South Dakota Small Business Health Insurance 2026 Guide

South Dakota small business health insurance for 2026 covers any employer with 1 to 50 full-time-equivalent employees, including the state’s roughly 84,000 small businesses that employ over half of South Dakota’s private workforce. Three carriers — Avera Health Plans, Sanford Health Plan, and Wellmark Blue Cross Blue Shield — sell small group coverage statewide; the same carriers also support Individual Coverage Health Reimbursement Arrangements (ICHRA) for South Dakota employers who prefer the reimbursement model. Small employers with fewer than 50 FTEs are not subject to the ACA employer mandate, but those who voluntarily offer benefits can access traditional small group plans, the federal SHOP marketplace through HealthCare.gov, ICHRA, or qualified small employer HRAs (QSEHRAs). For employers with under 25 FTEs and average annual wages under $61,000, the Small Business Health Care Tax Credit can offset up to 50% of premium contributions when coverage is purchased through SHOP. This guide walks through the available structures, the three-carrier landscape, cost ranges, and how to choose between traditional group coverage and ICHRA.

What brings you here today?

Four Ways to Offer Health Benefits as a South Dakota Small Business

South Dakota small business health insurance for 2026 comes in four structures: traditional small group plans purchased directly from Avera, Sanford, or Wellmark; small group plans purchased through SHOP on HealthCare.gov (which unlocks the Small Business Health Care Tax Credit for eligible employers); ICHRA reimbursement for individual marketplace plans employees buy themselves; and QSEHRA, a smaller-scale reimbursement option for employers with under 50 FTEs who don’t currently offer group coverage.

Direct-to-carrier group plans

The classic small employer model. The business chooses one or more group plans from Avera, Sanford, or Wellmark BCBS, contributes a percentage of premium (typically 50%–80% of employee-only), and enrolls all eligible employees. Plans use community-rated pricing within the small group market — premiums vary by employee age mix and family composition but not by individual health status. Best for employers with employees concentrated geographically and a stable network preference. Group plans remain a backbone of South Dakota small business health insurance.

- 1–50 FTE eligible

- Employer contributes typically 50%–80%

- Sold direct by Avera, Sanford, Wellmark

- HMO, EPO, and PPO designs available

SHOP-purchased group plans

Small Business Health Options Program — federal SHOP marketplace accessible through HealthCare.gov for employers with 1 to 50 FTEs. Plans are sold by the same three carriers (Avera, Sanford, Wellmark) but enrollment goes through a SHOP-certified agent. SHOP enrollment is required to qualify for the Small Business Health Care Tax Credit (up to 50% of employer premium contributions for under-25-FTE employers with average wages under $61,000). The SHOP credit is a key lever in South Dakota small business health insurance.

- 1–50 FTE eligible

- Required for the Tax Credit

- Same carriers as direct-to-carrier

- Two-year credit limit on Tax Credit

Individual Coverage HRA

Effective since January 2020, ICHRA lets employers of any size reimburse employees tax-free for individual marketplace plans the employees choose themselves. The employer sets a fixed monthly reimbursement (any amount), and employees enroll through HealthCare.gov in plans that match their preferred carrier and network. Best for employers with employees spread across South Dakota who need different carrier networks (Sanford in the East, Wellmark in the West, Avera anywhere), or for employers who want fully predictable benefit costs. Defined contribution is reshaping South Dakota small business health insurance.

- Any size employer

- Tax-free reimbursement to employees

- Employees choose their own plan

- Fixed monthly cost to employer

The fourth structure — QSEHRA (Qualified Small Employer Health Reimbursement Arrangement) — is a more limited cousin of ICHRA. QSEHRA is available to employers with fewer than 50 FTEs that don’t currently offer group health coverage. Reimbursement caps for 2026 are approximately $6,350 per single employee per year and $12,800 per family — significantly lower than uncapped ICHRA contributions. QSEHRA was the original employer reimbursement structure (created by Congress in 2016) and is still used by very small South Dakota employers who want a simple, capped reimbursement arrangement without the formal documentation requirements of ICHRA. QSEHRA is the simplest form of South Dakota small business health insurance.

South Dakota Small Group Carriers: Avera, Sanford, Wellmark

The same three carriers serving South Dakota’s individual marketplace also dominate the small group market — Avera Health Plans, Sanford Health Plan, and Wellmark Blue Cross Blue Shield. Each anchors a different part of the state, and the right carrier for a small business depends on where employees live and where they receive care. Wellmark is the dominant statewide and PPO carrier; Sanford and Avera anchor East River through their integrated health systems.

Sanford Health Plan offers small group plans built on the Sanford Health system network — Sanford USD Medical Center in Sioux Falls, Sanford Aberdeen, Sanford Vermillion, Sanford Watertown, and dozens of clinics across eastern South Dakota. For small businesses concentrated in Sioux Falls, Aberdeen, or other East River markets where employees use Sanford providers, Sanford Health Plan typically produces the lowest small group premiums. The trade-off is the same one that applies in the individual market — Sanford small group HMO and EPO designs work well when care stays inside the system, and become expensive or unworkable when employees need care across systems or out of state. Network reach drives many South Dakota small business health insurance decisions.

Avera Health Plans offers parallel small group coverage built on the Avera Health system network — Avera McKennan in Sioux Falls, Avera Sacred Heart in Yankton, Avera St. Luke’s in Aberdeen, Avera Queen of Peace in Mitchell. The Avera small group footprint mirrors Sanford’s geographic strength but anchors on a different integrated system. Small businesses in the same East River markets often have a real choice between Avera and Sanford, and the decision usually turns on which system contains the practical providers most employees use. Some larger small businesses (25–50 FTE) offer both options to give employees a choice of system.

Wellmark Blue Cross Blue Shield is the dominant carrier for South Dakota small businesses with statewide footprints, West River presence, employees who travel, or employees with providers across multiple systems. Wellmark’s broader network — contracting across Sanford, Avera, and Monument Health in Rapid City — plus BlueCard national reciprocity makes Wellmark the practical choice for trucking companies, agricultural distributors, regional sales operations, and any business with a mobile workforce. Wellmark also offers the most PPO design options in the small group market, which matters for employees who don’t want HMO referral requirements. Some small employers with above-cliff owners or executives also offer ICHRA paired with off-exchange PPO health insurance plans — letting executives shop broader networks while rank-and-file employees use marketplace plans through ICHRA.

Group Plan vs ICHRA: Which Structure Fits Your Business

The choice between a traditional group plan and ICHRA reimbursement comes down to three factors for South Dakota small businesses: geographic distribution of employees, predictability of benefit costs, and administrative complexity tolerance. Group plans work best for geographically concentrated employee populations on consistent networks. ICHRA works best for distributed workforces, businesses wanting fixed-cost benefit budgets, and employers who want employees to choose their own plan and carrier.

Choose a traditional group plan if…

Most employees live and receive care in the same South Dakota region — for example, a Sioux Falls professional services firm where most employees are East River and use Sanford or Avera providers. Group plans produce competitive premiums, leverage community rating, and simplify benefit administration to a single plan or small set of plans. Employer-paid premium contributions are tax-deductible, and employees receive coverage as a tax-free benefit. Tax treatment is a major advantage of South Dakota small business health insurance.

Choose ICHRA if…

Your employees are geographically distributed across South Dakota — Sioux Falls, Rapid City, Aberdeen, remote workers — and need different carrier networks. ICHRA lets each employee pick the carrier that fits their geography (Sanford East River, Wellmark West River, Avera anywhere) while you provide a fixed reimbursement. Benefit costs become fully predictable; administrative complexity is real but front-loaded into setup.

Choose SHOP if…

You qualify for the Small Business Health Care Tax Credit — under 25 FTEs, average annual wages under $61,000, paying at least 50% of employee premiums, and want to enroll through SHOP rather than direct-to-carrier. The tax credit is worth up to 50% of employer premium contributions and is available for two consecutive tax years. For very small SD employers paying significant employee premiums, the Tax Credit makes SHOP enrollment worth the slight administrative friction. That trade-off shapes South Dakota small business health insurance setup.

Choose QSEHRA if…

You have under 50 FTEs, don’t currently offer group health coverage, and want a simple reimbursement arrangement without ICHRA’s documentation overhead. QSEHRA is capped (~$6,350 single / ~$12,800 family for 2026) and works best as a starter benefit for very small employers — 5 to 15 employees — testing whether to invest in a more substantial program later.

Get an SD Small Group Quote

A licensed agent compares small group plans from Avera, Sanford, and Wellmark BCBS, evaluates whether ICHRA produces better economics for your employee distribution, and identifies whether you qualify for the Small Business Health Care Tax Credit. Free, no obligation.

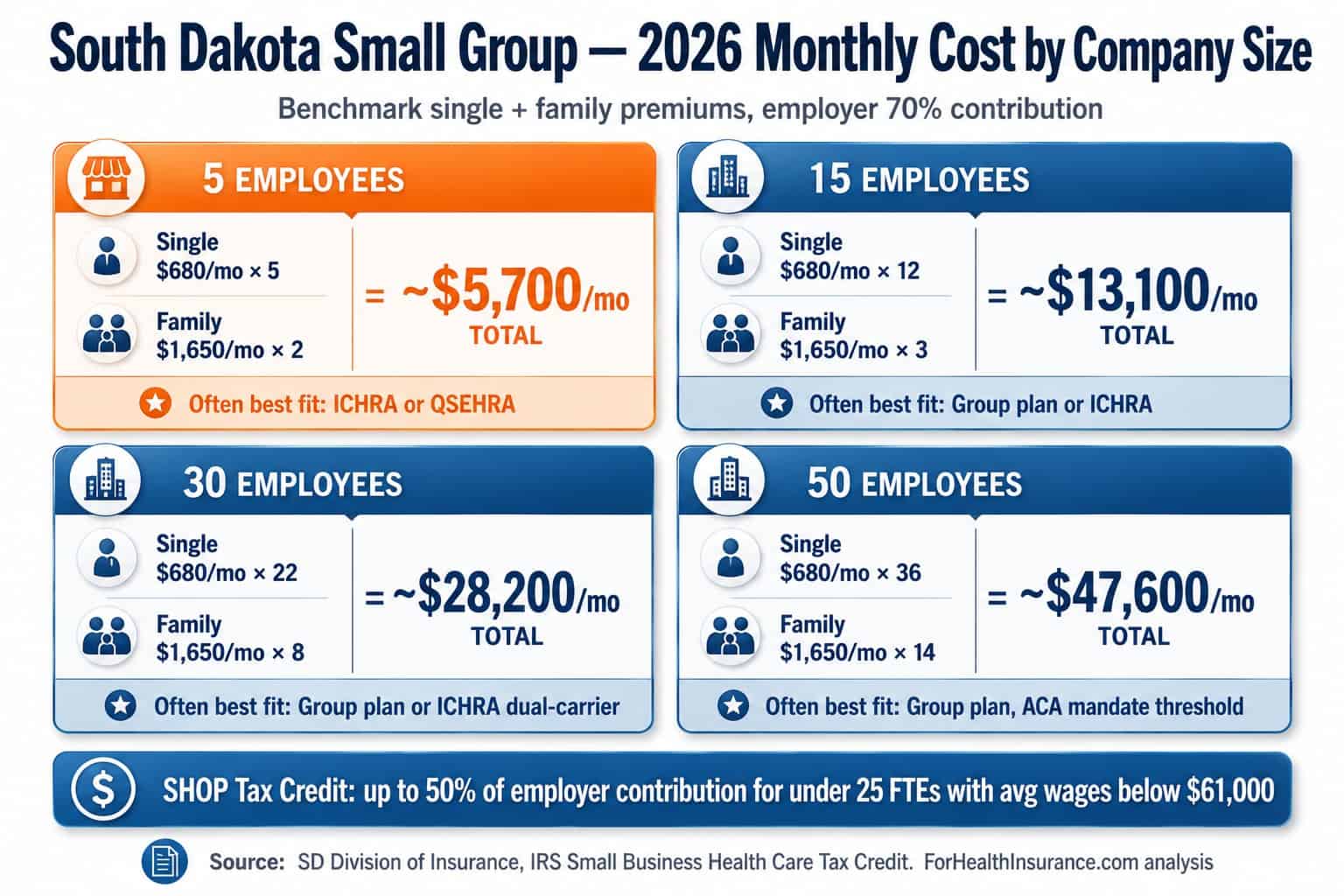

South Dakota Small Group Costs and the Tax Credit

Small group premiums in South Dakota for 2026 typically run $580 to $780 per employee per month for single coverage and $1,400 to $1,950 per month for family coverage. Most employers contribute 50%–80% of employee-only premiums and 0%–50% of dependent premiums. Employers with under 25 FTEs and average wages under $61,000 may qualify for the Small Business Health Care Tax Credit at up to 50% of premium contributions when enrolled through SHOP.

| Employee Headcount | Single Premium Range | Family Premium Range | Best-Fit Structure |

|---|---|---|---|

| 1–5 FTE | $580–$780/mo | $1,400–$1,950/mo | QSEHRA, ICHRA, or small group |

| 6–15 FTE | $580–$780/mo | $1,400–$1,950/mo | Group plan + SHOP if Tax Credit eligible |

| 16–25 FTE | $580–$780/mo | $1,400–$1,950/mo | Group plan or ICHRA, last year for Tax Credit |

| 26–50 FTE | $580–$780/mo | $1,400–$1,950/mo | Group plan or ICHRA dual-carrier |

| 50+ FTE | Custom rated | Custom rated | ACA employer mandate applies |

The Small Business Health Care Tax Credit is the most undervalued benefit available to small South Dakota employers. Eligibility requires fewer than 25 FTEs, average annual wages under $61,000, employer contribution of at least 50% of employee-only premiums, and enrollment through SHOP on HealthCare.gov. The credit can reach 50% of the employer’s premium contribution for two consecutive tax years. For a 12-FTE Sioux Falls professional services firm with average wages of $52,000 and 70% employee premium contribution, the Tax Credit can be worth $25,000–$40,000 per year — a material reduction in the effective cost of offering benefits. Many South Dakota small employers don’t claim the credit because they enroll directly with carriers rather than through SHOP. SHOP enrollment is the trigger; the same Avera, Sanford, or Wellmark plans are available either way, but only the SHOP path unlocks the Tax Credit. It is the headline incentive in South Dakota small business health insurance.

How to Set Up Small Group Coverage in South Dakota

Setting up South Dakota small business health insurance takes 30 to 90 days depending on the structure chosen. Group plans typically launch on the first of the month following enrollment. ICHRA setup requires an ICHRA plan document and a 90-day employee notice. SHOP enrollment goes through HealthCare.gov via a certified agent. The South Dakota Division of Insurance regulates all small group products and reviews carrier rate filings annually.

Determine your structure (group, ICHRA, SHOP, or QSEHRA)

Start by mapping your employee distribution geographically. If most employees are East River and use one health system, a traditional group plan with Sanford or Avera typically wins. If employees are statewide or you want predictable benefit costs, ICHRA is often better. If you have fewer than 25 FTEs with average wages under $61,000, evaluate SHOP for the Tax Credit. If you’ve never offered benefits and want a simple starter program, QSEHRA caps complexity.

Get quotes from all three South Dakota carriers

For traditional group or SHOP plans, request small group quotes from Avera Health Plans, Sanford Health Plan, and Wellmark BCBS. Carrier rate quotes require a census file (employee names, dates of birth, ZIP codes, family status, smoker status) — most carriers turn around quotes in 5 to 10 business days. For ICHRA, you don’t need carrier quotes; instead, model employee out-of-pocket cost against marketplace plan options at projected reimbursement amounts. Modeling costs first is smart in South Dakota small business health insurance.

Decide your contribution amount

For traditional group: most South Dakota small employers contribute 50%–80% of employee-only premiums and 0%–50% of dependent premiums. The minimum employer contribution required by carriers is typically 50% of employee-only. For ICHRA: choose a fixed monthly reimbursement amount (any amount the employer chooses) — typical SD employers reimburse $400–$700 per single employee per month. The reimbursement must be the same across employees in the same employee class.

Complete enrollment paperwork

Group and SHOP plans require a master application, group census, employer contribution agreement, and employee enrollment forms with completed health questionnaires (small group plans use community rating, not individual underwriting, but enrollment paperwork is still required). ICHRA requires an ICHRA plan document, a Section 105 plan administrator (third-party or self-administered), and a 90-day notice to all employees before the plan year begins.

Onboard employees and pay premiums

Group plans launch on the first of the month following enrollment completion. Employer pays the full monthly premium to the carrier; employees’ contributions are typically deducted pre-tax through payroll. ICHRA reimbursements are processed through payroll or a third-party administrator — employees submit proof of individual coverage and reimbursements are paid out tax-free. The South Dakota Division of Insurance regulates carrier compliance; employers should verify carrier licensure through South Dakota Division of Insurance before signing any group contract.

Frequently Asked Questions

Common questions about small business coverage in South Dakota cover whether small employers must offer coverage, which carriers participate, how ICHRA works, what small group plans cost in 2026, and what SHOP is.

Are South Dakota small businesses required to offer health insurance?

No. South Dakota small businesses with fewer than 50 full-time-equivalent employees are not required by federal or state law to offer health insurance. The ACA Employer Shared Responsibility Provision (the employer mandate) applies only to employers with 50 or more FTEs. South Dakota does not impose an additional state-level mandate. About 47% of South Dakota employers with under 50 FTEs voluntarily offer health benefits — typically as a recruitment and retention tool in a tight labor market. Small employers who do offer coverage can use traditional small group plans, an Individual Coverage Health Reimbursement Arrangement (ICHRA), or qualified small employer HRAs (QSEHRAs).

What carriers offer small group plans in South Dakota?

Three carriers dominate South Dakota’s small group market in 2026: Avera Health Plans (anchored at Avera McKennan in Sioux Falls and across eastern and central South Dakota), Sanford Health Plan (anchored at Sanford USD Medical Center in Sioux Falls with strong East River presence), and Wellmark Blue Cross Blue Shield (the broadest statewide network including West River and BlueCard national reciprocity for employees who travel). The same three carriers serve both individual and small group markets, but small group plans use community-rated pricing rather than individual age-banded rating, and offer different network and benefit configurations than the individual marketplace.

What is ICHRA and can South Dakota employers use it?

ICHRA — Individual Coverage Health Reimbursement Arrangement — allows employers of any size to reimburse employees tax-free for individual marketplace plans the employees buy themselves through HealthCare.gov. South Dakota employers can use ICHRA effective since January 2020. The employer sets a monthly reimbursement amount (any amount the employer chooses), and employees use it toward an individual plan from Avera, Sanford, or Wellmark. ICHRA reimbursements are not taxable income to employees and are deductible to the employer. ICHRA is often the right structure for South Dakota small businesses with employees spread across the state who need different network footprints, or for employers who want predictable benefit costs without the administrative complexity of group plan administration. That simplicity appeals to many buyers of South Dakota small business health insurance.

How much does small group health insurance cost in South Dakota?

Small group health insurance premiums in South Dakota for 2026 typically run $580 to $780 per employee per month for single coverage and $1,400 to $1,950 per month for family coverage. Premiums vary by carrier, plan tier, employee age mix, and whether the plan uses HMO, EPO, or PPO design. Most South Dakota small employers contribute 50%–80% of the employee-only premium and 0%–50% of dependent premiums. The Small Business Health Care Tax Credit is available to employers with fewer than 25 FTEs, average annual wages under $61,000, who pay at least 50% of employee premiums and enroll through SHOP — the credit can reach 50% of the employer’s premium contribution. That credit can transform South Dakota small business health insurance economics.

What is SHOP and is it available in South Dakota?

SHOP — Small Business Health Options Program — is the federal small business marketplace for employers with 1 to 50 full-time-equivalent employees. South Dakota employers access SHOP through HealthCare.gov by working with a SHOP-certified agent or broker. SHOP enrollment is required to qualify for the Small Business Health Care Tax Credit, which can be claimed by employers with under 25 FTEs and average wages under $61,000 who pay at least half of employee premiums. SHOP plans are sold by Avera, Sanford, and Wellmark BCBS in South Dakota, the same three carriers serving the individual and traditional small group markets.

Compare 2026 SD Small Group Options

A licensed agent compares small group plans from Avera, Sanford, and Wellmark BCBS, evaluates ICHRA economics for your employee distribution, and identifies whether your business qualifies for the Small Business Health Care Tax Credit through SHOP. Free, no obligation.

Free SD small business comparison — covers traditional group, SHOP, ICHRA, and QSEHRA options.

Related South Dakota Health Insurance Resources

Complete SD coverage guide — Avera, Sanford, Wellmark, Medicaid, costs.

SD Health Insurance MarketplaceHealthCare.gov enrollment, OEP windows, and the application walkthrough.

Affordable Coverage in South DakotaSubsidy strategies, average costs, and how to lower your 2026 premium.

HealthCare.gov SHOP MarketplaceFederal SHOP enrollment portal for South Dakota small employers.

SD Division of InsuranceSmall group carrier rate filings, complaints, and licensed agent verification.

IRS Small Business Health Care Tax CreditFederal eligibility and calculation rules for the SHOP-linked tax credit.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving South Dakota businesses. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.