Affordable Health Insurance South Dakota 2026: Cost Guide

Affordable health insurance in South Dakota for 2026 means understanding three things: what plans actually cost full price, how Advance Premium Tax Credits and Cost-Sharing Reductions reduce those costs for households between 138% and 400% of the federal poverty level, and when off-exchange Wellmark BCBS PPO plans produce better value than on-exchange options for households above the 400% FPL subsidy cliff. The full-price benchmark Silver plan in South Dakota runs approximately $695 per month for a 40-year-old in 2026, with rates increasing with age — but about 83% of marketplace enrollees qualify for federal subsidies averaging $568 per month, bringing the subsidy-eligible South Dakotan’s average premium to about $118 per month. Bronze plans run lower premiums with higher deductibles; Gold plans run higher premiums with lower deductibles. The 2025 expiration of enhanced American Rescue Plan subsidies returned the 400% FPL cliff for 2026 — making the math different for above-cliff households than it was during 2021–2025. This guide covers actual 2026 costs, subsidy maximization strategies, when each metal tier is the right call, and when off-exchange PPO produces better value than the marketplace.

What brings you here today?

What South Dakota Coverage Actually Costs in 2026

Affordable health insurance South Dakota pricing in 2026 starts at about $480 per month for a Bronze plan and runs to about $880 per month for Gold for a 40-year-old non-tobacco user before subsidies. After Advance Premium Tax Credits, the average subsidy-eligible South Dakotan paid about $118 per month — subsidies averaged $568 per month and reduced costs for 83% of marketplace enrollees. Costs vary by age, county, plan tier, and tobacco use.

Bronze plans

~$480/moFull-price benchmark for a 40-year-old non-tobacco user. Lowest premium, highest deductible (~$7,500 typical). Best for households above 250% of FPL who don’t expect heavy medical use. Bronze is a core route to affordable health insurance in South Dakota for the healthy.

Silver plans (full price)

~$695/moFull-price benchmark for a 40-year-old non-tobacco user. The benchmark tier — APTC is calculated against the second-cheapest Silver plan in your county. Eligible for Cost-Sharing Reductions up to 250% of FPL. CSR Silver is the strongest affordable health insurance in South Dakota for low-to-middle incomes.

Gold plans

~$880/moFull-price benchmark for a 40-year-old non-tobacco user. Higher premium, lower deductible (~$1,800 typical). Best for households expecting significant medical spending — chronic conditions, planned surgeries, ongoing care. Matching the plan to your health is the key to affordable health insurance in South Dakota.

Subsidy-eligible average

~$118/moAverage post-subsidy monthly premium for the 83% of South Dakota marketplace enrollees who qualified for Advance Premium Tax Credits in 2026. Subsidies averaged $568 per month before applying. Those credits are what make affordable health insurance in South Dakota reachable.

The South Dakota Division of Insurance approved an average 6.4% rate increase across the three marketplace carriers (Avera Health Plans, Sanford Health Plan, Wellmark Blue Cross Blue Shield) for 2026 — meaningful but moderate compared to the double-digit increases in some neighboring states. The 6.4% average masks variation by carrier and tier: some Bronze plans rose more aggressively than Silver, and Gold rate changes varied significantly across the three carriers. Premiums also vary by age (a 60-year-old pays roughly 3× what a 21-year-old pays for the same plan under federal age-rating rules), tobacco use (carriers can charge tobacco users up to 50% more in South Dakota), and household size on family policies. These factors set the real price of affordable health insurance in South Dakota.

What’s not visible in the headline numbers: the 2025 expiration of enhanced American Rescue Plan subsidies meaningfully changed the affordability picture for many South Dakotans. From 2021 through 2025, ARP enhancements capped marketplace premiums at 8.5% of household income for everyone — meaning even households above 400% of FPL received some federal assistance. That enhancement expired December 31, 2025. For 2026, the 400% FPL subsidy cliff returned to its pre-ARP form: above the threshold, no federal subsidy applies, and full-price premiums kick in. This is the single biggest reason South Dakota marketplace enrollment dropped from a record 54,721 in 2025 to 50,951 in 2026.

How South Dakota Marketplace Subsidies Work

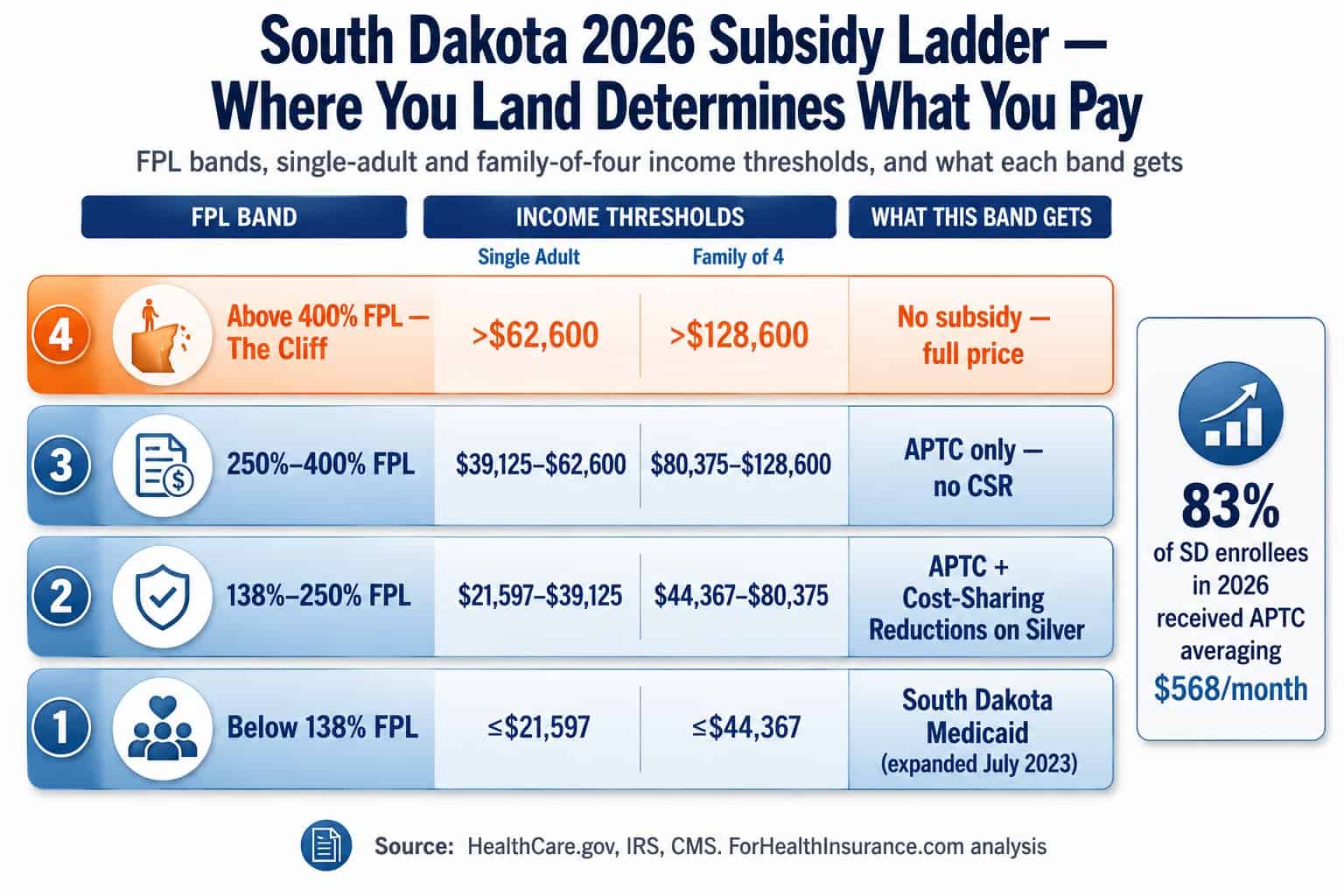

The marketplace uses two federal subsidies — Advance Premium Tax Credits and Cost-Sharing Reductions — calculated against your projected 2027 household income. APTC reduces your monthly premium directly. CSR is available only on Silver plans for households up to 250% of FPL and reduces deductibles and out-of-pocket costs. Both are calculated automatically by HealthCare.gov when you apply.

APTC is structured around an “applicable percentage” of your household income that you’re expected to contribute toward the second-cheapest Silver plan in your county. Below 150% of FPL, that contribution is essentially zero. At 200% of FPL, it’s about 2% of income. At 300% of FPL, it’s about 6%. At 400% of FPL, it’s about 8.5%. Above 400% of FPL in 2026, no APTC applies — the subsidy cliff returned with the ARP expiration. The dollar amount of your APTC is the difference between the benchmark Silver premium in your county and your applicable contribution. You can apply your APTC to any plan from any of the three South Dakota carriers — not just Silver — but the APTC dollar amount is fixed regardless of which plan you choose. Using that fixed credit well is central to affordable health insurance in South Dakota.

CSR works differently. It’s only available on Silver plans, and only for households below 250% of FPL. CSR effectively transforms the Silver plan’s actuarial value: at 138%–150% of FPL, Silver becomes a 94% AV plan (better than standard Gold). At 150%–200% of FPL, Silver becomes 87% AV. At 200%–250% of FPL, Silver becomes 73% AV. The carrier absorbs the cost-sharing reduction; the federal government reimburses carriers for it. For South Dakotans in these income bands, Silver almost always produces the lowest total annual cost — premium plus expected out-of-pocket — and Bronze is frequently a worse total deal even though the monthly premium looks lower.

| 2026 Income Range | Single Adult | Family of 4 | What You Get |

|---|---|---|---|

| 138%–150% FPL | $21,597–$23,475 | $44,367–$48,225 | APTC + 94% AV Silver (CSR maximum) |

| 150%–200% FPL | $23,475–$31,300 | $48,225–$64,300 | APTC + 87% AV Silver (CSR strong) |

| 200%–250% FPL | $31,300–$39,125 | $64,300–$80,375 | APTC + 73% AV Silver (CSR limited) |

| 250%–400% FPL | $39,125–$62,600 | $80,375–$128,600 | APTC only (no CSR) |

| Above 400% FPL | > $62,600 | > $128,600 | No subsidy — cliff returned in 2026 |

Five Strategies to Lower Your South Dakota Premium

Five strategies typically lower the cost of affordable health insurance South Dakota residents pay: maximize APTC by accurately projecting income, pick Silver if you qualify for CSR, choose Bronze for low expected medical use above 250% FPL, contribute to an HSA through an HSA-eligible plan, and shop off-exchange Wellmark PPO if above the 400% FPL cliff. Each strategy works for a different income band and care-use pattern.

Project your 2027 income accurately

APTC is calculated against your projected 2027 household Modified Adjusted Gross Income. Under-projecting income means HealthCare.gov gives you a larger monthly subsidy than you actually qualify for — the IRS reconciles at tax time and you owe back the overpayment. Over-projecting means you pay more in monthly premium than necessary and get a refund only when you file your 2027 taxes (12+ months later). For South Dakotans whose income fluctuates seasonally — agricultural workers, ranchers, contract workers, real estate agents — estimate annual MAGI realistically rather than picking a number that maximizes upfront subsidy. Honest income estimates protect your affordable health insurance in South Dakota.

Pick Silver if you qualify for CSR (138%–250% FPL)

Cost-Sharing Reductions are the most undervalued benefit in the marketplace. A Silver plan with CSR at 94% AV (for households at 138%–150% FPL) outperforms a standard Gold plan on actuarial value while costing less per month after APTC. South Dakotans in this income band who pick Bronze instead — chasing the lowest monthly premium — almost always come out worse on total annual cost when medical events occur. CSR is automatic on Silver plans and only on Silver plans. Switching from Bronze to Silver with CSR is the single highest-leverage adjustment most subsidized South Dakotans can make. It is the biggest single lever for affordable health insurance in South Dakota.

Choose Bronze if above 250% FPL with low expected use

Above 250% of FPL, CSR no longer applies, and Silver loses its primary advantage over Bronze. For South Dakotans in their 30s and 40s with no chronic conditions, no anticipated procedures, and a strong cash position to absorb the higher Bronze deductible, Bronze produces real annual savings. The premium gap between Silver and Bronze for a 40-year-old in South Dakota is typically $200–$300 per month — about $2,400–$3,600 per year. If you have one or two routine doctor visits annually and no major medical events, Bronze often wins on total cost. For the healthy, that is the most affordable health insurance in South Dakota.

Use an HSA-eligible high-deductible plan to reduce taxable income

Many Bronze and some Silver plans qualify as Health Savings Account-eligible high-deductible health plans. HSA contributions are tax-deductible (federal and South Dakota — South Dakota has no state income tax, so no state benefit, but federal deduction applies), grow tax-free, and are tax-free when used for qualified medical expenses. The 2026 HSA contribution limit is $4,300 for self-only coverage and $8,550 for family. For South Dakotans in the 22%–32% federal marginal tax bracket, an HSA contribution of $4,300 reduces federal tax by $946–$1,376 — effectively making the high-deductible plan cheaper than the headline premium suggests. HSA savings quietly improve affordable health insurance in South Dakota.

Shop off-exchange Wellmark PPO if above 400% FPL

Above the 400% FPL subsidy cliff, on-exchange and off-exchange compete on full-price terms. Off-exchange Wellmark Blue Cross Blue Shield PPO plans frequently offer broader provider networks, BlueCard national reciprocity, and more flexible plan designs — and price competitively against on-exchange Silver and Gold for above-cliff households. Off-exchange Wellmark PPO premiums for a 40-year-old in 2026 typically run $620 to $780 per month, comparable to or slightly below full-price on-exchange Silver. For above-cliff households, shopping both on-exchange and off-exchange before deciding is essential.

Calculate Your South Dakota Subsidy

A licensed agent runs your projected 2027 income against APTC and CSR thresholds, identifies your lowest total annual cost across Avera, Sanford, and Wellmark, and compares on-exchange and off-exchange options. Your real after-subsidy number in one call. Free, no obligation.

Real-World South Dakota Cost Scenarios

Because South Dakota’s three carriers split along integrated-system lines — Avera and Sanford run HMO and EPO networks tied to their own hospitals, while Wellmark is the statewide PPO with BlueCard reciprocity — the lowest-cost plan in each case below depends as much on which health system a household already uses as on income. These four 2026 examples run from the expansion floor to the subsidy cliff.

A 26-year-old Sioux Falls line cook earning about $32,000 (roughly 205% FPL)

At this income she lands in the Cost-Sharing Reduction band, where a Silver plan quietly upgrades to 87% actuarial value — Gold-level protection at a Bronze-level price. A Sanford or Avera Silver runs near $620 a month at full price; her premium tax credit trims that to $40–$80, and CSR pulls the deductible down from about $5,500 to near $1,800. Dropping to Bronze would save maybe $20 a month but forfeit the CSR entirely, so a single Sanford ER visit would erase the difference. For a healthy single renter in Minnehaha County, CSR Silver is the most affordable health insurance in South Dakota at this income.

An Aberdeen family of four at about $90,000 (roughly 350% FPL)

This Brown County household clears the CSR line but stays well inside subsidy range, and with four people on one policy the integrated-system question drives the choice. If the children’s pediatrician and the family clinic sit inside the Avera or Sanford network, a system-matched Silver or Gold keeps every visit in-network. A routine-care year rewards Bronze at roughly $850–$1,000 a month after the credit; a year with a chronic condition or a planned surgery rewards Gold, whose lower deductible outruns its higher premium. Families who split time between Aberdeen and a cabin across the Minnesota line lean toward a Wellmark PPO for the BlueCard reach.

A 58-year-old rancher near Rapid City at about $46,000 (roughly 300% FPL)

West River rewrites the math. Avera and Sanford footprints thin out west of the Missouri River, and Monument Health — the dominant Rapid City system — is reached mainly through Wellmark contracts. At 58, full-price Silver runs $1,050–$1,200 a month before the credit pulls it down to roughly $300–$380. A Wellmark PPO keeps Monument providers in-network and adds BlueCard access for the specialty care that often means a drive to Sioux Falls or out of state. With Medicare seven years off, choosing providers who also accept it smooths the eventual handoff at 65.

A self-employed Brookings couple at about $145,000 combined (above the 400% FPL cliff)

Past 400% FPL the subsidy vanishes, so staying on-exchange loses its only structural advantage. Two 50-year-olds face roughly $1,800–$2,000 a month for on-exchange Silver, while the same couple can buy an off-exchange Wellmark PPO closer to $1,500–$1,800 with broader networks and HSA-eligible designs. The HSA is the hidden discount: an $8,550 family contribution in 2026 trims federal tax by $1,800–$2,700 before a dollar of care is spent. Once that tax math is counted, off-exchange is usually the most affordable health insurance in South Dakota for above-cliff households.

These cases all assume individual-market enrollment through HealthCare.gov; for the full enrollment calendar and a carrier-by-carrier breakdown, see the South Dakota marketplace guide, and the South Dakota health insurance guide covers Avera, Sanford, and Wellmark statewide in depth. Owners covering a team should compare routes on the South Dakota small business health insurance page.

Above the 400% FPL Cliff: When Off-Exchange PPO Wins

South Dakotans above 400% of FPL — single adults earning more than $62,600 or families of four earning more than $128,600 in 2026 — get zero Advance Premium Tax Credits with the return of the subsidy cliff. For these above-cliff households, on-exchange and off-exchange compete on full-price terms, and off-exchange Wellmark BCBS PPO plans often produce better total value than on-exchange Silver or Gold.

The 400% FPL cliff is the single biggest affordability change in South Dakota’s marketplace for 2026. From 2021 through 2025, the American Rescue Plan and the Inflation Reduction Act capped marketplace premiums at 8.5% of household income for everyone — including above-cliff households. A 60-year-old couple in Sioux Falls earning $100,000 (about 600% of FPL) received roughly $400–$600 per month in APTC during those years. For 2026, that subsidy is zero. The same couple’s monthly premium jumped by the full APTC amount, and many such households dropped marketplace coverage between November 2025 and January 2026 — contributing to South Dakota’s enrollment decline from 54,721 to 50,951.

For above-cliff South Dakotans, the right strategy is shopping both channels. On-exchange marketplace plans through HealthCare.gov sell at full price with no subsidy applied — Silver for a 40-year-old runs about $695 per month, Gold runs about $880 per month. Off-exchange Wellmark BCBS PPO products at the same age typically run $620 to $780 per month with broader provider networks, BlueCard national reciprocity (in-network access in all 50 states), and access to HSA-eligible plan designs that aren’t always available on-exchange. For households that don’t need APTC anyway, off-exchange often produces better network value at competitive cost.

For South Dakotans evaluating off-exchange PPO options nationwide — particularly those who want to compare plans by ZIP code, network footprint, and HSA-eligible designs — off-exchange PPO health insurance plans are available nationwide with quotes by ZIP code and no referral requirements. Above-cliff South Dakotans frequently come out ahead off-exchange when they account for network breadth and HSA tax savings on top of premium.

The cliff is asymmetric — under-projecting income matters more above 400% FPL

For South Dakotans whose income hovers near the 400% FPL line, accurate income projection matters more than at any other income band. Under-projecting (estimating 380% of FPL when actual ends up at 410%) means HealthCare.gov gives APTC during the year — and then the IRS recovers the entire annual subsidy at tax time when actual income exceeds the cliff threshold. Above-cliff households are not protected by the same APTC repayment caps that apply to subsidized households. For self-employed South Dakotans, those with variable income (sales commission, real estate, agricultural earnings), or those who might receive year-end bonuses, projecting conservatively above the cliff and shopping off-exchange Wellmark PPO eliminates this tax-time recovery risk entirely.

Frequently Asked Questions

Common questions about affordable health insurance South Dakota residents shop for in 2026 cover actual costs, premium-lowering strategies, the cheapest available plans, off-exchange PPO economics, and subsidy income thresholds.

How much does health insurance cost in South Dakota for 2026?

Full-price benchmark Silver plans in South Dakota run approximately $695 per month for a 40-year-old before subsidies in 2026, reflecting a 6.4% average rate increase approved by the South Dakota Division of Insurance. After Advance Premium Tax Credits, the average subsidy-eligible South Dakotan paid about $118 per month — federal subsidies averaged $568 per month and reduced costs for 83% of marketplace enrollees. A Bronze plan at the same age runs roughly $480 per month full price; Gold runs about $880 per month. Costs vary by age, county, plan tier, tobacco use, and household size.

How can I lower my South Dakota health insurance premium?

Five strategies typically lower premiums: maximize Advance Premium Tax Credits by accurately projecting your 2027 income (under-projection causes overpayment recovery at tax time, over-projection costs you subsidy upfront), pick Silver if you qualify for Cost-Sharing Reductions (138%–250% of FPL), reduce premiums in exchange for higher deductibles by choosing Bronze if you don’t expect heavy medical use and don’t qualify for CSR, contribute to a Health Savings Account through an HSA-eligible high-deductible plan to reduce taxable income, and shop off-exchange Wellmark BCBS PPO designs if you’re above the 400% FPL subsidy cliff.

What is the cheapest health insurance plan in South Dakota?

The cheapest on-exchange plan in South Dakota for a 40-year-old non-tobacco user is typically a Bronze plan from Sanford Health Plan or Avera Health Plans, with full-price premiums around $480 per month before subsidies. With APTC, that same Bronze plan often runs $0 to $150 per month for households at 138%–250% of FPL. However, the cheapest premium is rarely the cheapest total annual cost. For households eligible for Cost-Sharing Reductions (up to 250% of FPL), a Silver plan with CSR almost always produces the lowest combined annual cost (premium plus expected out-of-pocket) despite the higher monthly premium.

Are off-exchange PPO plans more affordable in South Dakota?

Off-exchange Wellmark Blue Cross Blue Shield PPO plans are not eligible for premium tax credits and are not the affordable choice for South Dakotans below 400% of FPL who would qualify for substantial subsidies on-exchange. Above the 400% FPL subsidy cliff, however, off-exchange PPO becomes competitive — full-price on-exchange Silver runs about $695 per month for a 40-year-old, while off-exchange Wellmark PPO runs $620 to $780 per month with broader networks and BlueCard national reciprocity. For above-cliff households who don’t get APTC anyway, off-exchange PPO often produces better network value at comparable cost.

What income qualifies for marketplace subsidies in South Dakota?

South Dakotans with household incomes between 138% and 400% of the federal poverty level qualify for Advance Premium Tax Credits in 2026. For 2026 marketplace coverage, that range is approximately $21,597 to $62,600 for a single adult and $44,367 to $128,600 for a family of four. About 83% of South Dakota marketplace enrollees received APTC in 2026, with subsidies averaging $568 per month. Cost-Sharing Reductions on Silver plans are available up to 250% of FPL ($39,125 single, $80,375 family of four). Below 138% of FPL, applicants are routed to South Dakota Medicaid, which expanded in July 2023 after voters approved Constitutional Amendment D.

Get Your Real After-Subsidy SD Quote

A licensed agent calculates your APTC and CSR amounts, identifies the lowest total annual cost across Avera, Sanford, and Wellmark BCBS, and runs the off-exchange PPO comparison if you’re above the cliff. The number that actually applies to your household. Free, no obligation.

Free SD subsidy calculation — covers all carriers and on-exchange/off-exchange comparison.

Related South Dakota Health Insurance Resources

Complete SD coverage guide — Avera, Sanford, Wellmark, Medicaid, costs.

SD Health Insurance MarketplaceHealthCare.gov enrollment, OEP windows, and the application walkthrough.

SD Small Business Health InsuranceGroup plans, ICHRA, SHOP, and small group options for SD employers.

HealthCare.gov (Official)South Dakota’s official federal marketplace enrollment portal.

KFF Subsidy CalculatorEstimate your 2026 APTC amount before applying through HealthCare.gov.

IRS Premium Tax Credit BasicsFederal rules for APTC eligibility, calculation, and tax-time reconciliation.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving South Dakota residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.