Kansas Health Insurance Marketplace 2026: HealthCare.gov Enrollment Guide

The Kansas health insurance marketplace operates on the federal HealthCare.gov platform — Kansas does not run a state-based exchange. About 206,000 Kansans selected plans through the Kansas health insurance marketplace during the open enrollment period that closed January 15, 2026, with roughly 92% receiving advance premium tax credits that lowered monthly costs. For 2026, Kansas marketplace premiums rose by a weighted average of 26.6% before subsidies — the benchmark Silver plan for a family of four reached $2,381 per month, up from $1,848 in 2025. Five carriers compete on the Kansas health insurance marketplace: Blue Cross and Blue Shield of Kansas, Blue Cross and Blue Shield of Kansas City, Ambetter from Sunflower Health Plan, UnitedHealthcare, Oscar Health, and Cigna. Aetna exited the Kansas individual market for 2026. Open enrollment for the Kansas marketplace for plan year 2027 begins November 1, 2026 and ends January 15, 2027. This page covers every Kansas marketplace enrollment path: open enrollment dates, subsidy eligibility by income, special enrollment periods, plan tier selection, and cost-sharing reductions on Silver plans.

Where are you in the Kansas enrollment process?

Kansas Open Enrollment 2027: Dates and Deadlines

Open enrollment for plan year 2027 on the Kansas marketplace runs November 1, 2026 through January 15, 2027. Coverage starts January 1, 2027 for enrollments completed by December 15, 2026. Enrollments between December 16 and January 15 take effect February 1, 2027. Kansas uses the standard federal HealthCare.gov enrollment calendar shared by 32 federal-marketplace states.

Kansas has used the federal HealthCare.gov open enrollment schedule since the Kansas health insurance marketplace launched in 2014. The current 76-day window — November 1 through January 15 — was extended from the original 45-day federal window in 2022. Kansans who fail to enroll during open enrollment generally cannot purchase a plan through the Kansas health insurance marketplace until the following year’s open enrollment, except when a qualifying life event triggers a Special Enrollment Period or when household income is at or below 150% of the federal poverty level, qualifying for a year-round continuous SEP.

The two-tier deadline structure matters practically. Enrolling by December 15 produces January 1 coverage — critical for Kansans with scheduled procedures, ongoing prescriptions, or follow-up specialist appointments in early January. Enrolling after December 15 but before January 15 means coverage starts February 1, leaving a January gap. For Kansans with chronic conditions, diabetes management medications, or ongoing physical therapy, the December 15 deadline is the one that matters. For healthy Kansans comparing options without urgent coverage needs, the full January 15 window is available.

Already Have a 2026 Kansas Marketplace Plan?

Existing enrollees are automatically re-enrolled in the same or similar plan for 2027 if no action is taken during open enrollment. But auto-renewal carries real risk: if your carrier changed its network, your premium tier shifted, or your household income changed enough to alter your APTC, the auto-renewed plan may be more expensive or cover fewer providers than an actively selected plan. The Kansas Insurance Department recommends active plan review each open enrollment — particularly in years like 2026–2027 where carrier networks and subsidy structures are in flux.

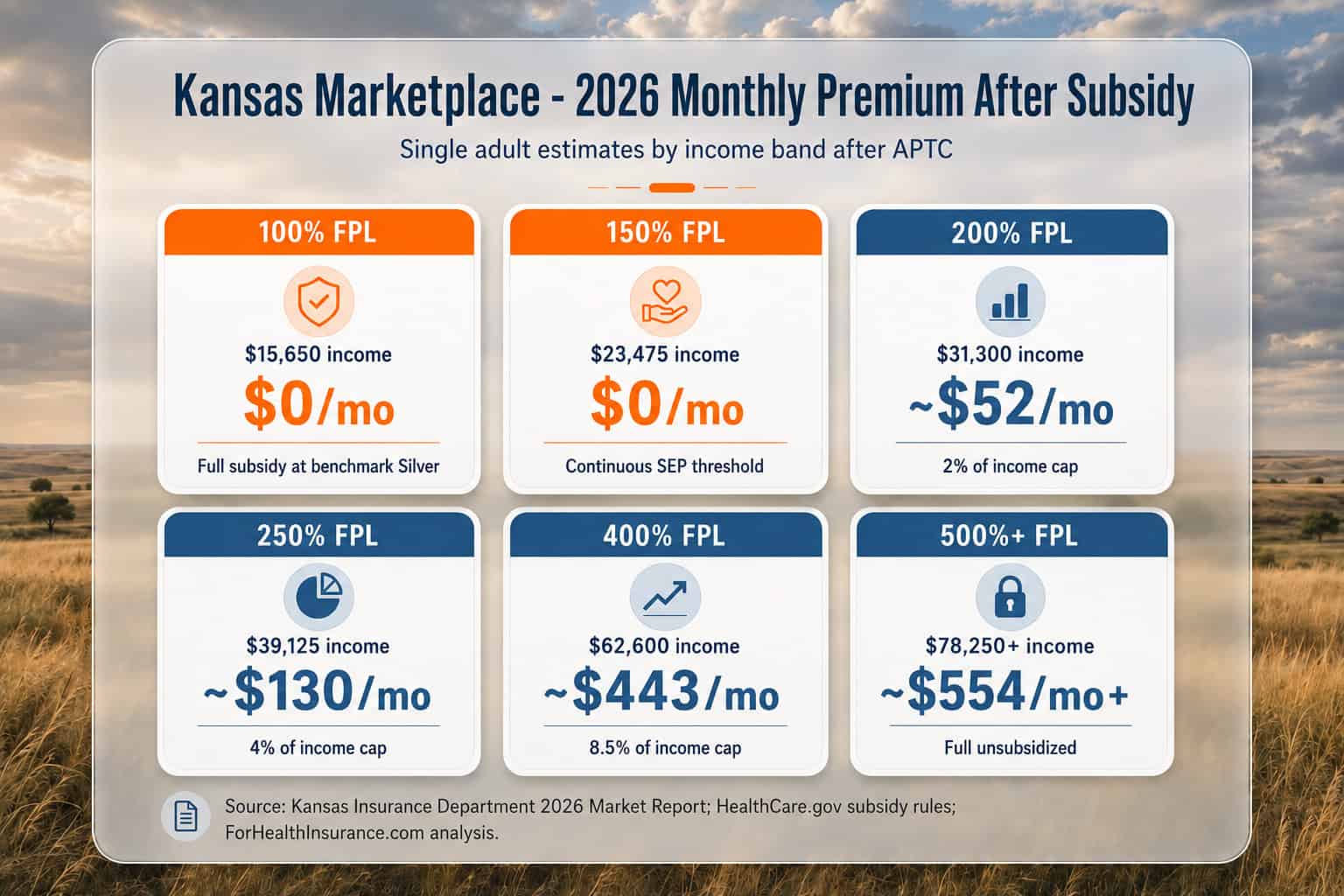

Kansas Marketplace Subsidies: APTC and CSR for 2026

About 92% of Kansas marketplace enrollees receive advance premium tax credits (APTC) that cap monthly premiums as a percentage of household income. For 2026, enrollees at 150% of the federal poverty level pay 0% of income; at 250% FPL they pay 4%; at 400% FPL they pay 8.5%. Kansans below 250% FPL who enroll in a Silver plan also receive cost-sharing reductions that lower deductibles and out-of-pocket maximums.

2026 Kansas Premium Cap by Income (Single Adult)

| Annual Income | % of FPL | Premium Cap (% of Income) | Est. Monthly Premium |

|---|---|---|---|

| $15,650 | 100% | 0% | $0 |

| $23,475 | 150% | 0% | $0 |

| $31,300 | 200% | 2% | ~$52 |

| $39,125 | 250% | 4% | ~$130 |

| $46,950 | 300% | 6% | ~$235 |

| $62,600 | 400% | 8.5% | ~$443 |

| $78,250+ | 500%+ | 8.5% (enhanced cap) | ~$554+ |

Cost-Sharing Reductions on Kansas Silver Plans

Cost-sharing reductions (CSR) are a second Kansas marketplace subsidy available only to enrollees below 250% of the federal poverty level who select a Silver-tier plan. CSR lowers deductibles, copays, coinsurance rates, and annual out-of-pocket maximums — not the monthly premium. For a Kansas enrollee below 200% FPL, CSR can reduce a Silver plan’s out-of-pocket maximum from roughly $9,200 to as low as $3,100 annually. This makes Silver the most valuable tier for lower-income Kansas marketplace enrollees even when a Bronze plan appears cheaper on monthly premium alone.

CSR is built into the Silver plan automatically when your income qualifies — enrollees do not apply separately. But it only applies to Silver-tier plans. If a CSR-eligible Kansas enrollee selects a Bronze or Gold plan instead, the CSR benefit is lost entirely. Whether CSR applies depends on household income, and modeling the annual total cost difference between Silver and Bronze at a specific income level routinely shows Silver saving $2,000–$4,000 in annual out-of-pocket costs for Kansas enrollees below 200% FPL. For more ways to lower your total cost, see the guide to affordable health insurance in Kansas.

Special Enrollment Periods in Kansas

A qualifying life event triggers a 60-day Special Enrollment Period (SEP) on the Kansas marketplace. Common qualifying events include marriage, divorce, birth or adoption of a child, loss of job-based coverage, aging off a parent’s plan at 26, and a permanent move into Kansas. Kansans at or below 150% of FPL — about $23,475 for a single adult in 2026 — qualify for a year-round continuous SEP with no triggering event needed.

The 60-day SEP clock begins on the date of the qualifying event — not the date you file an application. Missing the 60-day window means waiting for the next open enrollment period on the Kansas health insurance marketplace. For Kansans who lose job-based coverage, COBRA continuation is typically available but expensive: the employee must pay the full premium plus a 2% administrative fee, often $600–$900 per month for a single adult. The Kansas marketplace SEP is almost always the better path for Kansans who qualify for subsidies, which covers the majority of people who lose employer-sponsored coverage.

Family Change

Life Event SEPs

Marriage, divorce, birth or adoption of a child, or a dependent child aging off your plan at 26 each open a 60-day window starting on the event date. Marriage requires that at least one spouse had prior coverage; birth and adoption allow coverage retroactive to the event date; and divorce creates a SEP for the spouse losing coverage.

Coverage Loss

Loss of Coverage SEPs

Loss of employer-sponsored coverage, loss of KanCare or CHIP eligibility, COBRA expiration, or loss of coverage as a dependent all qualify. Voluntary resignation of employer coverage generally does not qualify, but KanCare redetermination losses and COBRA expiration both count as qualifying losses.

Move or Status

Move and Citizenship SEPs

A permanent move into Kansas from another state or country, a within-Kansas move that changes available plans, or gaining U.S. citizenship or lawful status. The move must be permanent rather than seasonal, within-Kansas moves qualify when the zip code changes plan availability, and a prior-coverage requirement applies to move-based SEPs.

Income or Error

Income-Change and Special SEPs

A household income change that newly qualifies you for — or ends — KanCare or cost-sharing reductions can open an SEP, as can enrollment errors, exceptional circumstances, or a successful marketplace appeal. Kansans with income at or below 150% of the federal poverty level also qualify for a year-round continuous SEP with no triggering event needed.

Kansas Low-Income Continuous SEP

Kansans with household income at or below 150% of the federal poverty level — about $23,475 for a single adult or $48,225 for a family of four in 2026 — can enroll in a Kansas marketplace plan year-round under the low-income continuous SEP. No qualifying event is required. At this income level, subsidies fully cover the benchmark Silver premium, eliminating the adverse-selection concern that normally drives the SEP rules.

Compare Kansas Marketplace Plans Now

Running full subsidy calculations across all five Kansas marketplace carriers — and confirming CSR eligibility and in-network status at The University of Kansas Health System, Stormont Vail, or Via Christi Ascension — narrows the options, at no extra cost over HealthCare.gov direct enrollment.

Kansas Marketplace Plan Tiers: Bronze, Silver, Gold, and Catastrophic

Kansas marketplace plans come in four metal tiers — Bronze, Silver, Gold, and Catastrophic — plus an Expanded Bronze option on some carriers. Tiers differ in how costs are split between monthly premium and out-of-pocket costs at the time of care. For most Kansans below 250% FPL, Silver is the best tier because it’s the only one eligible for cost-sharing reductions. Above 400% FPL, Gold or Bronze depends on expected healthcare usage.

Bronze — Lowest Premium, Highest Out-of-Pocket

The cheapest monthly premium tier in Kansas — UnitedHealthcare offers the 2026 Kansas Bronze starting at $442/month for a 40-year-old. High deductibles ($7,000–$9,000 typical) mean you pay most costs until the deductible is met. Best for healthy Kansans above subsidy limits who rarely use medical care. CSR does not apply to Bronze — a CSR-eligible Kansas enrollee loses the benefit by choosing Bronze over Silver.

Silver — The CSR Tier for Most Kansans

The benchmark tier for Kansas marketplace subsidies — all APTC calculations use the Silver benchmark. The only tier eligible for cost-sharing reductions. For Kansas enrollees below 250% FPL, Silver consistently delivers lower annual total cost than Bronze despite a higher monthly premium, because CSR can cut the out-of-pocket maximum in half. Ambetter Sunflower and BCBS Kansas both offer competitive Silver plans on the 2026 Kansas marketplace.

Gold — Lower Out-of-Pocket, Higher Premium

Gold plans have higher monthly premiums than Silver but lower deductibles and cost-sharing. For Kansas enrollees between 300% and 400% FPL who use regular medical care — frequent prescriptions, ongoing specialist visits, or planned procedures — Gold can produce lower total annual cost than Silver despite the premium difference. Run a side-by-side annual cost model before choosing Gold over Silver.

Catastrophic — Under-30 or Hardship Exemption Only

Available only to Kansans under 30 or those with a hardship exemption. Very low monthly premium, very high deductible (the 2026 ACA out-of-pocket maximum of $9,200 for a single person). BCBS Kansas offers Catastrophic coverage in Kansas. Not eligible for APTC subsidies — the monthly savings are offset by significant exposure in any year with meaningful medical use. Best suited for young, healthy Kansans who want catastrophic protection only.

How to Enroll in the Kansas Health Insurance Marketplace

Kansas residents enroll in marketplace health insurance through HealthCare.gov during open enrollment — November 1 through January 15 — or via a Special Enrollment Period triggered by a qualifying life event. Enrolling through HealthCare.gov carries no extra cost over self-enrollment, and subsidy calculations and provider-network checks should be completed before selecting a plan.

Gather what you need before starting

Household size, estimated 2026 annual income, Social Security numbers for every household member applying, employer coverage information (if offered), and a list of current doctors, specialists, or hospitals you want to keep in-network.

Compare plans for your zip code

Enter your Kansas zip code at HealthCare.gov to see all plans available in your area, with subsidy calculations applied for a side-by-side comparison.

Check your subsidy amount first

Input your household income and size to get your APTC estimate. If you’re below 250% FPL, identify the Silver plan cost after CSR before comparing Bronze. The monthly premium difference between Bronze and CSR-enhanced Silver is often much smaller than it appears.

Verify your providers

Confirm your current doctors and The University of Kansas Health System, Stormont Vail, or Via Christi Ascension are in-network on the plan you’re considering. Network verification is the most common missed step — and the most expensive mistake when you get it wrong.

Complete enrollment by December 15 for January 1 coverage

Enrollment completed between December 16 and January 15 starts February 1, 2027. Pay your first premium within 30 days of plan selection to activate coverage.

Frequently Asked Questions

When is open enrollment for the Kansas health insurance marketplace?

Open enrollment for plan year 2027 runs November 1, 2026 through January 15, 2027. Kansans who want coverage starting January 1, 2027 must enroll by December 15, 2026. Plans purchased between December 16 and January 15 take effect February 1, 2027. The 2026 plan year open enrollment closed January 15, 2026 and covered approximately 206,000 Kansas enrollees through HealthCare.gov.

Can I enroll in a Kansas marketplace plan outside of open enrollment?

Yes, if you have a qualifying life event. Qualifying events that trigger a 60-day Special Enrollment Period in Kansas include marriage or divorce, birth or adoption of a child, loss of job-based health coverage, aging off a parent’s plan at 26, a permanent move into Kansas from another state, and gaining U.S. citizenship. Kansans with household income at or below 150% of the federal poverty level — about $23,475 for a single adult in 2026 — can enroll year-round under a continuous SEP with no qualifying event required.

How are Kansas marketplace subsidies calculated?

Kansas marketplace subsidies cap your monthly premium at a percentage of household income scaled by federal poverty level. For 2026, enrollees at 150% of FPL pay 0% of income toward the benchmark Silver plan; at 250% FPL they pay 4%; at 400% FPL they pay 8.5%. The benchmark Silver plan for a family of four in Kansas costs $2,381 per month in 2026 before subsidy — even modest household incomes generate substantial advance premium tax credits. The enhanced subsidy structure enacted in 2021 is set to expire December 31, 2025 unless Congress extends it.

Which carriers offer plans on the Kansas marketplace in 2026?

Five carriers offer 2026 Kansas marketplace plans through HealthCare.gov: Blue Cross and Blue Shield of Kansas (statewide), Blue Cross and Blue Shield of Kansas City (KC metro counties only), Ambetter from Sunflower Health Plan, UnitedHealthcare, Oscar Health, and Cigna Healthcare. Aetna CVS Health exited the Kansas individual market for 2026. Carrier availability varies by zip code — BCBS Kansas is the only option with coverage across all 105 Kansas counties. Enter your zip code at HealthCare.gov to see which carriers serve your area.

Should I choose Bronze, Silver, or Gold on the Kansas marketplace?

For Kansans below 250% of the federal poverty level, Silver is almost always the right tier because Silver plans are the only tier eligible for cost-sharing reductions (CSR) that lower deductibles and out-of-pocket maximums. For Kansans between 250% and 400% FPL who want predictable costs, Gold tier often delivers lower annual total cost despite higher premiums. Bronze and Catastrophic tiers work best for healthy Kansans above subsidy limits who want the lowest monthly premium and are comfortable with high deductibles. Annual total cost across tiers can be modeled at a specific income level to find the best value.

More Kansas Health Insurance Resources

Related guides cover the complete Kansas health insurance overview, carrier rankings across BCBS Kansas and its competitors, small business and group coverage options, and PPO plans for Kansans who want broader provider access.

Complete 2026 Kansas health insurance overview — KanCare, marketplace, employer, and PPO paths.

Best Health Insurance in KansasBCBS Kansas, Ambetter, UnitedHealthcare, Oscar, and Cigna compared on price and network.

Kansas Small Business Health InsuranceGroup plans, ICHRA, SHOP marketplace, and BCBS Kansas small group for Kansas employers.

PPO Health Insurance PlansOff-exchange PPO options for Kansas residents who want broader network access, no referrals.

Enroll in a Kansas Marketplace Plan Today

Screening for KanCare and CHIP eligibility, comparing all five Kansas marketplace carriers with subsidy calculations applied, and confirming CSR eligibility on Silver plans covers every Kansas enrollment path, at no extra cost over enrolling directly.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Kansas residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.