Short-Term Health Insurance in Texas

Looking for a broader overview? Visit our Texas Health Insurance guide or explore private plans available in Texas.

What Is Short-Term Health Insurance?

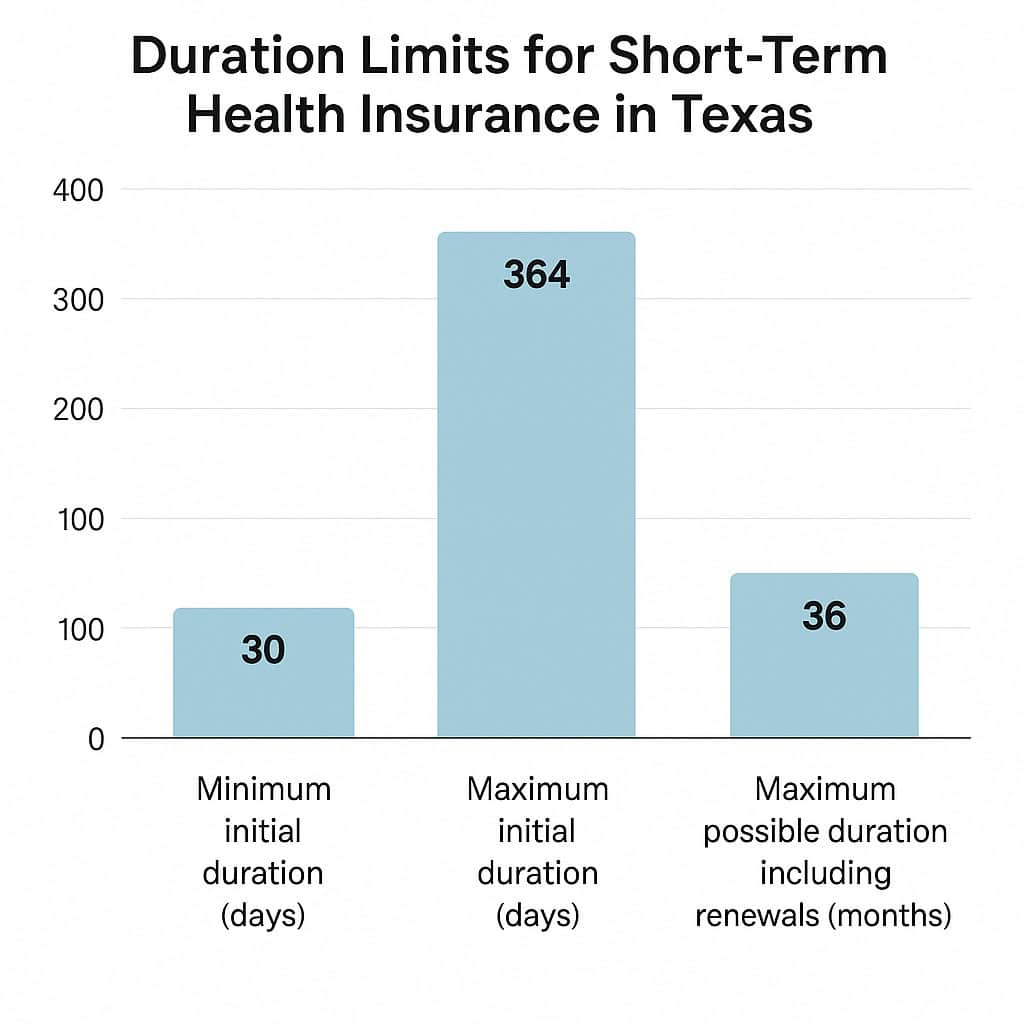

Short-term health insurance in Texas offers temporary coverage for people who are in between jobs, waiting for ACA enrollment, or need a quick solution for unexpected gaps. These plans typically last 30 to 364 days, with renewals allowed for up to 36 months, depending on the carrier.

Who Should Consider a Short-Term Plan in Texas?

- Texans who missed Open Enrollment

- Freelancers and gig workers without employer coverage

- College graduates and new job starters

- People in a waiting period for new employer coverage

- Recent transplants to Texas needing gap protection

How Do Short-Term Plans Work?

Short-term plans are medically underwritten, which means you may be denied for certain pre-existing conditions. They’re not ACA-compliant but are affordable alternatives when major medical coverage isn’t available.

- Fast approval (often same-day)

- Choose your deductible and coinsurance

- Limited preventive care, but covers emergencies and unexpected illnesses

Pros and Cons of Short-Term Insurance

| Pros | Cons |

|---|---|

| Low monthly premiums | No guaranteed issue or subsidies |

| Nationwide networks often included | Excludes pre-existing conditions |

| Flexible durations (1 to 12 months) | Limited coverage for prescriptions & preventive care |

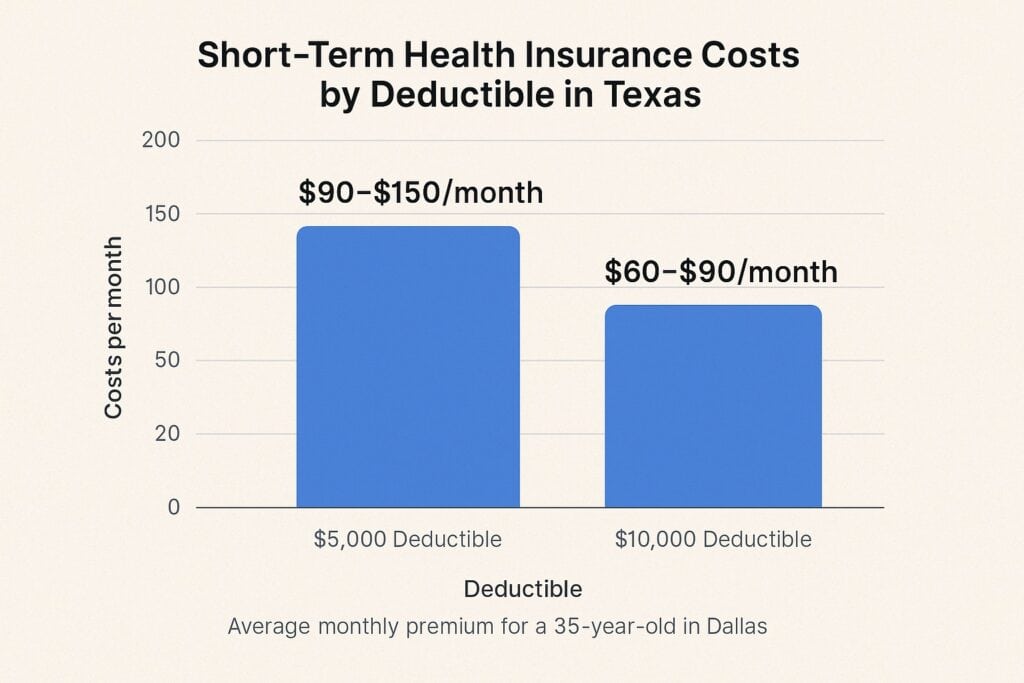

Cost of Short-Term Health Plans in Texas

Premiums vary based on age, ZIP code, deductible, and carrier. Below are average costs for a 35-year-old in Dallas:

- Plan with $5,000 deductible: $90–$150/month

- Plan with $10,000 deductible: $60–$90/month

When a Short-Term Plan May Not Be the Right Fit

- You qualify for an ACA Special Enrollment Period (SEP)

- You have pre-existing health conditions

- You need maternity care or mental health support

- You plan to use it long-term instead of full coverage

Real Story: Temporary Coverage During a Move

“When I relocated from Houston to El Paso, I had a two-month gap before my new job’s benefits kicked in. A short-term plan gave me peace of mind during the move, just in case something unexpected happened.” — Karla S., El Paso

Need Help Choosing a Short-Term Plan?

We help Texans find reliable short-term coverage options—without confusing fine print or hidden fees. Whether you need a 1-month bridge plan or coverage through the end of the year, our licensed brokers can walk you through the pros and cons.

FAQs About Short-Term Health Insurance in Texas

Can I renew a short-term plan in Texas?

Yes. Some carriers allow renewals up to 36 months, but coverage resets each term.

Does it cover prescriptions or doctor visits?

Some plans do, but not all. Check the specific benefit summary for limits.

Is it cheaper than ACA coverage?

Yes, in most cases—but short-term plans offer fewer benefits and less protection.

Can I cancel my plan early?

Yes. Most plans are month-to-month and allow cancellation at any time.

Short-Term Plans vs. ACA Marketplace Coverage

Many Texans weigh short-term health insurance against ACA marketplace plans. While ACA plans offer more comprehensive coverage and subsidies for low-income households, short-term plans fill specific needs for those who want fast, flexible options.

- Short-Term: Lower cost, faster enrollment, fewer benefits

- ACA: Higher cost, subsidy-eligible, includes all essential health benefits

Our team can help you compare both types to see what fits your health needs and budget best.

Common Situations Where Short-Term Coverage Helps

- Waiting out the 90-day period before employer coverage starts

- Recent college graduates who lost student health coverage

- Laid-off workers without COBRA access or who need cheaper options

- Seasonal workers or part-time employees without benefits

- Divorced or separated individuals who lost spousal coverage

How Long Can You Keep a Short-Term Plan in Texas?

In Texas, most short-term plans can be purchased for an initial period ranging from 30 to 364 days. Some carriers allow you to renew or reapply for coverage up to a maximum duration of 36 months. However, these renewals may reset your deductible and coverage limits each time.

This flexibility makes short-term plans useful for transitional periods, but they’re not a permanent solution. If you need consistent long-term coverage, consider ACA-compliant plans or employer-sponsored options.

Which Insurance Companies Offer Short-Term Plans in Texas?

For the self-employed, we also offer dedicated plans for freelancers and gig workers in Texas.

Several well-known carriers offer short-term medical plans in Texas. Availability may vary by ZIP code and age, but some of the most common include:

- UnitedHealthcare (Golden Rule): One of the largest providers, known for national networks and same-day coverage.

- Pivot Health: Offers customizable short-term coverage options with telemedicine add-ons.

- National General (Allstate): Competitive rates and various plan durations with added supplemental benefit options.

Each insurer has different underwriting rules and coverage exclusions, so it’s a good idea to compare side-by-side before applying. A broker can help you sort through the fine print and avoid unexpected gaps in coverage.

Important Caveats: What Short-Term Plans Don’t Cover

One of the biggest drawbacks of short-term health insurance is that these plans are not required to meet the Affordable Care Act’s (ACA) standards. That means they typically do not include the 10 essential health benefits mandated by ACA-compliant plans.

These missing benefits can include:

- Maternity and newborn care

- Mental health and substance use services

- Prescription drug coverage

- Preventive services like annual checkups or screenings

- Rehabilitative services

Because short-term plans are medically underwritten and offer fewer protections, they are much more affordable than ACA plans—but they also come with higher financial risk if you end up needing services not included in the policy. Always read the fine print or talk with a licensed broker to make sure the coverage fits your real-world needs.

Related Texas Health Insurance Guides

- Texas Health Insurance (Pillar Page)

- Private Health Insurance in Texas

- Cheap Health Insurance in Texas

Your Texas Short-Term Insurance Resource

If you’re still deciding, check out our rankings for the best health insurance in Texas to compare top-rated options.

We specialize in helping Texans bridge coverage gaps with short-term medical insurance that fits their budget and timeline. Whether you’re between jobs, moving, or just need something fast, we’ve got you covered. Reach out today to speak with a licensed broker who can walk you through all your options.