Affordable Health Insurance in Georgia: 2026 Guide

Affordable health insurance in Georgia is within reach for most residents, but the path to low-cost coverage depends heavily on income. Georgians earning between $15,060 and $60,240 per year qualify for premium tax credits that can cut monthly costs by hundreds of dollars. Those earning below $15,060 may qualify for Georgia Pathways Medicaid with a work requirement. Georgia’s 12.9% uninsured rate, the highest in the Southeast, suggests that many residents either don’t know what they qualify for or haven’t enrolled in available programs.

This guide breaks down the real cost of health insurance in Georgia for 2026, who qualifies for subsidies, the cheapest plan options by carrier, and practical strategies for lowering premiums.

What brings you here today?

See plans in my price range

Get a free quote with subsidy estimates for your Georgia ZIP code

Get a quote →Do I qualify for help paying?

Check APTC subsidy eligibility by income level for 2026

Check eligibility ↓Compare costs by plan type

Bronze, Silver, Gold premiums and deductibles side by side

See cost table ↓Ways to lower my premium

Strategies to reduce your Georgia health insurance costs in 2026

See strategies ↓How to Find Affordable Health Insurance in Georgia

The most effective way to find affordable health insurance in Georgia is to apply through the Georgia Access marketplace, where premium tax credits reduce monthly costs for households earning $15,060 to $60,240 per year. In 2026, a 40-year-old earning $35,000 in Atlanta could find a Silver plan for approximately $100–$150 per month after subsidies. Ambetter by Peach State Health Management offers the lowest base premiums statewide, with Bronze plans starting around $220 per month before subsidies.

How Much Does Health Insurance Cost in Georgia?

Before subsidies, a Georgia resident purchasing an individual marketplace plan in 2026 can expect to pay approximately $220–$310 per month for Bronze, $340–$490 for Silver, and $480–$580 for Gold, based on a 40-year-old non-tobacco user. Premiums vary by county; Atlanta metro plans tend to price slightly higher than rural Georgia plans from the same carrier. After subsidies, most income-qualifying enrollees pay significantly less.

Bronze Plan

~$220–$310/mo age 40, before subsidies

Lowest premium tier. Deductible: $6,000–$8,000. Best for healthy Georgians with low expected healthcare use. HSA-eligible plans available.

Silver Plan

~$340–$490/mo age 40, before subsidies

Most popular tier. Deductible: $3,000–$5,000. Best for subsidy-eligible enrollees; cost-sharing reductions only apply at Silver tier.

Gold Plan

~$480–$580/mo age 40, before subsidies

Higher premium, lower cost-sharing. Deductible: $500–$2,000. Best for Georgians with predictable high healthcare use.

Catastrophic Plan

~$150–$210/mo age 40, before subsidies

Lowest available premium. Deductible: $9,100 (2026 max). Available to Georgians under 30 or with hardship exemption. Not eligible for premium tax credits.

These ranges reflect 2026 Georgia marketplace benchmark data. According to CMS marketplace enrollment reports, the majority of Georgia marketplace enrollees received premium tax credits in 2026, reducing actual costs well below these sticker prices. Age significantly affects premiums; a 60-year-old pays roughly three times the premium of a 21-year-old for the same plan.

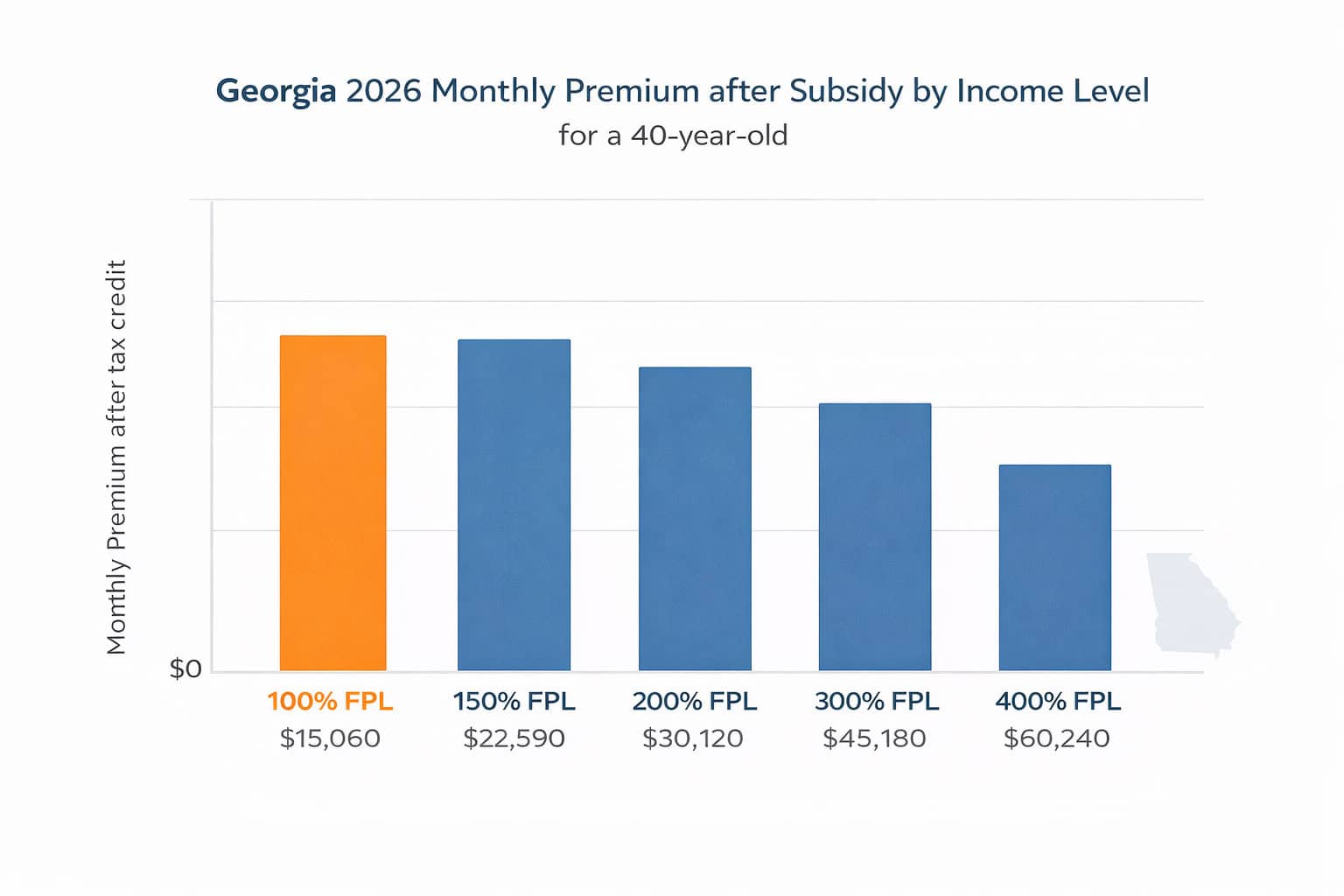

Georgia Subsidies: Who Qualifies and How Much

Premium tax credits in Georgia are available to households earning between 100% and 400% of the federal poverty level ($15,060 to $60,240 for a single adult in 2026) under standard 2026 ACA rules for some enrollees. The subsidy caps premiums at a percentage of household income, meaning many lower-income Georgians qualify for $0 or near-$0 monthly plans. Approximately 960,000 Georgians enrolled through the marketplace in 2026; the vast majority received subsidies.

| Annual Income (Single Adult) | % of FPL | Estimated Monthly Premium After Subsidy (Silver, Age 40) | Subsidy Tier |

|---|---|---|---|

| $15,060 or below | 100% FPL | $0/mo (benchmark Silver) | Maximum subsidy; full premium covered |

| $18,000–$22,590 | 120–150% FPL | ~$0–$30/mo | Very high subsidy; near-zero cost plans |

| $22,590–$30,120 | 150–200% FPL | ~$30–$80/mo | High subsidy; strong cost-sharing reductions at Silver |

| $30,120–$45,180 | 200–300% FPL | ~$80–$175/mo | Moderate subsidy; Silver plans most cost-effective |

| $45,180–$60,240 | 300–400% FPL | ~$175–$320/mo | Standard subsidy; reduces but does not eliminate premium |

| Above $60,240 | 400%+ FPL | Full premium (no subsidy at standard threshold) | Standard 2026 ACA credits up to 400% FPL; verify eligibility at enrollment |

Subsidy amounts are calculated at enrollment through HealthCare.gov and applied directly to monthly premiums. Georgia residents who receive more subsidy than they’re entitled to based on actual income must repay the difference at tax time. The Georgia Office of Insurance provides a Georgia-specific estimate before enrolling.

Example: How Subsidies Work for a Bibb County Resident

A 45-year-old non-tobacco user in Bibb County (Macon) earning $32,000 per year sits at approximately 212% of the federal poverty level. Without a subsidy, a mid-range Ambetter Silver EPO plan might cost approximately $390 per month. After premium tax credits, the same plan could cost approximately $95–$115 per month, a reduction of roughly $275–$295 per month. Choosing a Silver plan also makes this enrollee eligible for cost-sharing reductions, which reduce the plan’s deductible from around $4,500 to as low as $700, depending on the specific Silver variant selected.

See What Affordable Coverage Costs at Your Income

Get a personalized subsidy estimate and compare every plan available in your Georgia county. In 2026, a single adult at 150% FPL in Georgia could find a Silver plan for approximately $0–$30 per month after tax credits.

Free and Low-Cost Options: Medicaid and Georgia Pathways

Georgians earning below $15,060 per year (100% FPL for a single adult) may qualify for free or near-free coverage through traditional Georgia Medicaid or Georgia Pathways to Coverage. Traditional Medicaid is primarily available to children, pregnant women, and adults with qualifying disabilities. Georgia Pathways extends coverage to working-age adults meeting an 80-hour-per-month activity requirement; approximately 25,000 Georgians were enrolled as of 2025.

Traditional Georgia Medicaid

Cost: Free for most enrollees

Who qualifies: Children, pregnant women, elderly, and disabled adults. Most working-age adults without dependents do not qualify.

Apply: Georgia Gateway (gateway.ga.gov) or call the Division of Family and Children Services.

Georgia Pathways to Coverage

Cost: Low premiums (~$1–$8/mo depending on income)

Who qualifies: Adults 19–64 earning up to 100% FPL ($15,060/year) meeting 80 hrs/month work, education, or community service.

Note: ~25,000 enrolled as of 2025, far below the 200K–300K in the coverage gap.

Children’s Health Insurance (PeachCare)

Cost: Free to low-cost

Who qualifies: Georgia children up to age 19 in families earning too much for Medicaid but unable to afford private coverage.

Apply: Georgia Gateway portal; no enrollment period, apply any time.

ACA Marketplace (Subsidized)

Cost: $0–$320+/mo depending on income

Who qualifies: Georgians earning 100%–400% FPL ($15,060–$60,240) under standard 2026 ACA rules.

Enroll: Through Georgia Access (HealthCare.gov or licensed agent) during open enrollment or SEP.

Cheapest Health Insurance Plans in Georgia by Carrier

Ambetter by Peach State Health Management consistently offers the lowest base premiums in Georgia’s 2026 marketplace; the only carrier available in all 159 counties, including rural areas where no other carrier competes. Kaiser Permanente offers competitive pricing in Atlanta metro, where its HMO model produces lower premiums through integrated care. For off-exchange buyers without subsidies, BCBS Georgia’s Bronze PPO may be competitive for residents who prioritize national network access over premium savings.

| Carrier | Lowest Bronze (Age 40, pre-subsidy) | Lowest Silver (Age 40, pre-subsidy) | Coverage Area | Plan Type |

|---|---|---|---|---|

| Ambetter (Peach State) | ~$220–$255/mo | ~$340–$380/mo | All 159 counties | EPO |

| Kaiser Permanente | ~$195–$235/mo | ~$320–$360/mo | Atlanta metro only | HMO |

| Oscar Health | ~$240–$275/mo | ~$370–$420/mo | Atlanta metro + select markets | EPO |

| Cigna | ~$255–$295/mo | ~$410–$460/mo | Select counties | PPO |

For most subsidy-eligible Georgians seeking affordable health insurance in Georgia, Ambetter’s lower base premiums translate to the lowest after-subsidy cost regardless of location. In rural counties where Ambetter is the only carrier, Ambetter is effectively the marketplace there. In Atlanta metro counties where Kaiser also competes, the difference between Ambetter and Kaiser often comes down to provider preference rather than cost.

Strategies to Lower Your Premium in Georgia

Several strategies can reduce the cost of health insurance for Georgia residents in 2026. The most impactful is choosing a Silver plan if subsidy-eligible. Silver’s cost-sharing reductions can cut deductibles from $4,500 to as low as $700 for lower-income enrollees, making Silver a far better value than Bronze at the same income level. Choosing an EPO over a PPO, enrolling before the deadline, and accurately reporting income all affect final cost.

Choose Silver If Subsidy-Eligible

Cost-sharing reductions (CSRs) only apply to Silver tier plans. For Georgians earning 100%–250% FPL, a Silver plan with CSRs can dramatically reduce deductibles and copays, turning a $4,500 deductible plan into one with a $700–$2,500 deductible at little or no additional premium cost compared to Bronze.

Use an HSA-Eligible Bronze Plan

High-deductible Bronze plans that qualify for a Health Savings Account allow Georgia residents to contribute pre-tax dollars for medical expenses: $4,150 for individuals and $8,300 for families in 2026. HSA contributions effectively reduce the true cost of a Bronze plan for enrollees who rarely use care.

Verify Your Income Estimate at Enrollment

Overestimating income at enrollment results in a smaller subsidy and higher monthly premiums. Underestimating results in a repayment at tax time. Reporting the most accurate income estimate, especially important for self-employed and gig workers with variable Georgia earnings, to maximize subsidy accuracy throughout the year.

Consider EPO Over PPO for Cost Savings

PPO plans from Cigna cost approximately $80–$120 more per month than comparable EPO plans from Ambetter in the same county. For Georgians who see in-network providers only, an EPO delivers the same network access at a lower premium. PPO plans are worth the premium only for Georgians who regularly need out-of-network access.

Catastrophic Plans for Under-30 Georgians

Georgia residents under 30 can purchase a catastrophic plan, the lowest-premium tier, starting around $150–$210 per month before subsidies. These plans cover three primary care visits per year before the deductible and provide protection against worst-case costs, but are not subsidy-eligible and carry a $9,100 deductible in 2026.

Enroll Through a Licensed Agent at No Cost

Enrolling through a licensed Georgia agent or EDE partner like ForHealthInsurance.com costs nothing extra; agent commissions are paid by carriers, not enrollees. Agents can compare all Georgia marketplace plans side by side, identify CSR Silver opportunities, and flag eligibility for Georgia Pathways or PeachCare for household members.

Frequently Asked Questions About Affordable Health Insurance in Georgia

How can I get affordable health insurance in Georgia?

The most direct route to affordable health insurance in Georgia is the Georgia Access marketplace, where premium tax credits reduce monthly costs for households earning $15,060 to $60,240 per year. Applying through HealthCare.gov or a licensed enhanced direct enrollment partner gives access to all available carriers and subsidy estimates. Georgians earning below $15,060 may qualify for Georgia Pathways to Coverage, a limited Medicaid expansion with an 80-hour-per-month work requirement, or traditional Georgia Medicaid if they meet categorical eligibility criteria such as pregnancy or disability.

What is the cheapest health insurance in Georgia?

The cheapest marketplace health insurance in Georgia for 2026 comes from Ambetter by Peach State Health Management, which offers Bronze EPO plans starting around $220 per month before subsidies for a 40-year-old. Kaiser Permanente’s Bronze HMO starts around $195 per month in Atlanta metro counties where it’s available. Catastrophic plans, available to Georgians under 30 or those with hardship exemptions, start around $150 per month but carry a $9,100 deductible and are not eligible for premium tax credits. After subsidies, many lower-income Georgians qualify for $0 or near-$0 monthly plans.

What is the income limit for free health insurance in Georgia?

Georgia does not offer free health insurance to most working-age adults through Medicaid. Traditional Georgia Medicaid is primarily limited to children, pregnant women, and adults with qualifying disabilities. Georgia Pathways to Coverage extends coverage to adults earning up to 100% of the federal poverty level ($15,060 for a single adult in 2026) who meet an 80-hour-per-month work or activity requirement, at very low or no premium. Through the marketplace, Georgians earning at 100% FPL can qualify for $0 monthly Silver plans through premium tax credits. Georgia has not adopted full Medicaid expansion, which would provide near-free coverage to adults earning up to 138% FPL.

Do I qualify for a subsidy on Georgia health insurance?

Most Georgia residents purchasing individual marketplace plans qualify for some level of subsidy. Premium tax credits are available to households earning between 100% and 400% of the federal poverty level ($15,060 to $60,240 for a single adult in 2026) under standard 2026 ACA rules. To qualify, residents must enroll through the Georgia Access marketplace (not off-exchange), must not have access to affordable employer-sponsored coverage, and must not be eligible for Medicaid or Medicare. Self-employed Georgians use projected net self-employment income to determine subsidy eligibility.

Is it worth paying for health insurance in Georgia if I’m healthy?

Going without health insurance in Georgia carries no penalty; there is no state mandate and the federal penalty was reduced to $0 in 2019. However, one unexpected hospitalization or emergency can produce medical bills of $20,000 to $100,000 or more without insurance. Georgia’s uninsured rate of 12.9% is among the highest in the Southeast, partly reflecting residents who underestimate this risk. For Georgians who qualify for subsidies, particularly those earning under 200% FPL where Bronze plans may cost under $50 per month after tax credits, the financial protection typically outweighs the premium cost even for healthy individuals.

More Georgia Health Insurance Resources

Complete 2026 overview of carriers, exchange, and enrollment for all Georgians.

Georgia Marketplace GuideGeorgia Access enrollment, open enrollment dates, and subsidy eligibility

Individual Health Insurance in GeorgiaCoverage for self-employed, gig workers, and those between jobs

Best Health Insurance Companies in GeorgiaAmbetter, Oscar, Kaiser, Cigna, and BCBS Georgia compared for 2026.

Georgia PPO Health InsuranceWhen a PPO is worth the extra cost, and when it isn’t

Short-Term Health Insurance in GeorgiaBridge coverage for Georgians between plans; up to 364-day terms allowed.

Small Business Health Insurance in GeorgiaGroup plans and tax credits for Georgia employers.

Compare PPO Health Insurance PlansBrowse PPO options nationwide; no referrals required.

Find Affordable Georgia Coverage for 2026

Get a free quote with subsidy estimates applied to your income, showing every plan available at your Georgia ZIP code, including $0 premium options for qualifying enrollees.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Georgia residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.