Individual Health Insurance New Jersey 2026: ACA Plans, Subsidies & Enrollment

Individual health insurance in New Jersey for 2026 means navigating a state that operates its own marketplace, requires residents to carry coverage under a state mandate, and offers a state subsidy program that extends financial help further up the income ladder than any federal equivalent. New Jersey’s GetCoveredNJ marketplace hosts five carriers following Aetna’s exit at the end of 2025. This guide walks through every path available to NJ individuals — on-exchange plans with NJHPS, off-exchange ACA-compliant options, and the mandate rules that apply regardless of which path is chosen.

What are you looking for?

Individual Health Insurance Options in NJ for 2026

Individual health insurance in New Jersey for 2026 comes through two primary channels — on-exchange through GetCoveredNJ, and off-exchange directly from carriers. The distinction matters because only GetCoveredNJ plans qualify for federal premium tax credits and NJ Health Plan Savings. Individuals who purchase coverage directly from carriers — even for identical plan designs — forfeit both subsidy streams and pay full unsubsidized premiums.

| Coverage Path | Subsidy Eligible | Plan Tiers Available | Carrier Options |

|---|---|---|---|

| GetCoveredNJ (on-exchange) | Yes — APTC + NJHPS | Bronze, Silver, Gold | 5 carriers |

| Off-exchange ACA-compliant | No | Bronze, Silver, Gold, Platinum | Horizon + select nationals |

| NJ FamilyCare (Medicaid) | N/A — state-funded | Comprehensive (no tiers) | NJ FamilyCare contractors |

| Short-term coverage | No — and doesn’t satisfy mandate | Limited (not ACA-compliant) | Specialty carriers only |

For individuals below 600 percent of the federal poverty level — approximately $93,900 in annual income for a single adult in 2026 — GetCoveredNJ is almost always the right starting point. The platform automatically calculates both federal Advance Premium Tax Credits and NJ Health Plan Savings simultaneously, showing the household’s actual net premium rather than the carrier’s gross price. For individuals above 600 percent FPL, off-exchange plans become competitive if the household wants Platinum-tier coverage or a specific carrier not available on the marketplace.

The NJ Individual Mandate and Why It Matters

Individual health insurance in New Jersey is not optional — the state has maintained a mandate since 2019 under the NJ Health Insurance Market Preservation Act. Residents who go uninsured without a qualifying exemption owe a Shared Responsibility Payment on their state tax return. New Jersey is one of a small number of states — alongside California, Massachusetts, Rhode Island, and DC — that still require coverage after the federal penalty was eliminated in 2019.

| SRP Component | 2026 Amount | Applies To |

|---|---|---|

| Per adult | $695 annually | Each uninsured adult in household |

| Per child under 18 | $347.50 annually | Each uninsured dependent |

| Family maximum (flat dollar) | $2,085 | Aggregate household cap |

| Income-based alternative | 2.5% of household income above filing threshold | Whichever is greater |

| Absolute maximum | NJ statewide average Bronze plan premium | Cap on total SRP |

NJ Health Plan Savings for Individual Buyers

NJ Health Plan Savings gives individual New Jersey buyers a financial advantage unavailable in most other states. The $20 to $100 per person per month state subsidy stacks on top of federal Advance Premium Tax Credits through GetCoveredNJ. For individuals between 400 and 600 percent FPL where federal credits phase out, NJHPS is often the only subsidy keeping coverage affordable — a single adult earning $80,000 receives $60–100 per month in state savings unavailable elsewhere.

| Annual Income (Single Adult) | FPL % | Federal APTC | NJHPS/mo | Effective Monthly Premium |

|---|---|---|---|---|

| Under $21,597 | Under 138% | N/A | N/A | NJ FamilyCare — $0 |

| $21,597–$30,120 | 138%–200% | Large | $20–$40 | $0–$60 (Silver CSR 94) |

| $30,120–$37,650 | 200%–250% | Significant | $40–$60 | $60–$180 (Silver CSR 87) |

| $37,650–$62,160 | 250%–400% | Moderate | $60–$100 | $160–$380 (Silver or Gold) |

| $62,160–$93,900 | 400%–600% | Minimal/none | $20–$100 | $385–$620 (NJHPS only) |

| Over $93,900 | Over 600% | None | Not eligible | $485–$680 (full premium) |

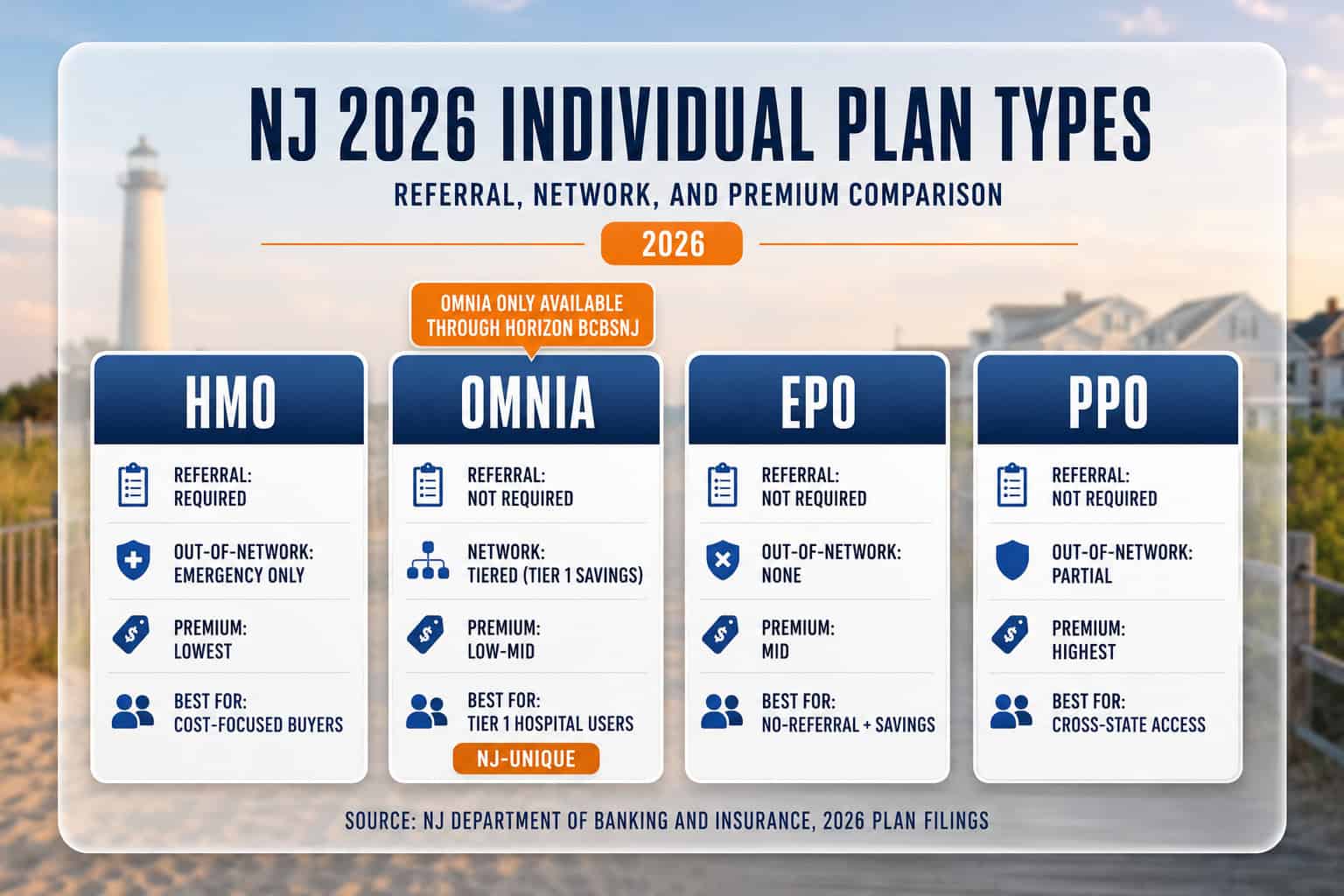

Choosing an Individual Plan Type in New Jersey

Individual health insurance plan types in New Jersey span HMO, PPO, EPO, OMNIA tiered, POS, and Direct Access — each with different referral requirements, out-of-network coverage, and premium implications. Most individual buyers on GetCoveredNJ choose between HMO (lowest premium, referral required) and OMNIA (no referral, Tier 1 hospital savings). PPO is available primarily through Horizon for individuals who need cross-state or out-of-network coverage.

| Plan Type | Referral Required | Out-of-Network | Premium Level | Best For |

|---|---|---|---|---|

| HMO | Yes (PCP) | Emergency only | Lowest | Cost-focused, NJ-anchored |

| OMNIA (Horizon) | No | Tier 1/2 only | Low-mid | Tier 1 hospital users |

| EPO | No | None | Mid | No-referral + lower than PPO |

| POS | Yes for out-of-network | Partial with referral | Mid | PCP coordination + some flexibility |

| PPO | No | Partial | Highest | Cross-state, NYC/Philly access |

For most individual buyers, the decision narrows to HMO versus OMNIA. Both are available through Horizon on GetCoveredNJ, and OMNIA’s no-referral access combined with Tier 1 hospital savings makes it a compelling upgrade from HMO at a small premium difference. Individuals who see specialists frequently without going through a PCP — a common preference among younger adults and those managing chronic conditions — consistently find OMNIA or EPO preferable to HMO despite the modest premium increase.

Find Your Individual NJ Health Plan for 2026

Matching plan type, carrier, and tier to your income and provider preferences takes a side-by-side comparison. A licensed NJ broker confirms NJHPS eligibility, compares all five carriers, and completes GetCoveredNJ enrollment at no extra cost.

Individual Coverage for Specific NJ Buyer Profiles

Individual health insurance needs in New Jersey differ significantly across buyer types — the freelancer above 400 percent FPL, the recent college graduate, the self-employed professional, and the early retiree each face different cost structures and enrollment considerations. Matching the right coverage path to the household situation avoids paying for flexibility never used or carrying gaps that trigger the mandate penalty.

How to Enroll in Individual NJ Health Insurance

Individual health insurance enrollment in New Jersey follows structured pathways — the standard open enrollment window, special enrollment periods for qualifying life events, and the state-unique NJ Easy Enrollment Health Insurance Program via the state tax return. Each pathway has different documentation requirements and effective date rules that affect when coverage actually starts.

| Enrollment Path | When Available | Coverage Start | NJ-Specific? |

|---|---|---|---|

| Open enrollment | Nov 1 – Jan 31 annually | Jan 1 (if by Dec 31) or Feb 1 (if Jan) | NJ has longer window than federal |

| Loss of job-based coverage SEP | 60 days before/after loss | First of month following selection | No (federal standard) |

| Pregnancy SEP | 60 days from start of pregnancy | First of month following selection | Yes — NJ only |

| Marriage SEP | 60 days after event | First of month following selection | No (federal standard) |

| NJ Easy Enrollment Program | Year-round via state tax return | Varies — contact GetCoveredNJ | Yes — NJ only |

The NJ Easy Enrollment Program is the most distinctive individual enrollment feature in the state. Residents who file the NJ-1040 state income tax return and indicate household members lack coverage can complete the NJ-EZ Enroll Form to trigger a special enrollment period — no qualifying life event required. The NJ Treasury health insurance mandate page confirms that uninsured residents who take the Easy Enrollment path and enroll in coverage avoid the Shared Responsibility Payment for months following their enrollment.

Common Individual Coverage Mistakes in NJ

Four mistakes consistently produce worse outcomes for individual health insurance buyers in New Jersey — each reflects a reasonable instinct applied without accounting for NJ-specific rules around the mandate, NJHPS, and the Silver CSR interaction.

Frequently Asked Questions About Individual NJ Health Insurance

Common questions about individual health insurance in New Jersey — covering available options for 2026, the state mandate and SRP penalty, how NJHPS reduces individual costs, on-exchange vs off-exchange differences, year-round enrollment paths, and which metal tier is best by income band.

What individual health insurance options are available in New Jersey for 2026?

New Jersey residents shopping for individual health insurance in 2026 have two primary paths: on-exchange plans through GetCoveredNJ, the state-based marketplace, and off-exchange ACA-compliant plans purchased directly from carriers. GetCoveredNJ offers five carriers — Horizon BCBSNJ, AmeriHealth, Oscar, UnitedHealthcare, and Ambetter — with access to federal premium tax credits and NJ Health Plan Savings subsidies up to 600 percent FPL. Off-exchange plans forfeit subsidy access but may offer broader plan types including Platinum tier.

Is individual health insurance required in New Jersey?

Yes. New Jersey has maintained an individual health insurance mandate since 2019 under the NJ Health Insurance Market Preservation Act. Residents who go without minimum essential coverage and do not qualify for an exemption owe a Shared Responsibility Payment on their NJ state income tax return — the greater of $695 per adult or 2.5 percent of household income, capped at the statewide average Bronze plan premium. The mandate makes NJ one of a small number of states that still require coverage.

How does NJ Health Plan Savings affect individual health insurance costs?

NJ Health Plan Savings reduces individual health insurance premiums on GetCoveredNJ by $20 to $100 per person per month for households earning up to 600 percent of the federal poverty level — approximately $93,900 for a single adult in 2026. The state subsidy stacks on top of federal Advance Premium Tax Credits and applies automatically during enrollment. For individuals between 400 and 600 percent FPL where federal credits phase out, NJHPS is often the only subsidy available.

What is the difference between on-exchange and off-exchange individual plans in NJ?

On-exchange individual plans purchased through GetCoveredNJ are eligible for federal premium tax credits and NJ Health Plan Savings subsidies. Off-exchange ACA-compliant plans use the same underwriting rules and consumer protections but cannot receive any subsidy assistance. For individuals below 600 percent FPL, on-exchange plans almost always produce lower net costs. Off-exchange makes sense primarily for individuals above 600 percent FPL or those seeking Platinum-tier coverage not offered on the NJ marketplace.

Can I enroll in individual health insurance in NJ outside of open enrollment?

Yes. GetCoveredNJ offers special enrollment periods triggered by qualifying life events including job loss, marriage, birth, moving to New Jersey, aging off a parent’s plan, and pregnancy — a NJ-specific trigger not available federally. The NJ Easy Enrollment Health Insurance Program also lets uninsured residents trigger a special enrollment period through the state income tax return, without needing a qualifying life event. This makes NJ one of the most accessible states for year-round individual enrollment.

Which metal tier is best for individual health insurance in New Jersey?

The best metal tier for individual NJ health insurance depends on income and expected healthcare use. Silver with cost-sharing reductions is best for individuals at 138–250 percent FPL — CSR dramatically reduces deductibles at no extra premium cost. Gold is competitive for individuals above 250 percent FPL who expect moderate to heavy healthcare use. Bronze is appropriate only for healthy individuals above 250 percent FPL who primarily want protection against major unexpected expenses.

New Jersey Health Insurance Resources

Complete 2026 overview — carriers, FamilyCare, mandate, and all subsidy paths

GetCoveredNJ MarketplaceStep-by-step enrollment, NJHPS stacking, and the Easy Enrollment Program

Best NJ Health PlansFive-carrier comparison with 2026 rate changes and OMNIA network guide

Self-Employed CoverageNJHPS strategies and tax deductions for NJ freelancers and 1099 workers

Costs & Savings GuidePremium ranges by age and county with the full NJHPS subsidy guide

Short-Term Health InsuranceGap coverage rules, mandate implications, and marketplace alternatives

New Jersey PPO PlansHorizon PPO and OMNIA for individuals needing cross-state coverage

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required

Enroll in Individual NJ Health Insurance for 2026

Whether on GetCoveredNJ or off-exchange, the right individual plan depends on income, providers, and whether the NJ mandate penalty or NJHPS savings apply. ForHealthInsurance.com’s licensed NJ brokers run the full comparison at no cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving New Jersey residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.