Individual Health Insurance in Maryland: 2026 Private & Marketplace Plans

Maryland residents purchasing individual health insurance have two pathways: Maryland Health Connection at MarylandHealthConnection.gov (where federal and state subsidies are available) or directly from one of five carriers off-exchange (at full price). Unlike some states, Maryland’s individual and small group markets are separate — individual rates are set independently. This guide covers both pathways, self-employed coverage strategies, and how Maryland’s unique Easy Enrollment and Premium Assistance programs expand access to individual coverage.

What’s your situation?

On-Exchange vs. Off-Exchange Individual Plans in Maryland

Individual health insurance Maryland residents purchase is available both on-exchange (through Maryland Health Connection) and off-exchange (directly from carriers). The key difference: federal APTC and Maryland Premium Assistance subsidies are only available on-exchange. For Maryland residents earning under 400% FPL ($62,600/individual), on-exchange plans are almost always cheaper after combined federal and state subsidies — approximately 80% of applicants receive financial help.

| Feature | On-Exchange (MD Health Connection) | Off-Exchange (Direct from Carrier) |

|---|---|---|

| Subsidies available | Yes — federal APTC + Maryland Premium Assistance | No subsidies available |

| Carriers | 5 (CareFirst ×2, Kaiser, UHC, Wellpoint) | Same 5 + additional off-exchange carriers (Cigna, Aetna) |

| Plan types | HMO + PPO (CareFirst only); Bronze through Platinum | HMO, PPO, POS options from more carriers |

| Enrollment period | OEP (Nov 1–Jan 15) or qualifying life event | OEP for ACA-compliant; year-round for non-ACA |

| Best for | Anyone earning under 400% FPL who qualifies for subsidies | Higher earners wanting PPO flexibility or broader carrier access |

The subsidy calculation makes on-exchange coverage the clear choice for most Maryland residents. An UHC/Optimum Choice Silver HMO that costs $302/month at full price might cost $30–$80/month after federal APTC and Maryland Premium Assistance for someone earning $28,000/year. The state Premium Assistance program — expanded for 2026 from young adults only to all ages up to 400% FPL — adds a layer of subsidy that most other states do not offer, making individual health insurance Maryland residents access through the exchange particularly affordable.

Off-exchange individual plans in Maryland are available from the same five marketplace carriers plus additional off-exchange-only options from Cigna and Aetna (which exited the marketplace but continues off-exchange). Off-exchange plans follow the same ACA essential health benefit requirements if ACA-compliant but lack subsidy access. For residents earning above 400% FPL who want broader PPO options beyond CareFirst’s marketplace PPO, off-exchange provides additional carrier and network choices. The Maryland Insurance Administration publishes approved rates for all individual market carriers.

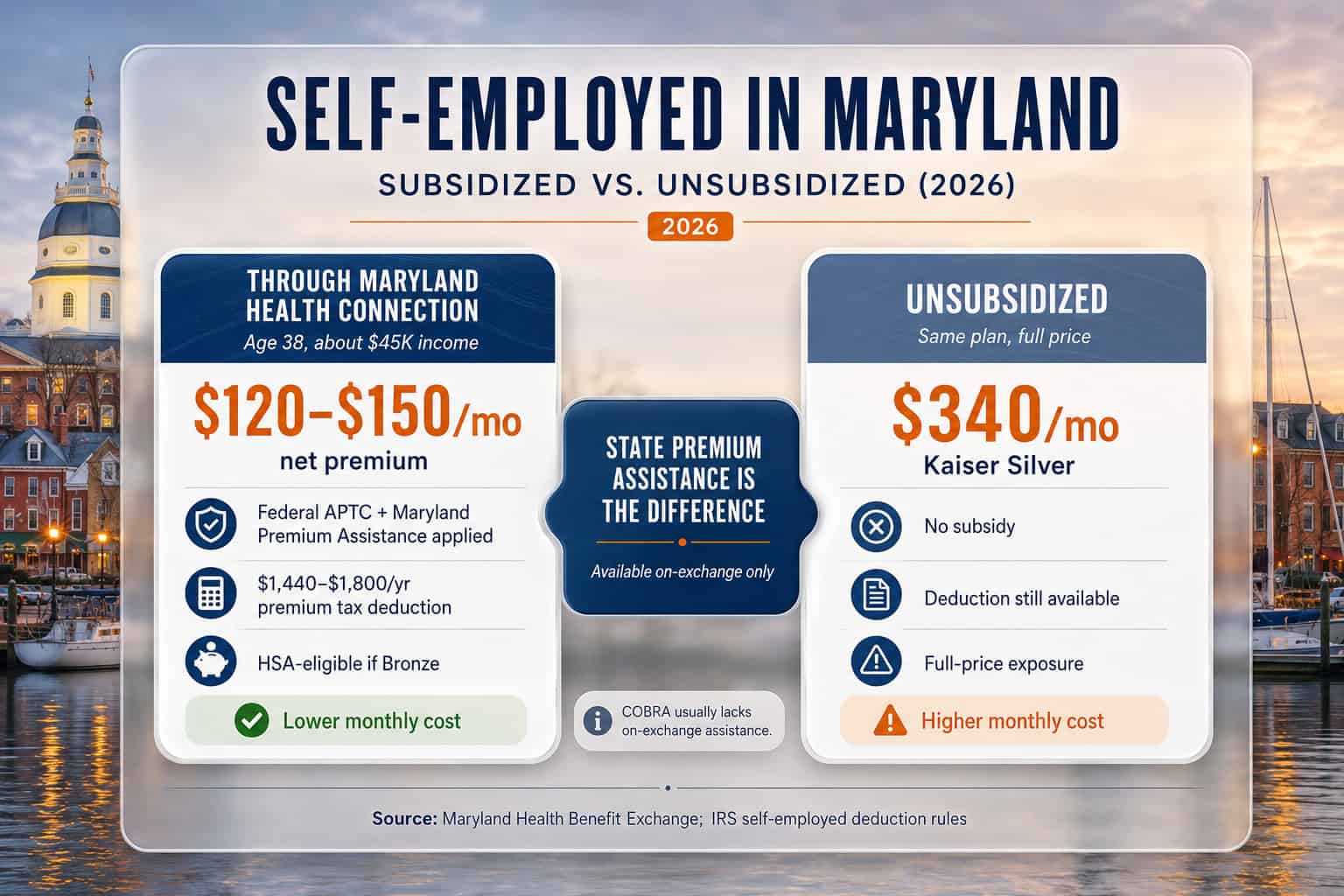

Individual Health Insurance for Self-Employed Maryland Residents

Self-employed Maryland residents — including freelancers, 1099 contractors, gig workers, and sole proprietors — purchase individual health insurance through Maryland Health Connection and qualify for the same federal APTC and Maryland Premium Assistance subsidies as any other enrollee. Self-employed individuals can deduct 100% of health insurance premiums from adjusted gross income on their federal return, and HSA contributions up to $4,400/individual are deductible for 2026.

Maryland’s proximity to Washington, D.C., creates a large population of self-employed consultants, contractors, and gig workers who live in Maryland but work in the DC metro area. These residents purchase individual health insurance Maryland carriers offer through the Health Connection — and should verify that Maryland-based plans cover their preferred DC-area providers if they regularly seek care across state lines. CareFirst’s PPO ($510/month Silver) and CareFirst BlueChoice HMO both include some DC-area providers, while Kaiser Permanente serves the Baltimore–DC corridor with its own integrated facilities on both sides of the state line.

Easy Enrollment for self-employed: Maryland’s Easy Enrollment program is particularly useful for self-employed residents who may not realize they qualify for subsidized coverage. By checking a box on the Maryland state income tax return, freelancers and contractors can share information with Maryland Health Connection. If the exchange determines they may qualify for free or low-cost coverage, it follows up with enrollment assistance — connecting self-employed residents with individual health insurance Maryland subsidies they might otherwise miss.

Compare Individual Health Insurance Plans in Maryland

See on-exchange and off-exchange options, check Maryland Premium Assistance eligibility, and compare carriers for your county.

Who Buys Individual Health Insurance in Maryland?

Maryland’s individual health insurance market serves approximately 290,000+ enrollees through Maryland Health Connection, plus an additional off-exchange population. The typical individual plan buyer is self-employed, works for a small business without group coverage, is between jobs, or is an early retiree under 65. Per CMS enrollment data, approximately 80% of Maryland marketplace applicants receive financial help through federal and state subsidies.

Self-employed & freelancers

No employer coverage available. Eligible for Maryland Premium Assistance and federal APTC based on net self-employment income. Maryland’s large DC-metro contractor and consultant population drives significant individual plan enrollment in Montgomery, Prince George’s, and Howard counties. Easy Enrollment via state tax return helps connect self-employed residents with subsidized coverage they may not know they qualify for.

Between jobs or transitioning

Job loss triggers a 60-day special enrollment period on Maryland Health Connection. Individual coverage through the exchange is typically cheaper than COBRA for Maryland residents who qualify for subsidies. COBRA preserves the existing employer plan at full cost — often $600–$900/month for individual coverage. Maryland does not have a state individual mandate, so there is no penalty for a temporary coverage gap.

Early retirees (under 65)

Bridge coverage between employer retirement and Medicare at 65. Maryland uses the federal 3:1 age rating ratio — a 62-year-old pays up to 3x what a 21-year-old pays for the same plan. Maryland Premium Assistance can significantly reduce this cost for retirees with income below 400% FPL ($62,600/individual). The state reinsurance program also keeps base premiums lower for all enrollees regardless of age.

DC-area workers with Maryland residence

Maryland residents who work in DC or Virginia purchase individual health insurance through Maryland Health Connection — not the DC or Virginia exchanges. Verify that Maryland-based carrier networks include your preferred DC-area providers. CareFirst and Kaiser both serve the Baltimore–DC corridor. The Best Health Insurance in Maryland guide maps carrier networks by region.

Maryland’s state reinsurance program — established in 2019 — benefits all individual market enrollees by keeping full-price premiums lower than they would otherwise be. Combined with the expanded Maryland Premium Assistance program (177,000 enrollees receiving state subsidies for 2026), individual health insurance Maryland residents access through the exchange is among the most heavily subsidized in the mid-Atlantic region. The Affordable Health Insurance in Maryland guide covers all cost-saving strategies including Value Plans and CSR eligibility.

Individual Health Insurance FAQ for Maryland

Common questions about individual health insurance Maryland residents face — including on-exchange vs. off-exchange differences, self-employed deductions, COBRA alternatives, Easy Enrollment, and how Maryland Premium Assistance affects 2026 individual plan costs.

Can I buy individual health insurance outside of Maryland Health Connection?

Yes. Off-exchange individual plans are available directly from the same five marketplace carriers plus Cigna and Aetna (which exited the marketplace but continue off-exchange). However, off-exchange plans do not qualify for federal APTC or Maryland Premium Assistance subsidies. For Maryland residents earning under 400% FPL ($62,600/individual), on-exchange plans through Maryland Health Connection are almost always cheaper after subsidies.

Can self-employed people in Maryland deduct health insurance premiums?

Yes. Self-employed Maryland residents can deduct 100% of health insurance premiums (net of subsidies received) as an above-the-line deduction on the federal return (Form 1040). For 2026, HSA contributions are also deductible up to $4,400/individual or $8,750/family, and all marketplace Bronze and Catastrophic plans now qualify as HDHPs for HSA eligibility. Maryland does not have a separate state-level health insurance premium deduction beyond the federal AGI adjustment that flows through to the state return.

Is COBRA or Maryland Health Connection cheaper?

For most Maryland residents who qualify for subsidies, Maryland Health Connection plans are significantly cheaper than COBRA. COBRA continuation requires paying the full employer + employee premium share — often $600–$900/month for individual coverage. A subsidized Silver plan through Maryland Health Connection for someone earning $32,000/year might cost $65–$95/month after federal and state subsidies. COBRA makes sense only when the employer plan has unique provider access or when income exceeds subsidy eligibility.

What is Easy Enrollment and how does it help with individual coverage?

Easy Enrollment is a Maryland-specific program that lets residents check a box on their state income tax return to share information with Maryland Health Connection. If the exchange determines you may qualify for free or low-cost health coverage, it follows up with enrollment assistance. This is particularly useful for self-employed residents and gig workers who may not realize they qualify for subsidized individual health insurance Maryland offers through the exchange.

Does Maryland have an individual mandate penalty?

No. Maryland does not have a state individual mandate — there is no state-level tax penalty for going without health insurance. The federal individual mandate penalty was eliminated in 2019. Maryland residents can choose whether to purchase coverage without facing a fine. However, approximately 80% of Maryland Health Connection applicants qualify for financial help, making subsidized coverage significantly more affordable than paying out of pocket for medical care.

More Maryland Health Insurance Guides

Explore related guides for individual coverage in Maryland — the statewide overview, marketplace enrollment, affordable coverage and subsidies, carrier comparisons, small business plans, and nationwide PPO options.

Plans, carriers, costs, and enrollment across the state.

Marketplace & EnrollmentHow to enroll, deadlines, and qualifying life events.

Affordable Coverage & SubsidiesPremium Assistance, Medicaid, and low-cost plan options.

Best Plans & CarriersCareFirst, Kaiser, and UHC ranked and compared.

Small Business Group PlansGroup coverage options for Maryland employers.

Nationwide PPO PlansFlexibility for specialists and out-of-network care.

Find Individual Health Insurance in Maryland

Compare Maryland Health Connection and off-exchange plans from five carriers. Check state and federal subsidy eligibility and see 2026 pricing for your county.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Maryland residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.