

Alabama Small Business Health InsuranceGroup plans, the SHOP tax credit, and ICHRA for Alabama employers

Short-Term Health Insurance AlabamaBridge and gap coverage options for Alabama residents between plans

Ready to enroll in an Alabama marketplace plan?

A licensed agent handles the HealthCare.gov enrollment, applies subsidies, and finds the right plan for your income and providers — at no cost to you.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Alabama residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.