Self-Employed Health Insurance New Jersey 2026: NJHPS, Tax Deductions & HSA Strategies

Self-employed health insurance in New Jersey for 2026 has a specific financial advantage unavailable to freelancers in most other states. New Jersey’s Health Plan Savings program extends state subsidies to 600 percent of the federal poverty level — approximately $93,900 for a single adult — meaning self-employed residents with higher 1099 incomes that push them above the federal APTC ceiling still receive meaningful state premium assistance through GetCoveredNJ. That NJHPS subsidy stacks with the federal Self-Employed Health Insurance Deduction on Schedule 1, producing a compounding tax benefit. This guide covers every coverage path, the deduction mechanics, and the HSA pairing strategies that matter most for NJ self-employed filers.

What are you looking for?

Understand the Schedule SE deduction

How NJHPS and the deduction stack together

See deduction rules ↓Coverage Paths for Self-Employed NJ Residents

Self-employed health insurance in New Jersey follows the same two paths as individual coverage — GetCoveredNJ on-exchange and off-exchange ACA-compliant — with one key addition: the NJ mandate applies to self-employed residents just as it does to employees. Most self-employed NJ residents below 600 percent of the federal poverty level should start at GetCoveredNJ to access both federal premium tax credits and the NJ Health Plan Savings state subsidy.

| Self-Employed Profile | Best Coverage Path | Subsidy Available |

|---|---|---|

| Net income under $21,597 (138% FPL) | NJ FamilyCare (Medicaid) | State-funded, free |

| Net income $21,597–$62,160 (138–400% FPL) | GetCoveredNJ + APTC + NJHPS | Federal + state combined |

| Net income $62,160–$93,900 (400–600% FPL) | GetCoveredNJ + NJHPS only | State only (no federal APTC) |

| Net income over $93,900 (600%+ FPL) | GetCoveredNJ or off-exchange | None — full premium |

| S-corp owner (W-2 wage earner) | Company plan or GetCoveredNJ | APTC + NJHPS if not employer-eligible |

Net self-employment income — not gross revenue — determines FPL placement and subsidy eligibility. A freelance designer with $120,000 in revenue and $35,000 in deductible business expenses has a net self-employment income of $85,000, placing the household at approximately 457 percent of FPL as a single adult and within the NJHPS-eligible range. The NJ Department of Banking and Insurance publishes annual plan availability data confirming carrier and tier options for self-employed buyers. Understanding net income before projecting subsidy eligibility prevents significant missteps in coverage planning.

The NJ NJHPS Advantage for Self-Employed Filers

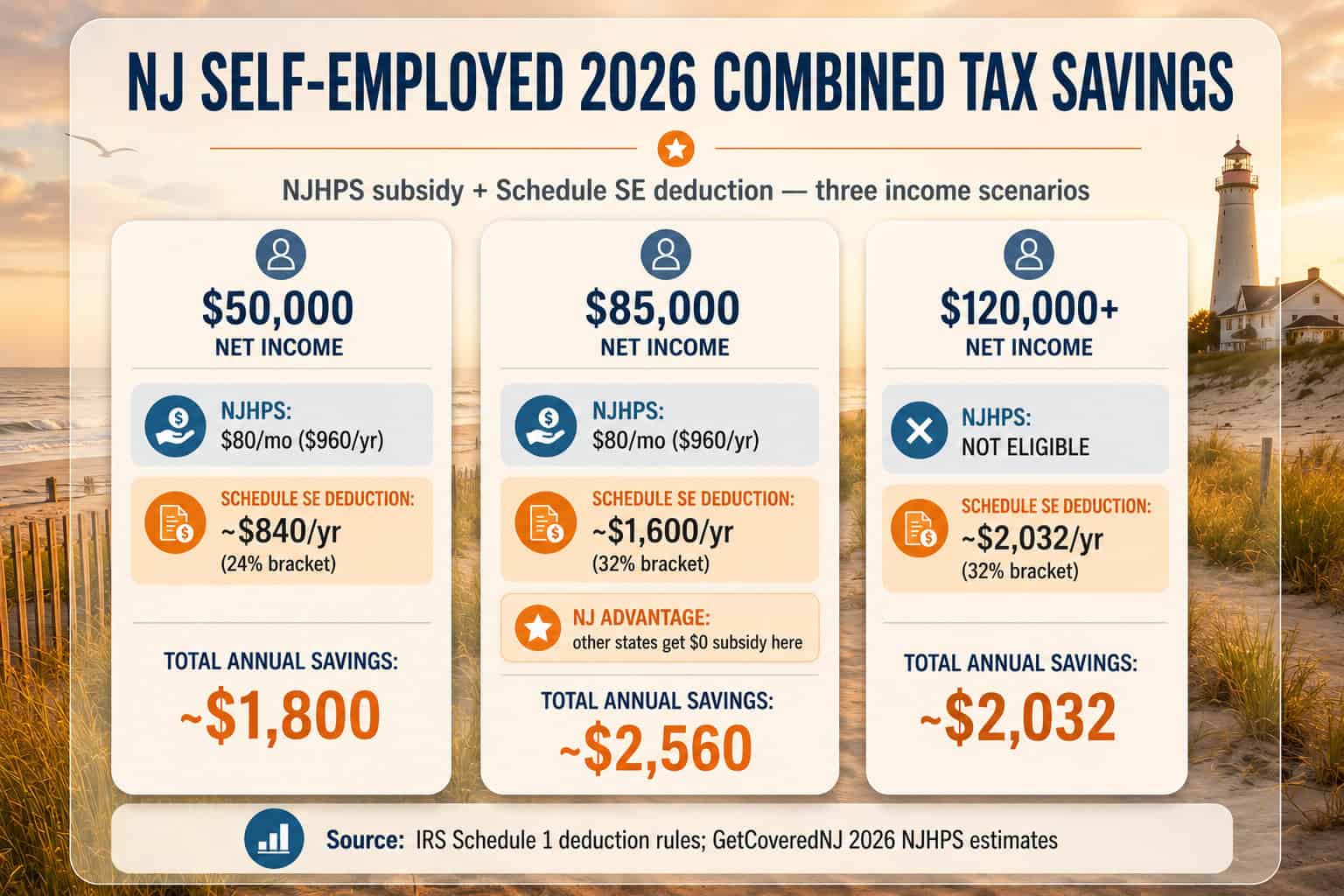

Self-employed health insurance buyers in New Jersey benefit more from the NJHPS state subsidy than residents of almost any other state. The 600 percent FPL ceiling — compared to the federal 400 percent APTC phase-out — means self-employed NJ residents with variable or higher income continue to receive state premium assistance even when federal credits disappear. This matters particularly for 1099 workers whose income fluctuates across FPL thresholds year to year.

| Annual Net Income (Single) | Federal APTC | NJHPS/mo | Schedule SE Deduction Also Available? |

|---|---|---|---|

| $35,000 (~190% FPL) | Large | $20–$40 | Yes — on net premium after subsidies |

| $50,000 (~270% FPL) | Moderate | $60–$100 | Yes — on net premium after subsidies |

| $70,000 (~378% FPL) | Reduced | $80–$100 | Yes — more valuable as gross deduction rises |

| $85,000 (~460% FPL) | Minimal/none | $60–$100 | Yes — NJHPS + deduction working together |

| $110,000 (~595% FPL) | None | $20–$40 | Yes — deduction most valuable at this income |

| $120,000+ (600%+ FPL) | None | Not eligible | Yes — full premium deductible |

The $85,000–110,000 net income band is where New Jersey’s advantage over other states is most pronounced. A NJ freelancer at $90,000 net income receives $60–100 per month in NJHPS that would be unavailable in states without a supplement program — savings of $720–1,200 per year that stack directly on top of the Schedule 1 deduction. In most other states, this income level produces no subsidy and the deduction applies to the full gross premium.

The Self-Employed Health Insurance Deduction in New Jersey

The Self-Employed Health Insurance Deduction is an above-the-line federal tax deduction available to sole proprietors, partners, and S-corp owner-employees who are not eligible for employer-subsidized coverage through a spouse’s plan. The deduction reduces federal adjusted gross income on Schedule 1, Line 17 of Form 1040 — and because NJ taxable income tracks federal AGI in many respects, the deduction also reduces state income tax liability.

| Scenario | Gross Monthly Premium | After NJHPS + APTC | Annual Deduction |

|---|---|---|---|

| 200% FPL, Silver CSR | $530 | $40/mo | $480 |

| 300% FPL, Silver | $530 | $180/mo | $2,160 |

| 460% FPL, Silver (NJHPS only) | $530 | $430/mo | $5,160 |

| 600%+ FPL, no subsidy | $530 | $530/mo (full) | $6,360 |

| Family plan, 300% FPL | $1,800 | $560/mo | $6,720 |

Calculate Your NJ Self-Employed Coverage Cost for 2026

NJHPS, APTC, and the Schedule SE deduction produce different outcomes at every income level. A licensed NJ broker calculates net premium, identifies the optimal tier and carrier, and completes GetCoveredNJ enrollment — at no extra cost.

HSA Pairing for NJ Self-Employed Filers Above Subsidy Thresholds

Self-employed NJ residents above the 600 percent FPL NJHPS ceiling — or those who prefer maximum out-of-pocket protection and tax efficiency over subsidy optimization — often benefit from combining an HSA-eligible High-Deductible Health Plan with maximum Health Savings Account contributions. The triple tax benefit of an HSA compounds with the Schedule SE deduction for self-employed filers in high marginal brackets.

| HSA Component | 2026 Amount | Tax Treatment |

|---|---|---|

| HSA contribution limit (self-only) | $4,400 | Deductible on federal return; NJ-exempt |

| HSA contribution limit (family) | $8,750 | Deductible on federal return; NJ-exempt |

| HDHP minimum deductible (self-only) | $1,700 | Required for HSA eligibility |

| HDHP minimum deductible (family) | $3,400 | Required for HSA eligibility |

| HSA investment growth | Tax-free | No federal or NJ state tax on growth |

| HSA withdrawals for medical | Tax-free | No tax on qualifying withdrawals |

For a self-employed NJ resident at $120,000 net income in the 32 percent federal bracket, the HDHP-plus-HSA math is compelling. Maximum HSA contribution of $4,400 produces $1,408 in federal tax savings immediately, plus the HDHP premium itself runs substantially lower than Gold or Silver plans. Combined with the Schedule SE deduction on the HDHP premium, total first-year tax savings from coverage alone can exceed $3,000 — before any actual healthcare use.

Variable Income Planning for NJ Self-Employed Buyers

Variable income is the defining challenge for self-employed health insurance planning in New Jersey. APTC and NJHPS are calculated on estimated annual income declared at enrollment — if actual income ends up significantly higher, excess credits must be repaid at tax time. Two proactive habits reduce this risk substantially.

Plan Selection for NJ Self-Employed Buyers

Plan selection for self-employed NJ buyers follows standard carrier and tier logic, with one additional factor: the interaction between tier and the Schedule SE deduction. Higher premiums from Gold or OMNIA increase the deduction amount at higher marginal rates — while Bronze’s lower premium produces a smaller deduction. The optimal tier minimizes total annual cost (premium + deductible used), not just the lowest monthly payment.

NJ Mandate Compliance for Self-Employed Residents

Self-employed health insurance in New Jersey must satisfy the state individual mandate, just like coverage for employees. The NJ Health Insurance Market Preservation Act requires all NJ residents — including sole proprietors, freelancers, and 1099 contractors — to carry minimum essential coverage or owe the Shared Responsibility Payment. GetCoveredNJ plans, off-exchange ACA-compliant plans, and NJ FamilyCare all satisfy the mandate.

| Income Level | SRP (Annual) | Comparison: Subsidized Silver Premium |

|---|---|---|

| $30,000 (~160% FPL) | $695 (flat dollar wins) | ~$240/yr after subsidies |

| $50,000 (~270% FPL) | ~$875 (2.5% of income above threshold) | ~$1,200/yr after subsidies |

| $80,000 (~432% FPL) | ~$1,575 (2.5% of income above threshold) | ~$4,800/yr (NJHPS only) |

| $120,000 (~649% FPL) | ~$2,575 (capped at avg Bronze premium) | ~$6,360/yr (full premium, but fully deductible) |

Coverage is almost always cheaper than the SRP for self-employed NJ residents with any meaningful income. At $80,000 net income, the SRP is approximately $1,575 — but subsidized coverage through GetCoveredNJ with NJHPS runs roughly $4,800 annually. The penalty doesn’t make coverage “not worth it” — it makes going uninsured cheaper than being insured, but only before accounting for healthcare expenses the uninsured resident would pay entirely out-of-pocket. The expected value of coverage almost always exceeds both the premium and the penalty.

Frequently Asked Questions About NJ Self-Employed Health Insurance

Common questions from self-employed New Jersey residents — covering subsidy eligibility, how the Schedule SE deduction works, stacking NJHPS with the deduction, HSA compatibility with GetCoveredNJ plans, variable income planning, and the NJ mandate for freelancers and 1099 workers.

Can self-employed New Jersey residents get subsidized health insurance?

Yes. Self-employed NJ residents who purchase coverage through GetCoveredNJ qualify for federal Advance Premium Tax Credits based on household income and NJ Health Plan Savings — the state subsidy that extends to 600 percent of the federal poverty level, approximately $93,900 for a single adult in 2026. Both subsidies are available regardless of whether the health insurance premium is also deducted on Schedule 1 of the federal tax return as the Self-Employed Health Insurance Deduction.

How does the self-employed health insurance tax deduction work in New Jersey?

Self-employed NJ residents — sole proprietors, partners, and S-corp owner-employees — can deduct health insurance premiums as an above-the-line adjustment on the federal tax return using Schedule 1, Line 17. The deduction reduces federal adjusted gross income and New Jersey state taxable income, lowering both federal and NJ state income tax liability. The deduction applies whether the plan is purchased on GetCoveredNJ or off-exchange, and whether or not premium tax credits are also claimed.

Can I get both NJHPS subsidies and the self-employed health insurance deduction?

Yes, with an important interaction to understand. The Self-Employed Health Insurance Deduction applies to the net premium paid after subsidies — meaning the deduction covers the out-of-pocket premium remaining after federal APTC and NJHPS reduce the bill. A self-employed NJ resident paying $200 per month after subsidies deducts $2,400 annually on Schedule 1, not the $600 gross monthly premium. Both the subsidy and the deduction work together to reduce total coverage cost.

Is an HSA compatible with GetCoveredNJ marketplace plans?

Yes, if the marketplace plan qualifies as a High-Deductible Health Plan under IRS rules — a deductible of at least $1,700 for self-only coverage or $3,400 for family coverage in 2026. GetCoveredNJ offers HDHP-eligible plans from several carriers. HSA contributions reduce federal taxable income, are exempt from New Jersey state income tax, and grow tax-free. For self-employed NJ residents above the NJHPS subsidy threshold, the HDHP plus HSA combination can produce substantial compound tax savings.

What if my self-employment income varies year to year?

Variable income is the most important planning consideration for self-employed NJ residents on GetCoveredNJ. Premium tax credits and NJHPS are based on estimated annual income declared at enrollment. If actual income ends up higher than estimated, excess credits must be repaid at tax time. If income falls lower, additional credits are refunded. Self-employed NJ residents should update their income estimates on GetCoveredNJ whenever there is a significant change during the year to keep subsidies accurate and avoid a large year-end reconciliation.

Does the NJ individual mandate apply to self-employed residents?

Yes. The NJ individual health insurance mandate applies to all New Jersey residents including the self-employed, freelancers, and 1099 contractors. Self-employed residents who go without minimum essential coverage owe the Shared Responsibility Payment — the greater of $695 per adult or 2.5 percent of household income above the filing threshold, capped at the statewide average Bronze plan premium. Coverage purchased on GetCoveredNJ or off-exchange satisfies the mandate.

New Jersey Health Insurance Resources

Complete 2026 overview — carriers, FamilyCare, mandate, and all subsidy paths

GetCoveredNJ MarketplaceEnrollment steps, NJHPS stacking, and the NJ Easy Enrollment Program

Best NJ Health PlansFive-carrier comparison with 2026 rate changes and OMNIA network guide

Individual Health InsuranceACA individual market plans, mandate rules, and enrollment paths for NJ buyers

Costs & Savings GuidePremium ranges by age and county with the full NJHPS subsidy guide

Short-Term Health InsuranceGap coverage rules, mandate implications, and marketplace alternatives

New Jersey PPO PlansHorizon PPO and OMNIA for NJ residents needing cross-state coverage

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required

Find the Best Self-Employed NJ Coverage for 2026

NJHPS, the Schedule SE deduction, and HSA pairing produce different outcomes at every income level. ForHealthInsurance.com’s licensed NJ brokers calculate the full picture — subsidy eligibility, net premium, and deduction value — and complete GetCoveredNJ enrollment at no extra cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving New Jersey residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.