New Jersey Health Insurance Costs 2026: Premiums, Rate Increases & NJHPS Savings

Health insurance costs in New Jersey rose an average of 16.6 percent for 2026 — the largest single-year increase in the GetCoveredNJ marketplace era. The cause was twofold: enhanced federal premium tax credits expired at the end of 2025, and underlying medical and pharmacy costs continued rising. The state’s NJ Health Plan Savings program, funded at approximately $215 million for 2026, cushions the increase for households up to 600 percent of the federal poverty level — a protection unavailable in most other states. This guide breaks down actual 2026 premium ranges by age, how NJHPS stacks to reduce costs, and what households across every income band actually pay.

What are you looking for?

Why NJ Health Insurance Costs Rose 16.6% in 2026

New Jersey health insurance costs increased 16.6 percent on average for 2026. Enhanced federal premium tax credits expired on December 31, 2025 — credits that had suppressed premiums since 2021 by capping household contributions below what the standard ACA structure produced. Ongoing medical inflation of 6–8 percent annually compounded the effect, pushing premiums higher regardless of the subsidy change.

| Factor | Premium Impact | Who It Affects Most |

|---|---|---|

| Enhanced federal subsidy expiration | +8 to +12 percentage points | Households above 250% FPL most exposed |

| Medical cost inflation | +4 to +6 percentage points | All enrollees equally |

| Pharmacy cost increases | +2 to +4 percentage points | All enrollees equally |

| Aetna exit — market concentration | Modest upward pressure | Concentrated in Aetna-dominant counties |

| NJ Health Plan Savings offset | −$20 to −$100/person/mo | Households up to 600% FPL |

The practical effect of the subsidy expiration was immediate and visible in enrollment data. The percentage of GetCoveredNJ enrollees paying $10 or less per month dropped from 48 percent in 2025 to 11 percent in 2026. Approximately 70,000 New Jersey residents dropped coverage between January 31 and April 15, 2026, primarily due to inability to pay the higher post-expiration premiums. New Jersey’s NJHPS cushioned this for some households — but could not fully replace the federal enhanced credit value that expired nationally.

2026 NJ Health Insurance Premium Ranges by Age

Premium pricing follows ACA age-rating rules — carriers can charge older adults up to three times what they charge younger adults for the same plan at the same tier. Premium ranges below reflect typical 2026 Silver plan pricing across NJ carriers and rating areas before any subsidy. Actual premiums vary by county, carrier, specific plan, and tobacco use status.

| Age | Silver Monthly (Unsubsidized) | Bronze Monthly | Gold Monthly |

|---|---|---|---|

| 25 | $370–$480 | $280–$370 | $490–$640 |

| 30 | $420–$550 | $320–$420 | $560–$730 |

| 40 | $485–$680 | $370–$520 | $640–$900 |

| 50 | $695–$960 | $530–$730 | $920–$1,270 |

| 55 | $870–$1,200 | $660–$910 | $1,150–$1,590 |

| 60 | $1,050–$1,440 | $800–$1,100 | $1,390–$1,910 |

| Family of 4 (parents 40) | $1,650–$2,200 | $1,260–$1,680 | $2,180–$2,910 |

These unsubsidized premiums are the starting point, not the ending point. Almost all New Jersey marketplace enrollees qualify for federal premium tax credits, NJ Health Plan Savings, or both. Eight in ten households who enroll through GetCoveredNJ qualify for financial assistance. The NJ Department of Banking and Insurance publishes annual rate filings confirming carrier-level increases. The unsubsidized premium matters primarily for households above 600 percent FPL and for off-marketplace buyers who forfeit subsidy access entirely.

NJ Health Plan Savings: The State Subsidy That Changes the Math

NJ Health Plan Savings is the feature that makes New Jersey health insurance costs meaningfully different from most other states. The $20 to $100 per person per month state subsidy stacks on top of federal Advance Premium Tax Credits through GetCoveredNJ. The 600 percent FPL ceiling — compared to the federal 400 percent baseline — means households earning up to $192,900 for a family of four receive state subsidy even when federal credits have phased out.

$400

Max monthly NJHPS for a family of four at 300% FPL

$4,800

Annual savings for the same family from NJHPS alone

600%

FPL ceiling for NJHPS — vs 400% for federal APTC

| Household Income | FPL Band | Federal APTC | NJHPS/person/mo | Combined Monthly Help |

|---|---|---|---|---|

| $24,860 (single) | ~138% FPL | Large (near-zero premium) | $20–$40 | Near-zero premium Silver |

| $37,000 (single) | ~200% FPL | Significant | $40–$60 | $60–$120/mo after both |

| $62,600 (single) | ~340% FPL | Moderate | $80–$100 | $180–$320/mo after both |

| $75,000 (single) | ~405% FPL | Minimal or none | $60–$100 | NJHPS only — still meaningful |

| $93,900 (single) | ~508% FPL | None | $20–$60 | NJHPS only |

| Over $93,900 (single) | Over 600% FPL | None | Not eligible | Full premium |

The 400-to-600 percent FPL bracket is where New Jersey health insurance costs deviate most sharply from other states. A single New Jersey resident earning $80,000 — above the standard federal APTC phase-out for most plan selections — pays full unsubsidized premiums in states without state supplement programs. In New Jersey, that same resident receives $60–100 per month in NJHPS, reducing a $600 monthly unsubsidized Silver premium to $500–540 after state assistance. The math scales for families: a household of four at 450 percent FPL earning $140,000 receives up to $400 per month in NJHPS that would be unavailable in any other state market at that income level.

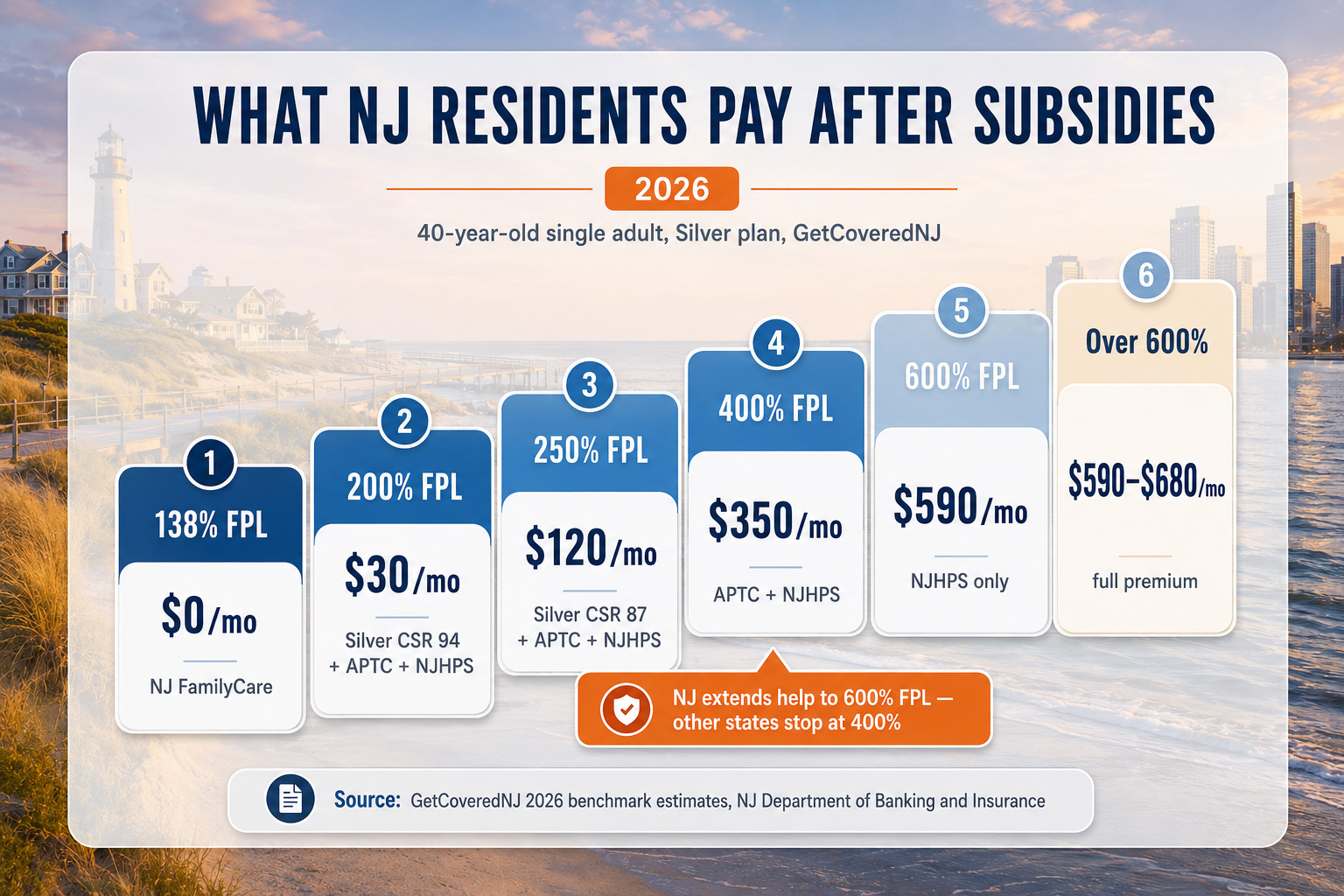

What NJ Residents Actually Pay After Subsidies

Costs after federal APTC and NJ Health Plan Savings produce a very different picture from gross premiums for New Jersey residents. The table below shows typical after-subsidy monthly costs for a 40-year-old single adult at various income levels, using Silver plan pricing as the benchmark tier and assuming enrollment on GetCoveredNJ where both subsidy streams apply.

Affordability Snapshot: What New Jersey Residents Actually Pay

Gross Silver premiums for a 40-year-old run $485 to $680 per month across NJ counties. After federal APTC and NJ Health Plan Savings, a single adult at 138–200 percent FPL ($21,597–$30,120) pays $0 to $60, and at 200–250 percent FPL pays $60 to $180. Below $21,597, NJ FamilyCare covers the household at no premium. NJHPS is what extends help all the way to 600 percent FPL — well past the federal cliff.

| Annual Income (Single) | FPL % | Gross Silver Premium | After APTC + NJHPS | Best Tier Choice |

|---|---|---|---|---|

| Under $21,597 | Under 138% | $485–$680 | $0 (NJ FamilyCare) | Medicaid — no marketplace |

| $21,597–$30,120 | 138%–200% | $485–$680 | $0–$60 | Silver CSR 94 |

| $30,120–$37,650 | 200%–250% | $485–$680 | $60–$180 | Silver CSR 87 |

| $37,650–$62,160 | 250%–400% | $485–$680 | $160–$380 | Silver or Gold |

| $62,160–$93,900 | 400%–600% | $485–$680 | $390–$620 (NJHPS only) | Silver or Gold |

| Over $93,900 | Over 600% | $485–$680 | $485–$680 (full premium) | Gold or off-marketplace |

See Your Actual NJ Health Insurance Cost for 2026

Gross premiums are just the starting point. A licensed New Jersey agent calculates your exact after-APTC and after-NJHPS monthly cost across all five carriers and identifies which plan tier produces the lowest total annual expense for your household.

How Metal Tier Choice Affects Total NJ Health Insurance Costs

The metal tier decision is the single largest cost variable within any given income band. Cost differences between Bronze and Silver CSR exceed the gaps between most carrier options at the same tier. The right tier depends on how much healthcare the household expects to use — and most shoppers systematically underestimate this, leading to the Bronze-over-Silver mistake that drove the 2026 enrollment shift. Households weighing network breadth alongside tier should also review the New Jersey PPO health insurance cost comparison.

| Income Band | Bronze Annual Total* | Silver (+ CSR) Annual Total* | Gold Annual Total* |

|---|---|---|---|

| 138%–200% FPL | $360–$960 + $7,000+ deductible | $0–$720 + $100–$400 deductible | Not recommended (CSR unavailable on Gold) |

| 200%–250% FPL | $1,200–$2,400 + $7,000+ deductible | $720–$2,160 + $1,500–$2,500 deductible | $2,400–$3,600 + $1,000–$2,500 deductible |

| 250%–400% FPL | $2,400–$4,800 + $7,000+ deductible | $1,920–$4,560 + $4,500–$6,000 deductible | $4,800–$7,200 + $1,000–$2,500 deductible |

*Totals represent premium costs only. Actual total annual cost depends on healthcare usage, which determines whether and how much of the deductible and out-of-pocket maximum is reached.

⚠️ The Bronze trap in 2026

New Jersey saw Bronze selections nearly double from 16 to 31 percent in 2026 as households tried to offset higher premiums. For households at 138–250 percent FPL eligible for Silver CSR, this is almost always the wrong move. A Silver CSR 94 plan has a $100–400 deductible versus Bronze’s $7,000–9,000 — a single urgent care visit, prescription refill, or routine lab test erases any annual premium savings from Bronze. Households in this income band should compare Silver CSR specifically, not standard Silver.

Regional Cost Variation Across NJ Counties

Premium costs vary by geographic rating area across New Jersey — the state groups counties into rating zones that reflect local healthcare cost structures. Premium variation statewide is modest compared to states like Texas or Florida, typically ranging within 10 to 15 percent between the lowest and highest rating areas. Urban North Jersey counties tend toward the lower end; rural South Jersey counties tend slightly higher.

| Region | Key Counties | Premium Tier vs State Average | Carrier Availability |

|---|---|---|---|

| North Jersey | Bergen, Hudson, Essex, Union | At or slightly below average | All 5 carriers |

| Central Jersey | Mercer, Middlesex, Monmouth, Somerset | Near state average | All 5 carriers (most areas) |

| Jersey Shore | Ocean, Monmouth coastal | Slightly above average | Horizon, AmeriHealth, Oscar (select) |

| South Jersey | Camden, Burlington, Atlantic | Near average; AmeriHealth competitive | Horizon, AmeriHealth strong |

| Rural South Jersey | Salem, Cumberland, Cape May | Slightly above average | Horizon primary; others limited |

County-level carrier availability is the most important regional factor. Oscar does not operate in all NJ counties — its 4.6 percent rate increase advantage is only accessible to households in counties where Oscar participates. Similarly, AmeriHealth’s competitive family-plan pricing in South Jersey is only relevant for households in AmeriHealth’s service area. GetCoveredNJ shows county-specific carrier availability automatically during the enrollment flow, filtering to only plans available at the household’s ZIP code.

Strategies to Lower NJ Health Insurance Costs

Coverage costs in New Jersey are most effectively reduced through four strategies — all of which work within the GetCoveredNJ framework and stack with NJHPS where applicable. The right combination depends on household income, expected healthcare use, and provider priorities.

Frequently Asked Questions About NJ Health Insurance Costs

Common questions about New Jersey health insurance costs for 2026 — covering the 16.6 percent premium increase, how NJ Health Plan Savings reduces monthly costs, Silver plan pricing by age, the 400–600 percent FPL state subsidy extension, county-level premium variation, and Bronze vs Silver total annual value.

How much did NJ health insurance cost go up in 2026?

New Jersey individual market premiums rose an average of 16.6 percent from 2025 to 2026. The increase was driven primarily by the expiration of enhanced federal premium tax credits at the end of 2025 and rising medical and pharmacy costs. Rate changes varied by carrier: Oscar increased 4.6 percent, AmeriHealth 13.5 percent, Horizon 17.0 percent, and UnitedHealthcare 18.4 percent. For households with income below 400 percent FPL, NJ Health Plan Savings and federal APTC offset much of the gross increase.

What is NJ Health Plan Savings and how much does it reduce costs?

NJ Health Plan Savings is a state-funded premium subsidy of $20 to $100 per person per month that stacks on top of federal Advance Premium Tax Credits. Households earning up to 600 percent of the federal poverty level qualify — approximately $93,900 for an individual or $192,900 for a family of four in 2026. For a family of four at 300 percent FPL, NJHPS alone can reduce premiums by up to $400 per month, saving $4,800 annually.

What does a Silver plan cost in New Jersey for 2026?

Unsubsidized Silver plan premiums in New Jersey for 2026 range from approximately $420 to $550 per month for a 30-year-old single adult, $485 to $680 for a 40-year-old, $695 to $960 for a 50-year-old, and $1,050 to $1,440 for a 60-year-old. Family of four premiums run $1,650 to $2,200 per month. After federal premium tax credits and NJ Health Plan Savings, most households under 400 percent FPL pay substantially less — often under $200 per month for individuals and under $500 for families.

Does New Jersey have state subsidies for health insurance above 400% FPL?

Yes. New Jersey Health Plan Savings extends state subsidy eligibility to 600 percent of the federal poverty level — approximately $93,900 for an individual or $192,900 for a family of four in 2026. This means households between 400 and 600 percent FPL who receive no federal premium tax credits can still receive $20 to $100 per person per month in state subsidy through GetCoveredNJ. This is one of the most generous state supplements in the country.

Are NJ health insurance premiums different by county?

Yes. New Jersey uses geographic rating areas that group counties into rating zones. Premiums vary modestly by rating area — typically within a 10 to 15 percent range statewide. Urban North Jersey counties (Hudson, Essex, Bergen) tend toward the lower end of the range due to larger risk pools. Rural South Jersey counties (Salem, Cumberland, Cape May) tend slightly higher. The difference matters when comparing carrier options county by county on GetCoveredNJ.

Is Bronze cheaper than Silver in New Jersey after subsidies?

Bronze has a lower monthly premium than Silver, but for households below 250 percent FPL, Silver with cost-sharing reductions almost always produces better total annual value than Bronze. Silver CSR reduces deductibles from the $7,000–9,000 range down to $100–400 for households at 138–200 percent FPL. Any household who uses healthcare at all during the year will almost certainly save more in lower out-of-pocket costs with Silver CSR than the premium difference would suggest.

Related New Jersey Health Insurance Resources

Explore the rest of the New Jersey coverage library — the statewide overview, the GetCoveredNJ marketplace, carrier comparisons, and individual plan options.

Complete 2026 overview — carriers, FamilyCare, mandate, and subsidy paths.

GetCoveredNJ MarketplaceEnrollment steps, NJ Health Plan Savings, and the Easy Enrollment Program.

Best NJ Health PlansFive-carrier comparison with 2026 rate changes and OMNIA network guide.

Individual Health InsuranceACA individual market plans, mandate rules, and enrollment pathways.

Calculate Your 2026 NJ Health Insurance Cost

NJ Health Plan Savings, federal APTC, and the right metal tier combine differently for every household. ForHealthInsurance.com’s licensed New Jersey agents calculate your exact after-subsidy cost across all five carriers and identify the plan with the lowest total annual exposure — at no extra cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving New Jersey residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.