Small Business Health Insurance in Arkansas 2026: Group, ICHRA & Options

Small business health insurance in Arkansas for 2026 runs through three main paths: traditional small group plans purchased directly from carriers, the Individual Coverage Health Reimbursement Arrangement (ICHRA) that lets employees choose their own plans with employer-funded dollars, and the QSEHRA for the smallest employers. There is no functioning SHOP marketplace in Arkansas — carriers withdrew before 2019, leaving direct-to-carrier and HRA-based approaches as the practical options for small business health insurance in Arkansas. Small group rates increased roughly 7.9 percent for 2026, significantly below the 22.2 percent individual market increase. This guide covers what Arkansas employers actually use, how costs compare, the small business tax credit, and when ICHRA outperforms traditional group coverage for small business health insurance in Arkansas.

What are you looking for?

Arkansas Small Business Coverage Options at a Glance

Arkansas small employers have three main health coverage structures to consider in 2026. Traditional group plans provide employer-selected coverage through direct carrier contracts. ICHRA gives employees individual plan choice with employer-funded tax-free reimbursements. QSEHRA is the simpler HRA option for employers under 50 FTEs with lower contribution ceilings. The defunct SHOP marketplace — no longer active in Arkansas since carriers withdrew before 2019 — is not a functional path.

| Option | Who It Fits | 2026 Cost Control | Employee Choice | Tax Credit Available? |

|---|---|---|---|---|

| Traditional group plan | 10–50 employees; stable workforce | Shared premium; fixed renewal | Employer selects plan(s) | Yes — if under 25 FTEs (2 yr max) |

| ICHRA | Any size; variable workforce | Fixed monthly allowance per employee | Employee picks own plan | No direct credit; fully tax-deductible |

| QSEHRA | Under 50 FTEs; no group plan | Capped reimbursement ($537.50/mo single) | Employee picks own plan | No direct credit; tax-deductible |

| SHOP marketplace | N/A in Arkansas | N/A — no carriers participating | N/A | N/A — defunct since ~2019 |

Traditional Group Plans — Costs and Carriers in Arkansas

Arkansas small group health insurance rates increased approximately 7.9 percent for 2026 — significantly lower than the individual market’s 22.2 percent increase. The gap exists because small group pricing is based on community rating and group risk pools, not the same benchmark Silver loading mechanism that drove individual market increases. Arkansas small employers purchasing group coverage buy directly from carriers, with ArkBCBS (Health Advantage, USAble Mutual) and Ambetter (Centene) as the primary options in most counties.

| Coverage Level | Avg Annual Employer Cost | Avg Monthly per Employee | Typical Employer Share |

|---|---|---|---|

| Single (employee-only) | ~$7,500–$8,500/yr | ~$625–$710/mo | ~84% of premium |

| Family coverage | ~$22,000–$26,000/yr | ~$1,833–$2,167/mo | ~75% of premium |

| 2026 rate increase (small group) | ~7.9% over 2025 | — | — |

Arkansas county rate uniformity: Unlike most states where urban premiums run significantly higher than rural, Arkansas marketplace rates are unusually uniform across all 75 counties — average Bronze premiums for a 30-year-old run roughly $374 per month regardless of county. This simplifies cost modeling for Arkansas small employers with workers in multiple counties, from Bentonville in Benton County to Blytheville in Mississippi County.

Arkansas small employers with workers across Pulaski, Benton, and Washington counties — the state’s three largest employment markets — can typically structure a single group plan covering the entire workforce without county-specific pricing complications. For businesses with employees in rural Delta counties, carrier network access is the more important consideration than premium differences.

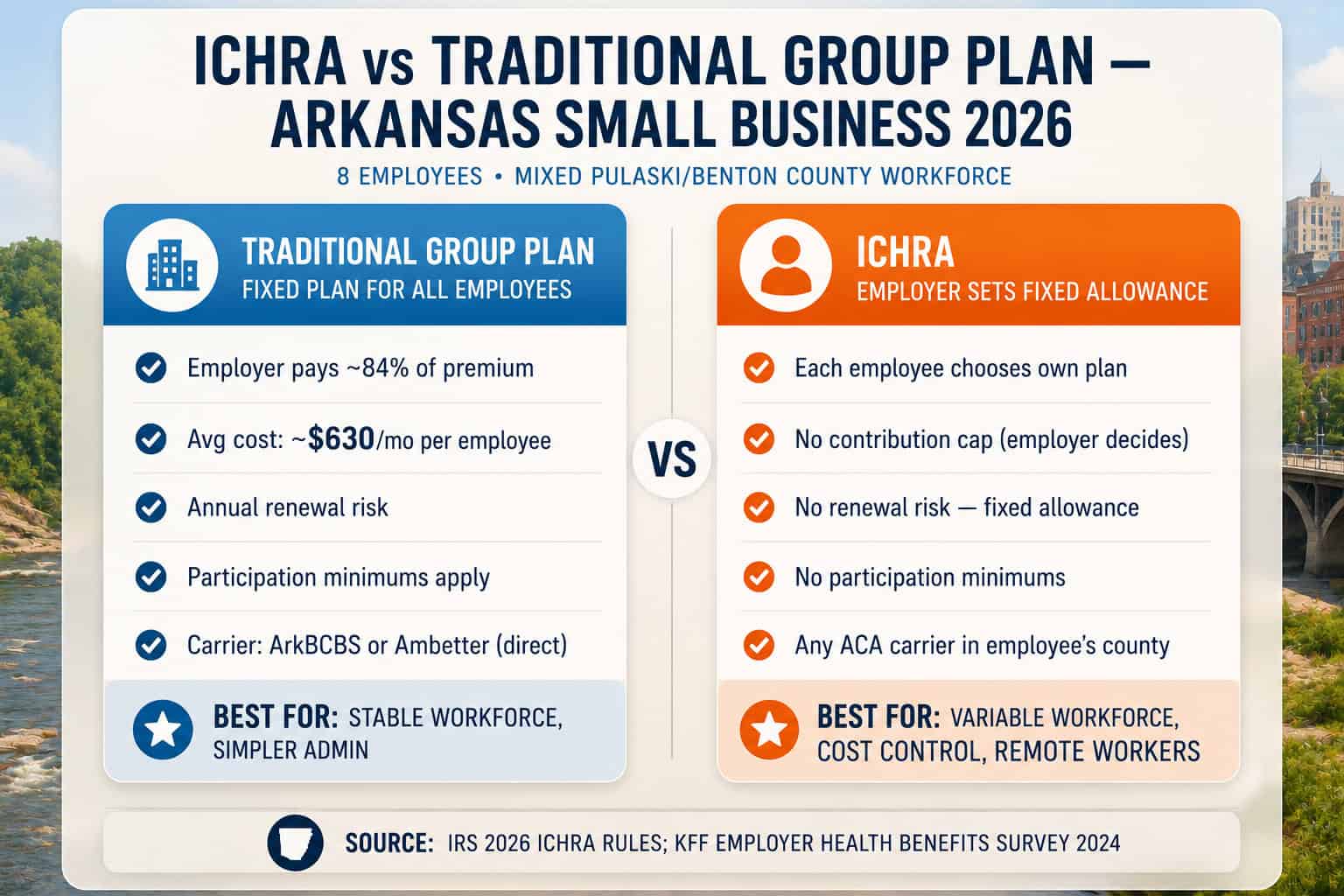

ICHRA — The Group Plan Alternative for Arkansas Employers

The Individual Coverage Health Reimbursement Arrangement (ICHRA) has emerged as the dominant alternative to traditional group coverage for small business health insurance in Arkansas, particularly in the Bentonville supplier ecosystem where workforce composition varies widely. An ICHRA lets the employer set a fixed monthly dollar allowance per employee class; employees then shop for their own ACA-compliant plan on HealthCare.gov or off-exchange and submit premiums for tax-free reimbursement.

| Feature | Traditional Group Plan | ICHRA |

|---|---|---|

| Employer contribution cap | Open-ended (% of premium) | Fixed allowance set by employer |

| Employee plan choice | Employer selects plan(s) | Employee chooses any ACA plan |

| Contribution limit (2026) | No IRS cap | No IRS cap |

| Tax treatment | Employer deducts premiums | Reimbursements tax-free for both |

| Participation minimums | Yes — typically 70% of eligible | None |

| Renewal risk | Annual rate renewal | Employer sets allowance; no renewal |

| Multi-county workforce | Single plan, varied network fit | Each employee picks local plan |

| Subsidy interaction | Employees ineligible for marketplace subsidies | Employees ineligible if ICHRA is affordable |

Scenario — Conway retailer, 8 employees, mixed income: A Conway small business with 4 employees earning $32,000 and 4 earning $55,000. The lower-income employees qualify for significant marketplace subsidies if not covered by an affordable employer plan. An ICHRA set deliberately below the 9.96% affordability threshold lets lower-income employees keep their marketplace subsidy while the employer provides some reimbursement — a design strategy that maximizes employee take-home value without the employer paying full group premiums. Employees shopping on the Arkansas HealthCare.gov marketplace can combine their subsidy with the ICHRA reimbursement when the arrangement is structured as “unaffordable” by design.

Get a Small Business Health Insurance Quote for Arkansas

ForHealthInsurance.com compares direct-to-carrier group plans and ICHRA structures for Arkansas small employers. Licensed brokers, no carrier preference, no extra cost.

Get a Quote Call 888-215-4045The Small Business Health Care Tax Credit in Arkansas

The Small Business Health Care Tax Credit covers up to 50 percent of premiums paid (35 percent for tax-exempt organizations) for qualifying Arkansas employers. The credit is available for two consecutive tax years and is claimed on IRS Form 8941. Qualification requires meeting all three thresholds: fewer than 25 FTE employees, average annual wages below approximately $56,000 (adjusted annually), and payment of at least 50 percent of the employee-only premium cost.

| Criterion | Maximum Credit Threshold | Phase-Out Ceiling |

|---|---|---|

| FTE employee count | 10 or fewer | 25 FTEs (credit phases out completely) |

| Average annual wages | Below ~$28,000 | ~$56,000 (credit phases out completely) |

| Employer premium contribution | 50%+ of employee-only premium | Required — no credit below 50% |

| Maximum credit (for-profit) | 50% of premiums paid | 2 consecutive years only |

| Maximum credit (tax-exempt) | 35% of premiums paid | 2 consecutive years only |

Two-year limit: The Small Business Health Care Tax Credit is available for only two consecutive tax years, not indefinitely. Arkansas employers who qualify should use the credit intentionally — it is best used while exploring whether ICHRA provides better long-term cost structure after the credit period ends. After two years, the credit disappears and the full group premium cost returns.

The credit is most valuable for the smallest Arkansas employers — a Searcy restaurant with 8 employees averaging $26,000 in wages that pays $4,000 per year per employee in premiums could receive up to $16,000 in federal tax credits ($4,000 × 8 employees × 50%) over two years. An employer of 15 workers averaging $45,000 would receive a smaller, partially phased-out credit. The HealthCare.gov small business tax credit estimator calculates the credit based on employee count, wages, and premium contribution.

ACA Employer Rules for Arkansas Small Businesses

Arkansas employers with fewer than 50 full-time equivalent employees are not subject to the ACA employer shared responsibility mandate — offering health insurance is optional. The mandate applies only to Applicable Large Employers (ALEs) with 50 or more FTEs, who must offer coverage meeting the 2026 affordability threshold of 9.96 percent of household income or face potential penalties under IRS Code Section 4980H.

| Business Size | ACA Mandate | 2026 Affordability Threshold | Recommended Path |

|---|---|---|---|

| 1–9 employees | None | N/A | ICHRA or QSEHRA for cost control |

| 10–24 employees | None | N/A | Group plan or ICHRA; tax credit if qualifying |

| 25–49 employees | None | N/A | Group plan or ICHRA — competitive benefit needed |

| 50+ employees (ALE) | Required | 9.96% of employee household income | Group plan or ICHRA meeting affordability |

For most Arkansas small employers — the Walmart supplier firms in Bentonville, the healthcare-adjacent businesses near UAMS in Little Rock, the agricultural service businesses in the Delta — the mandate is irrelevant. Small business health insurance in Arkansas is a competitive recruiting tool rather than a legal requirement for businesses under 50 FTEs. In a tight labor market, small business health insurance in Arkansas is one of the few benefits that meaningfully differentiates an employer. The Department of Labor EBSA small business health coverage guide covers employer obligations and rights in detail.

Frequently Asked Questions About Arkansas Small Business Coverage

Does Arkansas have a SHOP marketplace for small businesses?

No. Arkansas formerly operated a SHOP marketplace but carriers withdrew before 2019, leaving no insurer participation. Arkansas small employers now purchase group health insurance directly from carriers — Ambetter, Arkansas BlueCross BlueShield, QualChoice, and others — or use ICHRA or QSEHRA to reimburse employees for individual marketplace plans they choose themselves.

Are Arkansas small businesses required to offer health insurance?

No. Arkansas employers with fewer than 50 full-time equivalent employees are not required by the ACA to offer health insurance. The employer shared responsibility mandate applies only to businesses with 50 or more FTEs. Offering coverage is optional for small employers, though many do so to attract employees in competitive markets like Bentonville, Little Rock, and Fayetteville.

What is the small business health care tax credit in Arkansas?

The Small Business Health Care Tax Credit covers up to 50 percent of premiums paid for qualifying Arkansas employers with fewer than 25 FTE employees, average annual wages below approximately $56,000, and payment of at least 50 percent of employee-only premium costs. The credit is available for two consecutive tax years only and is most valuable for employers with 10 or fewer employees earning average wages below $28,000.

What is ICHRA and how does it work for Arkansas small businesses?

An ICHRA lets Arkansas employers of any size reimburse employees tax-free for individual health insurance premiums and qualified medical expenses up to a fixed monthly allowance set by the employer — with no IRS cap on the amount. Each employee buys their own ACA-compliant plan. ICHRA eliminates group plan participation minimums, annual renewal risk, and COBRA obligations while giving employees network and plan choice.

How much does small business health insurance cost in Arkansas?

Small group health insurance in Arkansas increased approximately 7.9 percent for 2026. Average employer cost for employee-only coverage runs roughly $625 to $710 per month, with employers typically covering about 84 percent of the single-coverage premium. Arkansas Bronze premiums are unusually uniform across all 75 counties at around $374 per month for a 30-year-old, simplifying cost projections for businesses with employees in multiple counties.

Related Arkansas Health Insurance Resources

Explore the rest of the Arkansas guide — the statewide overview, individual marketplace plans, carrier comparisons, affordability, and off-exchange private options.

Full 2026 overview — ARHOME, ARKids, marketplace, and all coverage paths.

Arkansas Costs & Silver LoadIndividual market cost guide — after-subsidy pricing and the 46% Silver load.

Best Arkansas Health PlansAll 6 carriers compared — premiums, quality ratings, and PPO availability.

Arkansas MarketplaceEnrollment windows, deadlines, and subsidy eligibility on HealthCare.gov.

Arkansas Private & Off-ExchangeOff-marketplace PPO plans for self-employed Arkansans and buyers above 400% FPL.

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required.

Get Small Business Health Insurance Quotes for Arkansas

ForHealthInsurance.com compares direct-to-carrier group plans, ICHRA structures, and QSEHRA options for Arkansas small employers. Licensed brokers, no carrier preference, no extra cost.

Get a Quote Call 888-215-4045Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Arkansas businesses. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.