Individual Health Insurance in Hawaii 2026: Plans for Self-Employed and Independent Residents

The individual health insurance Hawaii market is smaller than in any other state. The Prepaid Health Care Act covers most employed residents through their employers, and Med-QUEST covers low-income residents through Medicaid. That leaves a focused group who need individual coverage: the self-employed, part-time workers below the PHCA 20-hour threshold, those between jobs, family members aging off employer plans, and residents whose employers do not offer PHCA-covered positions. This guide covers every individual health insurance option available in Hawaii for 2026. For a full overview, see the Hawaii health insurance guide.

What’s your situation?

I’m self-employed or freelance

PHCA doesn’t cover you; here are your individual market options

Learn more ↓I lost coverage or left my employer

COBRA vs. marketplace; 60-day SEP window explained

See options ↓See coverage options by income

Med-QUEST at $0 to off-exchange HMSA — income pathway guide

See pathways ↓Get a free island-specific quote

Compare 2026 HMSA and Kaiser individual plans by ZIP and income

Get a quote →Who Needs Individual Health Insurance in Hawaii?

Most Hawaii residents with jobs already have employer coverage through the PHCA. The individual market serves those outside that system: the self-employed, part-time workers under 20 hours per week, people between jobs or after a layoff, and dependents aging off a parent’s employer plan at 26. Hawaii’s unique employment landscape creates a distinct individual health insurance Hawaii population.

Self-Employed and Freelancers

Hawaii’s tourism, arts, and creative economy includes a large self-employed population. Freelancers in Honolulu, independent contractors on Maui, and sole proprietors statewide are all outside PHCA coverage and must purchase individual HMSA or Kaiser plans on or off exchange. Self-employed health insurance premiums are fully deductible as a business expense. See the Hawaii small business health insurance guide for employer plan options.

Part-Time Workers Under 20 Hours

Employees working fewer than 20 hours per week fall below the PHCA threshold and are not entitled to employer coverage under Hawaii law. Per the Hawaii Department of Labor (DLIR), the 20-hour threshold applies after four consecutive weeks of employment. Part-time workers in Hawaii’s hospitality sector are among the most common individual health insurance Hawaii enrollees.

Between Jobs or After Layoff

Hawaii’s tourism economy creates significant seasonal employment, particularly on Maui, Kauai, and Hawaii Island. A seasonal layoff or job loss triggers a Special Enrollment Period on HealthCare.gov, opening a 60-day window to enroll in individual health insurance in Hawaii. COBRA is also available but typically more expensive than subsidized marketplace plans for income-qualifying residents.

Aging Off a Parent’s Plan at 26

Dependents lose employer-sponsored coverage when they turn 26. This life event triggers a Special Enrollment Period, allowing 60 days to enroll in individual HMSA or Kaiser coverage through HealthCare.gov. At age 26, most residents qualify for subsidized marketplace plans depending on income. The Hawaii marketplace guide covers enrollment steps and subsidy eligibility.

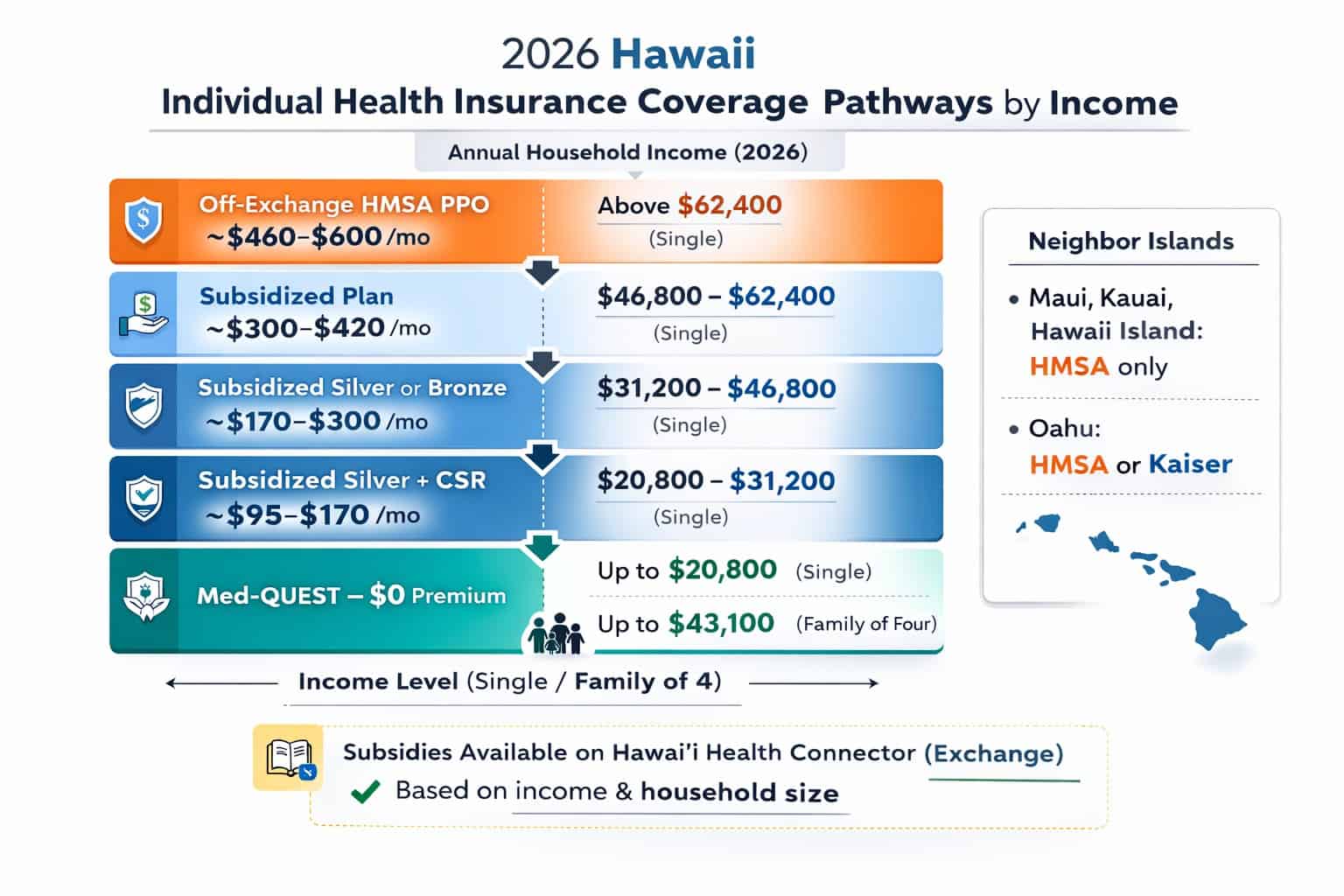

Individual Coverage Options in Hawaii for 2026

Three individual health insurance Hawaii pathways exist for 2026: Med-QUEST at $0 for incomes up to $20,800 (single), subsidized HMSA or Kaiser marketplace plans through HealthCare.gov for incomes 138% to 400% FPL, and off-exchange HMSA plans for residents above the subsidy cliff. On-exchange options vary by island; Oahu residents can choose HMSA or Kaiser, while neighbor island residents have access only to HMSA.

| Income Level (Single Adult, 2026) | Coverage Pathway | Estimated Monthly Cost | Carrier Options |

|---|---|---|---|

| Up to $20,800 (138% FPL) | Med-QUEST (Medicaid) | $0 | AlohaCare, Ohana Health Plan |

| $20,800 to $31,200 (138 to 200% FPL) | Subsidized Silver + CSR | ~$95 to $170/mo | HMSA; Kaiser (Oahu only) |

| $31,200 to $46,800 (200 to 300% FPL) | Subsidized Silver or Bronze | ~$170 to $300/mo | HMSA; Kaiser (Oahu only) |

| $46,800 to $62,400 (300 to 400% FPL) | Subsidized marketplace plan | ~$300 to $420/mo | HMSA; Kaiser (Oahu only) |

| Above $62,400 (400%+ FPL) | Off-exchange HMSA plans | ~$460 to $600/mo | HMSA PPO or HMO off-exchange |

Residents earning below $20,800 (single) should apply for Med-QUEST before purchasing any marketplace plan. Hawaii is a Medicaid expansion state; adults without children qualify based on income alone. For a full breakdown of subsidy amounts and cost-sharing reductions by income level, see the affordable health insurance guide for Hawaii.

Enrolling in Individual Health Insurance in Hawaii

Hawaii residents enroll in individual marketplace plans through HealthCare.gov during Open Enrollment (November 1 through January 15) or via a Special Enrollment Period triggered by a qualifying life event. Off-exchange HMSA plans can be purchased directly at any time with no enrollment period, but do not qualify for premium tax credits. Med-QUEST enrollment is open year-round.

Job Loss / Loss of Coverage

- Losing employer-sponsored coverage

- Employer stops offering PHCA coverage

- Hours reduced below PHCA 20-hour threshold

- COBRA expiration

Household Changes

- Marriage or divorce

- Birth or adoption of a child

- Dependent aging off plan at 26

- Death of a household member with coverage

Relocation

- Moving to Hawaii from the mainland

- Relocating between islands (changes carrier availability)

- Returning from abroad with Hawaii residency

Other Qualifying Events

- Gaining citizenship or lawful immigration status

- Release from incarceration

- Losing Medicaid or CHIP eligibility

- Marketplace error or administrative change

Island Relocation as a Qualifying Life Event

Moving between Hawaiian islands qualifies as a Special Enrollment Period trigger. Since carrier availability changes by island, a move from Oahu to Maui (losing Kaiser access) or from any neighbor island to Oahu (gaining Kaiser access) opens a 60-day enrollment window. Per HealthCare.gov’s Special Enrollment guidelines, permanent moves to a new ZIP code with different plan availability qualify as a SEP event.

Find Individual Health Insurance in Hawaii for 2026

Compare HMSA and Kaiser individual plans by island, check Med-QUEST eligibility at $20,800, and enroll during your Special Enrollment Period or Open Enrollment window.

No Short-Term Health Insurance in Hawaii: Alternatives Explained

Hawaii significantly restricts short-term limited duration health insurance (STLDI) plans. Unlike most mainland states, short-term plans are not a viable coverage gap option for individual health insurance Hawaii residents. Those needing temporary coverage between jobs should consider COBRA, a Special Enrollment Period on HealthCare.gov, or off-exchange HMSA plans purchased directly.

No Short-Term Health Plans in Hawaii

Hawaii law significantly restricts STLDI plans, making them effectively unavailable for most residents. Four alternatives for bridge coverage: (1) COBRA — continue employer coverage for up to 18 months; (2) Special Enrollment Period — enroll in HMSA or Kaiser within 60 days of a qualifying event; (3) off-exchange HMSA plan — purchase directly from HMSA any time; (4) Med-QUEST — if income is below $20,800 single, apply year-round at $0 premium. The IRS premium tax credit guidance covers deductibility rules for self-employed residents purchasing marketplace plans.

COBRA Continuation

Available for up to 18 months after losing employer coverage. Preserves the same plan and provider network, which is valuable for residents mid-treatment. COBRA premiums include the full premium (employer and employee share) plus a 2% admin fee, often $600 to $900/month for HMSA group plans. Compare against subsidized marketplace plans before electing COBRA.

Special Enrollment Period

Job loss triggers a 60-day SEP on HealthCare.gov. For income-qualifying Hawaii residents, marketplace plans with subsidies are typically far cheaper than COBRA. A Maui resident earning $35,000 after a seasonal layoff could enroll in a subsidized HMSA Silver plan for approximately $160 to $200/month vs. $700+ for COBRA continuation.

Off-Exchange HMSA

HMSA offers individual plans directly, outside HealthCare.gov, with no enrollment period restriction. Available year-round. No subsidy eligibility on off-exchange plans. Best for residents above the 400% FPL subsidy cliff ($62,400 single) who want HMSA PPO’s BlueCard national network for inter-island and mainland travel. See the Hawaii carrier comparison for plan details.

Med-QUEST (Medicaid)

For residents earning up to $20,800 (single) or $43,100 (family of four): $0 premium, year-round enrollment, no waiting period. Hawaii is a Medicaid expansion state. Managed through AlohaCare and Ohana Health Plan. Apply through the Hawaii Med-QUEST Division or HealthCare.gov. Coverage typically starts the first of the following month after approval.

Real Scenario: Oahu Resident, Age 29, Aging Off Parent’s Plan

A 29-year-old Oahu resident shopping for individual health insurance Hawaii options ages off their parent’s employer health plan. The birthday triggers a 60-day Special Enrollment Period on HealthCare.gov. Earning approximately $36,000 annually (about 232% FPL), this resident qualifies for premium tax credits and cost-sharing reductions on a Silver plan. On HealthCare.gov for Oahu ZIP codes, both HMSA and Kaiser plans appear. At 232% FPL, an HMSA Silver plan running $500/month at full price drops to approximately $165 to $195/month after premium tax credits. The CSR benefit also reduces the Silver deductible to well under $2,000. Given a freelance lifestyle with irregular travel between islands, the HMSA PPO’s BlueCard network may justify choosing HMSA over Kaiser’s lower-premium HMO option.

Frequently Asked Questions: Individual Health Insurance in Hawaii

The most common questions about individual health insurance in Hawaii involve the PHCA coverage gap, how to enroll after losing employer coverage, what plans are available by island, and whether short-term plans are an option.

Who needs individual health insurance in Hawaii?

Hawaii residents who need individual health insurance are those not covered by employer plans under the PHCA. This includes the self-employed and freelancers, part-time workers employed fewer than 20 hours per week, residents between jobs or after a seasonal layoff, dependents aging off a parent’s employer plan at 26, and residents whose employers do not offer PHCA-compliant coverage. Residents earning below $20,800 (single) should check Med-QUEST eligibility first; Medicaid covers eligible residents at $0 premium through AlohaCare and Ohana Health Plan.

What individual health insurance plans are available in Hawaii?

Hawaii’s individual health insurance market offers HMSA (Hawaii Medical Service Association) plans on all six major islands — both HMO and PPO options — and Kaiser Permanente Hawaii HMO plans on Oahu only. Both carriers offer Bronze, Silver, Gold, and Platinum tiers through HealthCare.gov. HMSA also offers off-exchange PPO plans directly for residents above the subsidy cliff. Neighbor island residents on Maui, Hawaii Island, Kauai, Molokai, and Lanai have access only to HMSA on the individual market.

Is short-term health insurance available in Hawaii?

No. Hawaii significantly restricts short-term limited duration health insurance (STLDI) plans; they are not a practical coverage option for Hawaii residents. Hawaii residents who need bridge coverage should use COBRA continuation (up to 18 months), enroll in HMSA or Kaiser through a Special Enrollment Period, purchase an off-exchange HMSA plan directly, or apply for Med-QUEST if income qualifies below $20,800 single.

Can self-employed residents deduct health insurance in Hawaii?

Yes. Self-employed Hawaii residents — sole proprietors, freelancers, and independent contractors — can deduct 100% of health insurance premiums paid for themselves, their spouse, and dependents as an above-the-line federal income tax deduction. This applies to HMSA and Kaiser individual plan premiums purchased on or off exchange. The deduction reduces adjusted gross income, which can increase ACA premium tax credit eligibility since credits are income-based. A tax advisor can help structure this deduction given Hawaii’s state income tax rules.

How do I enroll in individual health insurance after losing my job in Hawaii?

Job loss is a qualifying life event that opens a 60-day Special Enrollment Period on HealthCare.gov. Hawaii residents have 60 days from the date of coverage loss to enroll in an HMSA or Kaiser marketplace plan. For Oahu residents, both carriers appear on HealthCare.gov; for neighbor island residents on Maui, Hawaii Island, Kauai, Molokai, or Lanai, only HMSA plans are available. A Maui resident earning $35,000 after a layoff could enroll in a subsidized HMSA Silver plan for approximately $160 to $200/month. COBRA is also available but typically costs significantly more than a subsidized marketplace plan.

Hawaii Health Insurance Guides

Complete 2026 guide: PHCA, Med-QUEST, HMSA, Kaiser, and all coverage pathways

Hawaii Health Insurance MarketplaceHealthCare.gov enrollment, subsidy eligibility, and 2026 open enrollment dates

Best Health Insurance in HawaiiHMSA PPO vs. Kaiser HMO: island-by-island carrier and premium comparison

Affordable Health Insurance in HawaiiMed-QUEST eligibility, subsidies, and lowest-cost plan options by island

Small Business Health Insurance in HawaiiPHCA employer obligations, group plans, and SHOP marketplace options

PPO Health Insurance PlansCompare PPO plans nationwide: BlueCard network, provider flexibility, no referrals

Get Individual Health Insurance in Hawaii for 2026

Self-employed, between jobs, or aging off a parent’s plan — compare individual health insurance Hawaii options for 2026 by island, income, and situation. HMSA PPO with BlueCard, Kaiser HMO on Oahu, and Med-QUEST at $0 all available.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Hawaii residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.