Small Business Health Insurance in Maryland: 2026 Group Plans & Options

Maryland small businesses with 1–50 employees can offer health coverage through group plans from CareFirst, Kaiser Permanente, and UHC — with the 2026 small group market seeing an average rate increase of only 5.5%, significantly lower than the individual market’s 13.4%. The Maryland Health Benefit Exchange operates a small business marketplace through Maryland Health Connection, and the SHOP tax credit remains available for qualifying employers. This guide covers group plan options, the ICHRA alternative, tax credit eligibility, and how to set up small business health insurance Maryland employers can offer.

What does your business need?

Small Business Health Insurance Options in Maryland

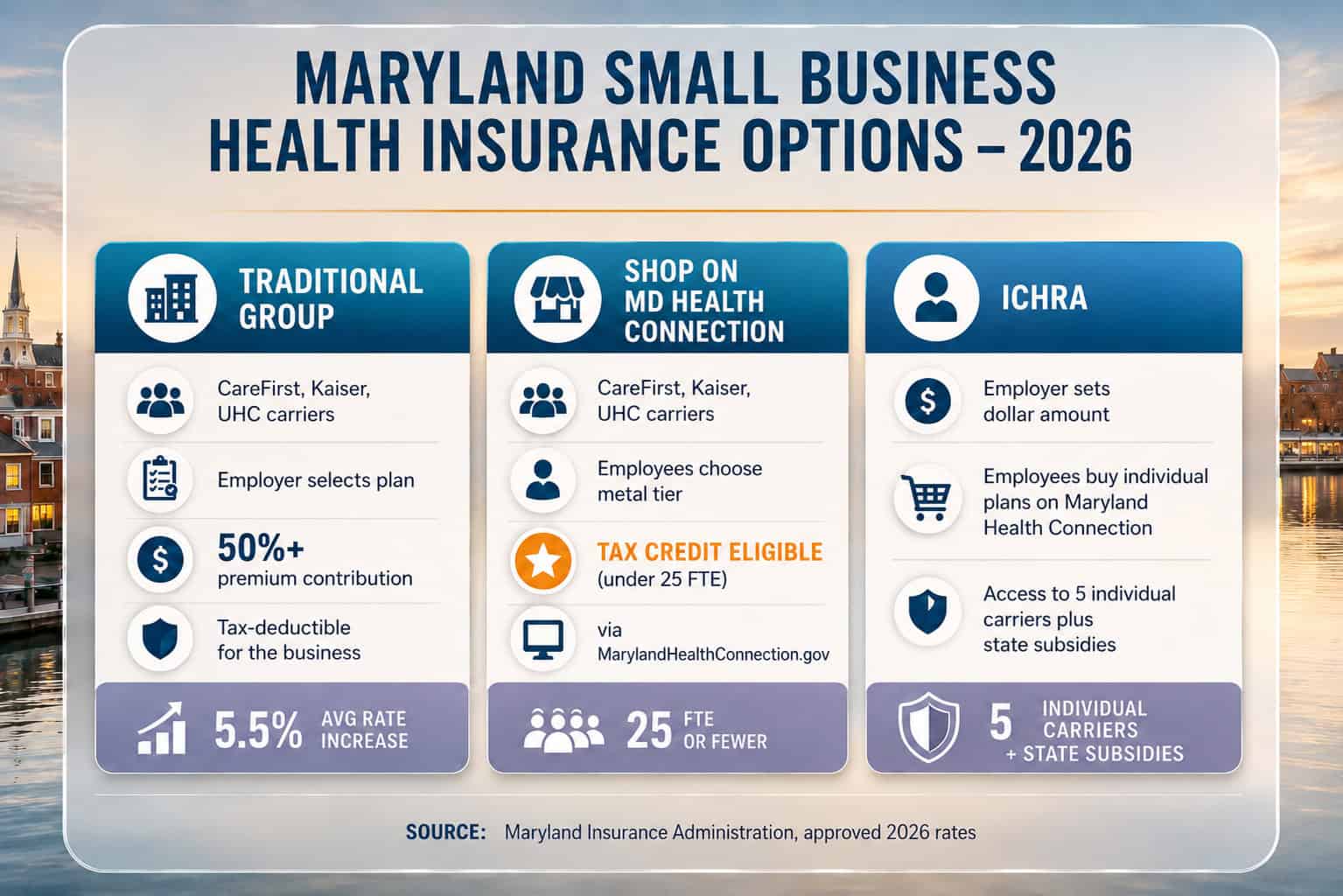

Small business health insurance Maryland employers can access comes through three primary channels: traditional small group plans from CareFirst, Kaiser Permanente, and UHC/Optimum Choice purchased directly or through a broker; the SHOP marketplace on Maryland Health Connection for tax credit eligibility; or an Individual Coverage Health Reimbursement Arrangement (ICHRA) that reimburses employees for individual plan premiums. Maryland’s small group and individual markets are separate — unlike some states, small group rates are set independently.

| Option | Eligible Businesses | Carriers in MD | Tax Credit Eligible | Employee Choice |

|---|---|---|---|---|

| Traditional small group | 1–50 FTE | CareFirst (3 entities), Kaiser, UHC | No (unless through SHOP) | Employer selects plan; employees enroll |

| SHOP on MD Health Connection | 1–50 FTE | Same carriers, via MHBE | Yes — under 25 FTE + avg wages under $58,000 | Employees may choose from available metal tiers |

| ICHRA | Any size | Any — employees choose their own | No (but contributions are tax-free) | Full employee choice — MD Health Connection or off-exchange |

| QSEHRA | Under 50 FTE, no group plan | Any — employees choose their own | No (but contributions are tax-free) | Full employee choice; max $6,350/individual in 2026 |

Maryland’s separate small group market means that small business rates are not affected by individual market dynamics — the 5.5% average small group rate increase for 2026 is less than half the 13.4% increase in the individual market. Per the Maryland Insurance Administration, small group carriers can request rate changes on a quarterly basis, so rates may adjust throughout 2026. CareFirst operates three small group entities in Maryland — CareFirst BlueChoice (HMO), CareFirst of Maryland (BCBS), and GHMSI (BCBS/PPO) — giving employers both HMO and PPO options within the CareFirst network.

Small Business Health Care Tax Credit in Maryland

For Maryland employers, the SHOP tax credit only flows through Maryland Health Connection’s small business portal — buying the same plan off-exchange forfeits it. A Maryland business with under 25 full-time-equivalent employees, average wages below $58,000, and an employer contribution covering at least half of employee-only premiums can claim up to 50% of its contributions (35% for tax-exempt Maryland nonprofits) on IRS Form 8941. The credit runs for two consecutive tax years and phases down as headcount and wages rise.

Maryland Small Group Rates for 2026

Small business health insurance Maryland employers purchase saw an average approved rate increase of 5.5% for 2026 — significantly lower than the individual market’s 13.4%. Small group premiums in Maryland are community-rated based on employee ages, tobacco use, and county. Carrier-level small group rate increases range from 3.3% to 12.2%, and carriers can adjust rates quarterly throughout the year.

A 10-person group in the Baltimore metro area with an average employee age of 38 can expect small group Silver premiums of approximately $500–$650/month per employee before employer contributions. CareFirst’s three entities offer the broadest small group network — including Johns Hopkins, University of Maryland Medical Center, and MedStar facilities. Kaiser Permanente’s closed-network model offers lower premiums for businesses near Kaiser facilities in the Baltimore–Washington corridor. The Best Health Insurance in Maryland guide profiles each carrier’s network by region.

The ICHRA alternative is increasingly popular for small business health insurance Maryland employers consider, particularly for businesses with employees spread across the Baltimore metro, DC suburbs, and rural counties. With an ICHRA, the employer sets a fixed monthly dollar amount (e.g., $400/employee) and employees purchase their own individual plans through Maryland Health Connection. Employees earning under 400% FPL may qualify for Maryland Premium Assistance — a state subsidy that further reduces their out-of-pocket costs on top of the employer’s ICHRA contribution. Per Maryland Health Connection, approximately 80% of marketplace applicants receive financial help.

Compare Maryland Small Business Health Plans

See group plan options from CareFirst, Kaiser, and UHC, check SHOP tax credit eligibility, and explore ICHRA alternatives for your Maryland business.

How to Set Up Small Business Health Insurance in Maryland

Setting up small business health insurance Maryland employers manage involves choosing a coverage type (group plan, SHOP, or ICHRA), selecting carriers (CareFirst, Kaiser, UHC), determining contribution levels (minimum 50% for SHOP tax credit eligibility), and enrolling employees. Maryland’s small business marketplace operates through Maryland Health Connection — not HealthCare.gov.

Determine your employee count and budget

Count full-time equivalent employees (30+ hours/week). Maryland businesses under 25 FTE with average wages under $58,000 should evaluate SHOP for the tax credit. Businesses with 1–5 employees may find ICHRA or QSEHRA more cost-effective than traditional group rates, especially in a year with 5.5% average small group increases.

Choose a coverage approach

Traditional group plan (employer selects carrier and plan), SHOP through Maryland Health Connection (employees may choose metal tier, tax credit available), or ICHRA (employer sets dollar amount, employees buy their own plans — potentially qualifying for Maryland Premium Assistance). Each approach has different administrative and cost implications.

Get quotes from Maryland small group carriers

CareFirst (three entities — BlueChoice HMO, CareFirst of Maryland BCBS, and GHMSI PPO), Kaiser Permanente, and UHC/Optimum Choice serve the Maryland small group market. Provide employee census data (ages, zip codes, tobacco status) for accurate quotes. Small group rates can adjust quarterly — request quotes close to your intended effective date.

Enroll and communicate to employees

Group plans can start the first of any month — no open enrollment restriction for employers. SHOP enrollment goes through the Maryland Health Benefit Exchange small business portal. Provide employees with plan details, contribution amounts, and network information. Coverage activates once the first premium payment is processed.

Maryland Small Business Health Insurance FAQ

Which carriers offer small group plans in Maryland?

CareFirst operates three small group entities in Maryland — CareFirst BlueChoice (HMO), CareFirst of Maryland/BCBS, and GHMSI/BCBS (PPO). Kaiser Permanente and UHC/Optimum Choice also serve the small group market. CareFirst offers the broadest network in the state, while Kaiser is limited to its facilities in the Baltimore–Washington corridor. Small group rate increases for 2026 averaged 5.5% across all carriers.

Is the Maryland small group market separate from the individual market?

Yes. Maryland operates separate individual and small group markets — unlike some states that merge these markets. This means small group rates are set independently with their own risk pool dynamics. The 2026 small group average rate increase of 5.5% is significantly lower than the individual market’s 13.4% increase, reflecting the more stable employer-sponsored risk pool.

Does Maryland require employers to offer health insurance?

Maryland has no state employer mandate requiring small businesses to offer health insurance. The federal ACA employer mandate applies only to Applicable Large Employers with 50 or more full-time equivalent employees. Businesses with fewer than 50 FTEs face no federal penalty for not offering coverage. Small business health insurance Maryland employers provide is voluntary for businesses under 50 FTE.

What is the Small Business Health Care Tax Credit?

The tax credit is worth up to 50% of employer premium contributions (35% for tax-exempt organizations) for small businesses purchasing through the SHOP marketplace. To qualify: fewer than 25 FTEs, average annual wages under $58,000, and coverage of at least 50% of employee-only premiums. The maximum credit applies to businesses with 10 or fewer FTEs and average wages under $30,000. Claimed on IRS Form 8941.

Can employees get Maryland Premium Assistance with an ICHRA?

It depends on the ICHRA contribution amount and employee income. If the employer’s ICHRA contribution is considered “affordable” under ACA standards, the employee may not qualify for individual marketplace subsidies including Maryland Premium Assistance. If the contribution falls below the affordability threshold, the employee can decline the ICHRA and receive full marketplace subsidies — including Maryland’s expanded state subsidy for enrollees up to 400% FPL.

More Maryland Health Insurance Guides

Explore related guides for Maryland employers and individuals — the statewide overview, marketplace enrollment, affordable coverage and subsidies, carrier comparisons, individual plans, and nationwide PPO options.

Plans, carriers, costs, and enrollment across the state.

Marketplace & EnrollmentHow to enroll, deadlines, and qualifying life events.

Affordable Coverage & SubsidiesPremium Assistance, Medicaid, and low-cost plan options.

Best Plans & CarriersCareFirst, Kaiser, and UHC ranked and compared.

Individual & Private PlansCoverage options for individuals and families in Maryland.

Nationwide PPO PlansFlexibility for specialists and out-of-network care.

Find Small Business Health Insurance for Your Maryland Team

Compare group plans from CareFirst, Kaiser, and UHC, check SHOP tax credit eligibility, and explore ICHRA options. Licensed enrollment assistance at no cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Maryland businesses. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.