Affordable Health Insurance in Idaho: 2026 Costs, Savings & Subsidy Guide

Health insurance in Idaho costs less than most states — and there are several ways to bring the price down further. Whether you’re looking at marketplace plans through Your Health Idaho, checking if you qualify for financial help, or comparing costs across carriers and plan types, this guide breaks down what affordable health insurance in Idaho actually costs for 2026 and how to pay the least for the coverage you need.

What brings you here today?

Why Affordable Health Insurance in Idaho Costs Less Than Most States

Idaho’s individual health insurance premiums are among the lowest in the country. A state program called the Idaho reinsurance waiver reduces premiums by approximately 18% compared to what they would be without it. For a 40-year-old, that translates to roughly $70–$100 per month in savings — built into the premium before any subsidies are applied. The average Bronze plan in Idaho costs about $317/month, well below the national average above $400.

The program works by covering a portion of the most expensive medical claims in the state’s insurance pool. When a small number of people have very high medical costs, those costs normally get spread across every customer’s premium. Idaho’s reinsurance waiver steps in to absorb some of that expense so the full cost doesn’t land on every policyholder. The state and federal government share the funding, and the program is managed through the Idaho High Risk Reinsurance Pool.

Idaho’s version of this program is structured differently from the 16 other states with reinsurance-focused 1332 waivers. Where most states reimburse insurers for any claim above a dollar threshold, Idaho also identifies specific high-cost medical conditions and covers those directly — a hybrid approach used by only Idaho and Alaska. This approach was approved by HHS on August 16, 2022 and has delivered consistent savings: 12% in 2023, 16% in 2024, 20% in 2025, and 18% in 2026. The Idaho Department of Insurance October 2025 rate release confirmed that the 2026 average rate increase of 10% is less than half the national average — largely because of this program.

Program timeline

Idaho’s current 1332 reinsurance waiver runs through December 31, 2027. The state has submitted an extension and amendment application to continue the program through 2031. Finding affordable health insurance in Idaho is significantly easier because of this program — without it, premiums would be roughly $70–$100 higher per month for most enrollees.

How Much Does Health Insurance Cost in Idaho in 2026?

For a 40-year-old in Idaho, monthly premiums before subsidies range from $349 (cheapest Bronze, St. Luke’s Health Plan) to $658 (Platinum POS, Moda) depending on carrier and plan type. The average across all plans is approximately $535/month before financial assistance. About 87% of Your Health Idaho’s roughly 117,000 enrollees received tax credits in 2025 — averaging $407/month per KFF — but enhanced credits expired December 31, 2025, so after-subsidy costs rose sharply for 2026.

| Metal Tier | Premium Range (Age 40) | Avg. Deductible | Out-of-Pocket Max |

|---|---|---|---|

| Bronze | $349–$404/month | $7,000–$10,000 | $9,200–$10,000 |

| Silver | $481–$565/month | $3,000–$6,600 | $8,200–$9,900 |

| Gold | $532–$610/month | $895–$2,250 | $8,000–$8,700 |

| Platinum | ~$658/month (POS only) | ~$500 | ~$4,000 |

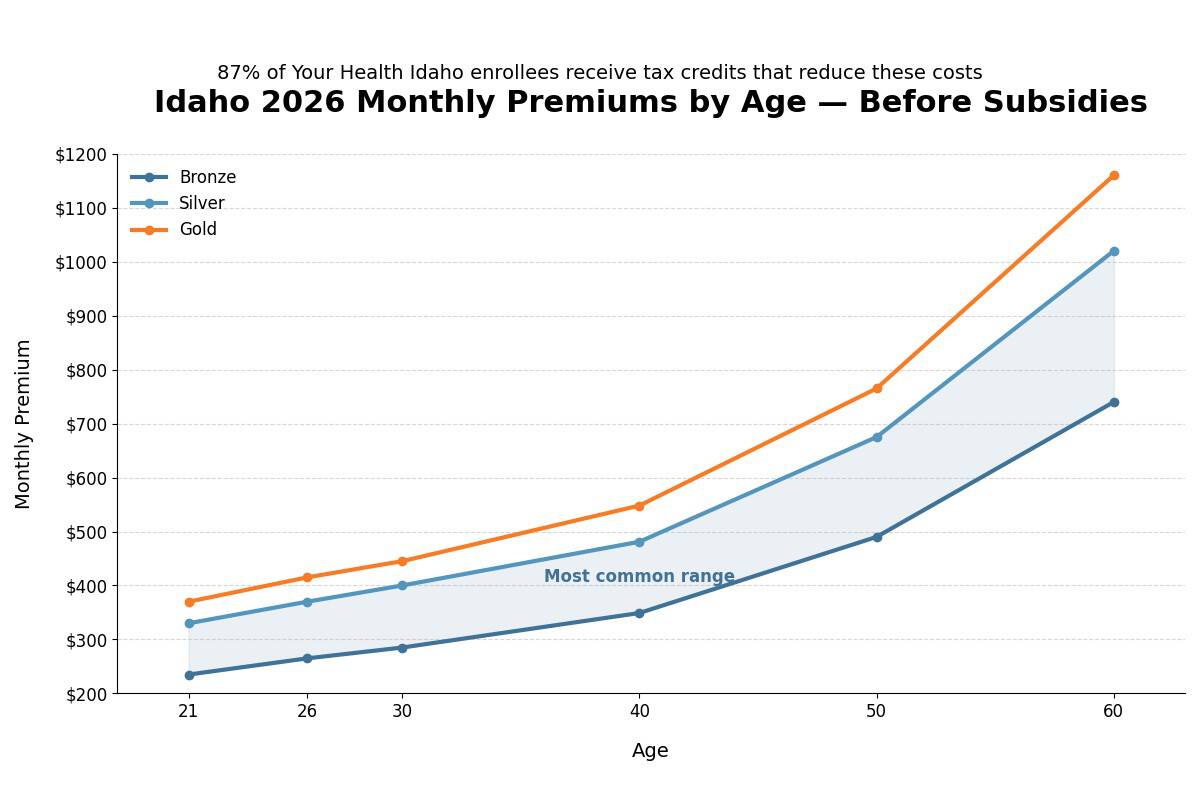

Premiums vary significantly by age. A 21-year-old pays roughly 60% of a 40-year-old’s rate, while a 60-year-old pays approximately 2.5 times more. Here’s how affordable health insurance in Idaho looks across age brackets at the Bronze and Silver tiers:

| Age | Cheapest Bronze | Avg. Silver | Avg. Gold |

|---|---|---|---|

| 21 | ~$235/month | ~$330/month | ~$370/month |

| 26 | ~$265/month | ~$370/month | ~$415/month |

| 30 | ~$285/month | ~$400/month | ~$445/month |

| 40 | ~$349/month | ~$481/month | ~$548/month |

| 50 | ~$490/month | ~$675/month | ~$765/month |

| 60 | ~$740/month | ~$1,020/month | ~$1,160/month |

The cheapest carrier in Idaho depends on the plan tier. St. Luke’s Health Plan offers the lowest Bronze premiums (~$349/month for age 40) but only serves Treasure Valley and Magic Valley counties. Blue Cross of Idaho offers the cheapest Silver plans starting at $412/month in some areas. Regence Blue Shield has the lowest POS premiums at $503/month. For the most affordable health insurance in Idaho across all carriers, checking Your Health Idaho with your specific zip code is the most accurate way to see what’s available and at what price.

Premium Tax Credits and Financial Help in Idaho for 2026

Premium tax credits through Your Health Idaho reduce monthly costs based on household income. For 2026, subsidies are available to households earning between 100% and 400% of the federal poverty level ($15,650–$62,600 for an individual using 2025 FPL). In 2025, 87% of Your Health Idaho’s roughly 117,000 enrollees received tax credits averaging $407/month per KFF. The enhanced subsidies in place since 2021 expired December 31, 2025 — meaning credits are smaller and fewer Idahoans qualify for 2026.

2026 Subsidy Change

The enhanced premium tax credits from the American Rescue Plan (2021) and Inflation Reduction Act expired December 31, 2025. Under the original ACA formula now in effect: subsidies are limited to 100%–400% FPL, households above 400% FPL ($62,600 for an individual using 2025 FPL) lost eligibility entirely, and remaining credits are calculated to keep the benchmark Silver plan at 2%–9.5% of household income rather than the enhanced cap of 8.5%. Your Health Idaho reported approximately 24,400 disenrollments in early 2026.

Below 138% FPL

Individual: under $22,025

Eligible for Idaho Medicaid — free or very low-cost coverage. Year-round enrollment through the Idaho Department of Health and Welfare at idalink.idaho.gov. Learn more about Idaho Medicaid eligibility →

138%–250% FPL

Individual: $22,025–$39,125

Eligible for premium tax credits AND cost-sharing reductions (CSRs) on Silver plans. CSRs lower deductibles, copays, and out-of-pocket maximums beyond what the premium subsidy provides. Silver plans with CSR are typically the best value at this income level.

250%–400% FPL

Individual: $39,125–$62,600

Eligible for premium tax credits but NOT cost-sharing reductions. The subsidy keeps the benchmark Silver plan between roughly 6%–8.5% of household income. Compare Bronze and Silver plans — Bronze may cost less monthly but Silver offers better coverage if you use regular care.

Above 400% FPL

Individual: above $62,600

No premium tax credit or CSR eligibility for 2026. On-exchange and off-exchange plans from the same carrier cost the same. Consider off-exchange PPO plans from Blue Cross of Idaho or Regence for broader network flexibility. Compare Idaho PPO and HMO costs →

Example: What Subsidies Look Like in Idaho

Jake, age 35, lives in Boise, earns $32,000/year (212% FPL): Before subsidies, a Silver plan costs approximately $440/month. His premium tax credit reduces that to roughly $175/month. Because his income is below 250% FPL, he also qualifies for cost-sharing reductions on a Silver plan — his deductible drops from $4,500 to approximately $1,800 and his out-of-pocket maximum from $9,000 to about $3,200. His total annual healthcare costs (premiums + likely out-of-pocket) are approximately $3,500 — compared to $10,800 without any financial assistance.

Cost-sharing reductions deserve special attention for anyone earning below 250% FPL in Idaho. In 2025, 47% of Your Health Idaho marketplace enrollees had CSR-eligible Silver plans. CSRs reduce the actual costs you pay when you visit a doctor, fill a prescription, or have a procedure — not just the monthly premium. They’re only available on Silver-tier plans purchased through the exchange, which is why Silver plans are often the best value even though Bronze plans have lower monthly premiums.

Check Your Idaho Subsidy Eligibility

See which affordable Idaho health insurance plans fit your budget — with your tax credit applied instantly. About 87% of Your Health Idaho’s 117,000 enrollees received tax credits in 2025.

Five Ways to Lower Your Idaho Health Insurance Costs

Beyond premium tax credits, Idaho residents have several practical strategies to reduce healthcare costs for 2026. These include choosing the right metal tier for your usage pattern, leveraging Silver CSR benefits, pairing Bronze plans with HSAs, shopping off-exchange for PPO plans above the subsidy threshold, and checking Idaho Medicaid eligibility before assuming marketplace prices apply. About 47% of Your Health Idaho Silver enrollees qualified for cost-sharing reductions in 2025.

Match Your Plan Tier to How You Use Healthcare

If you rarely see a doctor and want the lowest monthly payment, Bronze plans in Idaho start at $349/month for a 40-year-old. But if you have regular prescriptions, see specialists, or expect any medical procedures, a Silver or Gold plan may save money overall. A Gold plan at $548/month with a $1,000 deductible can cost less annually than a Bronze plan at $380/month with a $7,500 deductible — if you use more than a few doctor visits per year.

Get Silver CSR Benefits Below 250% FPL

If your household income falls between 138% and 250% of the federal poverty level ($22,025–$39,125 for an individual in Idaho), a Silver plan with cost-sharing reductions is almost always the smartest choice. The CSR version of a Silver plan has a lower deductible, lower copays, and a lower out-of-pocket maximum than the standard Silver — at the same premium. It’s effectively a Gold-quality plan at a Silver price, and it’s only available through Your Health Idaho.

Pair a Bronze HDHP with a Health Savings Account

For 2026, Bronze and Catastrophic plans through Your Health Idaho now qualify as high-deductible health plans (HDHPs). That means they can be paired with a Health Savings Account (HSA), which lets you save pre-tax dollars for medical expenses. In Idaho, contributions up to $4,300 (individual) or $8,550 (family) are tax-deductible for 2026. This strategy works best for healthy individuals who want the lowest premium and a tax-advantaged way to cover the high deductible. Self-employed Idahoans can also deduct the premium itself from taxable income.

Compare Off-Exchange PPO Plans Above 400% FPL

If you earn above the subsidy threshold ($62,600 for an individual using 2025 FPL), there’s no financial advantage to enrolling through the exchange — on-exchange and off-exchange plans from the same carrier cost the same. Off-exchange PPO plans from Blue Cross of Idaho, Regence Blue Shield, and SelectHealth offer broader provider networks and out-of-network coverage. For rural Idaho residents or those who travel frequently, the added flexibility of a PPO is worth comparing against HMO savings. See Idaho PPO vs. HMO costs and carrier comparisons →

Check Idaho Medicaid Before Shopping the Marketplace

Idaho expanded Medicaid effective January 1, 2020 after voters approved Proposition 2 by 61% in the November 2018 election. Adults with household income up to 138% FPL ($22,025 for an individual, $45,540 for a family of four using 2026 FPL) qualify for free or very low-cost coverage. As of October 2025, approximately 312,807 people were enrolled in Idaho Medicaid and CHIP. Enrollment is year-round — there’s no open enrollment period for Medicaid. Apply at idalink.idaho.gov or call 877-456-1233. If your income is close to the Medicaid cutoff, the Covered Choice waiver amendment — submitted by Idaho on January 30, 2026 — could let residents at 100%–138% FPL choose between Medicaid and a marketplace subsidy starting January 1, 2027 if approved. Learn more about Idaho Medicaid and the Covered Choice proposal →

Cheapest Idaho Health Insurance by Carrier for 2026

Eight carriers offer affordable Idaho health insurance through Your Health Idaho — Blue Cross of Idaho, Regence Blue Shield, SelectHealth, Mountain Health CO-OP, Molina, Moda, PacificSource, and St. Luke’s. The cheapest option depends on your county, age, and preferred plan type. St. Luke’s Health Plan offers the lowest Bronze premiums statewide ($349/month for age 40), Blue Cross of Idaho has the cheapest Silver plans in many areas, and Molina offers the most affordable Gold plans (~$548/month).

| Carrier | Cheapest Bronze (Age 40) | Silver Avg (Age 40) | Plan Type |

|---|---|---|---|

| St. Luke’s Health Plan | $349/month | $553/month | HMO |

| Regence Blue Shield | $380/month | $503/month | POS/PPO |

| Moda Health Plan | $382/month | $565/month | POS |

| Blue Cross of Idaho | $385/month | $412–$565/month | PPO |

| SelectHealth | $384/month | $552/month | PPO/HMO |

| Molina Healthcare | $395/month | $520/month | HMO |

| Mountain Health CO-OP | $390/month | $510/month | HMO |

| PacificSource | $398/month | $530/month | POS |

Blue Cross of Idaho deserves special attention for affordable Idaho health insurance because it’s the only carrier serving all 44 counties. In rural counties where carrier choice is limited to two or three options, Blue Cross is often one of them — and their Silver plans start as low as $412/month in some areas. Their statewide PPO network covers 96% of Idaho physicians, which means fewer surprise out-of-network bills. NCQA’s Health Plan Report Cards provide independent quality ratings that can help compare carriers beyond price alone.

How the Enhanced Subsidy Expiration Affects Idaho Costs

The expiration of enhanced premium tax credits on December 31, 2025 is the single largest cost change for Idaho marketplace enrollees in 2026. An estimated 87% of Your Health Idaho’s roughly 117,000 enrollees were receiving enhanced credits averaging $407/month per KFF. Without them, average net premiums increased significantly. Your Health Idaho reported approximately 24,400 disenrollments in early 2026, with officials projecting up to 30,000 more uninsured Idahoans this year due to affordability.

The impact varies dramatically by income. Households between 100% and 150% FPL ($15,650–$23,475 for an individual) see the smallest increase because Idaho allocated state resources to soften the blow for the lowest-income enrollees. Households between 300% and 400% FPL see moderate increases. But households above 400% FPL ($62,600 for an individual) lost subsidy eligibility entirely — for a family of four earning $130,000, annual premiums increased by approximately $10,831 according to estimates from Your Health Idaho.

One behavioral shift is worth noting: for 2026, nearly 60% of Idaho marketplace enrollees chose Bronze plans — up significantly from prior years when Silver and Gold were more popular. Many Idahoans who could no longer afford Silver premiums after the subsidy reduction downgraded to Bronze to keep monthly costs manageable. While affordable health insurance in Idaho is still available at the Bronze tier, those plans carry higher deductibles ($7,000–$10,000) that leave enrollees exposed to large out-of-pocket costs if they need significant medical care.

Affordable Idaho Health Insurance: Common Questions Answered

The most common questions about affordable Idaho health insurance for 2026 cover the cheapest carriers (St. Luke’s at $349/month Bronze, Blue Cross of Idaho at $412/month Silver), subsidy eligibility ranges (100–400% FPL, $15,650–$62,600 for an individual using 2025 FPL), Bronze vs. Silver tradeoffs, why Idaho premiums are lower (the 18% reinsurance reduction), family costs, and how to qualify for free coverage through Idaho Medicaid (138% FPL, about $22,025 for a single adult).

What is the cheapest health insurance in Idaho for 2026?

The cheapest Bronze plan in Idaho is from St. Luke’s Health Plan at approximately $349/month for a 40-year-old, but it’s only available in Treasure Valley and Magic Valley counties. Statewide, Regence Blue Shield offers the cheapest Bronze at $380/month. For Silver plans, Blue Cross of Idaho starts at $412/month in some areas. If you qualify for a premium tax credit through Your Health Idaho, your actual cost will be lower — many enrollees pay under $200/month after subsidies (the 87% subsidy receipt rate, with KFF reporting an average $407/month tax credit in 2025).

Do I qualify for health insurance subsidies in Idaho?

For 2026, premium tax credits through Your Health Idaho are available to households earning between 100% and 400% of the federal poverty level. That’s $15,650–$62,600 for an individual, or $32,150–$128,600 for a family of four (using 2025 FPL for 2026 marketplace eligibility). If you earn below 138% FPL ($22,025 individual using 2026 FPL), you likely qualify for Idaho Medicaid instead, which is free or very low cost. Apply year-round at idalink.idaho.gov.

Is a Bronze or Silver plan a better deal in Idaho?

It depends on your income and how much healthcare you use. If you earn below 250% FPL ($39,125 for an individual using 2025 FPL), Silver plans with cost-sharing reductions are almost always the better value — you get lower deductibles and copays at no extra premium cost. If you rarely need care and earn above the CSR threshold, Bronze plans save money monthly and now qualify for HSAs in Idaho for 2026. About 47% of Your Health Idaho Silver enrollees qualified for CSR in 2025. Run the numbers for your situation with a free quote to compare total annual costs, not just monthly premiums.

Why is health insurance cheaper in Idaho than other states?

Idaho runs a state reinsurance program (1332 waiver, approved by HHS on August 16, 2022) that reduces individual market premiums by approximately 18% for 2026. The program covers a portion of the most expensive medical claims so those costs don’t get passed to every policyholder. Idaho is one of 17 states with a 1332 reinsurance waiver, but Idaho’s hybrid approach — covering both high-cost claims and specific medical conditions — is used by only Idaho and Alaska, and has delivered consistent double-digit savings since 2023. The 2026 average rate increase of 10% is less than half the national average, largely because of this program.

How much does a family pay for health insurance in Idaho?

Family premiums depend on the number of family members, their ages, and the plan selected. As a rough benchmark, a family of four with two 40-year-old adults and two children can expect Bronze premiums starting around $1,000–$1,200/month before subsidies. Families earning up to 400% FPL ($128,600 for a family of four using 2025 FPL) may qualify for premium tax credits that significantly reduce this cost. Families below 138% FPL ($45,540 for four using 2026 FPL) likely qualify for Idaho Medicaid. Children under 19 may qualify for CHIP at income levels up to 190% FPL. See Idaho family coverage options →

Can I get health insurance in Idaho for free?

Yes, in two ways. First, Idaho Medicaid provides free or near-free coverage for residents earning below 138% FPL ($22,025 for an individual using 2026 FPL). Second, some marketplace enrollees with premium tax credits large enough to cover their entire monthly premium can get a $0-premium Bronze plan through Your Health Idaho. According to HealthCare.gov’s lower-costs guide, many uninsured residents who qualify for marketplace coverage could get a Bronze plan for $0/month after subsidies. Check your eligibility at yourhealthidaho.org.

Idaho Health Insurance Resources

Find the Most Affordable Idaho Health Insurance Plan

Licensed agents from ForHealthInsurance.com compare plans from all 8 Your Health Idaho carriers — Blue Cross of Idaho, Regence, SelectHealth, Mountain Health CO-OP, Molina, Moda, PacificSource, and St. Luke’s — with your subsidy applied, at no extra cost. Free help at 888-215-4045 or 855-944-3246 (Your Health Idaho).

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Idaho residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.