Affordable Health Insurance in Connecticut 2026: Costs, Subsidies & Programs

Finding affordable health insurance in Connecticut for 2026 requires understanding four layers of financial assistance that stack on top of each other — and knowing which tier of coverage is the right choice at your income. Connecticut’s average Silver plan premium for a 40-year-old runs $859 per month before subsidies, but the average subsidy-eligible Access Health CT enrollee pays about $310 per month after credits. For residents earning below 175 percent of the federal poverty level, Covered Connecticut offers full coverage at $0. The sticker price on a Connecticut health insurance plan almost never reflects what most buyers actually pay. This guide breaks down what affordable health insurance in Connecticut actually costs by income, which programs help, and when the marketplace stops being the cheapest option.

What’s your situation?

What Affordable Health Insurance in Connecticut Actually Costs in 2026

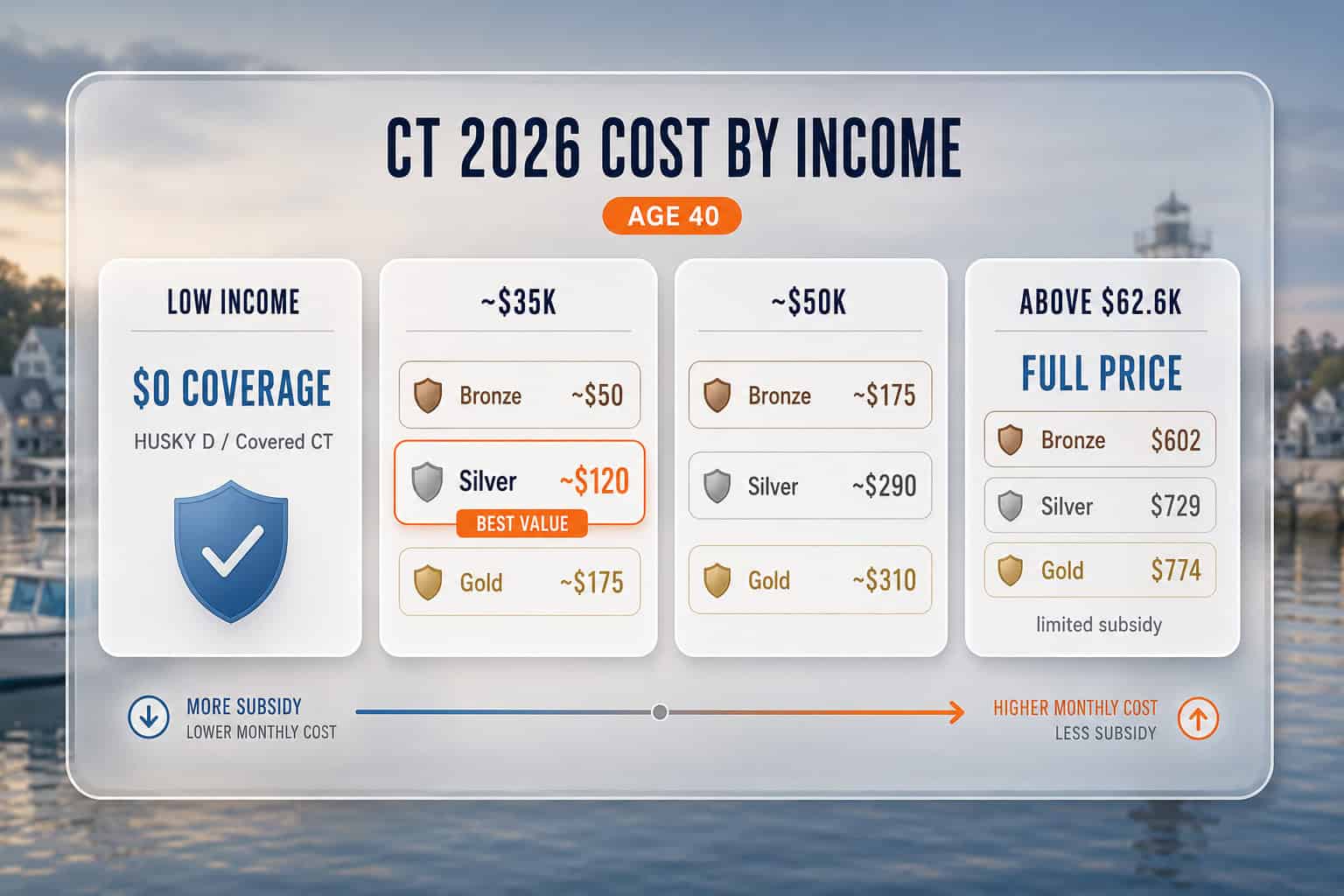

For a 40-year-old in Connecticut, 2026 marketplace premiums before subsidies average $602 per month for Anthem Bronze HMO, $729 for Anthem Silver PPO, and $774 for Anthem Gold. The average after-subsidy cost for subsidy-eligible enrollees is approximately $310 per month — up from $182 in 2025 due to the expiration of enhanced federal credits. Buyers in the lower income bands pay far less, and Covered Connecticut enrollees at 138–175 percent FPL pay nothing at all.

| Annual Income (Single, Age 40) | % FPL | Bronze After Subsidy | Silver After Subsidy | Gold After Subsidy |

|---|---|---|---|---|

| Under $22,025 | <138% | HUSKY D — $0 Medicaid | ||

| $22,025–$26,575 | 138–175% | Covered CT — $0 premium + $0 cost-sharing on Silver | ||

| ~$35,000 | ~219% | ~$50/mo | ~$120/mo (CSR87 — ~$900 deductible) | ~$175/mo |

| ~$50,000 | ~313% | ~$175/mo | ~$290/mo | ~$310/mo |

| Above $62,600 | >400% | $602/mo (full sticker) | $729/mo (full sticker) | $774/mo (full sticker) |

These figures draw from KFF’s Health Insurance Marketplace Calculator and 2026 Access Health CT plan data, which show the step-by-step math behind APTC eligibility. Actual premiums vary by zip code, exact plan selection, and ConnectiCare vs Anthem pricing. The key takeaway: for anyone with household income below 400 percent FPL, the after-subsidy cost of affordable health insurance in Connecticut is dramatically lower than the sticker price. Connecticut small employers looking to offer affordable health insurance in Connecticut to their workforce should review the Connecticut small business guide for group plan and ICHRA options.

Silver vs Gold vs Bronze — Which Tier Is Right in Connecticut

Connecticut does not use a Silver loading rule like some states impose, so plan tier selection follows standard logic. For buyers earning between 100 and 250 percent of the federal poverty level, Silver is almost always the best choice because cost-sharing reductions (CSR) are only available on Silver plans and dramatically lower deductibles and out-of-pocket costs. For buyers above 250 percent FPL, comparing Bronze and Gold on total annual cost — premium plus expected care — is the right approach.

| CSR Silver Tier | Income Range | Plan Pays | Typical Deductible | Verdict |

|---|---|---|---|---|

| Silver CSR 94 | 138–150% FPL ($22,025–$23,940) | 94% | ~$0–$300 | Nearly Platinum coverage — always pick Silver |

| Silver CSR 87 | 150–200% FPL ($23,940–$31,920) | 87% | ~$600–$1,200 | Silver beats Bronze and Gold |

| Silver CSR 73 | 200–250% FPL ($31,920–$39,900) | 73% | ~$2,500–$3,500 | Silver usually beats Gold; compare both |

| Standard Silver | Above 250% FPL | 70% | ~$4,800 | Compare total cost vs Gold; Gold’s $2,000 deductible may win |

Why Silver CSR is a genuine value in Connecticut: Some states standardize a Silver loading surcharge that makes Silver artificially expensive and pushes buyers toward Bronze and Gold. Connecticut has no such rule. Silver plan premiums in Connecticut are priced normally — CSR Silver is a genuine value for buyers under 250 percent FPL, just as it was designed to be. The Silver-avoid strategy used in loading-rule states does not apply in Connecticut.

Scenario — Hartford resident, age 35, $32,000 income (~200% FPL): Standard Silver (no CSR) sticker: ~$720/mo. After APTC: ~$95/mo. Silver CSR 87 deductible: ~$900. Gold sticker: ~$750/mo. After APTC: ~$125/mo. Gold deductible: ~$2,000. Silver CSR wins — $30/mo less in premium AND $1,100 less in deductible exposure. A resident using their coverage even twice a year will pay less total on Silver CSR 87 than Gold.

Covered Connecticut — The $0 Coverage Option

Covered Connecticut is the state’s most powerful affordability tool. For adults ages 19–64 earning between 138 and 175 percent of the federal poverty level who are not eligible for HUSKY Medicaid, Covered CT combines federal tax credits and state funding to eliminate both the monthly premium and all cost-sharing on a Silver plan. It covers medical, dental, and non-emergency transportation at zero cost. Over 51,629 Connecticut residents enrolled for 2026 — a record, up nearly 10,500 from 2025.

| Covered CT Detail | 2026 Value |

|---|---|

| Monthly premium | $0 |

| Deductible | $0 |

| Copays / coinsurance | $0 |

| Dental coverage | Included |

| Non-emergency transportation | Included |

| Plan tier required | Silver (must select Silver through AHCT) |

| Income limit (single adult) | Up to 175% FPL (~$27,388 in 2026) |

| How to enroll | AccessHealthCT.com or call 1-855-805-4325 |

| 2026 enrollees | 51,629 (record) |

Covered CT is the one situation where a Silver plan is mandatory rather than advisory — enrollees must select Silver to activate the state payment. Choosing Bronze or Gold forfeits the $0 cost-sharing benefit even if income qualifies. Enrollees must also accept 100 percent of the federal premium tax credit available to them before the state steps in to cover the rest. Applications go through AccessHealthCT.com or the Connecticut Department of Social Services.

See Your Real After-Subsidy Cost in Connecticut

ForHealthInsurance.com checks eligibility for Covered CT, Temporary Premium Assistance, and standard federal APTC — then shows after-subsidy pricing across Anthem and ConnectiCare plans in one comparison. Licensed brokers, no extra cost.

Get a Quote Call 888-215-4045Affordable Health Insurance in Connecticut Above 400% FPL

Connecticut residents earning above 400 percent of the federal poverty level — about $62,600 for a single adult in 2026 — receive no federal premium tax credit. The enhanced credits expired December 31, 2025. Connecticut’s Temporary Premium Assistance provides a partial offset for 400–500 percent FPL households, but buyers above 500 percent FPL ($78,250 single) face full sticker prices of $729 per month or more. Off-marketplace PPO plans are often better value at this income level.

Fairfield County and the Stamford corridor: With a median household income of $83,771 statewide and significantly higher figures in Fairfield County, a substantial portion of Connecticut households fall above the 500 percent FPL ceiling. A two-income household in Greenwich or Westport earning $120,000 combined pays full sticker price for marketplace plans — typically $1,400–$2,000 per month for two adults on Silver. Off-marketplace PPO plans from Anthem often provide comparable or better coverage at a lower monthly cost without the HMO network restrictions of on-exchange products.

| Income (Single Adult) | Approx. FPL | Anthem Silver Monthly (Full Sticker) | Better Option |

|---|---|---|---|

| $65,000 | ~407% | $729/mo + partial state assist | Call AHCT for state assistance |

| $80,000 | ~501% | $729/mo — no subsidy | Off-marketplace PPO — compare |

| $100,000 | ~626% | $729/mo — no subsidy | Off-marketplace PPO almost always better |

| $150,000+ | >939% | $729–$1,548/mo (age 60) | Off-marketplace PPO or employer plan |

For self-employed Connecticut residents in the Stamford tech and finance corridor, the combination of an off-marketplace PPO with an HSA and the 100 percent self-employed premium deduction often produces a lower effective cost than sticker-priced marketplace HMOs. See private Connecticut health insurance for the full off-marketplace analysis, or use the carrier comparison guide to run Anthem’s on-exchange vs off-exchange side by side.

How to Lower Your Health Insurance Cost in Connecticut

Several strategies reliably reduce what Connecticut residents pay for health insurance in 2026. The most impactful depend on income level — different tactics apply at different points on the subsidy ladder.

| Strategy | Works Best For | Potential Saving |

|---|---|---|

| Apply for Covered CT (if 138–175% FPL) | Low-income adults not on Medicaid | $600–$900/mo in premium + all cost-sharing |

| Choose Silver CSR (if 138–250% FPL) | All subsidy-eligible buyers in CSR range | $2,000–$8,000/yr in out-of-pocket costs |

| Call AHCT for Temporary Assistance (if 100–200% or 400–500% FPL) | Buyers who missed the online gap | Hundreds/mo at 100–200% FPL |

| Compare Anthem vs ConnectiCare by zip code | Hartford and New Haven metro buyers | $50–$150/mo depending on area |

| Switch to off-marketplace PPO | Above 500% FPL buyers | Often $100–$300/mo vs on-exchange sticker |

| HSA-eligible Bronze + self-employed deduction | Self-employed above subsidy threshold | $1,500–$3,000/yr in tax savings |

Frequently Asked Questions About Affordable Connecticut Coverage

How much does health insurance cost per month in Connecticut?

Connecticut health insurance averages $859 per month for a 40-year-old on a Silver plan before subsidies in 2026. After premium tax credits, the average subsidy-eligible enrollee through Access Health CT pays approximately $310 per month — up from $182 in 2025. Anthem Bronze HMO plans start around $602 per month before subsidies. Residents qualifying for Covered Connecticut receive full coverage at $0 per month with no deductible or copays.

What is the cheapest health insurance plan in Connecticut for 2026?

The cheapest Access Health CT plans are Anthem Bronze HMO options starting around $602 per month for a 40-year-old before subsidies. After premium tax credits, many subsidy-eligible buyers can access Bronze plans for well under $100 per month. Residents eligible for Covered Connecticut receive $0 premium Silver coverage with no deductibles or copays — the most comprehensive low-cost option for households at 138–175 percent of the federal poverty level.

Should I choose Bronze, Silver, or Gold in Connecticut for 2026?

For Connecticut buyers earning between 100 and 250 percent of the federal poverty level, Silver is almost always the right choice because cost-sharing reductions are only available on Silver plans and dramatically lower deductibles and out-of-pocket costs. For buyers above 250 percent FPL with subsidies, Bronze or Gold may beat Silver depending on health usage. Connecticut has no Silver loading rule — standard plan selection logic applies, unlike in states with loading surcharges.

What programs help make Connecticut health insurance more affordable?

Connecticut has four layers of financial assistance for 2026: HUSKY Health Medicaid covers adults under 138 percent FPL at no cost; Covered Connecticut provides $0-premium, $0-cost-sharing Silver coverage for 138–175 percent FPL; federal premium tax credits reduce monthly premiums for 100–400 percent FPL households; and the 2026 Temporary Premium Assistance from $70 million in state funds offsets expired federal credits for 100–200 percent and 400–500 percent FPL households.

What happens to Connecticut health insurance costs above 400% FPL?

Connecticut residents above 400 percent of the federal poverty level — about $62,600 for a single adult in 2026 — receive no federal premium tax credit. Connecticut’s Temporary Premium Assistance provides partial help for 400–500 percent FPL households, but buyers above 500 percent ($78,250 single) face full sticker prices of $729 per month or more for a Silver plan. Off-marketplace PPO plans are often the better value at this income level, particularly for the Fairfield County and Stamford corridor population.

Related Connecticut Health Insurance Resources

Explore the rest of the Connecticut guide — the statewide overview, small business coverage, carrier comparisons, the Access Health CT marketplace, and private off-exchange options.

The complete guide to health insurance options across Connecticut for 2026.

Connecticut Small BusinessGroup plans, the SHOP tax credit, and ICHRA for Connecticut employers.

Best Health Insurance in ConnecticutAnthem, ConnectiCare, and Cigna compared on price and provider network.

Connecticut MarketplaceEnrollment windows, deadlines, and subsidies on the Access Health CT marketplace.

CT Private & Off-ExchangeOff-exchange and private plan options for Connecticut residents wanting flexibility.

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required.

Find Affordable Health Insurance in Connecticut for 2026

ForHealthInsurance.com checks all four layers of Connecticut financial assistance, shows real after-subsidy pricing across Anthem and ConnectiCare, and completes Access Health CT enrollment at no extra cost.

Get a Quote Call 888-215-4045Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Connecticut residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.