Kansas Small Business Health Insurance 2026: Group Plans, ICHRA & SHOP

Small business health insurance in Kansas is one of the most consequential benefits decisions a Kansas employer makes — and for 2026, it is also one of the most expensive. Group health insurance premiums for Kansas small businesses rose in line with the broader Kansas market, which posted a 26.6% weighted average rate increase on the individual marketplace. While small group rates are not publicly reported with the same precision as individual market rates, Kansas carriers including Blue Cross and Blue Shield of Kansas, Medica, and Ambetter all filed meaningful small group rate increases for 2026. Kansas small businesses with 2 to 50 full-time equivalent employees have five main coverage approaches: traditional group health insurance through a carrier like BCBS Kansas, the federal SHOP marketplace, an Individual Coverage HRA (ICHRA) that reimburses employees for individual plans they select themselves, a Qualified Small Employer HRA (QSEHRA) for businesses under 50 employees with no existing group plan, or self-insured coverage for businesses large enough to absorb claims risk. The Kansas small business health insurance market is dominated by BCBS Kansas on a statewide basis, with Blue Cross and Blue Shield of Kansas City competing in the KC metro, and Medica and United Healthcare providing alternatives in select markets. Average group coverage CPC in Kansas is $26.21 — among the highest of any Kansas health insurance keyword — reflecting the intensity of employer-side purchasing decisions. This guide walks through every Kansas small business health insurance option for 2026.

What’s your Kansas small business situation?

Kansas Small Group Health Insurance: Carrier Options

Kansas small businesses with 2 to 50 full-time equivalent employees can purchase group health insurance directly from carriers or through the SHOP marketplace. Blue Cross and Blue Shield of Kansas is the dominant small group carrier statewide, covering all 105 Kansas counties with HMO, EPO, and Premier Blue PPO plan designs. BCBS Kansas City serves the KC metro small group market. Medica, United Healthcare, and Aetna offer group alternatives in select Kansas markets.

BCBS Kansas’s small group product line mirrors its individual market strength — statewide network, contracts with The University of Kansas Health System, Stormont Vail Health, and Via Christi (Ascension Kansas), and BlueCard national reciprocity for businesses with employees who travel. For most Kansas small businesses outside the KC metro, BCBS Kansas is the starting point for group plan comparison. Premiums are community-rated in Kansas’s small group market — meaning rates are based on the age mix of enrolled employees rather than individual health history — which prevents premium penalties for businesses with older or less healthy employees.

Blue Cross and Blue Shield of Kansas City serves the small group market in Johnson, Wyandotte, Leavenworth, and Miami counties. Its PPO products — Preferred Care Blue and Blue Access — are well-suited to KC metro small businesses whose employees use both sides of the state line for care. Medica has a presence in the Wichita and Kansas City metro small group markets with competitive HMO pricing. The Kansas Insurance Department maintains a list of licensed small group carriers in Kansas and publishes annual market conduct data that Kansas employers can use to compare complaint ratios before selecting a carrier.

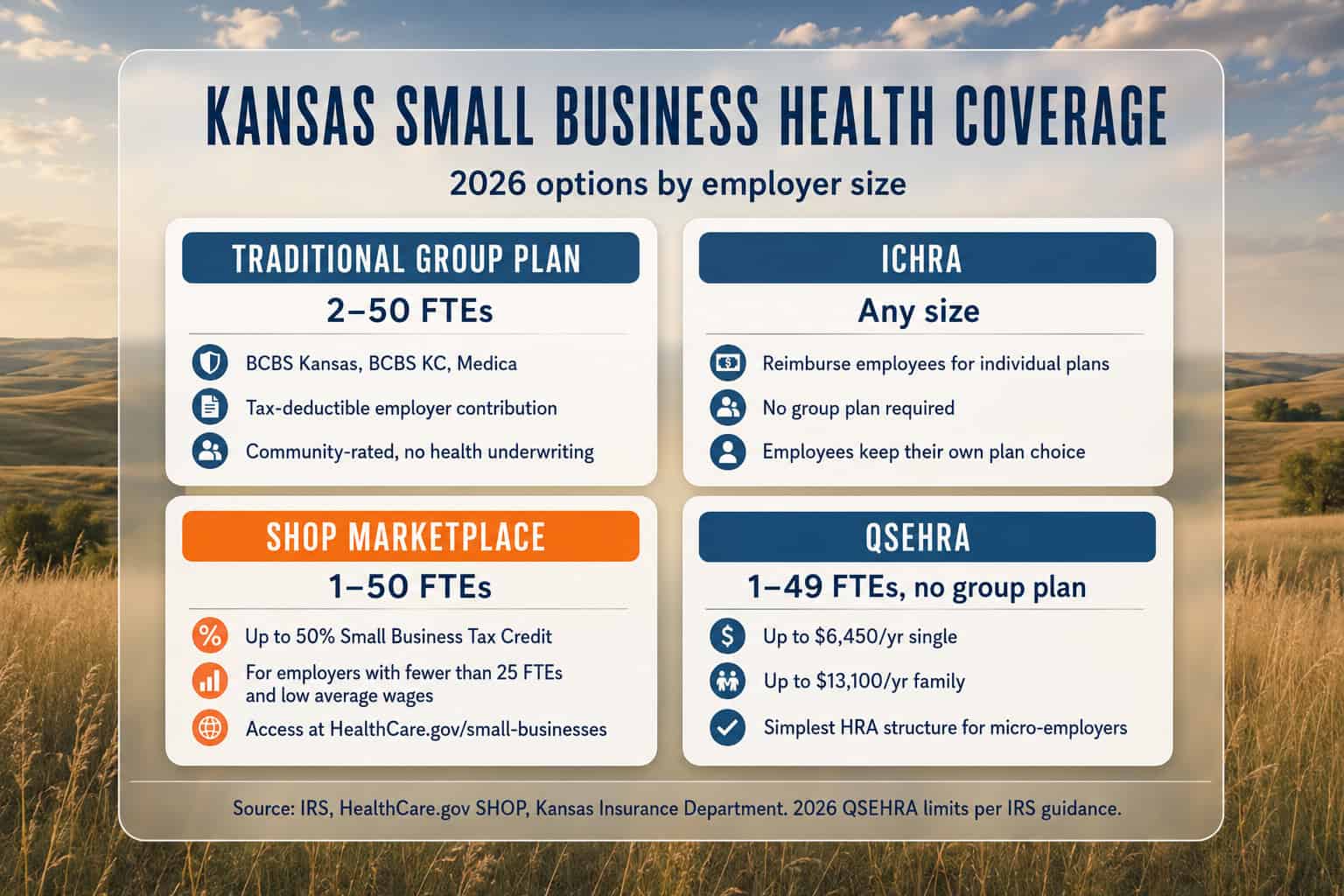

| Option | Group Size | Employer Contribution Required | Tax Credit Available | Best For |

|---|---|---|---|---|

| Traditional Group Plan (BCBS KS) | 2–50 FTEs | Typically 50%+ of employee premium | Via SHOP only | Most Kansas employers; broadest network |

| SHOP Marketplace | 1–50 FTEs | Typically 50%+ of employee premium | Up to 50% of contribution | Employers with <25 FTEs, low avg wages |

| ICHRA | Any size | Set monthly reimbursement amount | No (employees may get APTC) | Dispersed workforce; cost control |

| QSEHRA | 1–49 FTEs, no group plan | Up to $6,350/yr single, $12,800 family (2026) | No | Very small employers, simple structure |

| Self-Insured | Typically 50+ FTEs | Employer bears claims risk | No | Larger Kansas employers with stop-loss |

ICHRA: Reimburse Kansas Employees for Individual Plans

An Individual Coverage HRA (ICHRA) lets Kansas employers of any size reimburse employees tax-free for individual health insurance premiums and eligible medical expenses — without buying a group plan. The employer sets a monthly reimbursement cap; employees choose their own ACA-compliant plan from HealthCare.gov or off-exchange. ICHRA is particularly effective for Kansas businesses with employees spread across multiple cities or rural counties where a single group plan network may not cover everyone well.

ICHRA became available January 1, 2020 under IRS final rules and has grown rapidly among Kansas small businesses as an alternative to traditional group coverage. The mechanics are straightforward: the employer establishes the ICHRA, sets monthly allowance amounts by employee class (full-time, part-time, seasonal, etc.), and employees submit premium receipts for reimbursement up to the monthly cap. Reimbursements are excluded from both employer payroll taxes and employee income taxes, producing tax efficiency comparable to traditional group coverage. There is no federal cap on the ICHRA reimbursement amount — Kansas employers can set any monthly allowance that fits their budget.

The critical ICHRA limitation for Kansas employers: employees who receive ICHRA reimbursements cannot simultaneously receive advance premium tax credits on the HealthCare.gov individual marketplace. If an employee would qualify for a substantial APTC — typically those below 400% of the federal poverty level — the ICHRA reimbursement may be worth less to them than the marketplace subsidy they’d receive without it. Employees weighing this tradeoff can review how subsidies and enrollment work in the Kansas marketplace enrollment guide. Kansas employers considering ICHRA should model both the employer’s tax savings and the employee’s net cost at different income levels before switching from or foregoing a group plan.

The Kansas SHOP Marketplace and the Small Business Tax Credit

The federal SHOP (Small Business Health Options Program) marketplace is available to Kansas employers with 1 to 50 full-time equivalent employees at HealthCare.gov/small-businesses. The primary advantage is the Small Business Health Care Tax Credit — up to 50% of employer premium contributions for employers with fewer than 25 FTEs and average wages below $62,000 in 2026. The credit requires SHOP enrollment to claim in most cases.

The Small Business Health Care Tax Credit phases out as the employer’s average wages rise above $31,000 and as FTE count rises above 10. Kansas employers with exactly 10 or fewer FTEs and average wages at or below $31,000 receive the full 50% credit. A Kansas employer contributing $300 per month per employee to SHOP coverage for 8 employees would generate a $14,400 annual federal tax credit — a meaningful offset to premium costs. Tax-exempt Kansas organizations (nonprofits, religious organizations) receive a 35% credit instead of 50%. The credit is available for a maximum of two consecutive tax years, after which the employer must continue coverage without the credit or switch to a direct carrier arrangement.

In practice, many Kansas small businesses find that SHOP offers a narrower selection of plans than the direct carrier market. BCBS Kansas, for example, offers its full small group product portfolio through direct employer enrollment — BCBS Kansas does not require SHOP enrollment. Kansas employers should compare the tax credit value against any premium or plan design differences before committing to SHOP enrollment. The tax credit value can be modeled at a specific FTE count, average wage, and contribution level.

Get a Kansas Small Business Health Insurance Quote

Comparing group plans from BCBS Kansas, BCBS Kansas City, Medica, and United Healthcare — and modeling ICHRA vs. group plan cost at a specific employee count and income mix — clarifies SHOP tax credit eligibility and the best structure at no extra cost over enrolling directly.

Kansas Small Business Health Insurance Costs for 2026

Kansas small group health insurance typically costs $400–$750 per employee per month for single coverage before any employer contribution, depending on carrier, plan design, and employee age mix. Kansas employers typically contribute 50%–75% of the employee-only premium — about $200–$560 per employee per month — with the remainder deducted pre-tax from employee paychecks. Family coverage adds $800–$1,400 per employee-family per month at unsubsidized small group rates.

Kansas uses community rating for small group health insurance, meaning premiums are based on the composite age of enrolled employees rather than individual health history. A Kansas small business with younger employees — average age 30–35 — will pay meaningfully less per employee than one with average employee age 45–50, even on the same plan. The Kansas Insurance Department reviews and approves small group rate filings annually; BCBS Kansas, BCBS Kansas City, and Medica all filed 2026 small group rate increases in line with the broader Kansas market trend.

Employer premium contributions are 100% deductible as a business expense on the Kansas business tax return and the federal return. Employees pay their share through pre-tax payroll deductions, reducing their taxable income. For a Kansas small business owner in the 24% federal bracket contributing $350 per month per employee to group health coverage, the after-tax cost is approximately $266 per employee per month — a meaningful difference from the gross premium figure. ICHRA reimbursements receive the same tax treatment: excluded from employer payroll taxes and employee income taxes when used for qualifying individual coverage.

1–10 Employees

QSEHRA or ICHRA

Micro-employers under 10 FTEs often find QSEHRA or ICHRA simpler and more cost-predictable than a full group plan. There is no minimum contribution and no group participation requirement, and employees choose their own plan on HealthCare.gov. QSEHRA 2026 limits are $6,350/year single and $12,800/year family.

2–25 Employees

SHOP + Tax Credit

Small Kansas businesses with fewer than 25 FTEs and average wages below $62,000 may qualify for the Small Business Health Care Tax Credit — up to 50% of employer contributions — through SHOP enrollment. The full 50% credit applies at 10 or fewer FTEs with average wages at or below $31,000, for a maximum of two consecutive tax years.

5–50 Employees

Direct Group Plan

Kansas businesses with 5 or more employees typically have the best plan selection and network options through a direct group carrier — BCBS Kansas statewide, BCBS Kansas City in the KC metro, or Medica in select markets. BCBS Kansas Premier Blue PPO is available in the group market, community-rated with no health underwriting, and typically requires 75% minimum employee participation.

50+ Employees

Self-Insured

Larger Kansas employers with the cash flow to absorb claims risk often self-insure with stop-loss coverage, paying employee medical claims directly rather than fixed premiums. This avoids state premium taxes and small group rating rules, but requires enough enrolled employees to spread risk — usually 50 or more FTEs — and a stop-loss policy to cap catastrophic exposure.

Frequently Asked Questions

Are Kansas small businesses required to offer health insurance?

No. Kansas small businesses with fewer than 50 full-time equivalent employees are not required to offer health insurance under the ACA’s employer mandate — the mandate applies only to employers with 50 or more FTEs, known as Applicable Large Employers (ALEs). Kansas does not have a state-level employer mandate beyond the federal ACA requirement. Offering group health insurance is entirely voluntary for Kansas small businesses under 50 FTEs, but doing so provides a federal tax deduction for the employer’s premium contribution and can significantly help with hiring and retention in the Kansas labor market.

What is ICHRA and can Kansas small businesses use it?

An Individual Coverage Health Reimbursement Arrangement (ICHRA) is an IRS-approved employer benefit that allows Kansas small businesses of any size to reimburse employees tax-free for individual health insurance premiums and eligible medical expenses. Instead of buying a group plan, the employer sets a monthly reimbursement amount — for example, $400 per month per employee — and employees purchase their own ACA-compliant plan through HealthCare.gov or off-exchange. ICHRA is particularly attractive for Kansas businesses with geographically dispersed employees, since each employee can choose a plan with the best network for their own location. Employees who receive ICHRA reimbursements cannot simultaneously receive advance premium tax credits on the marketplace.

Does BCBS Kansas offer small group health insurance?

Yes. Blue Cross and Blue Shield of Kansas offers small group health insurance plans for Kansas employers with 2 to 50 eligible employees. BCBS Kansas small group plans include HMO, PPO (Premier Blue), and EPO designs across Bronze, Silver, and Gold equivalent metal tiers. BCBS Kansas is the dominant small group carrier in Kansas, particularly outside the Kansas City metro, due to its statewide provider network covering all 105 counties and its contracts with The University of Kansas Health System, Stormont Vail Health, and Via Christi (Ascension Kansas). BCBS Kansas small group enrollment does not use the SHOP marketplace — employers enroll directly with BCBS Kansas.

What is the Kansas SHOP marketplace?

The Kansas SHOP (Small Business Health Options Program) marketplace is the federal small business exchange available to Kansas employers with 1 to 50 full-time equivalent employees. It is accessed through HealthCare.gov/small-businesses rather than the individual marketplace. The primary advantage of the SHOP marketplace for Kansas small businesses is eligibility for the Small Business Health Care Tax Credit, which provides a tax credit of up to 50% of employer premium contributions (35% for tax-exempt organizations) for employers with fewer than 25 FTEs and average wages below $62,000. In practice, most Kansas small businesses find the direct carrier market — BCBS Kansas, Medica, and others — offers more plan options than the SHOP exchange.

How much does small business health insurance cost in Kansas?

Small business health insurance in Kansas typically costs $400–$750 per employee per month for a single-employee plan before any employer contribution, depending on the carrier, plan design, age of employees, and geographic rating area. The employer’s average contribution in Kansas is typically 50%–75% of the employee-only premium, with employees paying the remainder through pre-tax payroll deductions. A Kansas employer contributing 60% of a $550/month Silver-equivalent small group premium pays $330 per employee per month — deductible as a business expense. Family coverage adds $800–$1,400 per month per employee family at full unsubsidized small group rates.

More Kansas Health Insurance Resources

Explore related guides covering the complete Kansas health insurance overview, strategies for finding affordable coverage and subsidies, carrier rankings across BCBS Kansas and competitors, and PPO plan options for employers and employees who need broader network access.

Complete 2026 Kansas health insurance overview — KanCare, marketplace, employer, and PPO paths.

Affordable Kansas Health InsuranceSubsidy options for Kansas employees who leave group coverage and buy individual plans.

Best Health Insurance in KansasBCBS Kansas, Ambetter, UnitedHealthcare, Oscar, and Cigna compared on network and price.

PPO Health Insurance PlansOff-exchange PPO options for Kansas employers and employees who need broader network access.

Compare Kansas Small Business Health Insurance Plans

Comparing BCBS Kansas, BCBS Kansas City, Medica, and United Healthcare group plans — and modeling ICHRA vs. group plan savings by employee count and income mix — clarifies SHOP tax credit eligibility at no extra cost over enrolling directly.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Kansas businesses. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.