Minnesota Health Insurance: 2026 Plans, Costs & Coverage Options

Minnesota residents shopping for health insurance in 2026 face a market defined by rising premiums, expiring federal subsidies, and a carrier landscape reshaped by UCare’s acquisition by Medica. This guide covers the six carriers on MNsure, how Minnesota’s reinsurance program holds premiums 25% below what they’d otherwise be, the MinnesotaCare program that serves residents other states send to the marketplace, and how to find the right plan whether you’re in the Twin Cities, Duluth, or rural western Minnesota.

What are you looking for?

How Much Does Minnesota Health Insurance Cost in 2026?

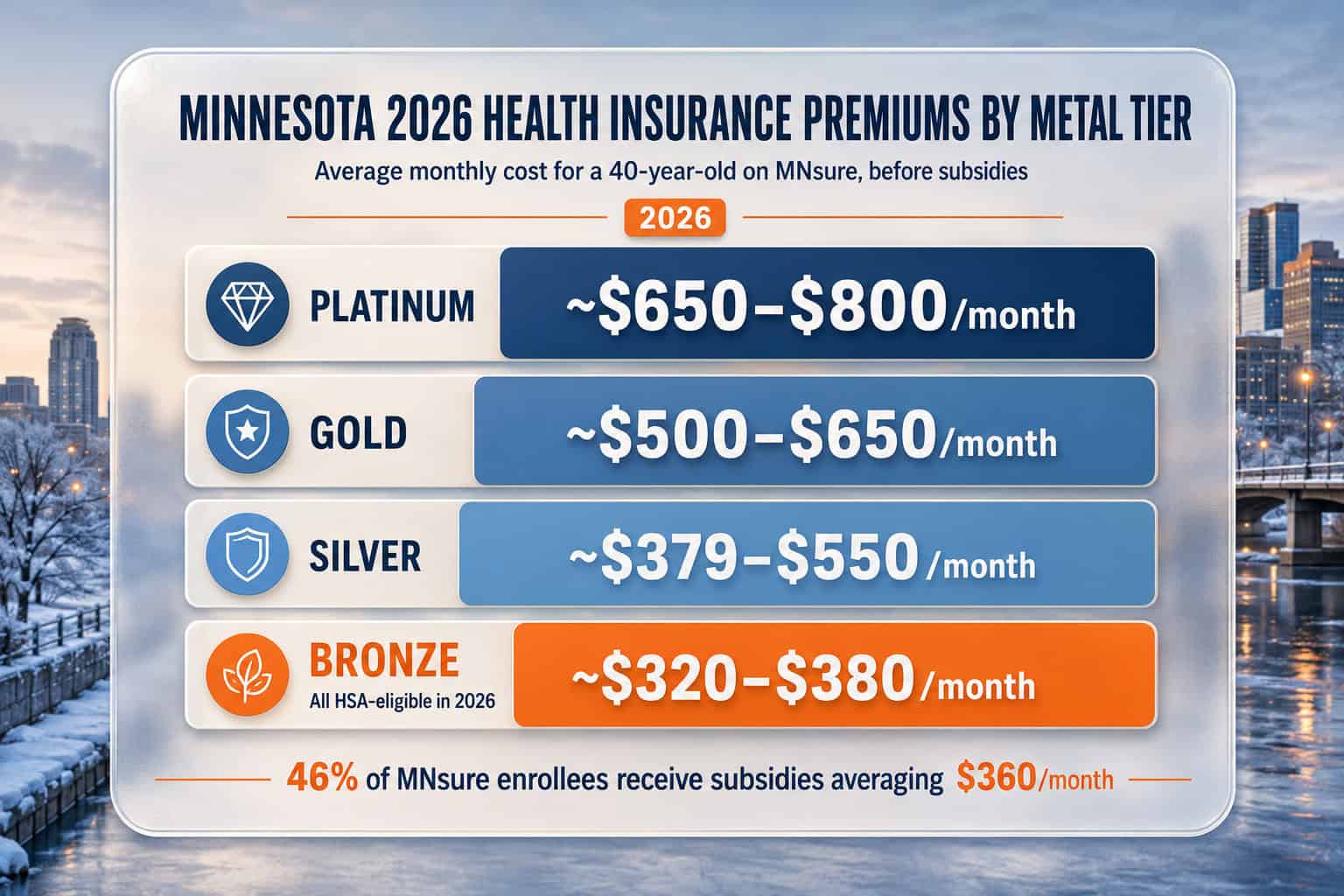

Minnesota health insurance premiums increased an average of 22% for the 2026 plan year — the largest increase since 2017. HealthPartners offers the lowest Silver plan premiums on MNsure at approximately $379/month for a 40-year-old, while the statewide Silver average runs approximately $450–$550/month depending on county and carrier. For the 46% of MNsure enrollees who receive premium tax credits, the average monthly subsidy is $360, and eligible families save an average of $600 per month on coverage.

The 22% average increase reflects both rising healthcare costs and actuarial adjustments for expected enrollment declines after the Enhanced Premium Tax Credit expiration at the end of 2025. Nearly 90,000 Minnesotans are paying an average of $177 more per month for coverage in 2026. Without the Minnesota Premium Security Plan (MPSP) reinsurance program, premiums would be approximately 25% higher still — the MPSP is the single largest factor keeping Minnesota health insurance premiums below what they’d be in a market without state intervention.

Premium variation across carriers is significant. HealthPartners’ lowest Silver plan starts at $379/month for a 40-year-old — the cheapest on MNsure. Blue Plus and UCare (now operating under Medica following the December 2025 acquisition) offer competing Silver plans in the $420–$550 range depending on network tier. Quartz, which serves only southeastern Minnesota, posted the smallest rate increase at 7.4% but exited Olmsted County for 2026. The affordable coverage guide covers strategies for finding the lowest-cost plans by county and income level.

Example: Young Professional in Hennepin County

A 32-year-old marketing coordinator in Minneapolis earning $45,000 per year (approximately 299% FPL) qualifies for roughly $200/month in premium tax credits on MNsure. A HealthPartners Silver plan with a full-price premium of $340/month costs her approximately $140/month after subsidies — with a $4,500 deductible and $8,700 out-of-pocket maximum. Without subsidies, the same plan would consume about 9% of her gross income.

Minnesota Health Insurance Carriers for 2026

Six carriers offer individual plans through MNsure for 2026: Blue Plus (Blue Cross Blue Shield of Minnesota’s entity), HealthPartners, Medica, Quartz, and UCare (now operating under Medica after a December 2025 court-ordered acquisition). Most Minnesotans can choose from at least three carriers, and Twin Cities metro residents have access to all six. Existing UCare enrollees retain their plans unchanged for 2026 despite the acquisition.

| Carrier | Plan Types | Coverage Area | 2026 Avg. Rate Change | Notable Feature |

|---|---|---|---|---|

| Blue Plus (BCBS MN) | HMO, PPO | Statewide networks | +20% to +26% | Largest PPO network; Allina Health + M Health Fairview access |

| HealthPartners | HMO | Twin Cities, central/western MN | +18% to +26% | Lowest Silver premiums ($379/mo); integrated care system |

| HealthPartners Insurance Co. | HMO | Varies by service area | New entity for 2026 | Affiliated with HealthPartners; some enrollees auto-moved |

| Medica | HMO | Regional networks | +17% to +22% | Acquired UCare December 2025; broad regional presence |

| UCare (under Medica) | HMO | 77 counties | +15% to +22% | Broadest HMO coverage (77 counties); nonprofit; plans unchanged for 2026 |

| Quartz | HMO | SE Minnesota (4 counties) | +7.4% | Lowest rate increase; exited Olmsted County for 2026 |

Blue Plus offers the broadest PPO-style network on MNsure, including access to Allina Health, M Health Fairview, and other major systems. For Minnesotans who want specialist access without referrals and the ability to see out-of-network providers, Blue Plus is the primary PPO option. HealthPartners operates an integrated care model — with its own clinics, hospitals (including Regions Hospital in St. Paul and Park Nicollet Methodist Hospital in St. Louis Park), and the Alpine network covering 87,000+ providers including Allina, CentraCare, M Health Fairview, Essentia Health, and Sanford Health. The carrier comparison guide evaluates each carrier’s network, pricing, and service quality in detail.

UCare acquisition update: On December 17, 2025, UCare was placed into court-ordered rehabilitation due to financial difficulties. Medica acquired UCare’s individual and family plans. If you’re enrolled in a UCare plan for 2026, your coverage continues unchanged — same benefits, network, premiums, and plan name. The transition is administrative and does not require action from enrollees.

Compare Minnesota Health Insurance Plans

See 2026 plans from Blue Plus, HealthPartners, Medica, UCare, and Quartz on MNsure. With HealthPartners Silver plans starting at $379/month and eligible families saving an average of $600/month through subsidies, comparing all carriers is the best way to find affordable Minnesota health insurance coverage.

Minnesota’s MPSP Reinsurance Program

The Minnesota Premium Security Plan (MPSP) is a state reinsurance program operating under a federal 1332 waiver that keeps individual market premiums approximately 25% lower than they would be without the program. The MPSP covers a portion of high-cost claims between $50,000 and $250,000 per year, reducing the financial risk for carriers and translating directly into lower premiums for all 187,000 Minnesotans who buy individual health insurance. Governor Walz signed legislation in 2025 extending the MPSP through 2027.

Without the MPSP, the 2026 rate increases — already averaging 22% — would have been closer to 47% according to RAND Health Care modeling commissioned by the Minnesota Council of Health Plans. The program is funded through a combination of federal pass-through savings (because lower premiums reduce federal subsidy spending) and state appropriations. The 2023 Legislature transferred $276 million out of the MPSP account to fund other priorities, nearly ending the program, but the 2025 extension restored funding and directed the Minnesota Department of Commerce to seek a 1332 waiver continuation for plan years 2028 and beyond.

The MPSP’s impact on Minnesota health insurance is visible in the competitive carrier landscape: five health plans offer individual coverage statewide, up from four before the reinsurance program launched in 2018. In states without reinsurance programs, carriers have exited markets and premiums have been more volatile. The program is administered by the Minnesota Comprehensive Health Association (MCHA), which determines the attachment point and reinsurance cap parameters each year.

MinnesotaCare: The Basic Health Program

MinnesotaCare is Minnesota’s Basic Health Program (BHP) — a state-run health coverage option for residents earning between 138% and 200% of the Federal Poverty Level, approximately $21,597 to $30,120 for an individual in 2026. MinnesotaCare is one of only two Basic Health Programs operating in the country (New York’s Essential Plan is the other). Approximately 105,000 Minnesotans are enrolled in MinnesotaCare, which offers comprehensive coverage with premiums ranging from $0 to approximately $80/month depending on income.

MinnesotaCare is the reason Minnesota’s MNsure marketplace statistics look different from the national average. Nationally, 92% of marketplace enrollees receive premium tax credits — in Minnesota, only 46% do. This isn’t because Minnesota is less generous; it’s because MinnesotaCare absorbs the lower-income population (138–200% FPL) that in other states would be on the marketplace with large subsidies. The result is that MNsure’s enrolled population skews higher-income than the national marketplace average, which affects carrier pricing and the subsidy distribution.

Enrollment in MinnesotaCare is year-round — there is no open enrollment restriction. Residents apply through MNsure, which automatically determines whether an applicant qualifies for Medical Assistance (Medicaid, for those under 138% FPL), MinnesotaCare (138–200% FPL), or marketplace plans with subsidies (above 200% FPL). The affordable coverage guide covers MinnesotaCare eligibility and the transition between MinnesotaCare and marketplace coverage in detail.

Medicaid changes ahead: The One Big Beautiful Bill Act (OBBBA), signed July 2025, includes Medicaid changes that will begin taking effect in fall 2026. These changes may affect Medical Assistance and MinnesotaCare eligibility for some Minnesotans, potentially shifting more residents into marketplace plans on MNsure. The Minnesota Department of Human Services will communicate specific changes as implementation dates approach.

Premium Tax Credits & Financial Assistance in Minnesota

Premium tax credits on MNsure are available to Minnesota households earning between 200% and 400% of the Federal Poverty Level — approximately $30,120 to $60,240 for an individual in 2026. Note that Minnesota’s subsidy floor is 200% FPL (not 100% like most states) because MinnesotaCare covers the 138–200% FPL population. In 2026, 46% of MNsure enrollees receive APTC averaging $360 per month, and eligible families save an average of $600 per month — over $7,000 per year.

The expiration of Enhanced Premium Tax Credits at the end of 2025 hit Minnesota’s marketplace hard. Minnesotans earning above approximately $62,000 per year (about $84,000 for a couple) no longer qualify for any tax credits. Nearly 90,000 Minnesotans face an average premium increase of $177/month due to the combined effect of rate hikes and reduced subsidies. During the 2026 open enrollment, MNsure saw an 87% increase in plan switching — most enrollees who switched moved to lower-cost plans, reflecting the affordability pressure. The federal premium tax credit is reconciled at tax time on Form 8962, and the IRS premium tax credit guidance explains how income changes during the year can affect the final credit.

| Income (Individual) | % of FPL | Program | Estimated Monthly Cost |

|---|---|---|---|

| Under $21,597 | Under 138% | Medical Assistance (Medicaid) | $0 |

| $21,597–$30,120 | 138%–200% | MinnesotaCare (BHP) | $0–$80/month |

| $30,120–$60,240 | 200%–400% | MNsure with premium tax credits | ~$140–$505/month (after subsidies) |

| Over $60,240 | Over 400% | MNsure — full price (no subsidy) | ~$379–$800+/month depending on tier |

Cost-sharing reductions (CSRs) are available on Silver plans for a small portion of MNsure enrollees — only 9.6% in 2026, compared to over 50% nationally. Again, this is because MinnesotaCare covers the population (under 200% FPL) that in most states would receive CSRs on marketplace Silver plans. For Minnesotans earning between 200% and 250% FPL who do qualify, CSRs lower the Silver plan deductible and out-of-pocket maximum. The smartest way to gauge your own subsidy is to run an estimate directly on MNsure during Open Enrollment, since the exact credit depends on your income, household size, and the benchmark Silver plan in your county.

How to Enroll in Minnesota Health Insurance

Minnesota residents enroll through MNsure, the state’s health insurance marketplace, which handles private plan enrollment, subsidy eligibility, MinnesotaCare applications, and Medical Assistance referrals. Open enrollment runs from November 1 through January 15 each year — plans selected by December 15 begin January 1, and those selected by January 15 begin February 1. During the 2026 open enrollment, 139,251 Minnesotans enrolled in private plans through MNsure — an 8% decline from the 151,512 enrolled in 2025.

Go to MNsure.org and set up an account. You’ll need Social Security numbers, income information, and employer details for all household members. MNsure automatically determines your eligibility for Medical Assistance, MinnesotaCare, or marketplace plans with subsidies — you don’t need to know which program you qualify for before applying.

MNsure’s Shop and Compare tool shows all available plans in your county with after-subsidy premiums. For 2026, all Bronze plans on MNsure are HSA-eligible — a change from prior years when some Bronze plans didn’t qualify. Compare carriers on premium, network, and whether your doctors are in-network. In the Twin Cities metro, you’ll typically see plans from five or six carriers.

After selecting, pay your first month’s premium to activate coverage. Coverage starts January 1 if enrolled by December 15, or February 1 if enrolled by January 15. A record number of Minnesotans contacted MNsure for help during 2026 enrollment — free assistance is available from certified navigators and brokers statewide. Call MNsure at 855-366-7873.

Upcoming enrollment changes: Starting with the 2027 plan year, open enrollment will end December 31 (not January 15) under new federal rules. All plans selected during open enrollment will take effect January 1. Additionally, starting in 2028, automatic reenrollment will be eliminated for enrollees receiving tax credits — you’ll need to actively confirm your eligibility each year to maintain subsidies.

Types of Health Insurance Plans in Minnesota

Minnesota’s MNsure marketplace offers primarily HMO plans, with Blue Plus as the only carrier providing PPO-style network flexibility for individual coverage. Most MNsure carriers — HealthPartners, Medica, UCare, and Quartz — offer HMO plans requiring a primary care provider and specialist referrals. Blue Plus offers multiple network tiers including PPO options with Allina Health and M Health Fairview access. For 2026, no catastrophic plans are offered on MNsure.

HealthPartners’ integrated care model is distinctive among Minnesota health insurance carriers. HealthPartners operates its own clinics and hospitals — including Regions Hospital, Park Nicollet Methodist Hospital, and a network of primary care clinics across the Twin Cities — and the Alpine network extends access to 87,000+ providers including Allina, CentraCare, Essentia, M Health Fairview, and Sanford Health. This integrated approach can result in better care coordination for members who use HealthPartners facilities, though it requires staying within the system for the most seamless experience.

PPO may be the better fit if

You see specialists regularly and want referral-free access. You want out-of-network coverage. You use providers across multiple health systems (e.g., Allina for your PCP but M Health Fairview for a specialist). Blue Plus is the primary PPO option on MNsure.

HMO may be the better fit if

You want the lowest monthly premium. You prefer coordinated care through one health system. You’re in the Twin Cities where HealthPartners’ integrated model provides comprehensive in-network care. Most MNsure carriers offer HMO plans at lower premiums than Blue Plus PPO.

Short-Term Health Insurance in Minnesota

Short-term health insurance is available in Minnesota as a temporary stopgap — for example, between jobs or while waiting for MNsure coverage to begin. Minnesota permits short-term plans but regulates them more tightly than most states: policies are limited to 185 days and cannot be renewed back-to-back with the same insurer. These plans are not ACA-compliant, so they can deny coverage for pre-existing conditions and exclude essential benefits, making them a poor long-term fit for most Minnesotans.

For most Minnesota residents, a MNsure plan is both more comprehensive and often cheaper than short-term coverage once premium tax credits and MinnesotaCare eligibility are taken into account. Short-term coverage makes sense only in narrow situations: a brief gap before employer coverage starts, or a missed Open Enrollment window with no Qualifying Life Event. Even then, it is worth checking MNsure first for a Special Enrollment Period or MinnesotaCare eligibility, since either provides real ACA coverage that a short-term plan cannot match. Anyone weighing a short-term policy should compare it against a subsidized MNsure option before enrolling.

Minnesota Health Insurance Enrollment Trends for 2026

MNsure enrollment for 2026 private health plans dropped to 139,251 — an 8% decline from the 151,512 enrolled in 2025 and the first significant enrollment decrease in several years. The decline was driven by the expiration of enhanced subsidies, which left nearly 90,000 Minnesotans paying an average of $177 more per month. Plan cancellations increased 50% year-over-year, and new consumer sign-ups dropped from 74,423 in the 2025 enrollment period to significantly fewer for 2026.

Consumer behavior shifted dramatically during the 2026 open enrollment. MNsure reported an 87% increase in the number of enrollees who switched health insurance plans — the vast majority moving to lower-cost options. The trend toward “buying down” — choosing a less expensive plan tier or carrier — increased 112% compared to 2025. Despite the premium increases, 46% of MNsure enrollees still receive APTC with an average monthly credit of $360, and eligible families save an average of $600/month. However, MNsure estimates the full enrollment impact may not materialize until later in 2026 as consumers who maintained coverage through the grace period face sustained higher premiums.

Health Insurance Access Across Minnesota’s Regions

Minnesota health insurance access varies significantly by region. Twin Cities metro residents have access to all six MNsure carriers with the most competitive premiums and broadest networks. Southeastern Minnesota lost options when Quartz exited Olmsted County (home to Rochester and the Mayo Clinic) for 2026. Northern Minnesota relies on Essentia and Sanford systems, with HealthPartners’ Alpine network and UCare as primary options. Rural western counties may have only two or three carriers.

The Twin Cities metro (Hennepin, Ramsey, Dakota, Anoka, Washington, Scott, Carver counties) is the state’s most competitive insurance market. All major health systems — Allina Health, M Health Fairview, HealthPartners, Hennepin Healthcare, and Children’s Minnesota — operate in the metro, and all MNsure carriers have strong metro networks. Moving north to the Duluth area (St. Louis County), Essentia Health and St. Luke’s are the primary hospital systems, and HealthPartners’ Alpine network includes Essentia. In southwestern Minnesota, Sanford Health and CentraCare serve smaller communities, and carrier options narrow.

Quartz’s exit from Olmsted County is particularly notable because Rochester is home to the Mayo Clinic — one of the world’s most recognized medical centers. Mayo Clinic is not in-network for most MNsure plans, so Rochester-area residents who want Mayo coverage typically need employer-sponsored insurance or must pay out-of-network rates. The affordable coverage guide covers plan-selection strategies for different regions, including how to evaluate network adequacy in rural areas where provider options are limited.

Frequently Asked Questions About Minnesota Health Insurance

How much does health insurance cost in Minnesota in 2026?

Minnesota health insurance premiums increased an average of 22% for 2026. HealthPartners offers the lowest Silver plan premiums on MNsure at approximately $379/month for a 40-year-old before subsidies. For the 46% of enrollees who receive premium tax credits, the average monthly subsidy is $360. Eligible families save an average of $600/month. Without the MPSP reinsurance program, premiums would be approximately 25% higher. Nearly 90,000 Minnesotans face an average $177/month increase due to combined rate hikes and EPTC expiration.

What health insurance companies are on MNsure?

Six carriers offer individual plans through MNsure for 2026: Blue Plus (BCBS Minnesota), HealthPartners, HealthPartners Insurance Company (new for 2026), Medica, UCare (now under Medica following a December 2025 acquisition), and Quartz (southeastern Minnesota only, 4 counties). Most Minnesotans can choose from at least three carriers. Twin Cities metro residents have access to all six. UCare plans continue unchanged despite the Medica acquisition.

What is MinnesotaCare?

MinnesotaCare is Minnesota’s Basic Health Program (BHP) — a state-run health coverage option for residents earning between 138% and 200% of the Federal Poverty Level ($21,597–$30,120 for an individual in 2026). It’s one of only two BHPs in the country (New York’s Essential Plan is the other). Approximately 105,000 Minnesotans are enrolled. Premiums range from $0 to about $80/month depending on income. Apply year-round through MNsure — no open enrollment restriction.

What is the MPSP and how does it affect my premiums?

The Minnesota Premium Security Plan (MPSP) is a state reinsurance program that keeps individual market premiums approximately 25% lower than they would be without the program. The MPSP covers a portion of high-cost claims between $50,000 and $250,000 per year, reducing carrier risk and lowering premiums for all 187,000 Minnesotans in the individual market. Governor Walz signed legislation in 2025 extending the MPSP through 2027. Without the MPSP, 2026 rate increases would have been closer to 47%.

When is open enrollment for Minnesota health insurance?

Open enrollment on MNsure runs from November 1 through January 15 each year. Plans selected by December 15 begin January 1, and plans selected by January 15 begin February 1. Starting with the 2027 plan year, open enrollment will end December 31 under new federal rules. Outside of open enrollment, qualifying life events (marriage, job loss, having a baby) trigger a 60-day special enrollment period. MinnesotaCare and Medical Assistance enrollment is year-round.

What happened with UCare?

On December 17, 2025, UCare was placed into court-ordered rehabilitation due to financial difficulties. Medica acquired UCare’s individual and family plans. If you’re enrolled in a UCare plan for 2026, your coverage continues unchanged — same benefits, network, premiums, and plan name. UCare covered 77 Minnesota counties with one of the broadest HMO networks available. The acquisition is administrative and does not require action from current enrollees.

Related Minnesota Health Insurance Resources

Explore related guides covering low-cost coverage and MNsure subsidy strategies, marketplace enrollment steps and deadlines, group and small business coverage options, and PPO plans offering out-of-network flexibility.

Low-cost options, MNsure subsidies, and ways to cut premiums.

MNsure Marketplace & EnrollmentHow to enroll, deadlines, and qualifying life events.

Small Business Health InsuranceGroup plans, SHOP tax credits, and ICHRA for employers.

PPO Health InsuranceOut-of-network flexibility and broader provider access.

Get Minnesota Health Insurance Coverage for 2026

Minnesota’s MPSP reinsurance keeps premiums 25% lower than they’d otherwise be, and 46% of MNsure enrollees receive subsidies averaging $360/month. Compare plans from Blue Plus, HealthPartners, Medica, UCare, and Quartz — check MinnesotaCare eligibility and connect with a licensed enrollment assistant at no cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Minnesota residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.