Short-Term Health Insurance in Alabama 2026: Plans, Rules and Tradeoffs

Short-term health insurance in Alabama fills coverage gaps for healthy people in a coverage transition — between jobs, waiting for employer benefits, or who missed marketplace open enrollment. Alabama permits plans up to 364 days with renewals allowed up to 36 months total, making it one of the most permissive states for short-term coverage. This guide covers what Alabama short-term plans cost, what they exclude, who they fit, and when marketplace coverage is the smarter choice despite the higher price.

What brings you here today?

Alabama Short-Term Plan Rules for 2026

Alabama permits short-term health insurance plans up to 364 days per term, with renewals allowed for a cumulative total of up to 36 months. This is significantly more permissive than most states — many cap terms at 3 months with no renewals. The Alabama Department of Insurance regulates short-term carriers but has not enacted stricter limits than the federal baseline. Plans can be purchased any time of year with no open enrollment window.

Alabama vs. other states: About 20 states have enacted strict short-term limits — California bans them entirely, and New York caps them at 3 months. Alabama has taken the opposite approach, permitting the maximum duration allowed under federal non-enforcement guidance. This makes Alabama one of the more accessible markets for short-term coverage in the Southeast, alongside Florida, Georgia, and Tennessee.

| Rule | Alabama Short-Term Plans | ACA Marketplace Plans |

|---|---|---|

| Maximum initial term | 364 days | Annual (renewable) |

| Maximum total duration | 36 months (with renewals) | Unlimited (renewable annually) |

| Purchase timing | Any time — no enrollment window | Open enrollment or qualifying event |

| Coverage start | As fast as next day | 1st of next month (or later) |

| Medical underwriting | Yes — can deny or exclude conditions | No — guaranteed issue |

| Pre-existing conditions | Can be excluded | Fully covered, no waiting period |

| Essential health benefits | Not required | Required (10 categories) |

| Regulator | Alabama DOI | Federal ACA / HHS |

Source: Alabama Department of Insurance and federal short-term plan guidance, 2026.

Who Short-Term Coverage Fits in Alabama

Short-term health insurance in Alabama fits a narrow but real set of use cases: healthy adults in a defined transition period who don’t qualify for meaningful marketplace subsidies. The core use cases are job transitions with a firm employer coverage start date, missed open enrollment with no qualifying life event, early retirees bridging to Medicare who are above the subsidy threshold, and young Alabamians in the coverage gap who can’t afford full marketplace prices.

Good fit — consider short-term

Between jobs with a new employer start date within 6 months. Missed January 15 enrollment with no qualifying event and no ongoing conditions. Income above $62,400 single — no subsidy available, full marketplace sticker price applies. Early retiree bridging 1-2 years to Medicare, healthy, above subsidy threshold.

Poor fit — use marketplace instead

Income below $62,400 single — almost certainly qualify for subsidized marketplace coverage at lower net cost than short-term. Any ongoing health condition — short-term will exclude it. Need maternity, mental health, or substance abuse coverage — all frequently excluded. In the Medicaid coverage gap — consider community health centers first.

Scenario: James, Decatur warehouse worker, age 29, laid off in March

James lost his job at a Decatur distribution center in March 2026 and his employer coverage ended April 30. His new job at a Morgan County manufacturer starts August 1 — but coverage doesn’t kick in until September 1. He has a 4-month gap. His options: COBRA costs $487/month to continue his former group plan. A marketplace plan after subsidies costs approximately $95/month, but enrolling requires documentation and takes 2-3 weeks to process. A Blue Cross short-term plan starts in 2 days at $138/month with a $2,500 deductible. James is 29 and healthy with no ongoing conditions. He chooses the marketplace — the $43/month difference over 4 months is $172, and the marketplace plan has no pre-existing exclusion risk and covers prescriptions. He uses his 60-day SEP triggered by job loss.

What Short-Term Plans Cover and Exclude

Short-term plans in Alabama cover basic hospitalization, emergency care, and physician visits — but commonly exclude pre-existing conditions, maternity care, mental health treatment, substance abuse services, and prescription drugs. Coverage limits and annual benefit caps vary significantly by plan and carrier. Some plans exclude any condition treated in the past 2 to 5 years, which can result in claim denials for conditions the enrollee did not know existed at enrollment.

| Benefit | Short-Term Plans (Alabama) | ACA Marketplace Plans |

|---|---|---|

| Emergency care | Covered (benefit caps may apply) | Covered (no annual/lifetime caps) |

| Hospitalization | Covered (benefit caps apply) | Covered (no annual/lifetime caps) |

| Physician visits | Covered (after deductible/copay) | Covered (after deductible/copay) |

| Pre-existing conditions | Often excluded entirely | Fully covered — no exclusion |

| Maternity care | Usually excluded | Required essential benefit |

| Mental health | Often excluded or limited | Required — parity with medical |

| Prescription drugs | Often excluded or limited formulary | Required essential benefit |

| Preventive care | Rarely covered | Covered at no cost (in-network) |

| Annual benefit cap | Common — varies by plan | Prohibited under ACA |

Source: ACA essential health benefit standards and typical Alabama short-term plan terms, 2026.

The pre-existing exclusion risk: Short-term plans in Alabama can exclude any condition for which you received advice, diagnosis, care, or treatment within a lookback period — typically 2 to 5 years. This means a condition you consider managed or minor could result in denied claims during the short-term coverage period. A knee injury from three years ago. A blood pressure medication started in 2023. A mental health visit in 2024. Any of these can trigger an exclusion. If you have any ongoing health conditions, marketplace coverage with ACA guaranteed issue is the safer choice regardless of cost difference.

Compare short-term and marketplace options side by side

A licensed agent runs both options with your actual subsidy and shows you the real cost difference before you decide.

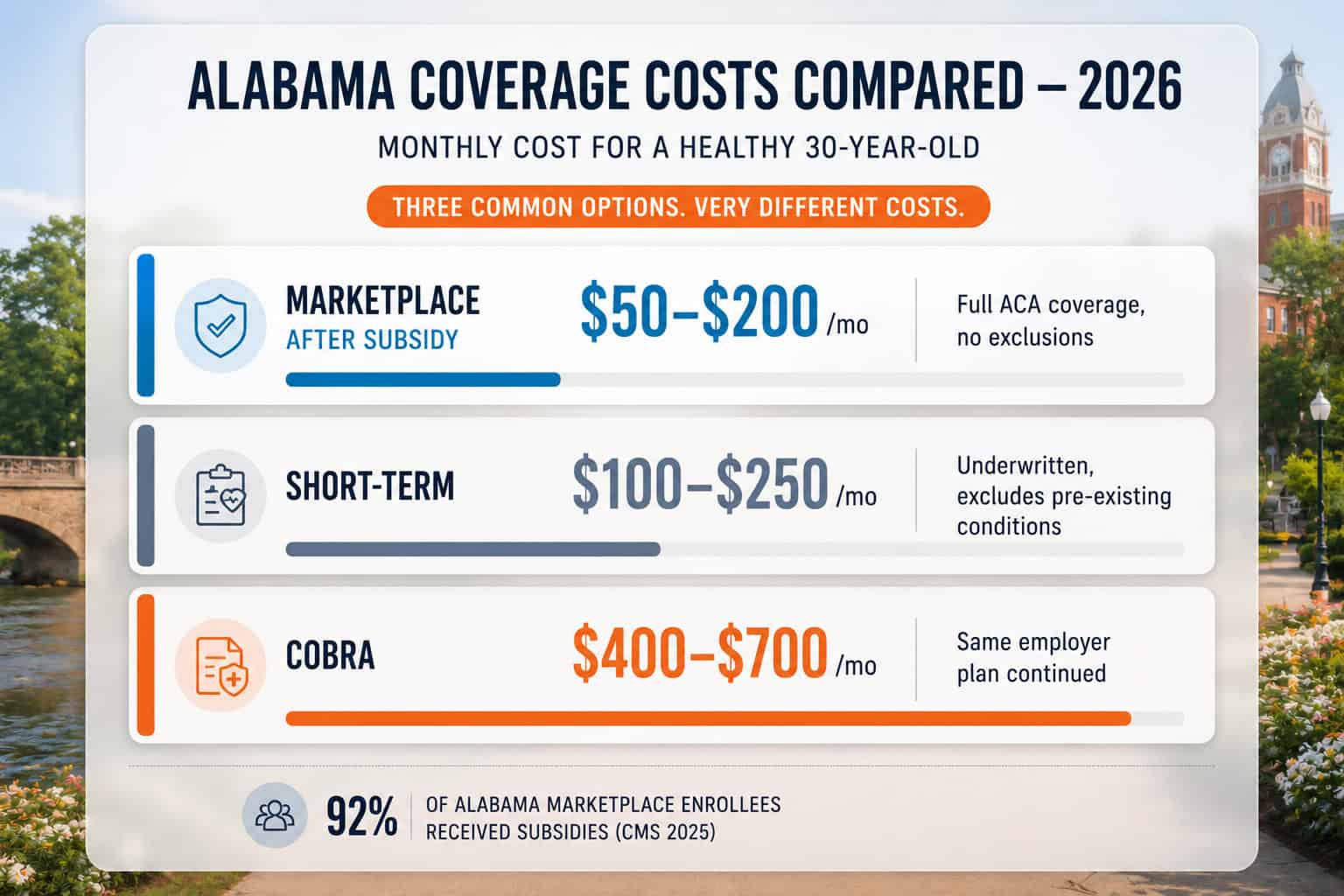

Short-Term vs COBRA vs Marketplace: The Real Cost Comparison

For most Alabamians who qualify for marketplace subsidies, the subsidized marketplace plan is cheaper than both COBRA and short-term. COBRA runs $400 to $700 per person monthly. Short-term plans run $100 to $250 monthly for a healthy adult, with higher deductibles and significant coverage exclusions. Subsidized marketplace Silver plans often cost $50 to $200 monthly for qualifying income levels with full ACA coverage and no pre-existing exclusions.

| Factor | Short-Term | COBRA | Marketplace (with subsidies) |

|---|---|---|---|

| Monthly cost (healthy 30-year-old) | $100 – $250 | $400 – $700 | $50 – $200 (after APTC) |

| Pre-existing conditions | Can be excluded | Covered (same plan) | Fully covered |

| Maternity coverage | Usually excluded | Covered | Covered |

| Prescription drugs | Often excluded | Covered | Covered |

| Enrollment timing | Any time | Within 60 days of job loss | 60-day SEP after job loss |

| Coverage start | 1-2 days | Retroactive to coverage end | 1st of next month |

| Duration | Up to 36 months | 18 months (most situations) | Annual, renewable |

Source: CMS marketplace data and typical 2026 Alabama short-term and COBRA premium ranges.

The right choice depends primarily on whether you qualify for marketplace subsidies. If your income is below $62,400 as a single adult, check your marketplace cost before assuming short-term is cheaper. Per CMS enrollment data, 92% of Alabama marketplace enrollees received subsidies in 2025 — the majority of people considering short-term coverage likely qualify for subsidized marketplace plans that cost less and cover more. The affordable Alabama health insurance guide covers subsidy calculations in detail. For those who don’t qualify for subsidies and are in a short defined transition, short-term coverage remains a practical lower-cost option when purchased from a reputable carrier like those reviewed by HHS. See the best health insurance in Alabama guide for a full carrier comparison, and if you employ staff, the Alabama small business health insurance guide covers group and ICHRA options.

Frequently Asked Questions

How long can short-term health insurance last in Alabama?

Alabama permits short-term health insurance plans up to 364 days per term, with renewals allowed up to 36 months total. This is more permissive than most states — many cap short-term plans at 3 months with no renewals. Alabama follows federal non-enforcement guidance that allows longer terms, and the state has not enacted additional restrictions beyond the federal baseline.

Does short-term health insurance in Alabama cover pre-existing conditions?

No. Short-term plans in Alabama use medical underwriting and can deny applicants for pre-existing conditions or exclude them from coverage after enrollment. Some plans exclude any condition treated within the past 2 to 5 years. This is the biggest difference from ACA marketplace plans, which are required to cover pre-existing conditions without exclusion. If you have ongoing health conditions, a marketplace plan is almost always a better choice.

Is short-term health insurance cheaper than marketplace plans in Alabama?

For healthy individuals who don’t qualify for marketplace subsidies, short-term plans typically cost 30% to 60% less per month than comparable marketplace plans at full sticker price. However, for the 92% of Alabama marketplace enrollees who qualified for subsidies in 2025, subsidized marketplace coverage is often cheaper than short-term — especially Silver plans with cost-sharing reductions below 250% FPL.

What does short-term health insurance not cover in Alabama?

Short-term plans in Alabama are not required to cover the ACA’s ten essential health benefits. Common exclusions include: pre-existing conditions (often any condition treated in the past 2 to 5 years), maternity care, mental health and substance abuse treatment, prescription drugs (or limited drug coverage), preventive care, and pediatric dental and vision. Coverage limits and benefit caps vary significantly by plan.

Who should consider short-term health insurance in Alabama?

Short-term coverage makes the most sense for healthy Alabamians in a defined transition: between jobs, waiting for new employer benefits to start, or who missed the January 15 marketplace enrollment deadline and have no qualifying life event. It is not appropriate for people with ongoing health conditions, those who need maternity coverage, or anyone who qualifies for meaningful marketplace subsidies — for those groups, marketplace plans are almost always a better choice.

What carriers sell short-term health insurance in Alabama?

Several carriers offer short-term plans in Alabama including Blue Cross Blue Shield of Alabama, Golden Rule (a UnitedHealthcare company), Pivot Health, and National General. Blue Cross short-term plans use the same provider network as their marketplace plans, which is an advantage for Alabamians who want continuity of care during a coverage gap.

Related Alabama Health Insurance Resources

Complete 2026 overview — BCBS and UnitedHealthcare plans, Medicaid, and subsidy eligibility

Best Health Insurance in AlabamaCarrier-by-carrier comparison with 2026 premium benchmarks and network depth

Individual Health Insurance AlabamaSelf-employed and individual coverage options through HealthCare.gov for 2026

Affordable Health Insurance AlabamaHow subsidies cut premiums for the 92% of Alabama enrollees who qualify

Alabama Health Insurance MarketplaceEnrollment, deadlines, and subsidy eligibility on the HealthCare.gov marketplace

Short-Term Health Insurance AlabamaBridge and gap coverage options for Alabama residents between plans

Ready to compare your Alabama coverage options?

A licensed agent compares short-term, marketplace, and COBRA options for your specific situation — at no cost to you.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Alabama residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.