New Jersey Health Insurance 2026: GetCoveredNJ Plans, Carriers & State Subsidies

New Jersey health insurance for 2026 looks different from almost every other state in two important ways. The Garden State runs its own marketplace — GetCoveredNJ — instead of using HealthCare.gov, and it funds a state premium subsidy program (NJ Health Plan Savings) that extends financial help up to 600 percent of the federal poverty level, well above the federal cutoff. New Jersey also maintains an individual mandate, requiring residents to carry minimum essential coverage or pay a Shared Responsibility Payment on their state tax return. This guide walks through the 2026 marketplace, all five participating carriers, NJ Health Plan Savings, NJ FamilyCare, and how to choose coverage for your household.

What are you looking for?

The New Jersey Health Insurance Marketplace for 2026

New Jersey residents buying individual coverage for 2026 do so through GetCoveredNJ, the state-based health insurance marketplace operated by the New Jersey Department of Banking and Insurance. New Jersey transitioned from HealthCare.gov to its own platform in November 2020, unlocking a longer open enrollment window, state-funded premium subsidies, and a tax-time enrollment program unavailable on the federal platform.

| Feature | GetCoveredNJ (NJ State-Based) | HealthCare.gov (Federal Default) |

|---|---|---|

| Open Enrollment Window | Nov 1 – Jan 31 (3 months) | Nov 1 – Jan 15 (most states) |

| State subsidy | NJ Health Plan Savings to 600% FPL | None |

| Tax-time enrollment | NJ Easy Enrollment Program | Not available |

| Number of 2026 carriers | 5 carriers | Varies by state |

| Operating since | November 2020 | 2014 |

Open enrollment for 2026 ran from November 1, 2025 through January 31, 2026 — about two weeks longer than the federal default. New Jersey closed open enrollment with 509,192 residents enrolled, though approximately 70,000 dropped coverage by April 15, 2026 due to non-payment of higher premiums following the expiration of enhanced federal subsidies. The 2026 plan year is the most disrupted in NJ marketplace history, with average premiums up 16.6 percent and many enrollees shifting from Silver to Bronze plans to keep monthly costs manageable.

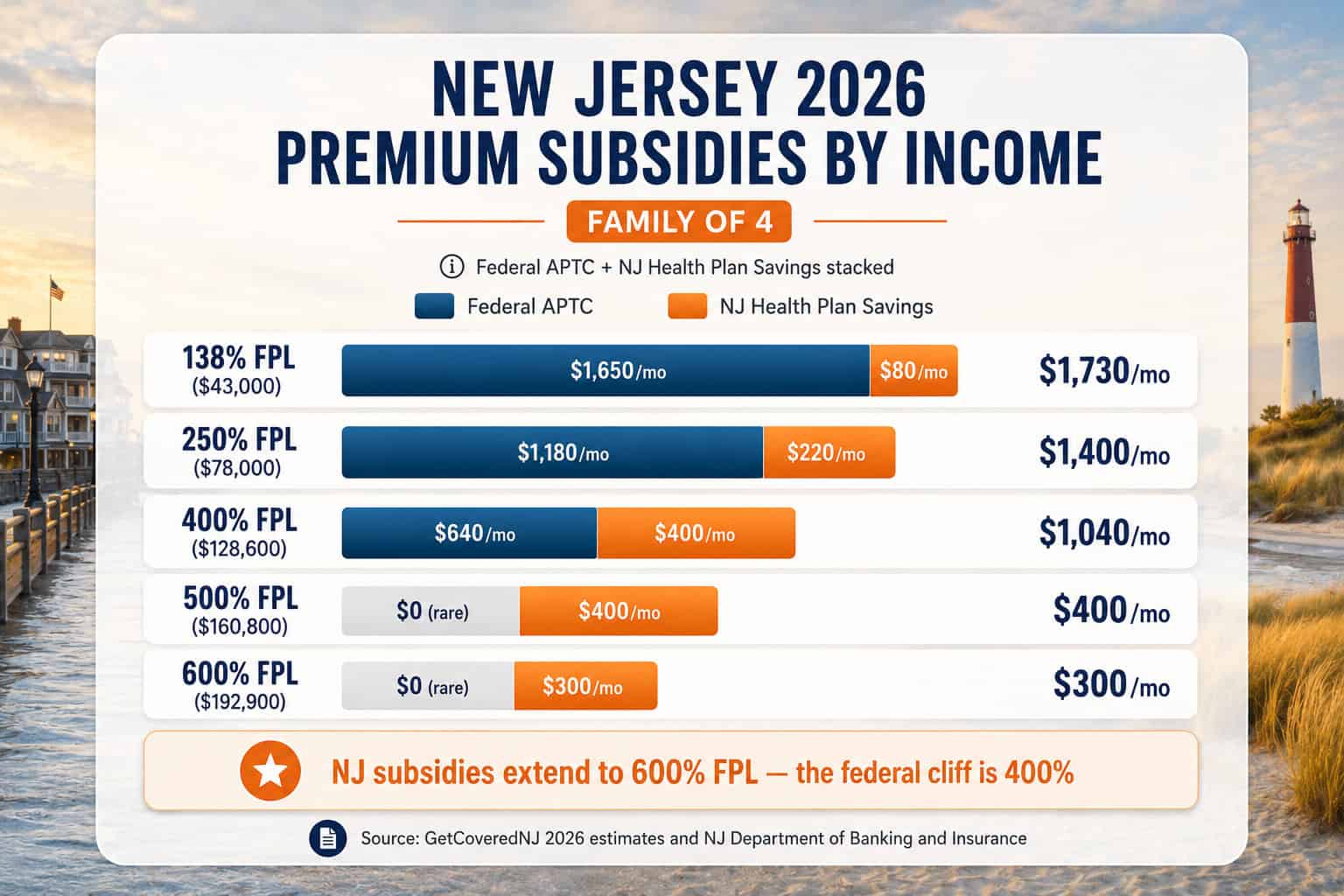

How NJ Health Plan Savings Work in 2026

New Jersey residents have access to a state-funded premium subsidy that no other state offers in quite the same way. NJ Health Plan Savings — known as NJHPS — provides $20 to $100 per person per month in additional premium assistance on top of any federal premium tax credit. Eligibility extends to households earning up to 600 percent of the federal poverty level, beyond the federal 400 percent ceiling. The state allocated approximately $215 million to fund NJHPS for 2026.

| Income Range (Family of 4) | FPL Band | Federal APTC | NJ Health Plan Savings |

|---|---|---|---|

| Under $43,000 | Under 138% | Likely Medicaid eligible | Not applicable |

| $43,000–$78,000 | 138%–250% | Yes + Full CSR | Yes ($20–$60/person/mo) |

| $78,000–$128,600 | 250%–400% | Yes | Yes ($60–$100/person/mo) |

| $128,600–$192,900 | 400%–600% | Only if 8.5% cap applies | Yes — sometimes the only subsidy |

| Over $192,900 | Over 600% | Rare | Not eligible |

The 400-to-600 percent FPL bracket matters most in 2026. Federal premium tax credits phased back to their pre-2021 structure at the end of 2025, restoring the 400 percent FPL cliff for most households. For New Jersey residents in this income band, NJHPS is often the only subsidy available — a meaningful difference compared to residents in states without state-funded supplements. The state Department of Banking and Insurance has indicated NJHPS will continue at 600 percent FPL through 2026 regardless of federal action.

Health Insurance Carriers in New Jersey for 2026

GetCoveredNJ shoppers choose among five carriers for 2026 — down from six in 2025 after Aetna exited the New Jersey individual marketplace at the end of 2025. The remaining five carriers cover the state with varying plan portfolios and 2026 rate increases. Carrier choice matters significantly because provider networks, plan structures, and premium changes differ substantially between insurers.

Horizon Blue Cross Blue Shield of NJ

Largest NetworkHorizon BCBSNJ is the Garden State’s flagship insurer with 3.7 million members across coverage lines. Largest provider network in all 21 NJ counties with HMO, PPO, EPO, OMNIA, and Direct Access plan types. 2026 rate change: +17.0 percent. Strongest choice for households with established specialist relationships statewide.

AmeriHealth

Family ValueStrong Central and South Jersey network with competitive family-plan pricing. AmeriHealth has been a stable marketplace participant since the GetCoveredNJ launch and offers HMO and POS-style products. 2026 rate change: +13.5 percent. Good balance of network breadth and affordability for households without specific Horizon network requirements.

Oscar Health

Lowest 2026 IncreaseTech-focused carrier with strong digital experience and 24/7 telehealth integration. Oscar posted the lowest 2026 rate change among NJ carriers at +4.6 percent — making it disproportionately attractive for households willing to manage benefits through the Oscar app. Network is narrower than Horizon, especially in suburban North Jersey.

UnitedHealthcare

National ReachNational carrier with reciprocity that benefits NJ residents traveling out of state or maintaining ties to out-of-state providers. Strong digital tools and pharmacy benefit management. 2026 rate change: +18.4 percent — the highest among NJ carriers, partly reflecting broader national pricing trends.

Ambetter from WellCare

Budget BronzeCentene-operated Ambetter focuses on cost-conscious buyers with strong Bronze and Silver pricing across the state. Growing network coverage particularly in urban North Jersey. Useful option for healthy younger adults at 138-250 percent FPL where Silver with cost-sharing reductions delivers strong total value.

Aetna (Exited)

No Longer AvailableAetna withdrew from the New Jersey individual marketplace at the end of 2025 along with marketplaces nationwide. Aetna members who were auto-renewed needed to actively select a new carrier during 2026 open enrollment. Aetna still offers New Jersey small group and Medicare Advantage products — only the individual marketplace exited.

Plan Types in New Jersey

New Jersey residents can choose among several plan structures, each balancing premium cost against network flexibility differently. The carrier mix and the geographic reach of each plan type affect which structure makes sense for a given household. North Jersey residents who frequently travel to New York City and South Jersey residents with Philadelphia provider relationships often weigh network breadth differently than residents in Central Jersey.

| Plan Type | Referral Required | Out-of-Network Coverage | Typical Premium Tier |

|---|---|---|---|

| HMO | Yes (PCP-led) | Emergency only | Lowest |

| POS | Yes for out-of-network | Partial with referral | Mid |

| EPO | No | None (in-network only) | Mid |

| PPO | No | Partial | Highest |

| OMNIA Tiered | No | Partial (3 tiers) | Lower than PPO |

Horizon’s OMNIA Health Plans are unique to New Jersey and worth understanding. OMNIA uses a tiered network with three levels — Tier 1 (designated preferred providers and hospital systems), Tier 2 (standard network), and Tier 3 (out-of-network). Premiums are lower than traditional PPO, and out-of-pocket costs drop substantially when members use Tier 1 providers. The structure works well for households comfortable with Horizon’s preferred provider list — typically members of RWJBarnabas Health, Hackensack Meridian Health, and Atlantic Health System network hospitals.

Cost of Health Insurance in New Jersey for 2026

Health insurance costs in New Jersey rose substantially between 2025 and 2026. Average individual market premiums increased 16.6 percent year over year — driven largely by the expiration of enhanced federal premium tax credits at the end of 2025 and rising medical and pharmacy costs. Households eligible for both federal APTC and NJ Health Plan Savings absorbed much less of the increase than households above the 600 percent FPL subsidy cliff.

| Household Profile | Silver Premium Range | After Subsidies (if eligible) |

|---|---|---|

| 30-year-old single | $420–$550/mo | $60–$280/mo (varies by FPL) |

| 40-year-old single | $485–$680/mo | $80–$320/mo |

| 50-year-old single | $695–$960/mo | $140–$460/mo |

| 60-year-old single | $1,050–$1,440/mo | $240–$720/mo |

| Family of 4 (parents 40) | $1,650–$2,200/mo | $260–$1,050/mo |

The shift from Silver to Bronze plans tells the story of 2026 affordability. In plan year 2025, 83 percent of active shoppers on GetCoveredNJ chose Silver. For 2026, that dropped to 68 percent while Bronze selections nearly doubled from 16 percent to 31 percent. Households facing higher premiums traded richer benefits for lower monthly costs — a trade that often costs more annually if any meaningful care is needed because Bronze deductibles run $7,000-9,000 single and $14,000-18,000 family compared to Silver’s $4,500-6,000 and $9,000-12,000.

Compare GetCoveredNJ Plans with NJ Health Plan Savings

Eight in ten New Jersey residents qualify for federal premium tax credits, NJ Health Plan Savings, or both. A licensed New Jersey broker confirms subsidy eligibility, compares all five carriers, and handles enrollment through GetCoveredNJ at no cost.

NJ FamilyCare for Children and Low-Income Adults

NJ FamilyCare is New Jersey’s Medicaid and Children’s Health Insurance Program (CHIP), covering approximately 1.8 million state residents — roughly 20 percent of the population. Eligibility runs through the same GetCoveredNJ application as marketplace plans, so applicants are routed to FamilyCare automatically when household income qualifies. The NJ FamilyCare program covers comprehensive medical, dental, vision, mental health, prescription drug, and hospital care with minimal or no copays depending on category.

| NJ FamilyCare Category | FPL Limit | Approx Income Cap |

|---|---|---|

| Children (under 19) | 355% FPL | ~$111,000 family of 4 |

| Pregnant women | 205% FPL | ~$31,800 single + 12mo postpartum |

| Adults 19–64 (expansion) | 138% FPL | ~$21,597 single |

| Aged, Blind, Disabled | 100% FPL | ~$15,650 single (asset-tested) |

New Jersey children qualify for FamilyCare up to 355 percent of FPL regardless of immigration status — one of the most expansive children’s coverage thresholds in the country. Undocumented children of any household income up to the 355 percent ceiling are eligible. This makes the split-coverage approach common: children on NJ FamilyCare while parents enroll in a GetCoveredNJ marketplace plan with NJ Health Plan Savings. Most households with income below approximately $111,000 see children automatically routed to FamilyCare when applying through the marketplace.

The NJ Individual Mandate and Shared Responsibility Payment

New Jersey is one of a handful of states that maintains an individual health insurance mandate. The NJ Health Insurance Market Preservation Act of 2018 requires most state residents to carry minimum essential coverage each month or pay a Shared Responsibility Payment on the state income tax return. The mandate applies to children and adults, with the family penalty capped at three times the annual adult amount, and the total penalty capped at the statewide average annual bronze plan premium.

| SRP Component | 2026 Amount |

|---|---|

| Per adult (annual) | $695 |

| Per child under 18 | $347.50 |

| Family cap (flat dollar) | $2,085 |

| Income-based alternative | 2.5% of household income above filing threshold |

| Maximum total | NJ statewide average Bronze plan premium |

The SRP is the greater of the flat-dollar amount or the percentage-of-income calculation. Residents report coverage status on Schedule NJ-HCC, attached to Form NJ-1040. Acceptable coverage includes GetCoveredNJ marketplace plans, employer-sponsored plans meeting minimum essential coverage standards, NJ FamilyCare, Medicare, military coverage, and individual market plans purchased off-marketplace that meet the ACA’s December 2017 minimum essential coverage definition. Short-term health insurance does NOT satisfy the mandate and does not exempt buyers from the SRP.

Special Enrollment and the NJ Easy Enrollment Program

Open enrollment for NJ coverage runs annually from November 1 through January 31 — two weeks longer than the federal default of November 1 through January 15. Outside that window, residents need a qualifying life event for a Special Enrollment Period, with one exception unique to New Jersey: the NJ Easy Enrollment Health Insurance Program, which lets uninsured residents trigger enrollment by completing the NJ-EZ Enroll Form on the state income tax return.

| Qualifying Life Event | SEP Window |

|---|---|

| Loss of job-based coverage | 60 days before or after |

| Marriage or civil union | 60 days after |

| Pregnancy | 60 days from start of pregnancy |

| Birth or adoption | 60 days after |

| Permanent move into NJ | 60 days after |

| Aging off parent’s plan at 26 | 60 days before or after |

| NJ Easy Enrollment (NJ-EZ Enroll Form) | Year-round via state tax filing |

Pregnancy as a qualifying event is specific to New Jersey — most state marketplaces and the federal platform do not include pregnancy itself as an SEP trigger. NJ residents who become pregnant outside open enrollment can apply within 60 days of conception, with coverage starting the first day of the month following plan selection. The NJ Easy Enrollment Program, launched in 2022, has connected tens of thousands of uninsured residents to marketplace coverage by automating the SEP process from the state tax return.

How to Choose New Jersey Health Insurance for Your Situation

Marketplace shoppers do better when household profile drives plan selection rather than the other way around. Income band, household composition, network preferences, and how the household actually uses healthcare each shift the right answer. Five household profiles cover most situations encountered on GetCoveredNJ.

Frequently Asked Questions About NJ Coverage

Common questions New Jersey residents ask about health insurance — including how GetCoveredNJ differs from HealthCare.gov, what NJ Health Plan Savings pays, which 2026 carriers are available, how the individual mandate works, and who qualifies for NJ FamilyCare.

What is GetCoveredNJ and how is it different from HealthCare.gov?

GetCoveredNJ is New Jersey’s official state-based health insurance marketplace, operated by the New Jersey Department of Banking and Insurance since 2020. Unlike states that use HealthCare.gov, New Jersey runs its own platform, which lets the state offer a longer open enrollment window (November 1 through January 31), additional state subsidies through NJ Health Plan Savings, and the NJ Easy Enrollment Health Insurance Program for tax-time enrollment.

What is NJ Health Plan Savings and who qualifies?

NJ Health Plan Savings is a state-funded premium subsidy that stacks on top of federal premium tax credits. Households earning up to 600 percent of the federal poverty level qualify — approximately $93,900 for an individual or $192,900 for a family of four in 2026. The state subsidy ranges from $20 to $100 per person per month and is one of the only state programs in the country that extends premium assistance above 400 percent FPL.

Which carriers offer New Jersey health insurance for 2026?

Five carriers sell GetCoveredNJ marketplace plans for 2026: Horizon Blue Cross Blue Shield of New Jersey, AmeriHealth, Oscar, UnitedHealthcare, and Ambetter from WellCare. Aetna exited the New Jersey individual marketplace at the end of 2025. Carriers have different 2026 rate changes: Oscar increased premiums 4.6 percent (the lowest), AmeriHealth 13.5 percent, Horizon 17.0 percent, and UnitedHealthcare 18.4 percent.

Does New Jersey still require health insurance?

Yes. New Jersey is one of a handful of states that maintains an individual health insurance mandate. Residents without minimum essential coverage may owe a Shared Responsibility Payment when filing their state tax return — the greater of $695 per adult ($347.50 per child, with a family cap of $2,085) or 2.5 percent of household income above the filing threshold. The penalty is capped at the statewide average bronze plan premium and is reported on Schedule NJ-HCC of Form NJ-1040.

How much does health insurance cost in New Jersey for 2026?

New Jersey individual marketplace premiums rose an average of 16.6 percent from 2025 to 2026, driven mostly by the expiration of enhanced federal subsidies at the end of 2025. Unsubsidized Silver-tier premiums for a 40-year-old single typically run $485 to $680 per month in 2026 depending on county and carrier. After federal premium tax credits and NJ Health Plan Savings, most households earning under 600 percent FPL pay substantially less.

Who qualifies for NJ FamilyCare in 2026?

NJ FamilyCare is New Jersey’s Medicaid and CHIP program. Children qualify up to 355 percent of the federal poverty level regardless of immigration status — one of the most expansive children’s coverage thresholds in the country. Adults 19 to 64 qualify under the ACA expansion at 138 percent FPL (approximately $1,800 per month for a single adult). Pregnant women qualify up to 205 percent FPL with 12 months of postpartum coverage. New Jersey FamilyCare eligibility rules are scheduled to change starting Fall 2026 with new federal work requirements.

New Jersey Health Insurance Resources

GetCoveredNJ enrollment, open enrollment dates, and plan comparison

Best NJ Health PlansTop-rated 2026 carrier comparisons and plan selection guidance

Individual Health InsuranceACA individual market plans and off-marketplace options for NJ buyers

Self-Employed CoverageTax-advantaged options for NJ freelancers and 1099 workers

Costs & Savings GuidePremium ranges by age and county plus complete NJHPS subsidy guide

Short-Term Health InsuranceTemporary coverage rules and gap-bridging options for NJ residents

New Jersey PPO PlansHorizon PPO and flexible network options across all 21 NJ counties

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required

Enroll in New Jersey Health Insurance for 2026

GetCoveredNJ, NJ Health Plan Savings, and NJ FamilyCare combine to give most New Jersey households access to subsidized coverage. ForHealthInsurance.com runs the eligibility checks, compares all five carriers, and completes enrollment at no extra cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving New Jersey residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.