Illinois Health Insurance Marketplace 2026: Get Covered Illinois Enrollment Guide

The Illinois health insurance marketplace moved to a state-run platform on January 1, 2026. Get Covered Illinois replaces HealthCare.gov as the only place Illinois residents can shop marketplace plans and apply for premium tax credits. This guide walks through what changed, who can enroll, when open enrollment runs, which carriers participate, and how to complete an application without getting tripped up by the 2026 transition.

What brings you here today?

I want to enroll in a marketplace plan

Compare 7 carriers and 285 plans on Get Covered IL

Get a quote →What Get Covered Illinois Is

Get Covered Illinois is the state’s official health insurance marketplace, launched January 1, 2026 to replace HealthCare.gov for Illinois residents. The Centers for Medicare and Medicaid Services approved Illinois’ transition to a state-based marketplace in 2025, and enrollment for 2026 plans began November 1, 2025 on the new platform. Get Covered Illinois handles plan shopping, premium tax credit applications, and Medicaid routing through a single integrated system.

The shift gives Illinois control over enrollment periods, special enrollment pathways, and outreach in ways the federal exchange could not. Get Covered Illinois invested $6.5 million in a statewide navigator grant program, embedding certified navigators in community organizations across the state to provide free enrollment help. The call center at 1-866-311-1119 supports enrollment in English, Spanish, and up to 200 additional languages through live interpretation.

Why this matters for Illinois residents

Anyone who enrolled in marketplace coverage through HealthCare.gov in past years needs to use getcovered.illinois.gov for 2026 and beyond. Existing HealthCare.gov accounts do not transfer automatically — residents must claim their account on the new state platform or create a new one.

Illinois joins seventeen other states plus the District of Columbia running their own marketplace platforms. The practical difference is that state-based marketplaces can extend enrollment deadlines, build state-specific special enrollment pathways like the Tax Time Easy Enrollment Program, and tailor outreach to local populations. The plans themselves, the carriers, and the federal premium tax credit rules are the same as on HealthCare.gov — only the enrollment interface and timeline are different.

2026 Open Enrollment Through Get Covered Illinois

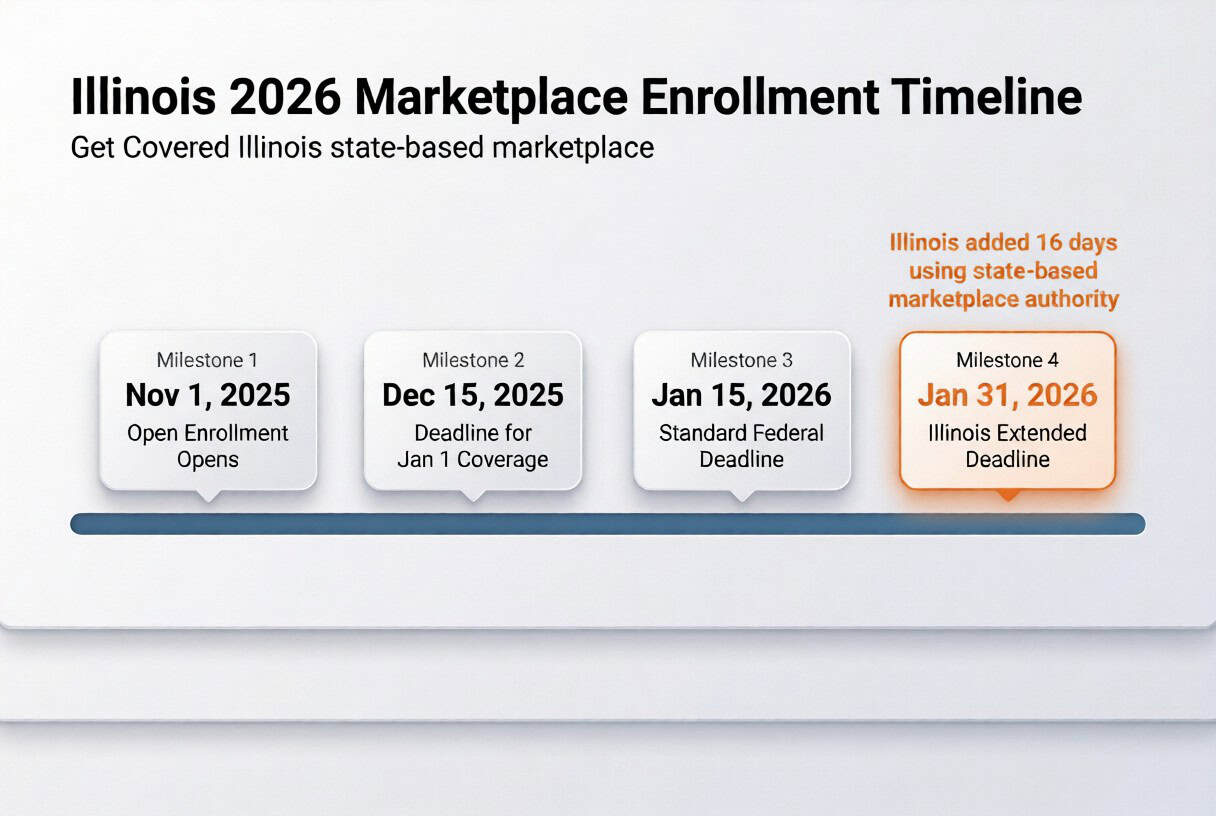

Open enrollment for 2026 Illinois marketplace coverage ran from November 1, 2025 through January 31, 2026. That sixteen-day extension past the federal January 15 deadline was made possible by Illinois’ new state-based marketplace authority, which lets the state adjust enrollment windows independently of HealthCare.gov rules. The extension gave Illinois residents extra time to compare seven carriers and 285 plan options after the carrier exodus that closed out 2025.

| Enrollment Date | Coverage Start | Window |

|---|---|---|

| November 1, 2025 | January 1, 2026 | Open Enrollment opens |

| December 15, 2025 | January 1, 2026 | Deadline for January 1 coverage |

| January 15, 2026 | February 1, 2026 | Standard federal deadline |

| January 31, 2026 | March 1, 2026 | Illinois extended deadline |

Enrolling by December 15 secured coverage starting January 1. Applications between December 16 and January 15 took effect February 1. Illinois’ extension created a third window: applications between January 16 and January 31 took effect March 1. After January 31, marketplace enrollment required a qualifying life event or the Tax Time Easy Enrollment pathway described below.

Existing enrollees who took no action by January 31 were automatically renewed into a similar plan from a participating carrier. Auto-renewal is straightforward when the prior carrier still operates in Illinois, but anyone who had Aetna CVS, Aetna Life, Health Alliance, or Quartz in 2025 needed to actively select a new plan — those four carriers exited the state at the end of 2025 and could not auto-renew their members.

Plan Categories and Carriers on Get Covered Illinois

Get Covered Illinois offers 285 unique plan options across seven on-exchange carriers for 2026, sorted into Bronze, Silver, Gold, and Catastrophic metal tiers. Platinum-tier plans were not filed by any carrier for the Illinois on-exchange market in 2026, per the Illinois Department of Insurance. Catastrophic plans remain available to applicants under 30 and to those with hardship exemptions, though premium tax credits cannot be applied to that tier.

Bronze

Lowest PremiumRoughly 60 percent of expected costs covered by the plan. Lowest monthly premiums, highest deductibles (typically $7,000 to $9,200 per individual in 2026). Best for healthy enrollees who want catastrophic protection but do not qualify for cost-sharing reductions.

Silver

Best With CSRCovers about 70 percent of expected costs. Critical tier for anyone between 100 and 250 percent of the federal poverty level — cost-sharing reductions only apply to Silver plans and can dramatically lower deductibles, copays, and out-of-pocket maximums.

Gold

Lower DeductibleAbout 80 percent coverage. Higher premiums but deductibles drop to roughly $1,500 to $3,000. Best for households who expect regular medical use, manage a chronic condition, or want more predictable costs and do not qualify for Silver CSRs.

Catastrophic

Under 30 OnlyAvailable to Illinois residents under 30 or those with hardship exemptions. Very low premiums but a deductible equal to the federal annual out-of-pocket maximum. No premium tax credits apply. Functions as worst-case-only protection for young, healthy enrollees.

Among carriers, Blue Cross Blue Shield of Illinois (operated by Health Care Service Corporation) is the only insurer offering HMO, POS, and PPO plans on the Illinois health insurance marketplace, with a network reaching all 102 Illinois counties. Cigna HealthCare of Illinois offers HMO plans in most counties but pulled out of Cook County for 2026. Ambetter from Celtic discontinued its Bronze tier in Illinois for 2026. Molina Healthcare, Oscar Health Plan, UnitedHealthcare, and MercyCare round out the seven participating carriers, with service areas varying significantly by county. The Illinois Department of Insurance publishes the annual on-exchange analysis confirming which carriers and metal tiers are offered statewide.

Premium Tax Credits and Subsidies

Premium tax credits remain the single biggest cost driver on Get Covered Illinois. Most Illinois marketplace enrollees still qualify for substantial monthly savings even after the enhanced subsidies expired at the end of 2025, but the math changed significantly. Illinois families pay roughly $130 per month more on average for 2026 coverage than they did in 2025 — a year-over-year increase near 50 percent driven by the subsidy expiration, not by carrier rate hikes alone.

| Household Income (Family of 4) | % FPL | Assistance Available |

|---|---|---|

| Up to $43,000 | Under 138% | Medicaid / Family Care |

| $43,000–$62,400 | 138%–200% | APTC + Full Cost-Sharing Reductions |

| $62,400–$78,000 | 200%–250% | APTC + Limited Cost-Sharing Reductions |

| $78,000–$124,800 | 250%–400% | APTC only |

| Over $124,800 | Over 400% | Unsubsidized marketplace |

Illinois fully expanded Medicaid under the Affordable Care Act in 2014, so adults with household income up to 138 percent of the federal poverty level qualify for Medicaid coverage through the Department of Healthcare and Family Services rather than marketplace plans. Applicants who fall below the marketplace threshold get routed automatically to Medicaid eligibility within the Get Covered Illinois application flow. Children up to 318 percent of FPL qualify for All Kids, the Illinois CHIP program, including children regardless of immigration status.

Cost-sharing reductions (CSRs) deserve specific attention. Households between 100 and 250 percent of FPL who choose a Silver-tier plan get reductions on deductibles, copays, and out-of-pocket maximums on top of premium tax credits. A Silver plan with full CSR for a family of four near 150 percent of poverty can have an effective deductible under $500 rather than the standard $5,000-plus. CSRs do not transfer to Bronze, Gold, or Catastrophic tiers — anyone eligible should choose Silver to capture the benefit.

Compare Subsidized Plans on Get Covered Illinois

Running a subsidy estimate before browsing plans is the single biggest cost-saving move on the 2026 Illinois marketplace. A licensed Illinois broker can verify subsidy eligibility, compare seven carriers, and complete enrollment at no extra cost.

Marketplace Enrollment Step-by-Step

Completing a Get Covered Illinois application takes 30 to 60 minutes for most households, longer for mixed-status families or self-employed applicants who need to estimate annual income carefully. The platform routes Medicaid-eligible applicants to the Department of Healthcare and Family Services automatically rather than requiring a separate application, and verifies household composition against state databases when possible.

- Window shop first. Browse 2026 plans by ZIP code without creating an account. The plan finder estimates subsidies based on income and household size before any personal information is submitted.

- Create an account. HealthCare.gov accounts do not transfer to Get Covered Illinois automatically. Residents who had federal exchange coverage in 2025 either claim their pre-populated state account or create a new one.

- Complete the application. Provide household size, income (current and projected annual), Social Security numbers for all applicants, immigration status documents for non-citizens, and any current coverage details.

- Review eligibility results. The system determines whether the household qualifies for Medicaid, All Kids, premium tax credits, cost-sharing reductions, or unsubsidized coverage only. Determination is usually same-day.

- Compare plans and enroll. Use the plan finder to compare carriers, networks, and total annual cost (premium plus expected out-of-pocket). Confirm preferred doctors and hospitals are in-network before selecting.

- Pay the first premium. Coverage activates only after the first month’s premium is paid to the chosen carrier directly. Most carriers offer auto-pay setup at the same time.

Free enrollment help is available statewide. Illinois invested $6.5 million in a navigator grant program through HFS and the Illinois Department of Insurance, embedding certified navigators in community organizations across the state. Brokers licensed in Illinois — including ForHealthInsurance.com — can also help residents compare plans and complete applications at no cost. Neither navigators nor brokers can charge for marketplace enrollment assistance.

Special Enrollment Periods (Including Tax Time)

Marketplace enrollment outside the November–January window normally requires a qualifying life event that triggers a 60-day special enrollment period. Illinois added a unique state-only pathway for 2026: the Tax Time Easy Enrollment Program, which lets residents enroll without a traditional life event if their state tax return indicates the household is uninsured. This option was not possible under the federal exchange and became available only with the transition to a state-based marketplace.

Qualifying life events that open a 60-day SEP

Marriage, divorce or legal separation, birth or adoption of a child, death of a household member, permanent move into Illinois or to a different rating area, loss of other health coverage (job loss, aging off a parent’s plan at 26, COBRA expiration), changes in income that affect subsidy eligibility, and changes in citizenship or lawful presence status.

The Tax Time Easy Enrollment Program works on a different trigger. When Illinois residents file their state income tax return, they can check a box indicating the household lacked health insurance for some or all of the prior year and request enrollment help. Get Covered Illinois follows up with personalized outreach, and the household gets a special enrollment opportunity even if they have no other qualifying event. Illinois is currently the only state offering this specific pathway at scale.

| SEP Trigger | Window | Documentation |

|---|---|---|

| Loss of job-based coverage | 60 days before or after | Letter from employer or COBRA notice |

| Marriage | 60 days after | Marriage certificate |

| Birth or adoption | 60 days after | Birth certificate or adoption papers |

| Permanent move | 60 days after | Proof of prior coverage + new address |

| Income change | Year-round | Pay stubs or self-attestation |

| Tax Time Easy Enrollment | Triggered by state tax filing | State tax return checkbox |

Documentation matters for most SEP triggers — Get Covered Illinois typically requires proof within 30 days of application. Without documentation, the special enrollment can be reversed and coverage canceled retroactively. Brokers and navigators help match the right SEP category to a resident’s situation and confirm which documentation will be accepted.

Common Marketplace Enrollment Mistakes in Illinois

The 2026 transition introduced four specific mistakes Illinois residents are more likely to make than residents of states using stable federal or longer-running state-based marketplaces. The Illinois health insurance marketplace works differently from HealthCare.gov in ways that catch first-time Get Covered Illinois applicants.

Trying to enroll through HealthCare.gov

The federal site stopped accepting Illinois applications at the end of 2025. Bookmarked HealthCare.gov account URLs no longer work for Illinois — use getcovered.illinois.gov for all 2026 enrollment.

Auto-renewing into a discontinued carrier

Aetna CVS, Aetna Life, Health Alliance, and Quartz exited Illinois at the end of 2025. Members of those four carriers needed to actively select a new plan; auto-renewal did not work for them.

Keeping a Cigna plan in Cook County

Cigna pulled out of Cook County for 2026. Chicago-area Cigna members got auto-renewed to a different plan that may have a substantially different network, deductible, or premium.

Assuming DACA recipients remain eligible

Federal rules ended marketplace eligibility for DACA recipients on August 31, 2025. State-funded coverage options through HFS may apply for some households — Illinois brokers can confirm alternatives case by case.

One additional pitfall: underestimating annual income to qualify for subsidies. Premium tax credits reconcile against actual annual income at tax filing. Households that received APTC based on a lower estimate than their actual earnings owe the difference back to the IRS — sometimes thousands of dollars. Over-estimating income is the safer error since it produces a refund at tax time rather than a bill.

Frequently Asked Questions About the Illinois Marketplace

The most common questions Illinois residents ask about Get Covered Illinois — covering the state platform transition, enrollment deadlines, subsidy availability, carriers, the Tax Time program, and whether HealthCare.gov still works for Illinois.

What is Get Covered Illinois?

Get Covered Illinois is the state-based health insurance marketplace that became Illinois’ official enrollment platform on January 1, 2026, replacing HealthCare.gov. The Centers for Medicare and Medicaid Services approved the transition in 2025. Illinois residents now apply for marketplace coverage, premium tax credits, and Medicaid through Get Covered Illinois at getcovered.illinois.gov or by calling 1-866-311-1119.

When can I enroll in marketplace coverage in Illinois for 2026?

Open enrollment through Get Covered Illinois ran from November 1, 2025 through January 31, 2026. Illinois extended the enrollment window sixteen days past the federal January 15 deadline using its new state-based marketplace authority. Outside open enrollment, a qualifying life event or the Illinois Tax Time Easy Enrollment Program is required to enroll.

Can I still get a subsidy on the Illinois marketplace in 2026?

Yes. The original Affordable Care Act premium tax credits remain in place for Illinois marketplace shoppers up to 400 percent of the federal poverty level. The enhanced subsidies that were added in 2021 expired at the end of 2025, which is why monthly premiums rose roughly 50 percent on average. Most marketplace enrollees still qualify for substantial assistance and should run an eligibility check before shopping plans.

Which carriers are on the Illinois marketplace for 2026?

Seven carriers participate in the Illinois marketplace for 2026: Blue Cross Blue Shield of Illinois (HCSC), Cigna HealthCare of Illinois, Ambetter from Celtic, Molina Healthcare, Oscar Health, UnitedHealthcare, and MercyCare. Four carriers exited the state at the end of 2025: Aetna CVS, Aetna Life, Health Alliance, and Quartz. Cigna no longer offers plans in Cook County for 2026, so Chicago-area residents who had Cigna needed to switch carriers.

What is the Illinois Tax Time Easy Enrollment Program?

The Tax Time Easy Enrollment Program is a special enrollment pathway unique to Illinois that lets residents enroll in marketplace coverage outside the regular open enrollment window if they indicate on their state tax return that the household is uninsured. This option became available with Illinois’ transition to a state-based marketplace and was not possible under the federal HealthCare.gov platform.

Do I have to use Get Covered Illinois, or can I still use HealthCare.gov?

Illinois residents must use Get Covered Illinois for 2026 marketplace coverage. HealthCare.gov stopped accepting Illinois applicants at the end of 2025 when Illinois transitioned to a state-based marketplace. Residents who previously had accounts on HealthCare.gov received direct messages from Get Covered Illinois with instructions to claim or recreate their account on the new platform.

Illinois Health Insurance Resources

Statewide overview of carriers, costs, and coverage paths for 2026

Best Illinois Health InsuranceTop-ranked carriers and plan options for Illinois residents in 2026

Illinois PPO PlansBCBSIL PPO options and other flexible network choices statewide

Family Health InsuranceAll Kids, marketplace splits, and mixed-status coverage for Illinois households

Affordable Illinois PlansSubsidy strategies and lowest-cost coverage paths after the 2026 rate jump

Private Medical InsuranceOff-exchange and private health coverage for unsubsidized Illinois buyers

Small Business CoverageGroup health insurance options for Illinois employers under 50 employees

Short-Term CoverageGap coverage rules and marketplace alternatives for Illinois residents

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required

Enroll Through Get Covered Illinois

Comparing seven carriers and 285 plan options on Get Covered Illinois is faster with a licensed Illinois broker. ForHealthInsurance.com helps Illinois residents verify subsidy eligibility, compare networks, and complete enrollment at no extra cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Illinois residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.