Georgia Health Insurance: 2026 Guide to Plans, Costs & Coverage

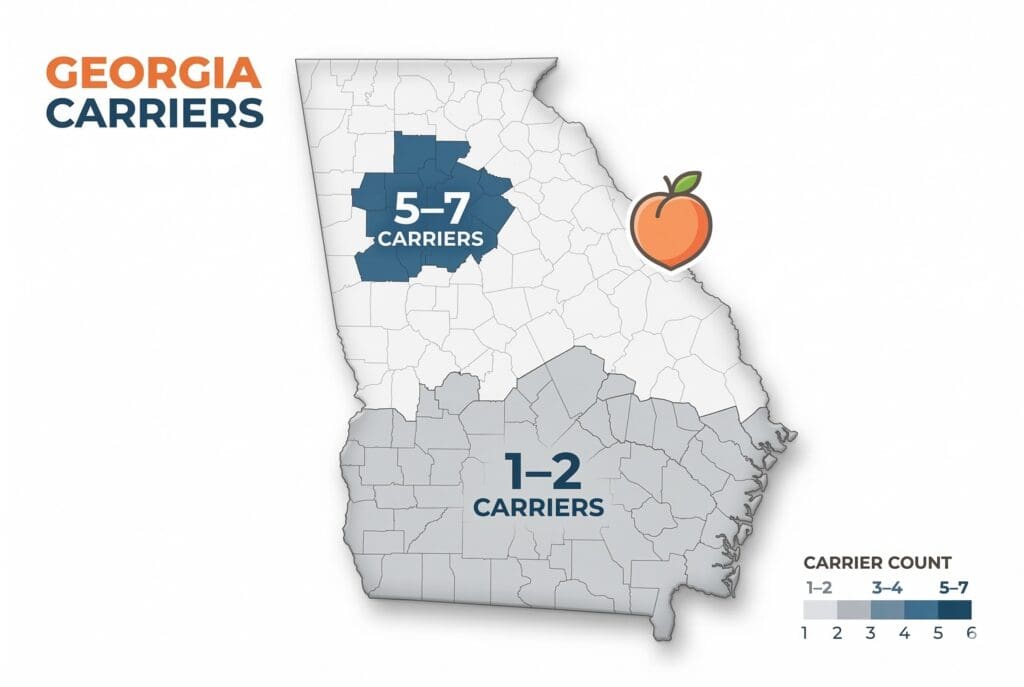

Georgia has one of the most distinctive health insurance markets in the country — shaped by partial Medicaid expansion, the Georgia Access waiver allowing direct enrollment outside HealthCare.gov, and a carrier landscape that ranges from 6–7 options in Atlanta to just one in rural South Georgia. With roughly 12.9% of residents uninsured — the highest rate in the Southeast — choosing the right plan matters. This guide covers plans, carriers, costs ($340–$600+/month before subsidies), Georgia Access enrollment, Pathways Medicaid, and what to do if you miss open enrollment.

What brings you here today?

I want to compare carriers

See who offers plans in Georgia — Ambetter, Aetna, Kaiser, and more

Compare carriers ↓I lost my coverage

Learn about Special Enrollment Periods and gap coverage options

See enrollment options ↓How Health Insurance Works in Georgia in 2026

Georgia residents who don’t have job-based or government coverage purchase health insurance through the individual market. The state uses the federal exchange at HealthCare.gov but added a layer called Georgia Access — a 1332 state innovation waiver — that lets licensed brokers and insurers enroll consumers directly, bypassing the federal portal. Most plans run January 1 through December 31.

Georgia uses the federal ACA marketplace — with Bronze plans starting around $340–$380/month for a 40-year-old before subsidies, and premium tax credits available up to 400% FPL (~$60,240/year for a single adult in 2026). The Georgia Access 1332 waiver lets licensed brokers complete full ACA enrollments entirely outside HealthCare.gov — subsidy calculation, plan selection, and effectuation — a pathway unavailable in most other federally facilitated exchange states. Coverage includes essential health benefits: doctor visits, preventive care, emergency services, prescriptions, maternity, and mental health. There is no state individual mandate and no federal penalty for going uninsured.

Georgia’s Exchange: HealthCare.gov and Georgia Access

Georgia uses HealthCare.gov for ACA plan enrollment, with Georgia health insurance shoppers able to enroll through the federal portal or directly via a licensed broker. Under the Georgia Access 1332 waiver, residents can also enroll through a licensed broker or carrier’s Enhanced Direct Enrollment portal — skipping the federal site entirely. Both pathways access the same subsidy-eligible plans. Open enrollment runs November 1 through January 15 each year.

Through Georgia Access, licensed brokers complete full ACA enrollments outside HealthCare.gov — quoting plans, calculating subsidies, and effectuating coverage without the applicant logging into the federal portal. Both pathways access identical plans at identical subsidy-adjusted prices. The difference is convenience: in Clinch County, where 1–2 carriers participate, a Georgia Access broker surfaces options faster and without the HealthCare.gov account setup that deters first-time enrollees.

HealthCare.gov enrollment

The standard federal pathway. Create a HealthCare.gov account, enter your Georgia household income and ZIP code, compare plans from carriers active in your county (up to 6 in metro Atlanta), and enroll.

Georgia Access (Direct Enrollment)

Work with a licensed Georgia broker or enroll through a carrier’s EDE portal. Same subsidies, same plans — but the process stays off HealthCare.gov. Useful for those who want guided assistance.

Open enrollment runs November 1 through January 15 — January 1 coverage for enrollments by December 15, February 1 for December 16–January 15. Georgia’s 2025 marketplace enrollment reached a record 1.3 million. Outside open enrollment, a qualifying life event triggers a Special Enrollment Period. To enroll through Georgia Access, call 888-215-4045 — a licensed Georgia broker can complete the full enrollment without HealthCare.gov.

Health Insurance Plans Available in Georgia

Georgia residents can choose from four plan types — HMO, EPO, PPO, and POS — across four metal tiers (Bronze, Silver, Gold, and Platinum). Ambetter by Peach State Health Management dominates the exchange with EPO and HMO options statewide, while Aetna and Cigna offer PPO plans in select counties. Plan availability varies significantly by ZIP code.

Plan Types in Georgia

HMO — Health Maintenance Organization

- Requires a primary care physician

- Referrals needed for specialists

- Lower premiums; limited to in-network care

- Common carrier: Ambetter, Kaiser (Atlanta only)

EPO — Exclusive Provider Organization

- No referrals needed for specialists

- Must stay in-network for coverage

- Mid-range premiums; no out-of-network benefit

- Common carrier: Ambetter, Oscar Health

PPO — Preferred Provider Organization

- See any provider, in or out of network

- No referrals required for specialists

- Higher premiums; maximum flexibility

- Common carrier: Aetna, Cigna, BCBS GA

Ambetter is the sole carrier in 30+ rural Georgia counties. Aetna and Cigna are the only on-exchange PPO carriers — BCBS Georgia PPO operates off-exchange. PPO premiums run $80–$120/month more than comparable Ambetter EPO plans. See Georgia PPO health insurance for details.

Metal Tiers in Georgia

Metal tiers reflect cost-sharing, not care quality. Georgia 2026 deductibles: Bronze $7,500–$8,700; Silver $3,500–$5,000 (before CSR); Gold $1,000–$2,500.

| Metal Tier | Plan Pays | You Pay | Best For |

|---|---|---|---|

| Bronze | ~60% | ~40% | Healthy adults who rarely need care; HSA-eligible options available |

| Silver | ~70% | ~30% | Most Georgians; only tier eligible for Cost-Sharing Reductions (CSR) |

| Gold | ~80% | ~20% | Frequent care users; predictable costs are worth higher premium |

| Platinum | ~90% | ~10% | Limited availability in Georgia; highest premium, lowest out-of-pocket |

Silver is the only tier eligible for Cost-Sharing Reductions (CSR) — available to Georgians earning 100–250% FPL. A CSR Silver plan can cut deductibles from $4,000+ to under $1,000, often outperforming Bronze even at a higher premium. See the affordable health insurance Georgia guide for income-by-income recommendations.

Health Insurance Carriers in Georgia

The Georgia health insurance market is led by Ambetter by Peach State Health Management, which offers plans in every county. Aetna, Oscar Health, BCBS Georgia, Cigna, and Kaiser Permanente (Atlanta metro only) round out the field. Carrier availability varies sharply by county — Atlanta-area residents may have six or seven choices, while rural South Georgia counties may have only Ambetter.

Ambetter by Peach State Health Management

- Centene subsidiary; Georgia-specific brand

- EPO and HMO plan types only; no PPO

- Available statewide — only carrier in many rural counties

- Lowest premiums on exchange in most regions

- Large network in Georgia metro areas

Aetna

- PPO plans available in Atlanta metro and select counties

- Primary on-exchange PPO carrier in Georgia

- Strong statewide provider network

- Mid-to-upper premium range for PPO flexibility

Oscar Health

- EPO plans; Atlanta metro focused

- Tech-forward member experience; concierge team model

- Moderate premium range; virtual-first care options

- Not available in rural Georgia counties

BCBS Georgia (Anthem)

- PPO plans primarily off-exchange

- BlueCard network provides national and out-of-state access

- Strong statewide brand and provider relationships

- Best option for Georgians who travel frequently

Cigna

- PPO plans in select Georgia markets

- Broad national network; strong out-of-state coverage

- On-exchange availability in metro counties

Kaiser Permanente

- Atlanta metro area only; HMO integrated care model

- Insurance and medical care under one roof

- High member satisfaction; no PPO option

- Not available outside Kaiser’s Georgia service area

For NCQA ratings, 2026 county-level availability, and a full plan type grid, see the best health insurance in Georgia guide.

Find the Right Georgia Health Insurance Plan

Compare plans from Ambetter, Aetna, Oscar, and more — a licensed Georgia broker can walk you through your options at no extra cost.

How Much Does Health Insurance Cost in Georgia?

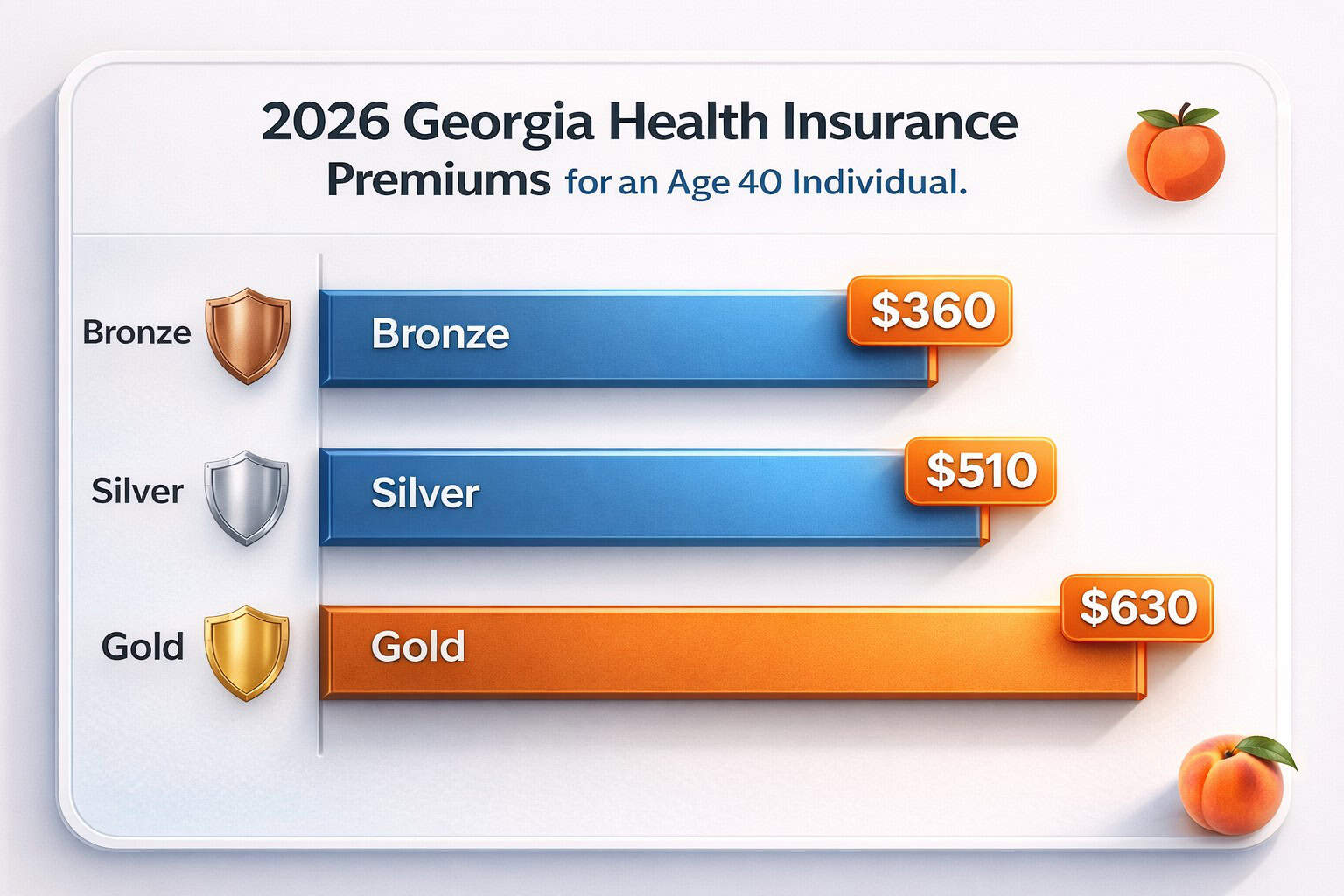

A 40-year-old shopping for Georgia health insurance pays roughly $340–$380 per month for a Bronze plan before subsidies in 2026, and $480–$540/month for Silver. Georgians earning between 100% and 400% of the Federal Poverty Level qualify for premium tax credits. ARP-enhanced subsidies expired at the end of 2025 — subsidies are smaller in 2026, and the 400% FPL cliff has returned.

2026 Georgia Benchmark Premiums (Pre-Subsidy)

Bronze

$340–$380/mo

Individual, age 40. Highest deductibles ($7,500–$8,700). Best for healthy Georgians who want low premiums and rarely need care.

Silver

$480–$540/mo

Individual, age 40. Only tier eligible for Cost-Sharing Reductions. Best value for Georgians earning 100–250% FPL.

Gold

$600–$660/mo

Individual, age 40. Lower deductibles ($1,000–$2,500). Better for frequent care or predictable medical needs.

Family (Silver)

$1,200–$1,400/mo

2 adults + 2 children, ages 35–38, pre-subsidy. Subsidy eligibility can reduce this significantly for qualifying households.

Premiums vary by age, county, and plan type. A 60-year-old pays two to three times more than a 30-year-old for the same plan. Smokers face a 50% surcharge in some plans.

Subsidies and the Premium Tax Credit

The Advance Premium Tax Credit (APTC) reduces monthly premiums based on household income and your county’s benchmark Silver plan cost (~$510/month in Atlanta metro). Note: ARP-enhanced subsidies expired December 31, 2025 — subsidies are smaller in 2026 and capped at 400% FPL. 2026 income thresholds for a single adult:

| Income Level | Annual Income (Single Adult) | Subsidy Eligibility |

|---|---|---|

| 100–138% FPL | ~$15,060–$20,782/year | APTC eligible; may qualify for low-premium Silver plan |

| 138–250% FPL | ~$20,782–$37,650/year | APTC + Cost-Sharing Reductions on Silver |

| 250–400% FPL | ~$37,650–$60,240/year | APTC only; no Cost-Sharing Reductions |

| 250–400% FPL | ~$37,650–$60,240/year | APTC only; no Cost-Sharing Reductions |

| Above 400% FPL | Above ~$60,240/year | No subsidy; cliff returned in 2026 after ARP enhancements expired |

Georgia enrollees averaged ~$430/month in federal premium tax credits in 2025. With ARP enhancements now expired, 2026 subsidy amounts are lower — and Georgians above 400% FPL (~$60,240/year) no longer qualify for any credit. Call 888-215-4045 to get a Georgia-specific subsidy estimate, or see the affordable health insurance Georgia guide for county-level CSR recommendations.

Georgia Medicaid and the Pathways Program

Georgia has not fully expanded Medicaid under the ACA. Instead, the state launched Georgia Pathways to Coverage in July 2023, a partial expansion requiring adults ages 19–64 to complete 80 hours per month of qualifying work, education, or community service. As of early 2026, roughly 25,000 adults are enrolled, leaving an estimated 200,000–300,000 Georgians in a coverage gap with no subsidized option.

Who Qualifies for Pathways

- Adults ages 19–64 not otherwise Medicaid-eligible

- Income at or below 100% FPL (~$15,060/year for a single adult)

- 80 hours/month of qualifying work or activity

- Georgia resident and U.S. citizen or qualifying immigrant

Qualifying Activities

- Paid employment or self-employment

- Job training or vocational programs

- Enrollment in an educational program

- Community service or volunteer work

- Caregiving for a child or dependent

| Income Level | Annual Income (Single Adult) | Coverage Option |

|---|---|---|

| Below 100% FPL | Under ~$15,060/year | Georgia Pathways (if meeting work requirement) — otherwise coverage gap |

| 100–138% FPL | ~$15,060–$20,782/year | ACA marketplace with APTC subsidies; may qualify for low-premium Silver |

| 138–250% FPL | ~$20,782–$37,650/year | ACA marketplace with APTC + Cost-Sharing Reductions on Silver |

| 250–400% FPL | ~$37,650–$60,240/year | APTC only; no Cost-Sharing Reductions |

| Above 400% FPL | Above ~$60,240/year | No subsidy; full premium cost (subsidy cliff returned in 2026) |

The Georgia Coverage Gap: Georgians earning below 100% FPL who don’t meet Pathways work requirements and don’t qualify for traditional Medicaid have no subsidized coverage option. An estimated 200,000–300,000 residents are affected. Forty other states closed this gap through full Medicaid expansion; Georgia has not. See Medicaid.gov Georgia Pathways for official eligibility rules, or the individual health insurance Georgia guide for low-income coverage options.

Open Enrollment Dates and Special Enrollment in Georgia

Georgia health insurance open enrollment runs November 1 through January 15 — January 1 coverage for enrollments by December 15, February 1 for December 16–January 15. Outside open enrollment, a qualifying life event triggers a 60-day Special Enrollment Period completable through the Georgia Access pathway without HealthCare.gov.

| Enrollment Window | Coverage Start Date |

|---|---|

| November 1 – December 15 | January 1 |

| December 16 – January 15 | February 1 |

Special Enrollment Periods in Georgia

A qualifying life event opens a 60-day SEP. COBRA averages $600–$800/month; Georgia Access ACA Silver may cost $0–$200/month after credits. Common triggers:

- Loss of employer-sponsored coverage

- Marriage, divorce, birth, or adoption

- Move to a new county or ZIP code in Georgia

- Loss of Medicaid or CHIP eligibility

SEP enrollments in Georgia can be completed through the Georgia Access pathway — no HealthCare.gov account required. A licensed broker can verify your qualifying event and effectuate coverage the same day. Call 888-215-4045 to start. Georgians without a qualifying event can consider short-term health insurance — Georgia permits plans up to 364 days at $80–$200/month, though without pre-existing condition, prescription, or maternity coverage.

Frequently Asked Questions About Georgia Health Insurance

Does Georgia have its own individual health insurance mandate?

No. Georgia has no state individual mandate, and the federal penalty was reduced to $0 in 2019. Georgians face no financial penalty for going uninsured, though they lose access to ACA protections and subsidy-eligible coverage outside of open enrollment.

What is the Georgia Pathways to Coverage program?

Georgia Pathways to Coverage is a partial Medicaid expansion (July 2023, CMS 1115 waiver) for adults 19–64 who complete 80 hours/month of qualifying work, education, or community service. As of early 2026, ~25,000 adults are enrolled. Those who don’t qualify and earn below 100% FPL may fall into the coverage gap.

Which carriers offer PPO plans in Georgia?

Aetna and Cigna offer PPO plans on the Georgia exchange in select counties. BCBS Georgia (Anthem) offers PPO plans primarily off-exchange. Ambetter, Oscar Health, and Kaiser Permanente do not offer PPO plans in Georgia — they are EPO or HMO only. PPO plan availability depends on your specific county; metro Atlanta residents generally have more PPO options than rural Georgians. See the Georgia PPO guide for a full carrier breakdown.

When does Georgia’s open enrollment period end?

Open enrollment ends January 15 (February 1 coverage) or December 15 (January 1 coverage). Georgia follows federal HealthCare.gov deadlines with no state extensions. Residents who miss it need a qualifying life event for a Special Enrollment Period, or can consider short-term coverage.

How do I know if I qualify for a subsidy in Georgia?

Georgians earning 100–400% FPL (~$15,060–$60,240/year for a single adult in 2026) qualify for Advance Premium Tax Credits. Note: ARP-enhanced subsidies expired at the end of 2025. In 2026, credits are smaller and the 400% FPL subsidy cliff has returned — Georgians above ~$60,240/year no longer qualify. Call 888-215-4045 for a current subsidy estimate.

What is Georgia Access and how is it different from HealthCare.gov?

Georgia Access is a state-approved 1332 waiver that allows licensed brokers and participating carriers to enroll Georgia residents in ACA marketplace plans through Enhanced Direct Enrollment portals — without using HealthCare.gov. Both pathways access the same subsidized plans and calculate the same tax credits. Georgia Access simply gives residents the option to work directly with a broker or carrier rather than navigating the federal website.

Georgia Health Insurance Guides

Georgia Access enrollment, open enrollment dates, and subsidy eligibility explained

Best Health Insurance Companies in GeorgiaCompare Ambetter, Aetna, Oscar, Kaiser, Cigna, and BCBS Georgia side by side

Individual Health Insurance in GeorgiaCoverage for self-employed Georgians, gig workers, and those between jobs

Affordable Health Insurance in GeorgiaSubsidy strategies, Medicaid options, and lowest-cost plans for 2026

Short-Term Health Insurance in GeorgiaGeorgia allows plans up to 364 days — what’s covered and when it makes sense

Small Business Health Insurance in GeorgiaGroup plans, SHOP marketplace, and ICHRA for Georgia employers

Georgia PPO Health InsuranceCompare Aetna and Cigna PPO plans — county availability and costs for 2026

Compare PPO Health Insurance PlansBrowse PPO options nationwide — flexible coverage with no referrals required

Ready to Compare Georgia Health Insurance Plans?

Get matched with plans available in your Georgia county — from Ambetter in rural South Georgia to Aetna, Kaiser, and Oscar in the Atlanta metro. A licensed broker compares your options and walks you through enrollment at no extra cost.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Georgia residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.