Kansas Health Insurance 2026: Plans, Marketplace & Costs

Kansas health insurance in 2026 sits at the intersection of three forces that shape every coverage decision in the state: Kansas uses the federal HealthCare.gov marketplace rather than running its own exchange, Kansas is one of nine non-expansion states leaving an adult coverage gap below 100% of the federal poverty level, and Kansas health insurance marketplace premiums rose by a weighted average of 26.6% for 2026 — among the largest gross rate increases in the country. About 206,000 Kansans selected Kansas health insurance plans during the most recent open enrollment period, with the benchmark Silver premium for a family of four climbing from $1,848 to $2,381 per month before subsidies. Five carriers compete on the 2026 Kansas marketplace: Blue Cross and Blue Shield of Kansas, Blue Cross and Blue Shield of Kansas City, Ambetter from Sunflower Health Plan, UnitedHealthcare, Oscar Health, and Cigna — Aetna CVS Health exited the Kansas individual market for 2026. KanCare, the state’s Medicaid managed care program, covers about 450,000 Kansans through three managed care organizations: Sunflower Health Plan, Aetna Better Health, and Healthy Blue. This guide covers every Kansas health insurance path for 2026.

What brings you here today?

Which Kansas carrier is best?

BCBS Kansas, Ambetter, UnitedHealthcare, Oscar compared

See carriers ↓HealthCare.gov: Kansas Uses the Federal Marketplace

Kansas does not operate a state-based exchange. All Kansas individual and family marketplace enrollment runs through HealthCare.gov, the federal platform also used by 31 other states. Open enrollment for plan year 2027 runs November 1, 2026 through January 15, 2027, with coverage starting January 1, 2027 for enrollments completed by December 15. Kansans who miss open enrollment can still qualify for a Special Enrollment Period after a qualifying life event.

The Kansas Insurance Department, headed by Insurance Commissioner Vicki Schmidt, reviews and approves Kansas health insurance marketplace rate filings each year but does not run the enrollment platform itself — that responsibility sits with the federal Centers for Medicare and Medicaid Services (CMS). The Kansas Insurance Department’s role is regulatory: reviewing actuarial filings, enforcing market conduct rules, and publishing the annual Kansas Health Insurance Market Report. The 2026 market report — released in advance of open enrollment — documented the 26.6% weighted average rate increase across the five participating carriers and explained the actuarial drivers behind it.

About 206,000 Kansans selected marketplace plans during the most recent open enrollment, making Kansas a mid-sized federal marketplace state. Roughly 92% of Kansas marketplace enrollees receive advance premium tax credits (APTC) that lower monthly premiums, and a meaningful share also receive cost-sharing reductions (CSR) that lower deductibles and out-of-pocket maximums on Silver-tier plans. The enhanced subsidies enacted in 2021 are set to expire on December 31, 2025 unless Congress extends them — a potential change that would significantly increase out-of-pocket premium costs for Kansas enrollees earning between 400% and 600% of the federal poverty level.

Kansas Health Insurance Carriers for 2026

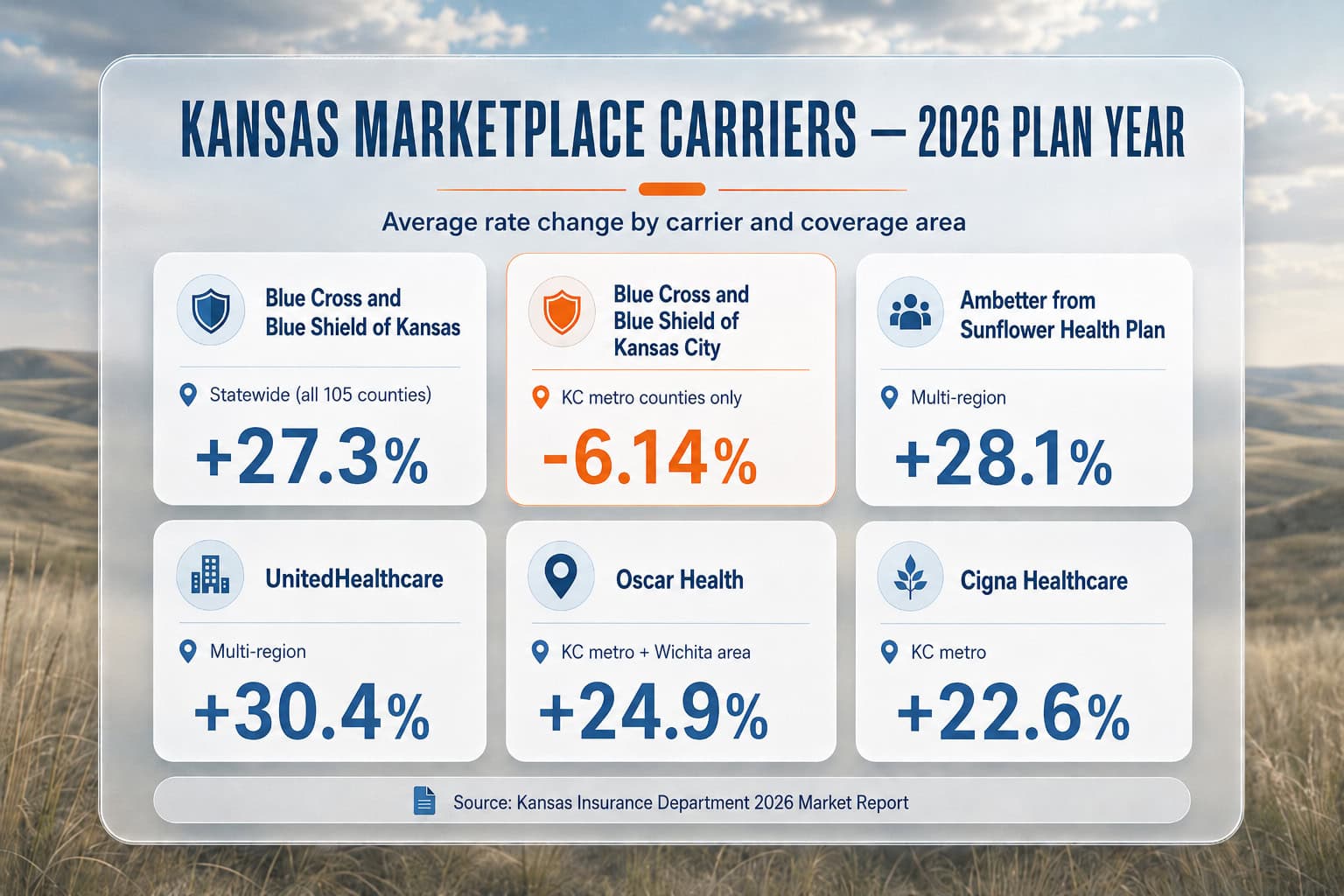

Five carriers offer 2026 Kansas marketplace plans: Blue Cross and Blue Shield of Kansas (statewide), Blue Cross and Blue Shield of Kansas City (Kansas City metro counties only), Ambetter from Sunflower Health Plan, UnitedHealthcare, Oscar Health, and Cigna. Aetna CVS Health left the Kansas marketplace for 2026 — Aetna members must select a new carrier. BCBS Kansas is the only carrier with statewide network coverage across all 105 Kansas counties.

The Kansas carrier landscape is split geographically. Blue Cross and Blue Shield of Kansas — headquartered in Topeka and the historical statewide Blues plan for the state — contracts with virtually every Kansas hospital and provider system including The University of Kansas Health System, Stormont Vail Health, and Via Christi (Ascension Kansas). Blue Cross and Blue Shield of Kansas City is a separate, independently-owned Blues plan that serves the Kansas City metro on both sides of the state line — including Johnson, Wyandotte, Leavenworth, and Miami counties in Kansas — but does not operate statewide. BCBS Kansas City’s average 2026 Kansas health insurance rate change was a 6.14% decrease, the only carrier in the state with a rate reduction.

Ambetter from Sunflower Health Plan, the Centene-owned marketplace brand, competes primarily on price in the subsidized Silver and Bronze tiers. Ambetter’s narrow-network design produces lower premiums but a smaller provider list than BCBS Kansas. UnitedHealthcare offers the cheapest 2026 Bronze plan in Kansas at $442 per month for a 40-year-old, according to Kansas Insurance Department filings. Oscar Health and Cigna round out the marketplace with regional plans concentrated in the Kansas City metro and Wichita-area counties. The HealthCare.gov enrollment portal shows which specific carriers offer plans in each Kansas zip code.

Carrier Comparison at a Glance

| Carrier | 2026 Coverage Area | 2026 Rate Change |

|---|---|---|

| Blue Cross and Blue Shield of Kansas | Statewide (all 105 counties) | +27.3% (avg) |

| Blue Cross and Blue Shield of Kansas City | KC metro counties only | -6.14% |

| Ambetter from Sunflower Health Plan | Multi-region | +28.1% (avg) |

| UnitedHealthcare | Multi-region | +30.4% (avg) |

| Oscar Health | KC metro + Wichita area | +24.9% (avg) |

| Cigna Healthcare | KC metro | +22.6% (avg) |

Coverage area maps shift year-to-year as carriers add or drop counties. Before enrolling, confirm your zip code falls within the carrier’s 2026 service area on HealthCare.gov — Ambetter, UnitedHealthcare, Oscar, and Cigna all have at least some counties where they do not offer plans, particularly in Western Kansas counties along the Colorado border. Blue Cross and Blue Shield of Kansas is the only carrier that does not have this coverage gap.

Coverage Paths: KanCare, Marketplace, Employer, and the Coverage Gap

Most Kansans get Kansas health insurance through one of four paths: employer-sponsored group coverage (the largest single source statewide), the HealthCare.gov marketplace with subsidies (about 206,000 enrollees), KanCare Medicaid (about 450,000 enrollees), or Medicare for residents 65 and older. Because Kansas has not expanded Medicaid, adults earning less than 100% of the federal poverty level — but above the KanCare income limit — fall into the coverage gap and may not qualify for any program.

Marketplace

HealthCare.gov Marketplace

Individual and family ACA-compliant plans with advance premium tax credit (APTC) subsidies for households earning 100%–400% of the federal poverty level, and currently higher under enhanced subsidies. Five carriers compete statewide, subsidies cap premiums as a percentage of income, and Special Enrollment Periods are available year-round for qualifying life events.

KanCare Medicaid

KanCare for Kansans Below the Income Limit

Kansas Medicaid managed care covers about 450,000 Kansans through three MCOs: Sunflower Health Plan, Aetna Better Health of Kansas, and Healthy Blue. Most enrollees pay no premium. Parents qualify up to 38% of FPL and children up to 166% of FPL (under age 1), with year-round enrollment and no open-enrollment window.

Employer Group

Employer-Sponsored Coverage

The largest single source of health insurance for Kansas working-age adults, including the State Employee Health Plan (SEHP) covering about 89,000 state workers and dependents through Aetna and BCBS Kansas. Self-insured large employers dominate, the small group market is available off-exchange, and ICHRA is growing as a Kansas small business health insurance alternative.

Medicare

Medicare for Kansans 65 and Older

Kansans aged 65 and older — and some younger residents with qualifying disabilities — get coverage through Medicare rather than the marketplace or KanCare. Original Medicare pairs with Medigap and Part D, while Medicare Advantage plans from BCBS Kansas, Aetna, and others bundle coverage. Enrollment runs through the federal Medicare program, not HealthCare.gov.

The Kansas Coverage Gap

Kansas is one of nine non-expansion states. Adults below 100% of the federal poverty level — about $15,650 for a single adult in 2026 — generally do not qualify for KanCare unless they are pregnant, disabled, 65 or older, or have a dependent child and household income at or below 38% of FPL. They also do not qualify for marketplace subsidies, which start at 100% of FPL. About 40,000 to 50,000 Kansans are estimated to fall in this coverage gap. Kansas has debated Medicaid expansion repeatedly since 2014 without passing it.

The 2026 Kansas Rate Increase: 26.6% Explained

Kansas marketplace premiums rose by a weighted average of 26.6% for 2026 — among the largest gross rate increases in the country. The benchmark Silver premium for a family of four climbed from $1,848 per month in 2025 to $2,381 per month in 2026 before subsidies. The drivers: anticipated expiration of enhanced ACA subsidies, rising claim costs, prescription drug inflation, and Kansas being a non-expansion state.

The Kansas Insurance Department’s 2026 market report identifies four main factors behind the rate increase. First, the enhanced premium tax credits enacted in 2021 are scheduled to expire at the end of 2025, and carriers priced 2026 plans assuming reduced subsidy support — which typically pulls healthier enrollees out of the marketplace and concentrates risk among sicker enrollees who remain. Second, projected claim costs per member per month rose from $589.04 in 2024 to $637.85 in 2026, an 8.3% medical trend. Third, prescription drug costs — particularly GLP-1 weight loss medications and high-cost specialty drugs — drove an outsized portion of the claim cost increase. Fourth, Kansas’s non-expansion status concentrates higher-acuity adults in the individual market who would otherwise be covered by Medicaid in expansion states.

What this means for Kansans receiving subsidies: about 92% of marketplace enrollees receive advance premium tax credits that cap monthly premiums as a percentage of household income. For these enrollees, the 26.6% gross rate increase is largely absorbed by larger federal subsidy payments — out-of-pocket increases are typically much smaller. For the 8% of unsubsidized enrollees — often self-employed Kansans or early retirees with incomes above the subsidy threshold — the full 26.6% increase hits the monthly premium. For a 40-year-old non-smoker earning $80,000 in Wichita, that translates to roughly $1,400 in additional annual premium for the same Silver plan compared to 2025.

Get a Kansas Health Insurance Quote

Comparing HealthCare.gov plans from all five Kansas carriers with subsidy calculations applied — and verifying which plans include your providers at The University of Kansas Health System, Stormont Vail, or Via Christi Ascension — helps identify the right fit at no extra cost over enrolling directly.

PPO Plans in Kansas: Off-Exchange Options

Most Kansas marketplace plans are HMO or EPO designs with narrow networks and primary care referral requirements. For Kansans who want broader provider access and no referrals, PPO plans are available off-exchange — including legacy BCBS Kansas Premier Blue PPO products, BCBS Kansas City Preferred Care Blue PPO, and Cigna PPO options. Off-exchange PPO plans do not qualify for premium tax credits but offer broader provider access.

Blue Cross and Blue Shield of Kansas offers Premier Blue commercial PPO products primarily through group employer plans, with some individual PPO options available off-exchange. Blue Cross and Blue Shield of Kansas City sells multiple PPO products: Preferred Care Blue, Preferred Care, Blue Access, and Blue Select Plus — all of which are accepted at The University of Kansas Health System and most KC-metro hospitals. For Kansans whose providers contract on a PPO basis but not HMO, an off-exchange PPO can be the only viable option even at a higher unsubsidized premium. Compare Kansas PPO plans through ForHealthInsurance.com — PPO availability varies by zip code and county.

How to Enroll in Kansas Health Insurance

Kansas residents enroll through HealthCare.gov for marketplace plans, through KanCare Connect for KanCare Medicaid and CHIP, directly through an employer for group coverage, or off-exchange for PPO plans. Open enrollment for plan year 2027 begins November 1, 2026 and ends January 15, 2027. Outside open enrollment, a qualifying life event triggers a 60-day Special Enrollment Period.

Gather your information

You’ll need household size, estimated 2026 household income, Social Security numbers for everyone applying, and your current employer’s coverage offer (if any) including whether it meets the ACA affordability threshold.

Compare plans

Use HealthCare.gov’s plan compare tool to see all carriers available in your Kansas zip code, with subsidy estimates applied. Comparing quotes across all five carriers side by side shows the real cost difference after subsidies.

Verify your providers

The biggest enrollment mistake in Kansas is picking a plan whose network excludes your current doctor or hospital. Confirm in-network status at The University of Kansas Health System, Stormont Vail, Via Christi Ascension, or wherever you receive care before enrolling.

Submit your application

Enroll at HealthCare.gov or apply for KanCare at KanCare.ks.gov. Coverage starts January 1 for enrollments completed by December 15; otherwise February 1.

Frequently Asked Questions

Does Kansas use HealthCare.gov for marketplace enrollment?

Yes. Kansas uses the federal HealthCare.gov platform for individual and family marketplace enrollment — Kansas does not operate its own state-based exchange. Kansas residents enroll, compare plans, calculate subsidies, and pay premiums through HealthCare.gov. Open enrollment for plan year 2027 will run November 1, 2026 through January 15, 2027, with coverage starting January 1, 2027 for enrollments completed by December 15. About 206,000 Kansans selected marketplace plans during the most recent open enrollment, making Kansas a mid-sized federal marketplace state.

Did Kansas expand Medicaid under the ACA?

No. Kansas is one of nine states that has not expanded Medicaid under the Affordable Care Act, alongside Alabama, Florida, Mississippi, South Carolina, Tennessee, Texas, Wisconsin (partial), and Wyoming. This creates a coverage gap in Kansas where adults with incomes below 100% of the federal poverty level — about $15,650 for a single adult in 2026 — generally do not qualify for either KanCare Medicaid or marketplace subsidies. Parents in Kansas qualify for KanCare only if their household income is at or below 38% of the federal poverty level, one of the strictest thresholds in the country. Adults without dependent children generally do not qualify for KanCare regardless of income unless they are disabled, pregnant, or 65 or older.

How much will Kansas health insurance cost in 2026?

Kansas marketplace premiums rose by a weighted average of 26.6% for 2026 — among the largest gross rate increases in the country. The benchmark Silver plan for a family of four in Kansas increased from $1,848 per month in 2025 to $2,381 per month in 2026 before subsidies are applied, a 28.9% increase. For a 40-year-old individual, the cheapest Bronze plan in Kansas starts at about $461 per month from UnitedHealthcare. Most Kansans receiving advance premium tax credits will see smaller out-of-pocket increases — about 92% of Kansas marketplace enrollees receive subsidies that cap premiums as a percentage of household income.

Which carriers offer Kansas marketplace plans in 2026?

Five carriers offer 2026 Kansas marketplace plans: Blue Cross and Blue Shield of Kansas (statewide), Blue Cross and Blue Shield of Kansas City (covering the Kansas City metro area only, including Johnson and Wyandotte counties), Ambetter from Sunflower Health Plan, UnitedHealthcare, Oscar Health, and Cigna Healthcare. Aetna CVS Health left the Kansas marketplace for 2026 — Aetna members in Kansas must select a new carrier through HealthCare.gov. BCBS Kansas is the only carrier with statewide coverage across all 105 Kansas counties; the others vary by region.

Does Kansas have a state individual mandate penalty?

No. Kansas does not have a state individual mandate or penalty for going without health insurance. The federal mandate penalty has been $0 since 2019, and only six states plus Washington DC have enacted their own coverage requirement — Massachusetts, New Jersey, California, Rhode Island, Vermont, and DC. Kansas residents who go uninsured for a full year owe no state or federal tax penalty for being uncovered, though they remain responsible for 100% of any medical expenses incurred while uninsured and may be subject to underwriting if they later apply for non-ACA coverage.

Explore Kansas Coverage In Depth

Related guides cover Kansas marketplace enrollment through HealthCare.gov, strategies for finding affordable coverage and subsidies, carrier rankings across BCBS Kansas and its competitors, and PPO options for residents who want broader provider access.

HealthCare.gov enrollment, open enrollment windows, subsidies, and carrier comparison for Kansas.

Affordable Kansas Health Insurance2026 Kansas premium increase, subsidies, KanCare, and the coverage gap explained.

Best Health Insurance in KansasBCBS Kansas, Ambetter, UnitedHealthcare, Oscar, and Cigna compared on price and network.

PPO Health Insurance PlansOff-exchange PPO plans for Kansas residents — quotes by zip, no referrals required.

Compare 2026 Kansas Health Insurance Plans

Comparing all five Kansas carriers with subsidy calculations applied — and confirming which plans cover providers at The University of Kansas Health System, Stormont Vail, or Via Christi Ascension — narrows the options quickly, at no extra cost over enrolling directly.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Kansas residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.