Individual Health Insurance in Alabama 2026: Plans, Costs and Subsidies

This guide covers individual health insurance in Alabama for 2026 — the four marketplace carriers competing for your business, what plans actually cost before and after subsidies, the self-employed tax angle, and how COBRA compares when you lose job coverage. About one in seven Alabama adults between 19 and 64 buys their own coverage, and 98% of Alabama marketplace enrollees received subsidies in 2025.

What brings you here today?

Who Buys Individual Coverage in Alabama

Individual health insurance in Alabama covers residents who don’t have access to a group plan through an employer or spouse. The largest segment is self-employed Alabamians — freelancers, contractors, consultants, and small business owners. Other major segments include people between jobs, young adults aging off a parent’s plan at 26, early retirees bridging to Medicare, and part-time workers without employer coverage.

Individual market enrollment in Alabama tracks closely with the state’s economic structure. Self-employed Alabamians make up the largest single share, with Birmingham, Huntsville, and Mobile metro areas accounting for the highest concentrations of independent contractors. Huntsville aerospace layoffs in early 2026 pushed thousands of newly unemployed engineers and technicians into the individual market — many qualifying for subsidies for the first time after years of generous employer coverage.

Self-Employed and 1099 Workers

Freelancers, independent contractors, consultants, and small business owners without group plans. This is the largest segment of Alabama’s individual market. The self-employed premium tax deduction makes marketplace plans even more financially attractive for this group.

Between Jobs

Job loss triggers a 60-day special enrollment period for marketplace coverage. This often beats COBRA pricing by hundreds of dollars per month, especially with subsidies. The Huntsville aerospace layoffs in early 2026 pushed thousands of workers into this category.

Aging Off a Parent’s Plan

Coverage under a parent’s plan ends at age 26. That birthday triggers a qualifying life event and a 60-day special enrollment window. Many young Alabamians qualify for substantial subsidies as new individual market entrants with lower starting incomes.

Early Retirees Pre-Medicare

Alabamians retiring between 55 and 64 use individual marketplace coverage to bridge to Medicare. Premium tax credits scale with income, so early retirees drawing down savings rather than salary often qualify for meaningful subsidies during the bridge years.

How to Buy Individual Coverage in Alabama

Alabama residents have three ways to purchase individual coverage: through the federal marketplace at HealthCare.gov, directly from a carrier, or with help from a licensed agent. Only the marketplace route qualifies for premium tax credits for individual health insurance in Alabama — 98% of enrollees received subsidies in 2025. Licensed agents can access marketplace plans on your behalf with subsidies applied, at no added cost to you.

HealthCare.gov Marketplace

Best for anyone who qualifies for subsidies (income $15,060 to $62,400 single). All four Alabama carriers — Blue Cross, UnitedHealthcare, Ambetter, and Oscar — compete here. Subsidies apply automatically based on projected income. Apply at HealthCare.gov.

Direct From Carrier

Best for people above the subsidy threshold ($62,400+ single) who want a specific carrier. Same plans and premiums as the marketplace, but no subsidy option. Useful if you know exactly which plan you want and don’t qualify for financial help.

Licensed Agent or Broker

Best for anyone who wants help comparing options across carriers. Agents access marketplace plans with subsidies on your behalf. Premiums are the same price as enrolling directly. There’s no added cost for using an agent.

Off-Exchange (Direct or Broker)

Off-marketplace plans from the same Alabama carriers do not qualify for subsidies. The premiums match on-exchange prices. Off-exchange is only relevant for higher-income Alabamians who don’t qualify for tax credits regardless of where they enroll.

Blue Cross dominates Alabama’s individual market with over 90% market share and the largest provider network in the state. For most Alabamians, especially in rural counties, Blue Cross is the default choice because virtually every doctor and hospital accepts it. Oscar, UnitedHealthcare, and Ambetter serve specific metropolitan niches but have more limited networks. See the best health insurance in Alabama guide for a full carrier comparison.

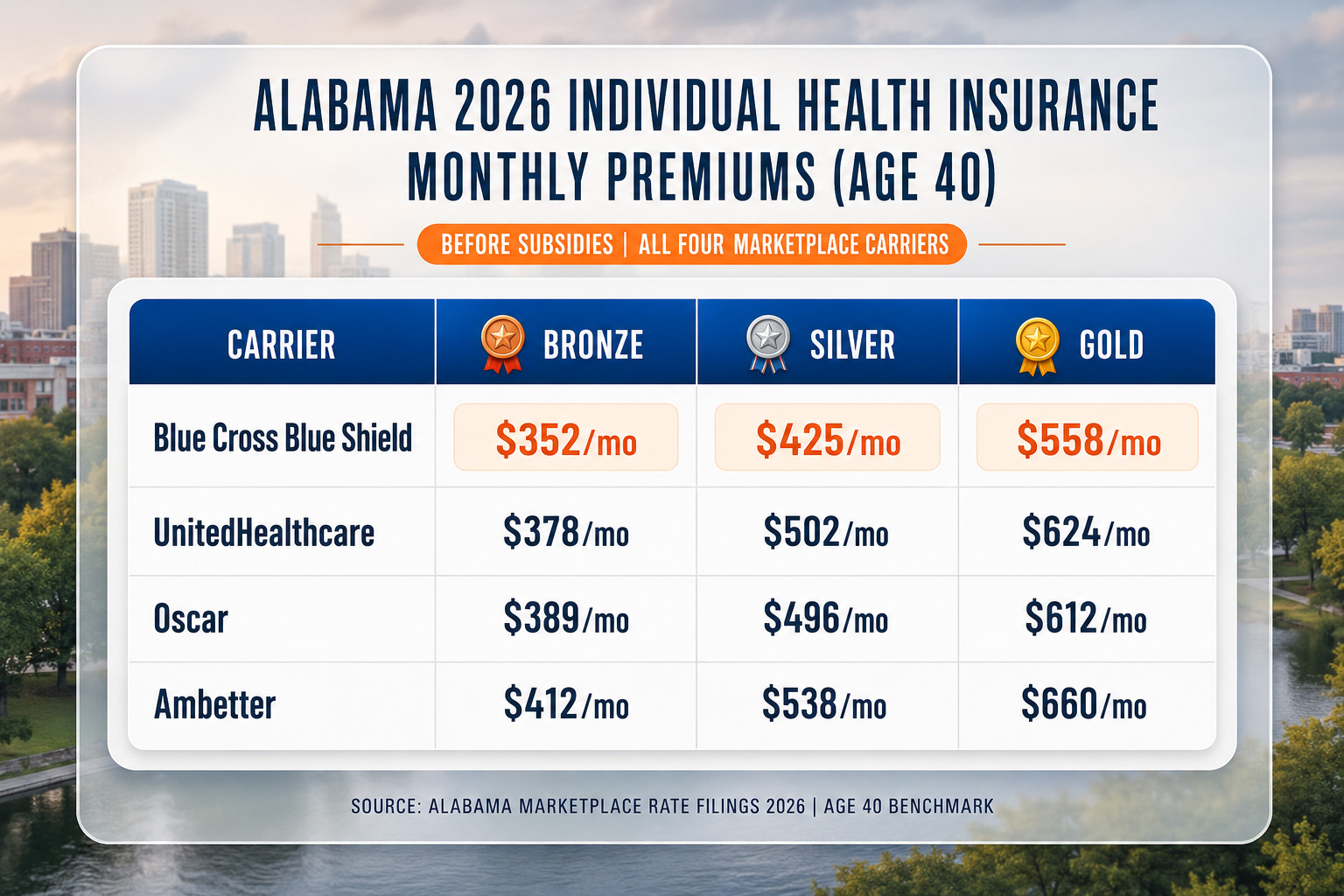

What Individual Plans Cost in Alabama for 2026

Alabama individual market premiums rose 19% to 25% for 2026 after carriers adjusted for higher claims costs and the expiration of enhanced federal subsidies. Before subsidies, a 40-year-old pays $352 to $538 per month for a Silver plan depending on carrier. After federal premium tax credits, 98% of Alabama enrollees pay significantly less — typically $100 to $250 per month for the same Silver plan. Bronze plans run lower; Gold plans run higher.

| Carrier | Bronze (40 y/o) | Silver (40 y/o) | Gold (40 y/o) | 2026 Rate Change |

|---|---|---|---|---|

| Blue Cross Blue Shield of Alabama | $352/mo | $425/mo | $558/mo | +19.3% |

| UnitedHealthcare | $378/mo | $502/mo | $624/mo | +20.0% |

| Oscar | $389/mo | $496/mo | $612/mo | New to AL |

| Ambetter | $412/mo | $538/mo | $668/mo | +25.0% |

These are pre-subsidy sticker prices. Per CMS open enrollment data, 98% of Alabama marketplace enrollees received premium tax credits in 2025, so most Alabamians shopping for individual coverage will pay substantially less than the table shows. A 35-year-old earning $40,000 typically pays $150 to $200 per month for a Silver plan after subsidies. Subsidy amounts scale with household income relative to the Federal Poverty Level and with the cost of the second-lowest Silver plan in your county.

Get a free Alabama individual health insurance quote

A licensed agent compares all four Alabama carriers, applies subsidies based on your income, and shows you the real net premium — at no cost.

Self-Employed Health Insurance in Alabama: The Triple Tax Strategy

Self-employed Alabamians get a tax advantage W-2 employees don’t: a 100% deduction for health insurance premiums on Schedule 1 of their federal return per IRS Publication 535. The deduction lowers adjusted gross income, which can push you into a higher subsidy bracket on the marketplace. Pairing a high-deductible Bronze plan with a Health Savings Account adds a second pre-tax savings layer.

Scenario: Keisha, Mobile graphic designer, age 34, $42,000 income

Keisha left her agency job in January 2026 to freelance from Mobile. Her COBRA option costs $680 per month — $8,160 per year. On the marketplace, she qualifies for subsidies at 279% FPL. A Blue Cross Bronze HSA plan costs $352 per month sticker price; after her premium tax credit, she pays approximately $185 per month. She also contributes $4,300 to an HSA pre-tax, deducts the full $2,220 in annual premiums on Schedule 1 of her 1040, and pays for routine care with HSA dollars. Her effective annual coverage cost after the triple tax benefit is closer to $1,400 — roughly six times cheaper than COBRA, with a higher deductible to manage.

The triple tax benefit math: Self-employed Alabamians who pair a Bronze HSA plan with maximum HSA contributions can stack three federal tax advantages — the Schedule 1 premium deduction, the pre-tax HSA contribution ($4,300 individual / $8,550 family for 2026), and tax-free HSA withdrawals for qualified medical expenses. Combined federal savings typically reach $3,000 to $5,000 per year depending on your bracket.

COBRA vs. Marketplace: The Real Cost Comparison

COBRA lets you keep your former employer’s group plan after job loss, but you pay the full premium plus a 2% administrative fee — typically $400 to $700 per person monthly in Alabama. A subsidized marketplace plan covering the same person usually costs $100 to $250 monthly. For most Alabamians losing job coverage, marketplace individual health insurance in Alabama is dramatically cheaper than COBRA, and job loss triggers a 60-day special enrollment period to switch.

| Factor | COBRA | Marketplace (with subsidies) |

|---|---|---|

| Monthly cost (typical) | $400 – $700 per person | $100 – $250 per person |

| Coverage duration | 18 months (36 for certain events) | Renewable annually, no time limit |

| Subsidy eligibility | Not eligible | Yes (income $15,060 – $62,400 single) |

| Pre-existing conditions | Covered (same plan continues) | Covered (ACA requirement) |

| Provider network | Same as previous employer plan | Carrier-specific Alabama network |

| Enrollment trigger | Within 60 days of job loss | 60-day special enrollment period |

When COBRA might still make sense: If you’ve already hit your annual deductible on your employer plan and have ongoing expensive treatment scheduled, finishing the calendar year on COBRA can avoid a new deductible reset on a marketplace plan. Also consider COBRA if your current providers are out-of-network on every Alabama marketplace carrier. For most Alabamians, marketplace coverage wins on cost — but a licensed agent can run the side-by-side math for your specific situation before you decide.

Open Enrollment and Special Enrollment Periods

Open enrollment for individual health insurance in Alabama runs November 1, 2025 through January 15, 2026. Outside that window, you can enroll within 60 days of a qualifying life event: losing job coverage, marriage, divorce, having a baby, moving to Alabama from another state, or aging off a parent’s plan. Special enrollment applications go through HealthCare.gov or a licensed agent.

The federal marketplace handles all individual market enrollment for Alabama — there is no state-based exchange. Most qualifying life events require documentation: a termination notice for job loss, a marriage certificate, a birth certificate, a lease showing a new Alabama address. The 60-day special enrollment window starts on the date of the qualifying event, not the date you apply.

If you miss both open enrollment and any special enrollment window, your options narrow significantly: short-term coverage (not ACA-compliant, doesn’t cover pre-existing conditions), Medicaid if you qualify in Alabama’s limited expansion framework, or paying out of pocket until the next open enrollment cycle. Most Alabamians who miss the window find a qualifying life event to trigger a special enrollment — moving, marriage, or income changes that affect Medicaid eligibility all qualify.

Frequently Asked Questions

Can I buy individual health insurance in Alabama without an employer?

Yes. Alabama residents without group coverage can purchase coverage through the federal marketplace at HealthCare.gov, directly from a carrier, or through a licensed agent. Only the marketplace route qualifies for premium tax credits — 98% of Alabama marketplace enrollees received subsidies in 2025.

How much does individual health insurance cost in Alabama in 2026?

Before subsidies, a 40-year-old in Alabama pays $352 to $538 per month for a Silver-tier individual plan in 2026, depending on carrier. After federal premium tax credits, most subsidized enrollees pay $100 to $250 per month. Bronze plans run lower, Gold plans run higher. Alabama individual market premiums rose 19% to 25% for 2026.

Is COBRA or marketplace insurance cheaper in Alabama?

Marketplace coverage with subsidies is typically far cheaper than COBRA for Alabama residents. COBRA runs $400 to $700 per person monthly because you pay the full group premium plus a 2% administrative fee. A subsidized Silver marketplace plan often costs $100 to $250 monthly for the same person. Job loss triggers a 60-day special enrollment period for marketplace coverage.

Can self-employed Alabamians deduct individual health insurance premiums?

Yes. Self-employed Alabamians can deduct 100% of premiums on Schedule 1 of their federal return per IRS Publication 535. The deduction lowers adjusted gross income, which can push you into a higher marketplace subsidy bracket. Pairing a high-deductible Bronze plan with an HSA adds another layer of pre-tax savings.

What carriers sell individual health insurance plans in Alabama for 2026?

Four carriers compete in Alabama’s individual marketplace for 2026: Blue Cross Blue Shield of Alabama (over 90% market share), UnitedHealthcare, Ambetter, and Oscar (new to Alabama for 2026). Blue Cross has the largest provider network, particularly in rural counties. The other three carriers serve specific metropolitan and regional niches.

When can I enroll in Alabama individual coverage?

Open enrollment for 2026 runs November 1, 2025 through January 15, 2026. Outside that window, you can enroll within 60 days of a qualifying life event — losing job coverage, marriage, divorce, having a baby, or moving. Special enrollment applications are filed through HealthCare.gov or a licensed agent.

Related Alabama Health Insurance Resources

Complete 2026 overview — carriers, Medicaid, the coverage gap, and subsidy eligibility

Affordable Health Insurance AlabamaHow subsidies cut premiums for the 92% of Alabama enrollees who qualify

Alabama Health Insurance MarketplaceEnrollment, deadlines, and subsidy eligibility on the HealthCare.gov marketplace

Short-Term Health Insurance AlabamaBridge coverage options, state duration limits, and what short-term plans exclude

Alabama Small Business Health InsuranceGroup plans, the SHOP tax credit, and ICHRA for Alabama employers

Best Health Insurance in AlabamaCarrier-by-carrier comparison with 2026 premium benchmarks and network depth

Ready to compare Alabama individual plans?

A licensed agent compares all four Alabama carriers, runs your subsidy calculation, and finds the plan that fits your budget and providers — at no cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Alabama residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.