Affordable Health Insurance Kansas 2026: Costs, Subsidies & Cheapest Plans

Finding affordable health insurance in Kansas in 2026 requires navigating a market shaped by a 26.6% average premium increase — the largest gross rate jump in the state’s marketplace history — combined with federal subsidies that absorb most of that increase for the 92% of Kansas marketplace enrollees who qualify for advance premium tax credits. The benchmark Silver plan for a family of four reached $2,381 per month before subsidies, up from $1,848 in 2025, but a Kansas family of four earning $65,000 annually might pay as little as $180 to $320 per month on a subsidized Silver plan after the tax credit is applied. For Kansans between 100% and 150% of the federal poverty level — about $15,650 to $23,475 for a single adult — the monthly premium on a benchmark Silver plan is $0 under both the standard formula and the continuous year-round enrollment window. The central challenge for affordable health insurance in Kansas is the non-expansion coverage gap: Kansas has not expanded Medicaid, leaving an estimated 40,000 to 50,000 low-income adults without access to either KanCare or subsidized marketplace coverage. This guide covers every affordable Kansas health insurance path for 2026 — subsidies, KanCare, the coverage gap, free or near-free plans, and the cheapest private options by income tier.

What’s your Kansas affordability situation?

How Subsidies Make Kansas Health Insurance Affordable in 2026

About 92% of Kansas marketplace enrollees receive advance premium tax credits (APTC) that cap monthly premiums as a percentage of income — not as a fixed dollar amount. For 2026, enrollees at 150% of FPL pay $0 per month; at 250% FPL they pay about 4% of annual income; at 400% FPL they pay 8.5%. For most subsidized Kansans, the 26.6% gross rate increase translates to a much smaller out-of-pocket change.

The advance premium tax credit works by filling the gap between what a Kansas household “should” pay for health coverage (a capped percentage of income) and what the benchmark Silver plan actually costs. With Kansas benchmark Silver premiums rising sharply for 2026, the federal government is paying significantly larger APTC amounts per Kansas enrollee this year — but the household’s out-of-pocket premium stays capped at the same income percentage. A Kansas family of four earning $65,000 who paid $220 per month for a Silver plan in 2025 would pay roughly $255 per month in 2026 under the same formula — a $35 increase, not the $533 increase the 26.6% gross rate change implies.

The enhanced subsidy structure — which extended the income cap above 400% of FPL — is set to expire December 31, 2025 unless Congress acts. If it lapses, Kansas marketplace enrollees earning between 400% and 600% of FPL could face premium increases of several hundred dollars per month. A self-employed Kansas resident earning $80,000 who currently pays about $510 per month for a Silver plan could see premiums jump to $800 or more if the enhanced cap disappears. This uncertainty is a significant factor for unsubsidized Kansans planning 2026 budgets.

The 2026 Kansas Rate Increase: 26.6% — What Drove It

Kansas marketplace premiums rose 26.6% on a weighted average gross basis for 2026 — the benchmark Silver plan for a family of four climbed from $1,848 to $2,381 per month before subsidies. Four factors drove the increase: anticipated expiration of enhanced ACA subsidies, rising per-member claim costs, prescription drug inflation, and Kansas’s non-expansion status concentrating higher-risk adults in the individual market.

The Kansas Insurance Department’s 2026 market report — reviewed and published by Commissioner Vicki Schmidt — identifies carrier actuarial filings that point to projected claim costs per member per month rising from $589.04 in 2024 to $637.85 in 2026, an 8.3% medical trend. Carriers priced in the anticipated expiration of enhanced subsidies, which would pull healthier enrollees out of the market and raise average risk. Prescription drug costs — particularly GLP-1 medications like Ozempic and Wegovy, and high-cost oncology drugs — contributed outsized cost pressure across all five Kansas marketplace carriers.

Blue Cross and Blue Shield of Kansas City was the only carrier with a rate decrease for 2026, at -6.14%, suggesting their KC metro enrollee pool carried lower average risk than statewide carriers. All other Kansas carriers posted increases ranging from 22.6% (Cigna) to 30.4% (UnitedHealthcare). For affordable health insurance in Kansas, the BCBS Kansas City rate decrease makes it a competitive option specifically in Johnson, Wyandotte, Leavenworth, and Miami counties — the Kansas side of the Kansas City metro.

| Carrier | 2026 Avg Rate Change | Coverage Area |

|---|---|---|

| Blue Cross and Blue Shield of Kansas City | -6.14% | KC metro counties |

| Cigna Healthcare | +22.6% | KC metro |

| Oscar Health | +24.9% | KC metro + Wichita area |

| Blue Cross and Blue Shield of Kansas | +27.3% | Statewide |

| Ambetter from Sunflower Health Plan | +28.1% | Multi-region |

| UnitedHealthcare | +30.4% | Multi-region |

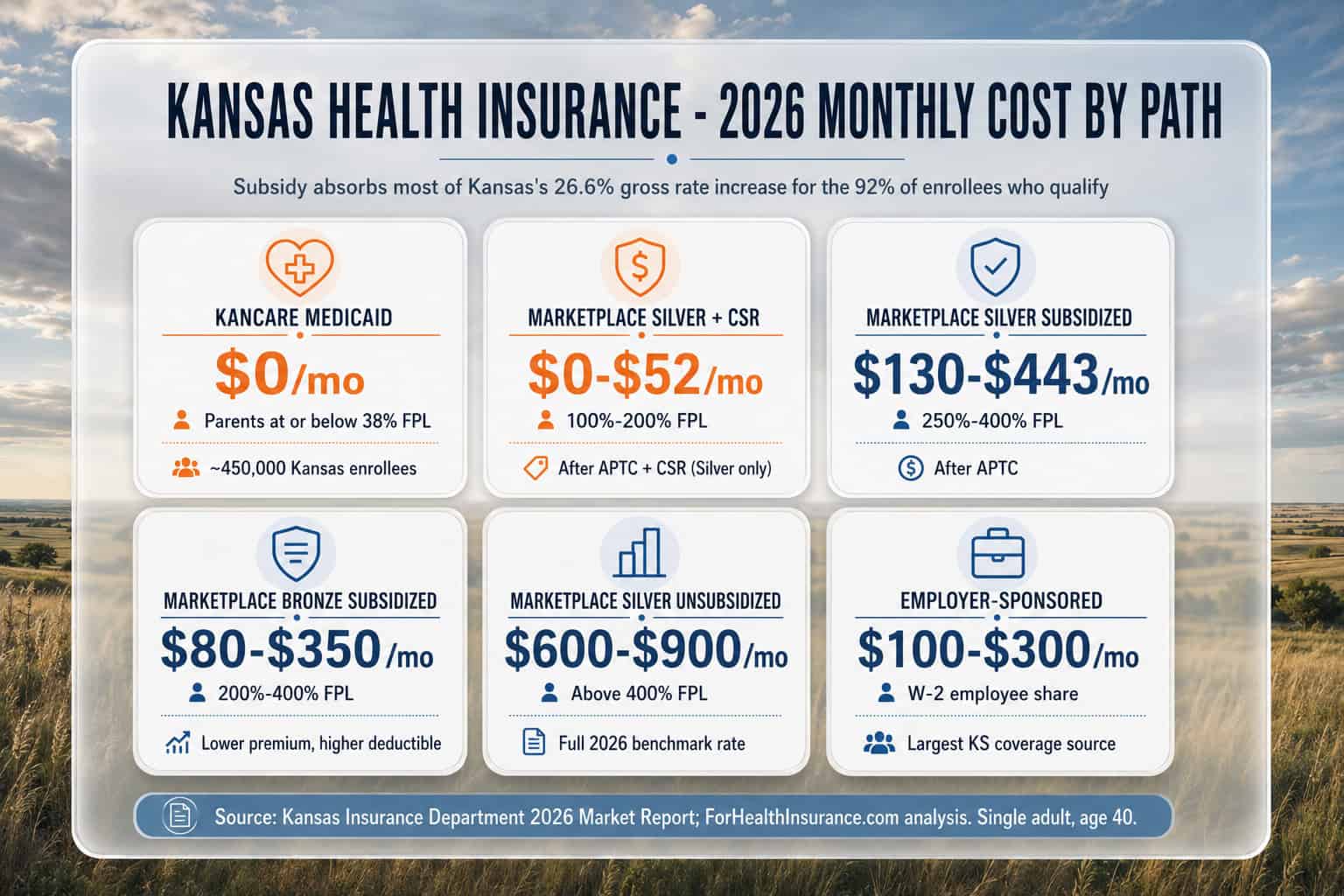

KanCare Medicaid: Free Coverage for Eligible Kansans

KanCare is Kansas’s Medicaid managed care program covering about 450,000 Kansans at no monthly premium through three MCOs: Sunflower Health Plan, Aetna Better Health of Kansas, and Healthy Blue. Parents qualify at or below 38% of the federal poverty level — about $8,194 for a family of three in 2026. Children qualify at higher income thresholds. Adults without dependent children generally do not qualify unless disabled, pregnant, or elderly.

KanCare covers the 10 ACA essential health benefits including hospital stays, emergency care, prescription drugs, mental health and substance use treatment, preventive care, and pediatric services. Coverage is delivered through managed care contracts with the three MCOs, each with its own provider network. Unlike marketplace plans, KanCare has no open enrollment window — qualifying Kansans can apply year-round through KanCare.ks.gov or the Kansas Department of Health and Environment (KDHE). Eligibility is redetermined annually and after income or household changes.

The Kansas Coverage Gap: ~40,000–50,000 Uninsured Adults

Kansas is one of nine non-expansion states. Adults earning less than 100% of the federal poverty level — about $15,650 for a single adult in 2026 — do not qualify for marketplace subsidies (which start at 100% FPL). Adults without dependent children do not qualify for KanCare unless they are disabled, pregnant, or 65 or older. Adults with dependent children qualify for KanCare only up to 38% FPL. This leaves an estimated 40,000–50,000 Kansas adults in a coverage gap where neither Medicaid nor subsidized marketplace coverage is available. Kansas has voted on Medicaid expansion five times in the legislature since 2014 without passage.

Find Affordable Health Insurance in Kansas

Screening for KanCare and CHIP eligibility, calculating subsidy amounts across all five Kansas marketplace carriers, and identifying CSR-eligible Silver plans at a specific income level shows the lowest true cost. Free enrollment carries no extra cost over enrolling at HealthCare.gov directly.

Affordable Health Insurance for Self-Employed Kansans

Self-employed Kansans — freelancers, sole proprietors, independent contractors, and small business owners without W-2 employees — can deduct 100% of marketplace health insurance premiums as an above-the-line federal income tax deduction, reducing adjusted gross income and potentially increasing subsidy eligibility. A self-employed Kansan earning $55,000 annually may qualify for an APTC that cuts a Silver plan premium from roughly $800 to under $400 per month.

The self-employed health insurance deduction works on Schedule 1 of the federal return, not as an itemized deduction — meaning it applies regardless of whether the taxpayer itemizes. Because it reduces AGI, it also lowers the income figure used to calculate the APTC, which can produce a feedback loop where lower AGI increases the subsidy, which further reduces net cost. A licensed Kansas agent can model the approximate net premium at different income estimates, which is particularly useful for self-employed Kansans seeking affordable health insurance and working with variable income.

For self-employed Kansans earning above subsidy limits, the off-exchange PPO market offers an alternative to marketplace HMO and EPO plans — with broader provider networks including out-of-state access that matters for Kansans near the Missouri border. Blue Cross and Blue Shield of Kansas’s Premier Blue PPO and BCBS Kansas City’s Preferred Care Blue PPO are the primary statewide and metro options. These do not qualify for APTC but may be preferable for Kansans with established specialist relationships or who travel frequently for work.

Cheapest Health Insurance in Kansas by Income Tier

The cheapest affordable health insurance in Kansas depends on income. At 100%–150% FPL, a Silver plan costs $0 per month after APTC. At 200%–300% FPL, Silver with CSR delivers the best total annual value despite higher premiums than Bronze. Above subsidy limits, UnitedHealthcare offers Kansas’s cheapest 2026 Bronze plan at $442 per month for a 40-year-old — the lowest unsubsidized entry point on the Kansas marketplace.

100%–150% FPL

$0/Month Silver Plan

Kansans at or below 150% of FPL pay $0/month for the benchmark Silver plan after APTC, and CSR reduces deductibles to as low as $350 and the out-of-pocket maximum to $3,100 for those below 200% FPL. A continuous SEP allows year-round enrollment with no qualifying event, Silver is the correct tier because Bronze loses the CSR benefit, and both Ambetter and BCBS Kansas offer $0-premium Silver options.

200%–400% FPL

Silver with APTC + Possible CSR

Kansans between 200% and 400% FPL receive APTC capping premiums at 2%–8.5% of income, and those below 250% FPL also get CSR on Silver, making Silver cheaper in total annual cost than Bronze. At $39,125 (250% FPL), Silver runs about $130/month after APTC; at $62,600 (400% FPL), about $443/month. Model annual total cost, not just the monthly premium.

Above Subsidy Limits

Cheapest Bronze or Off-Exchange PPO

For Kansans above subsidy limits, UnitedHealthcare’s Bronze starts at $442/month for a 40-year-old — the cheapest statewide — and BCBS Kansas City’s Bronze starts at roughly $457/month in KC metro counties with the benefit of the only 2026 carrier rate decrease (-6.14%). An off-exchange PPO is also available for broader network access without subsidy eligibility. See how the carriers compare in the guide to the best health insurance in Kansas.

Below the KanCare Limit

$0/Month KanCare Medicaid

Kansas parents at or below 38% of FPL and children up to 166% of FPL qualify for KanCare Medicaid at no monthly premium, covering roughly 450,000 Kansans through Sunflower Health Plan, Aetna Better Health, and Healthy Blue. Because Kansas has not expanded Medicaid, adults earning below 100% FPL but above the KanCare limit fall into the coverage gap and may not qualify for either KanCare or marketplace subsidies.

Frequently Asked Questions

What is the cheapest health insurance in Kansas for 2026?

For Kansans who qualify for subsidies, the cheapest affordable health insurance in Kansas in 2026 is a Silver plan with cost-sharing reductions — at 150% of the federal poverty level (about $23,475 for a single adult), the monthly premium is $0 after the advance premium tax credit. For Kansans above subsidy limits, UnitedHealthcare offers the cheapest Bronze plan in Kansas starting at $442 per month for a 40-year-old, with BCBS Kansas City Bronze plans starting slightly higher at $457 per month. Oscar Health and Cigna also offer competitive Bronze pricing in the Kansas City metro counties.

Did Kansas health insurance premiums actually go up 26.6% in 2026?

Yes — the Kansas marketplace saw a weighted average gross rate increase of 26.6% for 2026, one of the largest in the country. The benchmark Silver plan for a family of four rose from $1,848 per month in 2025 to $2,381 per month in 2026 before subsidies, a 28.9% increase. However, about 92% of Kansas marketplace enrollees receive advance premium tax credits that absorb most of this increase — for subsidized Kansans, the actual out-of-pocket premium change is much smaller. The full 26.6% increase only hits the roughly 8% of unsubsidized enrollees, typically self-employed Kansans or early retirees earning above subsidy limits.

Does Kansas have free or low-cost health insurance for low-income adults?

Kansas has not expanded Medicaid under the ACA, which creates a coverage gap for low-income adults without dependent children. KanCare covers parents with household incomes at or below 38% of the federal poverty level — about $8,194 for a family of three in 2026 — but adults without dependent children generally do not qualify for KanCare regardless of income unless they are disabled, pregnant, or 65 or older. Kansans between 100% and 150% of FPL can enroll in a marketplace Silver plan year-round with $0 monthly premium under the continuous SEP. Below 100% FPL and above 38% FPL, most low-income childless adults in Kansas have no subsidized coverage option.

How does the Kansas coverage gap work?

The Kansas coverage gap affects adults whose income falls below 100% of the federal poverty level — about $15,650 for a single adult in 2026 — but above the KanCare Medicaid threshold. Marketplace subsidies start at 100% FPL, so adults below that threshold cannot get subsidized marketplace coverage. KanCare covers parents only up to 38% FPL, and covers childless adults only if they are disabled, pregnant, or elderly. About 40,000 to 50,000 Kansans fall in this gap. Kansas has debated Medicaid expansion multiple times since 2014 without passing it, leaving this population without a subsidized coverage pathway.

Can a self-employed Kansas resident get affordable health insurance?

Yes. Self-employed Kansans who buy their own health insurance through the HealthCare.gov marketplace can deduct 100% of premiums paid as an above-the-line federal income tax deduction — lowering adjusted gross income and potentially increasing subsidy eligibility. A self-employed Kansas resident earning $55,000 annually may qualify for an advance premium tax credit that reduces a Silver plan from around $800 per month to $390 per month. The 2026 benchmark Silver for a single adult in Kansas varies by age and region, but the subsidy formula caps cost at 8.5% of income for earnings above 400% FPL under the currently-extended enhanced subsidies.

More Kansas Health Insurance Resources

Related guides cover the complete Kansas health insurance overview, small business and group coverage options, HealthCare.gov marketplace enrollment, and PPO plans for Kansans who want broader provider access.

Complete 2026 Kansas health insurance overview — KanCare, marketplace, employer, and PPO paths.

Kansas Small Business Health InsuranceGroup plans, ICHRA, SHOP, and BCBS Kansas small group options for Kansas employers.

Kansas Marketplace EnrollmentHealthCare.gov enrollment dates, special enrollment periods, and plan tier selection for Kansas.

PPO Health Insurance PlansOff-exchange PPO options for Kansans who need broader network access and no referrals.

Compare Affordable Kansas Health Insurance Plans

Screening for KanCare, calculating 2026 APTC and CSR, and comparing all five carriers side by side finds the cheapest plan that covers specific Kansas providers. Free enrollment carries no extra cost over HealthCare.gov direct enrollment.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Kansas residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.