Affordable Health Insurance in Maine: Low-Cost 2026 Plans & Subsidies

Finding affordable health insurance in Maine got harder in 2026 after enhanced federal subsidies expired and carriers raised rates by an average of 23.9%. But most Mainers can still find coverage for under $200 per month through CoverME.gov — and some qualify for free coverage through MaineCare. This guide covers every path to lower-cost coverage in the state, from premium tax credits to cost-sharing reductions to the cheapest carrier options by county.

What’s your budget situation?

Premium Tax Credits for Affordable Health Insurance in Maine

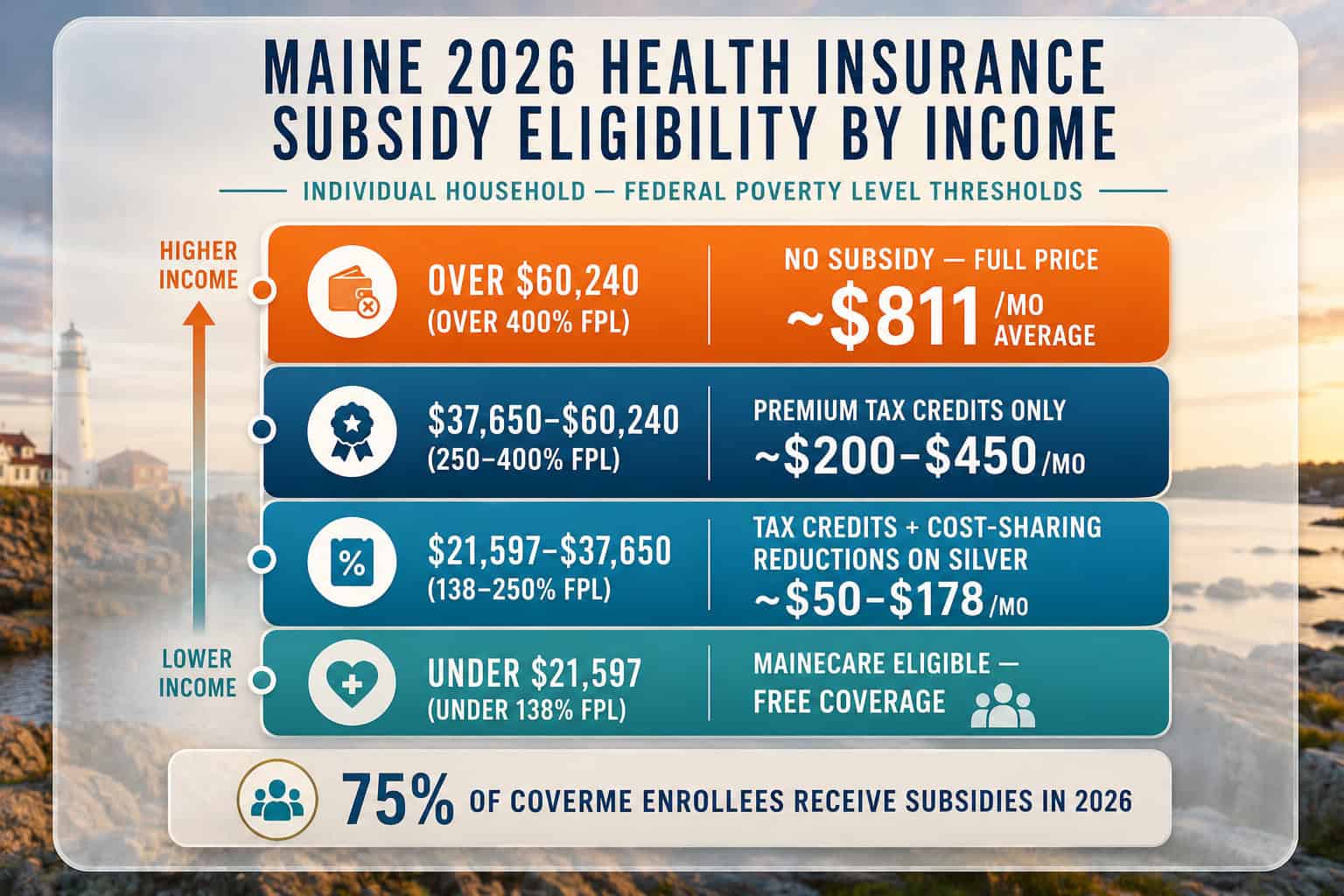

Premium tax credits reduce the monthly cost of CoverME.gov plans for Maine households earning between 100% and 400% of the Federal Poverty Level — approximately $15,060 to $60,240 for an individual in 2026. In 2026, 75% of CoverME enrollees receive credits averaging $772 per month, which lowers the average net premium to $178. Without subsidies, the average monthly premium for this group would be $913.

The expiration of Enhanced Premium Tax Credits at the end of 2025 is the single biggest change to affordable health insurance in Maine for 2026. These enhanced credits, in place since 2021, had expanded eligibility above 400% FPL and capped premiums at 8.5% of income for all earners. Without them, households above 400% FPL ($60,240 for an individual) receive no subsidy at all, and households between 300% and 400% FPL see reduced assistance. More than 3,000 CoverME enrollees who received tax credits in 2025 no longer qualify in 2026.

For those who still qualify, premium tax credits work by capping the expected premium contribution as a percentage of household income. At 150% FPL (approximately $22,590 for an individual), the expected contribution is roughly 4% of income — about $75/month. At 250% FPL ($37,650), it rises to approximately 8% — about $251/month. The credit covers the gap between this expected amount and the cost of the second-lowest-cost Silver plan in your county. Choosing a plan priced below the benchmark can result in monthly costs well under the expected contribution — including $0/month in some cases.

| Income (Individual) | % of FPL | Expected Premium | Est. Monthly Subsidy | Approx. Net Cost (Silver) |

|---|---|---|---|---|

| $15,060 | 100% | ~$0/month | ~$770+ | $0–$10/month |

| $22,590 | 150% | ~$75/month | ~$695 | ~$75/month |

| $30,120 | 200% | ~$170/month | ~$600 | ~$170/month |

| $37,650 | 250% | ~$251/month | ~$520 | ~$251/month |

| $45,180 | 300% | ~$345/month | ~$425 | ~$345/month |

| $60,240 | 400% | ~$505/month | ~$265 | ~$505/month |

| Over $60,240 | 400%+ | Full price | $0 | ~$771/month (Silver avg) |

Example: Home Health Aide in Kennebec County

A 45-year-old home health aide in Augusta earning $28,000 per year (approximately 186% FPL) qualifies for roughly $650/month in premium tax credits plus Silver cost-sharing reductions on CoverME.gov. An Anthem Silver Clear Choice plan with a full-price premium of $800/month costs her approximately $150/month after subsidies — with a reduced deductible of approximately $1,200 instead of the standard $4,500 Silver deductible. Her annual out-of-pocket maximum is also reduced from $8,700 to approximately $3,000 thanks to CSRs.

Cost-Sharing Reductions: The Hidden Value of Silver Plans in Maine

Cost-sharing reductions (CSRs) lower deductibles, copays, and out-of-pocket maximums on Silver plans purchased through CoverME.gov — without increasing the monthly premium. CSRs are available to Maine households earning between 100% and 250% of FPL (up to approximately $37,650 for an individual). During the 2025 enrollment period, more than one in four CoverME enrollees qualified for CSRs. At the lowest income levels, a Silver plan with CSRs functions like a Platinum plan at a Bronze price.

CSRs are the most underutilized tool for finding affordable health insurance in Maine. Nearly half of subsidized CoverME enrollees chose Bronze plans for 2026 — attracted by lower monthly premiums — but many of those enrollees earn under 250% FPL and would have paid less overall with a Silver plan enhanced by cost-sharing reductions. The math works like this: a standard Bronze plan has a deductible of $7,000–$9,200, meaning you pay thousands before insurance covers anything beyond preventive care. A Silver plan with CSRs at 150% FPL might have a deductible of $800–$1,200 — and the monthly premium after subsidies may be comparable to or even lower than the Bronze premium.

| Income Level | Standard Silver Deductible | Silver with CSR Deductible | Standard OOP Max | CSR OOP Max |

|---|---|---|---|---|

| 100–150% FPL | ~$4,500 | ~$800 | $8,700 | ~$2,800 |

| 150–200% FPL | ~$4,500 | ~$1,200 | $8,700 | ~$3,000 |

| 200–250% FPL | ~$4,500 | ~$2,500 | $8,700 | ~$6,500 |

CSR + Clear Choice advantage

Because Maine requires Clear Choice standardized plan designs, the CSR-enhanced deductible and copay schedule is identical across all carriers at a given income level. You get the same CSR benefit whether you choose Anthem, Harvard Pilgrim, CHO, or Mending — the only difference is the carrier’s network and monthly premium. This makes comparing affordable options straightforward: pick the cheapest Silver plan from a carrier whose network covers your doctors.

Check Your Subsidy Eligibility in Maine

See your estimated premium tax credits and cost-sharing reductions on CoverME.gov. Compare after-subsidy prices from Anthem, Harvard Pilgrim, CHO, and Mending.

Cheapest Health Insurance Plans in Maine for 2026

Anthem offers the cheapest health insurance in Maine for most residents, with the lowest Silver premiums in approximately 80% of counties — starting at about $660/month for a 40-year-old before subsidies in Cumberland County. Bronze plans from Anthem start at approximately $557/month. For subsidized enrollees under 200% FPL, Anthem Silver plans often cost $0–$100/month after tax credits. Harvard Pilgrim offers the cheapest plans in approximately 20% of counties, with Silver premiums starting around $755/month.

After subsidies, the cheapest path depends on income. For households under 250% FPL, a Silver plan with cost-sharing reductions is almost always the best value — even if the monthly premium is slightly higher than Bronze, the dramatically lower deductible and out-of-pocket maximum save money when you actually use care. For households between 250% and 400% FPL who don’t qualify for CSRs, Bronze may be the right choice if the goal is catastrophic protection at the lowest monthly cost. For households above 400% FPL paying full price, the cheapest option is an Anthem Bronze at approximately $557/month — though Mending’s direct primary care model may offer better value for residents who use primary care frequently. For a carrier-by-carrier breakdown of networks and ratings, the best Maine carriers guide compares all four on more than price alone.

Income under $37,650 (under 250% FPL)

Silver with CSR is your best path to affordable health insurance in Maine. Deductible drops from $4,500 to as low as $800. Monthly premium after subsidies: $0–$250 depending on income. Choose the cheapest Silver carrier in your county (typically Anthem).

Income $37,650–$60,240 (250–400% FPL)

Premium tax credits available but no CSR. Bronze ($557/mo average) or Silver ($771/mo average) — choose based on how often you use care. After subsidies, expect $200–$505/month depending on income. Compare Anthem and Harvard Pilgrim in your county.

MaineCare: Free Health Coverage for Low-Income Mainers

MaineCare — Maine’s Medicaid program — provides free health coverage to individuals earning up to 138% of the Federal Poverty Level, approximately $21,597 per year for a single adult in 2026. Families of four qualify with income up to approximately $44,000. Maine expanded Medicaid in 2019, and in 2023 further expanded eligibility for children and young adults under 21. MaineCare enrollment is year-round — there is no open enrollment restriction.

For Mainers whose income falls near the MaineCare threshold, the transition between MaineCare and CoverME marketplace coverage is a recurring pattern. Seasonal workers — lobster harvesters along the midcoast, tourism workers in the Acadia region, blueberry rakers in Washington County, and ski industry employees in Oxford and Franklin counties — may cycle between MaineCare during low-income months and subsidized marketplace plans during peak earning season. CoverME.gov provides a dedicated “Recently Lost MaineCare” special enrollment period to prevent coverage gaps during these transitions.

Residents who earn just above the MaineCare threshold (138% FPL, about $21,597) receive the largest premium tax credits and strongest cost-sharing reductions on CoverME.gov — making this the most accessible path to affordable health insurance in Maine for low-income workers. A single adult earning $22,000 would pay approximately $50–$75/month for a Silver plan with a CSR-reduced deductible of roughly $800 — making the transition from free MaineCare to marketplace coverage as affordable as possible. The CoverME marketplace guide explains enrollment steps for MaineCare transitions.

Options for Unsubsidized Mainers Paying Full Price

Maine residents earning above 400% FPL ($60,240 for an individual) receive no premium tax credits in 2026 following the EPTC expiration. Approximately 22% of CoverME enrollees now pay more than $1,000/month, and nearly 40% pay over $500/month. The average unsubsidized premium is $811. For this group, finding affordable health insurance in Maine means comparing carriers aggressively, weighing plan-type tradeoffs, and evaluating whether an ICHRA or a health care sharing ministry fits.

For unsubsidized Mainers, the cheapest ACA-compliant option is typically an Anthem Bronze plan at approximately $557/month for a 40-year-old. Younger adults pay less — a 30-year-old might find Bronze plans around $440/month. Choosing an HMO over a PPO saves approximately $50–$100/month at the same metal tier. Off-exchange plans from Anthem, Harvard Pilgrim, and CHO are the same price as on-exchange plans (since there’s no subsidy involved), but buying off-exchange avoids the CoverME application process.

Self-employed Mainers paying full price can deduct 100% of premiums on their federal tax return using IRS Schedule 1, which effectively reduces the cost by their marginal tax rate — a 22% bracket taxpayer saves approximately $1,470/year on a $557/month Bronze plan. Health Savings Accounts (HSAs) are available with Bronze and some Silver plans that qualify as high-deductible health plans, allowing pre-tax contributions of up to $4,300 for individual coverage in 2026. For freelancers, gig workers, and small-business owners without group coverage, buying an individual plan directly — on or off the CoverME exchange — is usually the most affordable route, and pairing a Bronze HDHP with an HSA is the single biggest cost lever available to a healthy self-employed Mainer.

Affordability pressure in 2026: During the 2026 open enrollment period, more than 8,000 CoverME consumers canceled coverage — with approximately 33% citing affordability as the reason. The full enrollment impact may not appear until later in 2026, as consumers with subsidies have a three-month grace period before carriers can terminate for non-payment. If you’re considering dropping coverage due to cost, a licensed enrollment assistant can run subsidy calculations to see if less expensive options exist.

Five Strategies for Lowering Health Insurance Costs in Maine

Finding affordable health insurance in Maine comes down to five key strategies: choosing Silver with CSRs if income qualifies (under 250% FPL), selecting the cheapest carrier in your county (Anthem in ~80% of counties), using the self-employed premium deduction, contributing to an HSA with a high-deductible plan, and reviewing plan options annually — the cheapest carrier and benchmark plan change each year as rates adjust.

Choose Silver with CSRs if you qualify

If your income is under 250% FPL ($37,650 individual), a Silver plan with cost-sharing reductions will almost always save you more than Bronze over the course of a year. The reduced deductible ($800–$2,500 vs. $7,000+) means you reach the point where insurance pays faster — even if the monthly premium is slightly higher.

Compare carriers in your county every year

Rate increases vary by carrier — Anthem raised rates 20.3% for 2026 while Mending raised 32.2%. The cheapest carrier in your county can change year to year. CoverME’s Plan Comparison Tool shows after-subsidy prices sorted by cost. In 2026, Anthem is cheapest in ~80% of counties and Harvard Pilgrim in ~20%.

Use the self-employed premium deduction

Self-employed Mainers — approximately 82,000 residents, or 12% of the workforce — can deduct 100% of health insurance premiums on their federal tax return. At a 22% marginal rate, that’s $1,470/year saved on a $557/month Bronze plan. This deduction applies whether you buy on or off CoverME.gov.

Open an HSA with a qualifying high-deductible plan

Health Savings Accounts let you save pre-tax dollars — up to $4,300 for individual coverage in 2026 — for medical expenses. Contributions reduce taxable income, growth is tax-free, and withdrawals for qualified medical expenses are untaxed. Most Bronze plans and some Silver plans on CoverME qualify as high-deductible health plans for HSA purposes.

Don’t auto-renew without shopping

CoverME automatically re-enrolls you in your current plan if you take no action during open enrollment. But with 23.9% average rate increases for 2026, the plan that was cheapest last year may not be cheapest now. A Harvard Pilgrim plan that beat Anthem in 2025 may cost $80/month more than Anthem in 2026. Always shop and compare before the deadline.

Frequently Asked Questions About Affordable Health Insurance in Maine

What is the cheapest health insurance in Maine for 2026?

Anthem offers the cheapest health insurance in Maine for most residents — with the lowest Silver premiums in approximately 80% of counties, starting at about $660/month for a 40-year-old before subsidies. Bronze plans from Anthem start at approximately $557/month. For subsidized enrollees earning under 200% FPL, Anthem Silver plans on CoverME.gov often cost $0–$100/month after tax credits. Harvard Pilgrim is cheapest in approximately 20% of Maine counties.

Can I still get subsidies on CoverME.gov after the EPTC expiration?

Yes — 75% of CoverME.gov enrollees still receive premium tax credits in 2026. The Enhanced Premium Tax Credits expired at the end of 2025, which eliminated subsidies for households above 400% FPL ($60,240 for an individual) and reduced them for some higher-income households. But the standard ACA premium tax credits remain available for incomes between 100% and 400% FPL. The average subsidy in 2026 is $772/month, and the average net premium for subsidized enrollees is $178/month.

What are cost-sharing reductions and do I qualify?

Cost-sharing reductions (CSRs) lower your deductible, copays, and out-of-pocket maximum on Silver plans purchased through CoverME.gov — without increasing your monthly premium. You qualify if your household income is between 100% and 250% of FPL (up to approximately $37,650 for an individual). At the lowest income levels (100–150% FPL), CSRs can reduce a standard Silver deductible from $4,500 to approximately $800 and the out-of-pocket maximum from $8,700 to approximately $2,800.

Is MaineCare free? Who qualifies?

Yes — MaineCare is Maine’s Medicaid program and provides free health coverage. Individual adults qualify with income up to 138% of the Federal Poverty Level — approximately $21,597 in 2026. Families of four qualify with income up to approximately $44,000. Children and young adults under 21 have expanded eligibility since 2023. MaineCare enrollment is year-round with no open enrollment restriction. Apply through CoverME.gov or directly through the Maine DHHS.

Should I choose Bronze or Silver in Maine?

If your income is under 250% FPL ($37,650 for an individual), Silver with cost-sharing reductions is almost always the better value — even if the monthly premium is slightly higher than Bronze. A standard Bronze deductible is $7,000–$9,200, while a CSR-enhanced Silver deductible can be as low as $800. If your income is above 250% FPL and you rarely use medical care, Bronze provides the lowest monthly cost with catastrophic protection. Compare both options on CoverME.gov’s Plan Comparison Tool using your actual income.

What happened to the enhanced subsidies?

The Enhanced Premium Tax Credits (EPTCs), first introduced through the American Rescue Plan Act in 2021 and extended through the Inflation Reduction Act, expired at the end of 2025. These credits had expanded subsidy eligibility above 400% FPL and capped premiums at 8.5% of income for all earners. Without them, households above 400% FPL receive no subsidy, and some previously eligible households receive smaller credits. More than 3,000 CoverME enrollees who received subsidies in 2025 no longer qualify in 2026.

More Maine Health Insurance Guides

Maine’s CoverME.gov subsidies, MaineCare eligibility, and Clear Choice plan designs all shape what affordable coverage looks like. These guides cover the statewide overview, marketplace enrollment, small business and group options, and nationwide PPO plans for those who travel or work across state lines.

Plans, carriers, costs, and enrollment across the Pine Tree State.

CoverME.gov Marketplace & EnrollmentHow to enroll on Maine’s state exchange, deadlines, and life events.

Small Business & Group Plans in MaineGroup coverage, SHOP tax credits, and ICHRA options for employers.

Nationwide PPO Health InsuranceOut-of-network flexibility and broader provider access nationwide.

Find Affordable Health Insurance in Maine

Check your 2026 subsidy eligibility on CoverME.gov, compare after-subsidy prices from all four Maine carriers, and get free enrollment help.

Broker Disclosure

ForHealthInsurance.com is an independent health insurance agency serving Maine residents. We are not affiliated with any carrier or government agency. We help you compare plans and enroll in coverage that meets your needs at no extra cost to you.