Affordable Health Insurance in DC: A Complete 2026 Guide to Cheaper Coverage

Affordable health insurance DC residents can access in 2026 depends almost entirely on income. Three coverage paths cover most District residents who need lower-cost options: free or near-free DC Medicaid for those under 215% of the Federal Poverty Level, the new no-premium Healthy DC Plan introduced for 2026, and federally subsidized marketplace plans on DC Health Link for everyone in between. This guide to affordable health insurance DC explains how each path works in 2026, what changed in this year’s rate review, and which DC residents qualify for each option.

What does affordable mean for your DC household?

I want a quote for cheap DC plans

Compare lowest-premium options from CareFirst and Kaiser

Get a quote →The 2026 DC Rate Review and What It Means for You

DC residents pay less for 2026 health insurance than they would have without state regulatory intervention. The DC Department of Insurance, Securities and Banking (DISB) approved an average 8.7% increase for individual plans and 9.5% for small group plans after cutting what CareFirst BlueCross BlueShield and Kaiser Permanente originally requested. The agency estimated the rate reduction saves DC residents more than $1.2 million in 2026 compared to the proposed rates.

Affordable health insurance DC shoppers can trace 2026 prices directly to a specific regulatory decision. CareFirst originally requested a 4.1% increase on individual HMO plans and a 12.6% increase on individual PPO plans. Kaiser Permanente requested 12.9% across the board. DISB held a public hearing on September 11, 2025 — actuaries presented their cases, DC residents shared concerns about premium increases on their household budgets, and consumer advocates challenged the underlying claims data. The final approved rates, announced September 29, 2025, were lower than what the carriers filed. The full rate filings remain available through DISB’s rate filings portal.

The drivers behind the 2026 increases were the same three factors named in DISB’s published findings: higher base-period claims experience in the combined risk pool, medical inflation in the DC metro area, and a lower projected risk adjustment receivable. None of those drivers are unique to DC — every state saw similar pressures for 2026 — but DC’s all-marketplace structure and active rate review process produced a measurably better outcome for residents than what carriers initially requested.

What this means in dollars: A DC resident on a CareFirst BlueChoice PPO Silver plan saves roughly $25 to $45 per month in 2026 thanks to the DISB rate review, depending on the specific plan and pricing region. Across a full year, that’s $300 to $540 per individual enrollee.

Free and Low-Cost Coverage Paths in DC

Affordable health insurance DC residents qualify for runs through three pathways in 2026: DC Medicaid (administered by the DC Department of Health Care Finance) for adults up to 215% of the Federal Poverty Level, the new Healthy DC Plan for qualifying residents with no monthly premium and no cost at care, and DC Healthy Families (CHIP) for children up to 324% of FPL. All three programs route through DC Health Link or District Direct, the consolidated DC benefits portal.

DC Medicaid is the deepest no-cost coverage option for adults in the District. The program covers adults earning up to 215% of FPL — about $32,400 for a single adult in 2026, or $66,400 for a family of four — one of the highest income thresholds for Medicaid expansion in the country. Three managed care organizations deliver Medicaid services: AmeriHealth Caritas DC, CareFirst Community Health Plan DC, and MedStar Family Choice. Members choose one MCO when they enroll, and routine care happens through that MCO’s provider network at no cost to the member.

The Healthy DC Plan, new for the 2026 plan year, fills a coverage gap between DC Medicaid and subsidized marketplace plans. Per the DC Health Link homepage, the Healthy DC Plan provides quality coverage with no monthly payments and no costs when DC residents receive care. Eligibility is income-based and limited to DC residents who meet specific criteria — DC Health Link routes applicants to the program automatically during the application process. The plan targets working DC residents whose income exceeds the Medicaid threshold but who still cannot reasonably afford full marketplace premiums even with federal subsidies.

DC Medicaid

FreeCost: $0 monthly premium, $0 most care

Eligibility: Up to 215% FPL ($32,400 single adult)

Carriers: AmeriHealth Caritas DC, CareFirst Community Health Plan DC, MedStar Family Choice

Enrollment: Year-round through District Direct or DC Health Link

Healthy DC Plan

New 2026Cost: $0 monthly premium, $0 at point of care

Eligibility: Income-based, limited to qualifying DC residents

Through: DC Health Link platform

Enrollment: During annual open enrollment or qualifying SEP

DC Healthy Families (CHIP)

KidsCost: $0 monthly premium for most enrollees

Eligibility: Children up to age 21 in households below 324% FPL

Through: Same three Medicaid MCOs

Enrollment: Year-round through District Direct

Subsidized DC Health Link Plan

Tax creditCost: Reduced monthly premium after federal tax credit

Eligibility: Income above Medicaid threshold, below subsidy cliff

Carriers: CareFirst BlueCross BlueShield, Kaiser Permanente

Enrollment: Open enrollment Nov 1 to Jan 31, or qualifying SEP

Federal Premium Subsidies on DC Health Link

Federal premium tax credits (APTC) and cost-sharing reductions (CSR) work the same on DC Health Link as on HealthCare.gov. The subsidy is calculated against the second-lowest-cost Silver plan on DC Health Link, scaled so that benchmark Silver coverage costs a defined percentage of household income. About 28% of DC individual enrollees receive subsidies — well below the 93% national marketplace average — because the District’s median household income is one of the highest in the country.

The subsidy uptake gap is the most important fact for understanding affordable health insurance DC dynamics. DC Health Link enrollment is concentrated in households earning above the standard subsidy ranges — federal workers, lobbyists, consultants, nonprofit professionals, and freelancers in DC’s policy and creative economies. Many DC enrollees pay full unsubsidized premium. Self-employed residents and contractors buying their own coverage can see how the unsubsidized math works in our guide to individual health insurance in DC. The 28% of enrollees who do qualify for APTC receive credits averaging meaningful monthly reductions, and the cost-sharing reduction layer further cuts out-of-pocket exposure for Silver plan enrollees between 100% and 250% of FPL. Subsidy patterns on DC Health Link are documented in the KFF State Exchange Profile for the District of Columbia.

Subsidy reconciliation happens at tax time. DC Health Link enrollees who received an advance premium tax credit during the year must file IRS Form 8962 to reconcile the advance credit against their actual annual income. If household income ended up lower than reported at enrollment, the enrollee receives the difference as a refund. If income ended up higher, a portion of the advance credit may need to be repaid. The reconciliation rules are identical to those used for HealthCare.gov subsidy enrollees in other states.

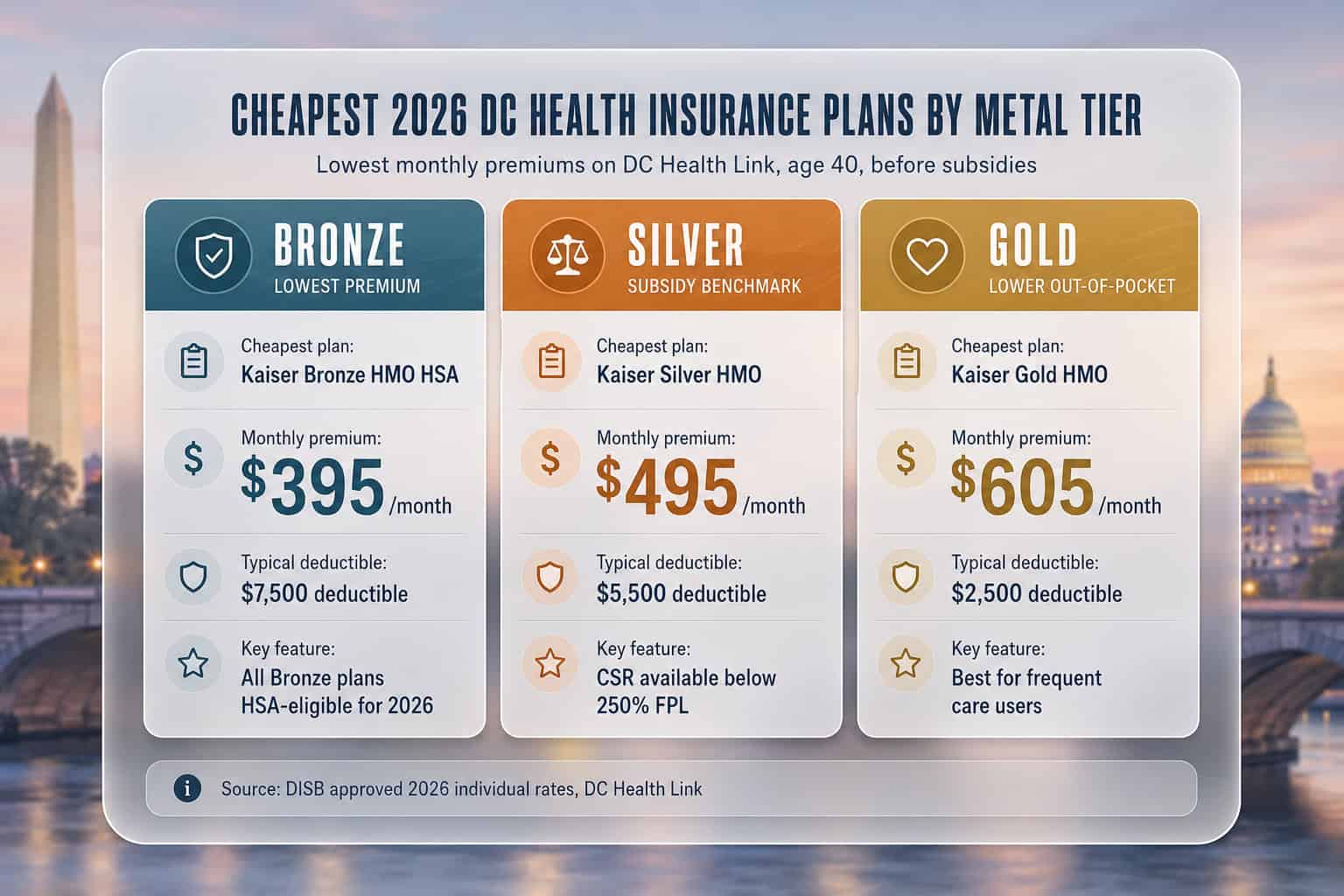

The Cheapest 2026 DC Plans by Metal Tier

Kaiser Permanente Bronze HMO plans deliver the most affordable health insurance DC residents can buy on the individual market for 2026, starting around $395 per month for a 40-year-old before subsidies. CareFirst BlueChoice HSA Bronze plans run slightly higher at around $410 to $440. New for 2026, every Bronze plan on DC Health Link is HSA-eligible, opening tax-advantaged savings at the lowest premium tier. Catastrophic plans for under-30 enrollees can be even cheaper but cover only essential health benefits.

The Bronze tier delivers the lowest monthly premium but the highest deductible — typically $7,000 to $8,500 in DC for 2026. Bronze plans suit DC residents who expect minimal care during the year and want financial protection against major medical events. The 2026 HSA-eligibility expansion means Bronze enrollees can pair their plan with a Health Savings Account, contributing pre-tax dollars (up to the annual federal limit) for use on medical expenses. HSA funds roll over year to year and can be invested for long-term growth.

| Plan | Carrier | Premium (Age 40) | Deductible | Best For |

|---|---|---|---|---|

| Kaiser Bronze HMO HSA | Kaiser Permanente | ~$395/month | ~$7,500 | Lowest premium + tax-advantaged savings |

| CareFirst BlueChoice HSA Bronze | CareFirst BCBS | ~$410–$440/month | ~$7,000 | HSA savings with CareFirst HMO network |

| Kaiser Silver HMO | Kaiser Permanente | ~$495/month | ~$5,500 | Subsidy benchmark, balanced cost-share |

| CareFirst BlueChoice Silver HMO | CareFirst BCBS | ~$510–$570/month | ~$5,000 | Lower deductible than Bronze, broader DC-area network |

| Catastrophic HMO (under 30) | CareFirst BCBS | ~$320–$360/month | ~$10,000 | Under-30 enrollees, hardship exemptions only |

Find Affordable 2026 DC Coverage With Help

A licensed DC agent checks DC Medicaid, Healthy DC, and subsidy eligibility, then compares cheapest plans. No cost to you.

How Income Determines Your DC Coverage Path

The path to affordable health insurance DC residents take follows household income relative to the Federal Poverty Level. Under 215% FPL routes most adults to DC Medicaid. Income above the Medicaid threshold but within Healthy DC eligibility routes to the no-cost Healthy DC Plan. Above that, federal premium tax credits subsidize DC Health Link marketplace plans up to roughly 400% FPL, after which most DC residents pay full unsubsidized premium. Each pathway has different enrollment timing and documentation requirements.

| Annual Income (Single Adult) | % of FPL | Primary Coverage Path |

|---|---|---|

| Under $32,400 | Under 215% | DC Medicaid (free) |

| $32,400 – ~$45,000 | 215% – ~300% | Healthy DC Plan (free) or subsidized DC Health Link |

| $45,000 – $60,240 | ~300% – 400% | Heavily subsidized DC Health Link plan |

| $60,240 – $90,000 | 400% – 600% | Partial subsidy (under extended ARPA rules if renewed) or full price |

| Over $90,000 | Over 600% | Full-price DC Health Link plan (no subsidy) |

The transition between paths is where most DC affordability decisions get made. A DC resident earning $35,000 falls into the Healthy DC eligibility zone for 2026 and would compare a no-cost Healthy DC Plan against a heavily subsidized Bronze or Silver marketplace plan. A resident earning $55,000 sits in the subsidized marketplace zone, with subsidy size depending on benchmark Silver pricing in their household composition. Above $90,000, most DC residents pay full unsubsidized premium and choose between Bronze for low premium or Gold/Platinum for lower out-of-pocket exposure.

Real-World Affordability Scenarios for DC Residents

DC affordability decisions look different across household types. A single bartender in Adams Morgan earning $28,000 qualifies for DC Medicaid. A teacher in Petworth earning $58,000 qualifies for federal subsidies on DC Health Link. A nonprofit professional in Capitol Hill earning $85,000 receives smaller subsidies but still pays meaningfully less than sticker price. A federal contractor in Brookland earning $135,000 pays full unsubsidized premium. The scenarios below illustrate how affordable health insurance DC paths shake out across real District households.

Maria, 32, server in Adams Morgan, earning $28,000 (about 185% FPL):

Maria falls below the 215% FPL DC Medicaid threshold. She qualifies for full DC Medicaid coverage at $0 monthly premium with $0 cost at care. She enrolls through District Direct, selects one of the three DC Medicaid MCOs (AmeriHealth Caritas DC, CareFirst Community Health Plan DC, or MedStar Family Choice), and is covered year-round. No DC Health Link plan would be cheaper.

James, 41, teacher in Petworth, earning $58,000 (about 390% FPL):

James is above the Medicaid threshold and above Healthy DC eligibility, but within federal subsidy range. The benchmark Silver plan on DC Health Link costs roughly $550/month at his age before subsidy. After APTC, his expected contribution drops to approximately $410/month. James can apply that credit to any tier — he might choose a Kaiser Bronze HMO HSA at ~$395 sticker (so ~$255 after subsidy) to maximize savings, or a Kaiser Silver HMO at ~$495 sticker (so ~$355 after subsidy) for lower deductible exposure.

Aisha and Marcus, both 38, nonprofit professionals in Capitol Hill, household $115,000 (about 580% FPL for family of 2):

This household sits in the partial-subsidy zone under the extended ARPA subsidy rules (if Congress renews them for 2026). Without renewal, they pay full unsubsidized premium. A CareFirst BlueChoice PPO Silver family plan costs roughly $1,250/month. With Bronze HSA Kaiser coverage at roughly $830/month for the family, premiums drop by about $420/month — at the cost of a higher deductible and Kaiser-only network.

David, 52, federal contractor in Brookland, earning $135,000 (about 900% FPL):

David earns above all subsidy thresholds and pays full unsubsidized premium. At age 52, his premiums run roughly 1.6x age-40 rates. A CareFirst BlueChoice PPO Silver costs about $970/month; a Kaiser Bronze HMO HSA runs about $635/month. David might prioritize the CareFirst PPO for the BCBS national network (he travels for work) or the Kaiser Bronze HSA for cost savings paired with HSA tax advantages.

FAQ About Affordable Health Insurance in DC

DC residents asking about affordable health insurance DC options want clear answers to the same six questions: what’s the cheapest plan, is there free coverage, how much did rates change, do DC residents get subsidies, what is Healthy DC, and what income qualifies for Medicaid. The answers below cover the practical decision points for every DC household considering 2026 coverage on DC Health Link.

What is the cheapest health insurance in DC for 2026?

The cheapest 2026 individual plans on DC Health Link are Kaiser Permanente Bronze HMO and CareFirst BlueChoice HSA Bronze, with monthly premiums starting around $395 to $440 for a 40-year-old before subsidies. After federal premium tax credits, qualifying DC residents can pay significantly less — and some may qualify for the new no-cost Healthy DC Plan.

Is there free health insurance in DC?

Yes. DC Medicaid is free for adults earning up to 215% of the Federal Poverty Level. New for 2026, the Healthy DC Plan offers no-premium, no-cost-at-care coverage for qualifying DC residents. Children up to age 21 in households below 324% of FPL qualify for DC Healthy Families (CHIP).

How much did DC health insurance go up in 2026?

DISB approved an average 8.7% increase for individual plans and 9.5% for small group plans for 2026, after reducing what CareFirst and Kaiser originally requested. The rate review saved DC residents an estimated $1.2 million compared to the proposed rates.

Do DC residents get federal health insurance subsidies?

Yes. DC Health Link applies the same federal premium tax credit and cost-sharing reduction rules as HealthCare.gov. About 28% of DC individual enrollees receive subsidies, compared to 93% nationally — reflecting the District’s higher median household income.

What is the Healthy DC Plan?

Healthy DC is a no-cost health coverage program launched for the 2026 plan year through DC Health Link. Qualified DC residents pay no monthly premium and no cost-sharing at the point of care. Eligibility is income-based and limited to specific DC residency criteria.

What income limits qualify for DC Medicaid?

DC Medicaid covers adults up to 215% of the Federal Poverty Level — one of the most generous expansion thresholds in the country. For a single adult in 2026, that’s roughly $32,400 annually. Children qualify for DC Healthy Families (CHIP) up to 324% of FPL, and pregnant residents have expanded eligibility.

DC Health Insurance Resources

Explore the rest of the DC guide — the statewide overview, the DC Health Link marketplace, carrier comparisons, and nationwide PPO coverage.

The complete guide to health insurance options across the District for 2026.

DC Health Insurance MarketplaceEnrollment windows, deadlines, and subsidies on DC Health Link.

Best Health Insurance in DCCareFirst and Kaiser compared on price and provider network.

PPO Health Insurance PlansNationwide PPO coverage — flexible provider access, no referrals required.

Compare Affordable 2026 DC Plans

A licensed DC agent compares Medicaid, Healthy DC, and subsidized DC Health Link plans across CareFirst and Kaiser. No cost to you.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving District of Columbia residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.