Affordable Health Insurance in Minnesota: 2026 Low-Cost Plans & Savings

Affordable health insurance in Minnesota for 2026 depends on where your household income lands. Minnesotans earning under 138% of the Federal Poverty Level qualify for Medical Assistance (the state’s Medicaid program), those between 138–200% FPL qualify for MinnesotaCare, and those above 200% FPL can shop for subsidized plans on MNsure. This guide walks through every low-cost option — what you qualify for, how much you pay, and how Minnesota’s MPSP reinsurance program keeps premiums lower than in most states.

What’s your path to affordable coverage?

Free and Low-Cost Coverage for Low-Income Minnesotans

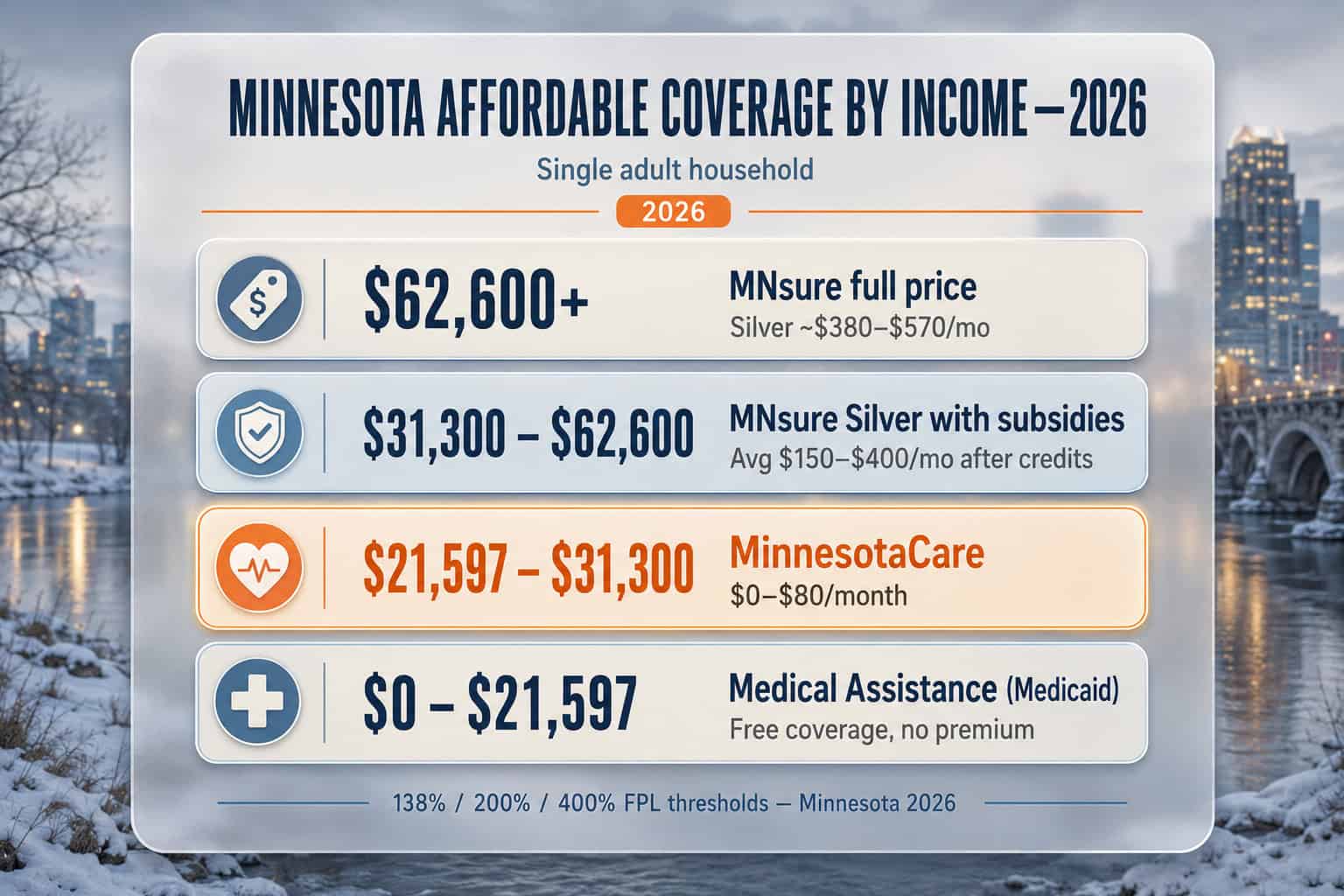

Minnesotans earning under 138% of the Federal Poverty Level — roughly $21,597 for a single adult or $44,367 for a family of four in 2026 — qualify for Medical Assistance, Minnesota’s Medicaid program. Medical Assistance is free to enrollees with no monthly premium, no deductible, and minimal copays. Approximately 1.2 million Minnesotans are enrolled in Medical Assistance, making it the largest source of health coverage in the state after employer-sponsored insurance.

Medical Assistance is the most affordable health insurance in Minnesota for low-income residents, covering a comprehensive set of benefits: primary care, specialist visits, hospital care, prescription drugs, mental health services, dental care, and preventive services. Unlike marketplace plans, Medical Assistance enrollees pay no monthly premium and face only nominal copays ($3 for most services, capped at 5% of household income annually). The program is administered by the Minnesota Department of Human Services, and enrollment is open year-round — there is no Open Enrollment Period limitation.

Minnesotans applying for Medical Assistance can do so through the MNsure application, which screens for all income-based coverage programs simultaneously. The MNsure marketplace guide walks through how that single application works and what documents you’ll need. If your income is too low for Medical Assistance — for example, if you don’t qualify due to asset limits or immigration status — the Minnesota DHS Medical Assistance page lists alternative programs including Emergency Medical Assistance and Refugee Medical Assistance.

MinnesotaCare — Basic Health Program for Moderate Income

MinnesotaCare is Minnesota’s Basic Health Program (BHP) — a unique state-run coverage option for Minnesotans earning between 138% and 200% of the Federal Poverty Level. That’s roughly $21,597–$31,300 for a single adult or $44,367–$64,300 for a family of four in 2026. MinnesotaCare premiums range from $0 to approximately $80/month per adult depending on income, with comprehensive benefits including medical, prescription, dental, and vision coverage. Only two states operate Basic Health Programs — Minnesota and New York.

MinnesotaCare was created in 1992 — long before the Affordable Care Act — as Minnesota’s affordable health insurance solution for working families earning too much for Medicaid but too little to pay full-price private coverage. When the ACA passed in 2010, Minnesota elected to continue MinnesotaCare as its Basic Health Program under Section 1331 of the law, taking federal funding that would otherwise go toward premium tax credits and applying it directly to MinnesotaCare coverage. The result is significantly lower out-of-pocket costs for enrollees compared to buying a subsidized MNsure plan at the same income level.

| Household Size | Min. Income (138% FPL) | Max. Income (200% FPL) | Monthly Premium Range |

|---|---|---|---|

| 1 person | $21,597 | $31,300 | $0–$80 |

| 2 people | $29,187 | $42,300 | $0–$160 |

| 3 people | $36,777 | $53,300 | $0–$240 |

| 4 people | $44,367 | $64,300 | $0–$320 |

MinnesotaCare is why MNsure’s subsidy participation rate is so different from other states. Approximately 46% of MNsure enrollees receive premium tax credits, compared to 92% nationally — not because Minnesotans earn more, but because low-to-moderate income Minnesotans enroll in MinnesotaCare instead of the marketplace. For eligible households, MinnesotaCare is typically the most affordable health insurance in Minnesota, with benefits on par with a Gold-tier marketplace plan at a fraction of the cost.

MinnesotaCare enrollment year-round: Unlike MNsure marketplace plans, MinnesotaCare is not limited to Open Enrollment. Eligible Minnesotans can apply any time of year through the MNsure application. Coverage typically begins the first of the month after approval. Enrollees recertify eligibility annually based on updated income information.

MNsure Premium Subsidies for 2026

Minnesotans earning above 200% of the Federal Poverty Level — too much for MinnesotaCare — qualify for premium tax credits on MNsure marketplace plans. The average subsidy in Minnesota for 2026 is approximately $600/month for eligible families, and subsidies scale based on income and the cost of the benchmark Silver plan in your county. A single adult earning $40,000 in Hennepin County typically qualifies for $150–$250/month in premium tax credits.

Premium tax credits are the primary mechanism for affordable health insurance in Minnesota for middle-income households. They work by capping the amount you pay for the benchmark (second-lowest-cost) Silver plan as a percentage of household income, ranging from roughly 2% at 200% FPL up to 8.5% at 400% FPL under the enhanced subsidy rules that have been in effect since 2021. For 2026, federal enhanced subsidies are scheduled to revert to pre-2021 levels unless Congress extends them. This is a critical planning consideration for Minnesotans at the higher end of the subsidy range, where the difference between enhanced and original subsidy rules can be several hundred dollars per month. The IRS premium tax credit guidance explains how the credit is calculated and reconciled at tax time on Form 8962.

Example: Bloomington Family of Four, $75,000 Income

A Bloomington family of four (two adults ages 40, two children) earning $75,000/year is at approximately 233% FPL — too high for MinnesotaCare but solidly in the MNsure subsidy range. Their estimated 2026 monthly costs: HealthPartners Silver family plan at approximately $1,350/month full price, minus approximately $880/month in premium tax credits, for an after-subsidy cost of approximately $470/month. A Bronze plan would run closer to $250/month after the same subsidy, though with a higher deductible. Running an estimate directly on MNsure during Open Enrollment is the most accurate way to see exact numbers for your own household, since the credit depends on income, household size, and the benchmark Silver plan in your county.

See What You’d Actually Pay in Minnesota

Get a personalized affordability estimate based on your income, household size, and county. Medical Assistance, MinnesotaCare, or subsidized MNsure — a licensed enrollment assistant can run all three scenarios.

How Minnesota’s MPSP Keeps Premiums Lower

The Minnesota Premium Security Plan (MPSP) is the state’s reinsurance program, operating under a federal 1332 waiver that keeps individual market premiums approximately 25% lower than they would be without the program. For 2026, the 22% average rate increase would have been closer to 47% without MPSP, according to RAND Health Care modeling commissioned by the Minnesota Council of Health Plans. Governor Walz signed legislation in 2025 extending MPSP through 2027.

MPSP works by covering a portion of high-cost claims between $50,000 and $250,000 per year, reducing the financial risk carriers absorb for catastrophic cases. This risk reduction makes affordable health insurance in Minnesota more accessible for all 187,000 Minnesotans who buy individual coverage — not just those who would hit the high-claim threshold. The program is funded through a combination of federal pass-through savings (because lower premiums reduce federal subsidy spending) and state appropriations.

For unsubsidized Minnesotans — those with income above 400% FPL who don’t qualify for MNsure tax credits under pre-enhanced subsidy rules — MPSP is the primary reason Minnesota premiums remain competitive with other states. Without MPSP, a 55-year-old Minneapolis resident paying approximately $770/month for a Silver plan in 2026 would likely be paying over $1,000/month. The Minnesota Department of Commerce publishes annual MPSP impact data.

Cheapest Health Insurance Plans in Minnesota for 2026

The cheapest health insurance in Minnesota for 2026 at the full-price level is Medica’s Bronze HMO at approximately $234/month for a 40-year-old in Hennepin County. HealthPartners offers the lowest Silver premium at $379/month — a better value for most enrollees because Silver plans qualify for cost-sharing reductions (CSRs) if income is under 250% FPL. For subsidized enrollees, after-subsidy pricing matters more than sticker price: a $50/month Silver plan with CSRs often beats a $0/month Bronze plan with a $7,500 deductible.

| Plan Type | Cheapest Carrier | Approx. 40yo Premium | Deductible | Best For |

|---|---|---|---|---|

| Bronze HMO | Medica | ~$234/mo | ~$7,500 | Healthy enrollees, unsubsidized |

| Bronze HSA | Medica | ~$250/mo | ~$7,000 | HSA savers, all Bronze plans HSA-eligible for 2026 |

| Silver HMO | HealthPartners | $379/mo | ~$4,000 | Subsidized enrollees under 250% FPL (CSR eligible) |

| Silver EPO | Medica | ~$425/mo | ~$3,500 | Rural counties where Medica is only option |

A new 2026 change: all Bronze plans on MNsure are now HSA-eligible, making this tier an increasingly popular option for affordable health insurance in Minnesota. The HSA eligibility allows enrollees to contribute pre-tax dollars to a Health Savings Account for medical expenses. This effectively lowers the net cost of Bronze coverage for anyone who can afford to save. An HSA contribution of $4,000 at a 22% marginal tax rate saves approximately $880 in federal taxes — meaningful offset against the higher Bronze deductibles. For detailed plan shopping strategies, the carrier comparison guide covers which insurer is strongest in each county.

Watch the Silver CSR trap: Cost-sharing reductions only apply to Silver plans and only for enrollees under 250% FPL. Choosing a Bronze plan to save on premiums when you’re CSR-eligible often costs more overall because the CSR Silver plan has much lower deductibles and copays. A licensed MNsure-certified assister can run the full cost comparison before you enroll.

Frequently Asked Questions About Affordable Minnesota Coverage

What is the cheapest health insurance in Minnesota?

The most affordable health insurance in Minnesota depends on household income. For Minnesotans earning under 138% FPL, Medical Assistance (Medicaid) is free with no premium. Between 138–200% FPL, MinnesotaCare ranges from $0–$80/month per adult. Above 200% FPL, the cheapest full-price plan is Medica’s Bronze HMO at approximately $234/month for a 40-year-old, though most subsidized enrollees save more with HealthPartners Silver at $379/month because of cost-sharing reductions.

What is MinnesotaCare and who qualifies?

MinnesotaCare is Minnesota’s Basic Health Program, one of only two state BHPs in the country. It covers adults and children with household income between 138% and 200% FPL — roughly $21,597 to $31,300 for a single adult or $44,367 to $64,300 for a family of four in 2026. Monthly premiums range from $0 to approximately $80 per adult depending on income. Benefits include medical, prescription, dental, and vision coverage with very low out-of-pocket costs.

How much are MNsure subsidies in Minnesota?

The average premium tax credit in Minnesota for 2026 is approximately $600/month for eligible families. Subsidies scale based on income and the cost of the benchmark Silver plan in your county. A single adult earning $40,000 typically qualifies for $150–$250/month in tax credits. Minnesotans earning above 400% FPL may or may not qualify depending on whether federal enhanced subsidies are extended by Congress.

Can I get free health insurance in Minnesota?

Yes. Medical Assistance (Minnesota Medicaid) provides free coverage with no monthly premium, no deductible, and minimal copays for Minnesotans earning under 138% FPL. Approximately 1.2 million Minnesotans are enrolled. MinnesotaCare may also be free or near-free for households at the lower end of the 138–200% FPL range. Apply through MNsure, which screens for all three programs simultaneously.

Does Minnesota have a reinsurance program that lowers premiums?

Yes. The Minnesota Premium Security Plan (MPSP) is a state reinsurance program operating under a 1332 waiver. It covers a portion of claims between $50,000 and $250,000 per year, reducing carrier risk and lowering individual market premiums by approximately 25%. Without MPSP, the 2026 rate increase would have been closer to 47% instead of the actual 22% average. Governor Walz signed legislation extending MPSP through 2027.

Is it cheaper to get Bronze or Silver with subsidies?

It depends on income and expected medical use. Silver plans are typically the better value for Minnesotans under 250% FPL because they qualify for cost-sharing reductions (CSRs) that dramatically lower deductibles and copays. Bronze plans have lower premiums but higher deductibles — they work best for healthy enrollees above the CSR threshold who prioritize low monthly costs and have savings to cover a potential deductible.

Related Minnesota Health Insurance Resources

Explore related guides covering Minnesota health insurance across the state, carrier rankings by cost and network, group and small business coverage options, and PPO plans offering out-of-network flexibility.

Plans, carriers, costs, and enrollment across the state.

Best Health Insurance in MinnesotaTop carriers ranked by cost, network, and member satisfaction.

Small Business Health InsuranceGroup plans, SHOP tax credits, and ICHRA for employers.

PPO Health InsuranceOut-of-network flexibility and broader provider access.

Find Affordable Minnesota Coverage for 2026

Get a free eligibility check for Medical Assistance, MinnesotaCare, and MNsure subsidies. Compare cheapest plans by carrier and see your actual after-subsidy cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Minnesota residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.